Fed Watch: Dissent - The FOMC statement contained a mini-bombshell, the dissent of Kansas City Fed President Thomas Hoenig. I am skeptical, however, that this dissent is a significant shift in the policy environment. Instead, I view the statement as taking another baby step forward to a normalization of monetary policy now that the financial crisis has eased and that the economic environment has firmed. Many policymakers will simply find themselves increasingly uncomfortable holding rates at rock bottom levels while sitting on a bloated balance sheet -- regardless of the unemployment rate. Short of a significant reversal of recent economic gains, I would be hard pressed to see the Fed back away from a policy stance that is growing tighter, albeit slowly tighter.

Fed Keeps ‘Extended Period’ Pledge; Hoenig Dissents (Bloomberg) -- The Federal Reserve restated its intention to cease buying $1.25 trillion of mortgage-backed securities in March and maintained its pledge to keep interest rates near zero for an “extended period,” opening a rift among policy makers for the first time in a year. Kansas City Fed President Thomas Hoenig dissented, saying the time had come to change the promise to keep rates low. The economy “has continued to strengthen,” the Fed said in a statement today in Washington, “although the pace of economic recovery is likely to be moderate for a time.”

And Now for Something Completely Different: FOMC Edition Inflation Hawk Admitted to the FOMC's Deflation Henhouse - The Federal Reserve Open Market Committee meeting concluded Wednesday and issued its traditional 2:15pm EST statement, with an interesting, but opaque, notation in the voting footnotes from newly elevated (for 2010) first-stringer Thomas M. Hoenig, President of the Federal Reserve Bank of Kansas City, who voted against the Committee's monetary policy action, based on his belief "that economic and financial conditions had changed sufficiently that the expectation of exceptionally low levels of the federal funds rate for an extended period was no longer warranted":

Fed Lays Ground for End to Stimulus With Recovery Declaration - The Federal Reserve panel in charge of interest rates declared for the first time the U.S. economy is in “recovery” and took several steps to prepare investors for the removal of aggressive monetary stimulus. The Federal Open Market Committee yesterday upgraded its economic outlook, reaffirmed it will end liquidity backstops and a $1.25 trillion program to buy mortgage-backed securities and expressed less confidence inflation will remain “subdued.” “This is as close an admission that we are likely to see that the FOMC thinks the recession is over and the economy is on a self-sustaining recovery path,”

Kansas City’s Hoenig Wants Fed to Find New Words - The Federal Reserve’s first Federal Open Market Committee meeting of 2010 brought a new voting lineup among regional Federal Reserve bank presidents. One hawkish president took the place of another hawk, and the transition appears to have been seamless — bringing a dissenting vote to the committee for the first time in a year.The FOMC voted 9-1 to keep its interest-rate target unchanged at near zero and maintain its language that economic conditions “are likely to warrant exceptionally low levels of the federal funds rate for an extended period.” That wording has remained in the FOMC’s post-meeting statement since last March. The lone dissenter, Kansas City Fed President Thomas Hoenig, “believed that economic and financial conditions had changed sufficiently that the expectation of exceptionally low levels of the federal funds rate for an extended period was no longer warranted,” the statement said.

Hoenig the hawk - As expected, the Fed’s zero rate strategy holds for now, but for the first time in a year there was a dissenting voter: Thomas M. Hoenig… FOMC Statement (our emphasis):

Meltzer on the Fed's Incomplete Exit Strategy- I commend Allan Meltzer's op-ed in yesterday's Wall St. Journal. Meltzer writes: The exit strategy is incomplete. Proponents are guilty of practicing economics without prices. They never say what the interest rate on reserves must be to get banks to hold the approximately $1 trillion of reserves above the minimum they're legally required to hold. That's the critical question. [...] No economist doubts that the Fed can induce banks to hold some more reserves by paying interest. But how much? I do have to say that Meltzer's critique, like Bernanke's strategy, is also somewhat incomplete. What might stop the Fed from raising the interest rate on reserves as high as necessary? He doesn't spell that out

Fed’s Kohn: Banks Need to Prepare for Higher Rates - The Federal Reserve’s number-two official issued a stern warning to investors, banks and other financial institutions Friday: Don’t be complacent, interest rates are going up at some point and it will cause new market turmoil if you’re not prepared. “We are in uncharted waters for monetary policy and the financial markets,” Donald Kohn, vice chairman of the Federal Reserve, said in a speech to bankers at the FDIC. Rattling off a long list of uncertainties about the outlook – a rising budget deficit, foreign demand for U.S. debt, the strength of the recovery – Mr. Kohn said bankers need to start preparing now for the risk that interest rates could move swiftly in unexpected directions, most likely up.“Many banks, thrifts, and credit unions may be exposed to an eventual increase in short-term interest rates,” he warned

"No rate hikes likely in 2010..." According to Bloomberg's latest survey of 57 economists the U.S. economy is expected to grow by 2.7% in 2010 and 2.9% in 2011 Indeed, judging by expectations of the future course of U.S. short-term interest rates, the market appears to believe that the U.S. recovery will prove to be stronger than a typical post-crisis recovery. Expectations for higher short-term interest rates are reflected both in the Fed Funds futures market and in the consensus interest-rate projections of leading economists While it is certainly the case that the Fed will eventually have to push its policy rate higher, there is reason to believe that the policy-rate path predicted in Figure 4 might be overly aggressive. Indeed, as we demonstrate below, the market's projection for Fed rate hikes is not consistent with the path forecasted by conventional Taylor Rule models. If we input the Federal Reserve's forecasts for core inflation and unemployment into a variety of Taylor Rule-type models, we actually end up with a zero or negative Fed Funds rate projected for all of 2010 and, in a number of cases, for 2011 as well.

The One Sentence Everyone Needs to Read and Understand - Bruce Bartlett: The Fed has talked openly about new procedures to soak up the bank reserves it has created even as those reserves remain largely idle and unlent. You don't get inflation if there is no money multiplier in play. So long as the banks are just holding the cash, worries about monetary policy leading to inflation are at best a shibboleth.

Fed Weighs Interest on Reserves as New Benchmark Rate (Bloomberg) -- Federal Reserve policy makers are considering adopting a new benchmark interest rate to replace the one they’ve used for the last two decades. The central bank has been unable to control the federal funds rate since the September 2008 bankruptcy of Lehman Brothers Holdings Inc., when it began flooding financial markets with $1 trillion to prevent the economy from collapsing. Officials, who start a two-day meeting today, have said they may replace or supplement the fed funds rate with interest paid on excess bank reserves. “One option you might want to consider is that our policy rate is the interest rate on excess reserves and we let the fed funds rate trade with some spread to that,” Richmond Fed President Jeffrey Lacker told reporters.

Why are 86% of the NY Fed’s MBS Purchases Occurring During Option Expiration Weeks? - This data suggests that the Fed's purchases of Market Backed Securities serves not only to artificially depress mortgage rates and the longer end of the yield curves. The purchases occur, with a remarkably high correlation of 86%, during monthly stock market options expiration weeks in the US. "...since July, there has only been one options expiration week whereby the Fed did not buy at least $60 billion of MBS during the options expiration week itself, providing instant and meaningful liquidity during options expiration weeks that have historically had an upward bias anyway! Talk about timing of liquidity injections to get maximum effect in the equities market."

Bernanke’s (new) Conundrum – Negative Convexity - The Atlanta Fed put out a report on the status of the Fed's purchases of MBS. The report confirms that 91% of the anticipated $1.25 Trillion of paper has been bought. This leaves about $110b of buying power left for the Fed. There is only nine weeks left until the anticipated time that this program will end. This implies an average of only $10b of intervention per week. The most recent purchase was for $16B. Look for that weekly number to fall pretty quickly from now on. The following graph clearly shows the STEADY accumulation of Agency paper. Now look at the following graph. If you print this out and check with a ruler (I did) you will see that the lowest point on the brown shaded area is 1,200 and the upper band is at 2,400 (1,200 total). The legend states that brown are both Agency Bonds and MBS. As a portion of all long term mortgages pre-pay prior to the stated maturity...

Central banks, debt and deflation - The Economist - WHY are central banks so scared of deflation? The reason, of course, was that banks were worried about repeating the Japanese experience of deflationary stagnation. Irving Fisher described this as the "deft deflation trap"; incomes fall but the debts remain the same in nominal terms and rise in real terms, making them harder to service. This debt trap is what persuaded central banks to cut rates to zero, use quantiative easing and pursue many other support schemes over the last couple of years. In short, if we had not got so indebted, the central banks would have not had to intervene. But of course, you should turn this round. If central banks had not intervened so often in the 1980s, 1990s and noughties, we would not have got so indebted.

Thoughts on the End Game - Over the next several months, we are going to start to explore various aspects of the end game. Whither Japan? Are they actually, as I think, a bug in search of a windshield? What does that mean for the world? How safe is the euro? Everyone over here seems to think Germany will bail out Greece. A breakup seems unthinkable to the people I've been talking to (so far). But what about Spain? Italy? Can you spell moral hazard?The Fed has said it will exit quantitative easing (QE) at the end of March. But what if mortgage rates rise? Where do we find $1 trillion (plus!!!) in US savings to fund the deficit, assuming foreigners buy about $400 billion? By definition, savings and foreign investment and the federal deficit must add up to zero. (We will go into that later - just take it as gospel for now.) How can we run 10% of GDP deficits if the Fed does not print money (as they did by buying Fannie and Freddie paper, which became treasuries, as I outlined last week)? That would require almost a 10% savings rate - with it all ending up in treasuries. How can that happen?

The Fed's Anti-Inflation Exit Strategy Will Fail -Federal Reserve Chairman Ben Bernanke has explained his exit strategy to prevent future inflation. The Fed recently began to pay interest to banks on the reserves they hold in their vaults. Using this new tool, it claims the ability to get banks to keep the money instead of lending it out, thus containing the money supply and inflation.I don't believe this will work, and no one else should. The exit strategy is incomplete. Proponents are guilty of practicing economics without prices. They never say what the interest rate on reserves must be to get banks to hold the approximately $1 trillion of reserves above the minimum they're legally required to hold. That's the critical question.

Issues Versus People - Paul Krugman Blog - NYTimes - Scott Sumner argues that we should be debating the substance of monetary policy, rather than whether Ben Bernanke should be reappointed. I wish it were that simple. Of course the underlying issues involve monetary policy. But the Senate doesn’t get a direct vote on that; the only vote it gets is on whether to approve a Fed nominee. And Senators are looking to economic analysts for guidance on that actual vote. Nor is it necessarily the case, as Sumner suggests, that the Obama administration chose Bernanke because it favors the policies it believes he will follow. Again, it’s not that simple: administration’s choose Fed chairs to appease markets, or to avoid a fight with the other party, or because they think it will look good on TV.

Excess Reserves - If you want a nice, concrete example of something the Fed could be doing to boost employment, look no further than this article on excess reserves (via): Banks’ excess reserves, or deposits held with the Fed above required amounts, totaled $1 trillion in the two weeks ended Jan. 13, compared with $2.2 billion at the start of 2007. The Fed created the reserves through emergency loans and a $1.7 trillion purchase program of mortgage-backed securities, federal agency and Treasury debt.By raising the deposit rate, now at 0.25 percent, officials reckon banks will keep money at the Fed and not stoke inflation by lending out too much as the economy recovers. People have wondered for a while what’s the Fed’s “exit strategy” from the current bout of credit easing, and there you have it.

Economists React: Should Bernanke Stay at the Fed? - WSJ - (a dozen) Journalists, economists, bloggers and others weigh in on the troubles facing Ben Bernanke’s confirmation as Fed chairman.

Why Bernanke should be reconfirmed – Econbrowser - readers are well aware that there are a number of issues on which I have concerns about some of the decisions the Fed has made, such as dropping the ball on regulation ([1], [2]), keeping interest rates too low for too long over 2003-2005 ([1], [2]), taking some real risks with the Fed's new balance sheet ([1], [2], [3]), and pretending the Fed had nothing to do with the commodity price boom of 2008 ([1], [2]). Notwithstanding, there is no question in my mind that Bernanke should be reconfirmed as Chair of the Federal Reserve Board. Here's why.

The Internet's Chief Bernanke Apologist Officer Speaks! - DeLong - The internet's Chief Bernanke Apologist Officer? That's me. And I guess I have to speak because Paul Krugman is "agonizing" over the Ben Bernanke question. Paul writes: The Bernanke Conundrum: I’m agonizing — which isn’t a place I ever expected to be, and not just because Bernanke hired me at Princeton... And he issues the first count in his bill of indictment: [Bernanke] completely failed to see the trouble building as the housing bubble inflated — and no, it wasn’t one of those things nobody could have predicted, since a lot of reputable economists were warning almost frantically about the bubble. Bernanke’s failure to see what was right in front of his nose was shared by almost everyone at the Fed —... In rebuttal, let me say that my conversations with senior Federal Reserve officials in 2004-2006 appear to have been very different than those Paul Krugman had.

Bernanke Apologist Watch - Shorter [1] Jim Hamilton (via [2] Brad DeLong):Ben Bernanke's record leaves nine links' worth of things to be desired, but considering the zombie ex-Fed Chair alternatives (plus Brett Fav-Paul Volcker), he deserves to be confirmed for a second term.I am almost not kidding. Here's what Hamilton actually asks Bernanke's critics: I wonder which of [sic] previous Fed Chairs critics think would be better for the job than Bernanke. Surely you don't think we'd have been better off bringing Alan Greenspan back? [touché] G. William Miller [deceased] fumbled badly with much simpler problems. Arthur Burns [also deceased] is a case study in how not to conduct monetary policy.Would DeLong accept this sort of argument from a Berkeley undergrad seeking a decent grade? The question of far greater interest is why critics should have preferred Bernanke to prospective candidates who might have the combination of background and metabolic function to carry out the job — say, Janet Yellen or Alan Blinder — and might also do better than Bernanke in a pop quiz on the Fed's dual mission.

Why Bernanke should be reconfirmed - Jim Hamilton nails it. Excerpts:Please permit me to suggest that intellectual stamina is the most important quality we need in the Federal Reserve Chair right now. And: How could there possibly be an alternative whom Barbara Boxer (D-CA) and Jim DeMint (R-SC) would both prefer to Bernanke? Elsewhere I have to strongly differ with the Johnson-Kwak proposal that Paul Krugman be selected. The Fed Chair has to be an expert on building consensus and at maintaining more credibility than Congress; even when the Fed screws up you can't just dump this equilibrium in favor of Fed-bashing. Would Krugman gladly suffer the fools in Congress? Johnson and Kwak are overrating the technocratic aspects of the job (which largely fall upon the Fed staff anyway) and underrating the public relations and balance of power aspects.

The Fed’s Best Man - A SENATE vote on President Obama’s nomination of Ben Bernanke for a second four-year term as chairman of the Federal Reserve is imminent. Rejecting him would be a big mistake, for it would both flog a distinguished public servant who helped avert catastrophe and turn the Fed chairmanship into yet another political football. Washington has plenty of political footballs already.The case for Ben Bernanke starts with his keen intellect. But perhaps more important in these trying times, he has demonstrated great creativity. He has also displayed the courage to put his head on the chopping block for policies he thinks right. And he is now battle-tested. (Disclosure: I am a long-time friend and former academic colleague of Mr. Bernanke.)

Faux News on Fifteenth Street (i.e., the Washington Post) Endorses Bernanke - Given the bias in its news coverage it should hardly be a surprise that the Washington Post editorial board endorsed Ben Bernanke for another term as Fed chairman. Still, the arguments in its editorial are worth noting.To begin with, the title of the piece "scapegoat at the Fed," should give everyone a good laugh to start the week. Umm, isn't Mr Bernanke the Fed chairman and before he took over in 2006 one of the seven members of the Board of Governors? Isn't it the Fed's job to maintain full employment? Is 10 percent unemployment full employment? The fact is that Bernanke either failed to see or opted not to counteract an $8 trillion housing bubble. Any competent economist could see that the collapse of this bubble would wreck the economy. How can you possibly fail more completely in a job than Mr. Bernanke has?

The Quarrel Over Bernanke - NYTimes Forum - Though it appears that he will overcome a filibuster threat, opposition to Mr. Bernanke has grown, along with worsening jobs numbers and public anger over the Fed’s failure to regulate banks before the financial crisis. His Democratic and Republican opponents have criticized him as the architect of the Wall Street bailout and being out of touch with the woes of Main Street. How much is Mr. Bernanke to blame for the regulatory failures, the weak recovery and high unemployment numbers? Could a new Fed chairman make a difference?

- Robert Kuttner, The American Prospect

- Tyler Cowen, economist, George Mason University

- Yves Smith, financial analyst

- Mark Thoma, economist, University of Oregon

- Robert J. Barbera, economist, I.T.G.

Why Bernanke’s Confirmation Is, and Should Be, in Trouble - No sooner had the New York Times released an initial story that "Opposition Grows Against Second Term for Bernanke," noting opposition from Sens. Feingold and Boxer, than Sen. Harry Reid made a Friday evening announcement that he would support Bernanke. With presumed White House urging, Reid was hoping to head off further erosion in Bernanke’s support. But it may not be enough. One unconfirmed vote count late Friday suggested there were still up to 59 Senators undecided, with those supporting/opposing split about 25/16. That was before Reid’s announcement. The fact that over half the Senate doesn’t know what to do about Bernanke speaks volumes. For such an important position, and with so much already known about Bernanke’s record, you’d think Bernanke’s fate would be known by now

Why Bernanke Might Be Out by February - Fed Chairman Ben Bernanke may have read his political obituary this morning. Prized by the White House for battling the crisis but despised by Republicans and some liberal Democrats for his perceived Wall Street bias, Bernanke's reappointment never looked like a shoo-in. But the surprisingly sweeping fallout from Republican Scott Brown's election to Ted Kennedy's Senate seat on Tuesday seat continues with reports that Bernanke may now lack the votes. Could Congress boot Bernanke from the post that won him Time person of the year and Foreign Policy's thinker of the year? Should they? His term is up January 31

Is Bernanke Hiding A Smoking Gun? - A Republican senator said Tuesday that documents showing Federal Reserve Board Chairman Ben Bernake covered up the fact that his staff recommended he not bailout AIG are being kept from the public. And a House Republican charged that a whistleblower had alerted Congress to specific documents provide "troubling details" of Bernanke's role in the AIG bailout.Sen. Jim Bunning (R-Ky.), a Bernanke critic, said on CNBC that he has seen documents showing that Bernanke overruled such a recommendation. If that's the case, it raises questions about whether bailing out AIG was actually necessary, and what Bernanke's motives were. A letter Bunning sent Monday to Banking Committee Chairman Chris Dodd (D-Conn.) also refers to an "[e]mail exchange regarding restructuring of assistance to AIG, initiated by Treasury Secretary Timothy Geithner" in March 2009.

What if Bernanke Isn’t Reconfirmed - What happens if Ben Bernanke isn’t reconfirmed? Well, some folks seem to think it will send markets into a tailspin. But it’s worth emphasizing that in literal terms almost nothing will happen. If a left-right coalition of 40 Senators blocks his confirmation, then it’s hard to see what other candidate would be more to their liking. You’d have gridlock. But Bernanke’s term as a member of the Fed’s Board of Governors is actually a 14-year term that doesn’t expire for a long time. Consequently, the same Open Market Committee that’s making decisions right now would just go on making decisions. Bernanke would, however, be unable to perform the formal responsibilities of the Chairman, so that role would devolve to Donald Kohn, the Vice Chair. Would that be a ridiculous situation for an erstwhile major country with a functioning political system to find itself in?

Bernanke Reconciliation? – Krugman - I’ve come out, albeit without enthusiasm, in favor of reappointing Ben Bernanke. But this would send a terrible signal:When it comes to progressive priorities in the Senate, there’s one standard: 60 votes are needed. But for Ben Bernanke, there’s a second standard: 50 will be just fine, thank you.Democratic leaders in the Senate are asking colleagues who are reluctant to support Bernanke’s nomination for a second term as Federal Reserve chairman to nevertheless vote with them to end a filibuster and allow a vote on the actual nomination. The reluctant members would then be free to vote no to express their displeasure. I can hardly think of anything more calculated to solidify the view that Wall Street doesn’t have to play by the rules that apply to everyone else.

Know Your Feds - Krugman -This isn't a simple question of good versus evil. There are substantive policy disputes, and some very good people are, in my view, on the wrong side of some issues. Volcker is usually a hard-money guy. I haven’t had an opportunity to ask him, but my guess is that he’s suspicious of quantitative easing, and would be more likely to side with the Fed’s inflation hawks than with those of us who think the Fed should expand its balance sheet, target higher inflation, and in general do whatever it takes to bootstrap ourselves out of the liquidity trap.

Bernanke Interlude - WSJ publishes a letter: ...Applying accountability principles, there's no way Chairman Bernanke should be reconfirmed by the Senate, let alone reappointed by the Obama administration....He's been at the helm from the very beginning of this Great Recession. That alone warrants a "no" vote on reconfirmation. At this point, I feel obligated to note that if you're going to declare this The Great Recession—i.e., if you are assuming the chance of having the third Depression is over*—then Bernanke deserves credit, not blame. In addition, the Fed has increased the monetary base (high-powered or wholesale money) by the largest amount ever... inflation is a virtual certainty over the coming decade. This is Gospel for the WSJ editorial page...

Bernanke Part 2 of 2: Leaders Lead, or Just Say No - The world would be a much better place if people had listened to Tom last August:Now some elite opinion favors Ben Bernanke's reappointment, but politicians are irritated over Fed stonewalling of bailout oversight and others (e.g. Dean Baker) point out that Ben Bernanke who put the Fed throttles to the firewall to save the world is also the Ben Bernanke who carried over Greenspan policy until it was too late. Not a strong enough source for you? How about Brad DeLong last August: I am surprised that he is being reappointed. I would have thought that the combination of people angry because he has given too much public money to the banks and people angry because he didn't stop the recession would together make him damaged and that Obama would want to bring in a fresh face--.

The Bernanke confirmation: incompetence, indifference and institutional inertia - Section 2a. Monetary Policy Objectives - The Board of Governors of the Federal Reserve System and the Federal Open Market Committee shall maintain long run growth of the monetary and credit aggregates commensurate with the economy’s long run potential to increase production, so as to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates. [12 USC 225a. As added by act of November 16, 1977 (91 Stat. 1387) and amended by acts of October 27, 1978 (92 Stat. 1897); Aug. 23, 1988 (102 Stat. 1375); and Dec. 27, 2000 (114 Stat. 3028).] In black and white, that’s the mandate carried by the Chairman of the United States Federal Reserve, Ben Bernanke. He, and others, may not like it, but until the law is changed, it is what it is. (article includes videos of several obviously ignorant senators...)

Wall Street Journal Questions Bernanke's Credibility and Political Will - Last week, Economist Steve Keen made "The Case Against Bernanke". Specifically, Keen says "Bernanke's ignorance of the factors that really caused the Great Depression is a major reason why the Global Financial Crisis occurred in the first place." On Monday, I was delighted to see the Wall Street Journal make a different case against Bernanke. Please consider The Bernanke Nomination Majority Leader Harry Reid declared his support for Mr. Bernanke on Friday, but not before extracting what he said were concessions about future Fed policy. The Fed chief promised, said Mr. Reid, that he would "redouble his efforts" to make credit available and that Mr. Bernanke "has assured me that he will soon outline plans for making that happen, and I eagerly await them." Redouble? The Fed has already kept interest rates at near zero for more than a year, and it is buying $1.25 trillion in mortgage-backed securities to refloat the housing bubble, among other interventions into fiscal policy and credit allocation. Is the Fed going to buy another $1.25 trillion, or promise to keep rates at zero for another 14 months?

Paul Krugman For The Fed - Simon Johnson - The case for Ben Bernanke’s reappointment was weak to start with, weakened with his hearings, and is now held together by string and some phone calls from the White House. Bernanke is an airline pilot who pulled off a miraculous landing, but didn’t do his preflight checks and doesn’t show any sign of being more careful in the future – thank him if you want, but why would you fly with him again (or the airline that keeps him on)? The danger here is uncertainty – the markets fear a prolonged policy vacuum. Fortunately, there is a way to address this. Ben Bernanke should withdraw and the president should nominate Paul Krugman to take his place. Paul Krugman is an expert on monetary policy – he wrote the classic paper on balance of payments crises (and probably could have got the Nobel Prize just for that), his work on Japan in the 1990s shaped everyone’s thinking of how to handle potential deflation, and his assessment of the crisis and needed response in fall 2008 was right on the money...

Paul Krugman for Fed Chair: “Crazy” - Paul Krugman says that Simon’s idea that he should be chair of the Fed is “crazy.” Krugman’s point is either that he wouldn’t be confirmed or that he wouldn’t be able to bring the Open Market Committee along. Maybe he’s right about the former; a Republican filibuster does seem reasonably likely. I don’t think he’s right about the latter; or, more precisely, I don’t think it matters. The FOMC is, on paper, a democratic body: they vote. There is a tradition that the votes are generally unanimous because of the perceived importance of demonstrating consensus. Given that we all know there are debates involved, how important is this fiction of consensus? Put another way, I think it would actually be good if we had a non-unanimous FOMC and even a FOMC that voted against its chair now and then.

Should Krugman replace Bernanke? - What would happen if Ben Bernanke withdrew his name from consideration as Fed chairman tomorrow, and Barack Obama picked up the phone and asked Paul Krugman to step into the breach? Bruce Bartlett reckons that “Paul has enough sense not to accept the position even if it is offered–just as Milton Friedman rejected Reagan’s offer for him to replace Volcker in 1982″ — but I’m not so sure. After Simon Johnson proposed the idea this morning Krugman said that it was “crazy” — but he did so without saying that he would refuse the job if offered. I think he’s sensible to leave the door ajar: it’s really hard to say no to a president who asks you to serve your country by taking what Matt Yglesias calls “the single most important domestic policy job in the country”. Krugman asks the key question: Does it make sense to deny Bernanke reappointment simply in order to appoint someone who would follow the same policies?

Krugman fed up with Fed chair suggestion - In a blog post early today on the New York Times Web site, Nobel-prize winning economist Paul Krugman (who is always introduced as ‘Nobel-prize winning economist Paul Krugman’) called the suggestion that the president should nominate him to chair the Federal Reserve “crazy.” After acknowledging that his ties to Fed Chair Ben Bernanke made his criticism difficult to write — Bernanke brought Krugman to Princeton — Krugman blasted him, noting that “he has been assimilated by the banking Borg” and completely missed signs that there was “trouble building as the housing bubble inflated.” “But it’s very hard to think of people with those qualities who have any chance of actually being confirmed, or of carrying the FOMC with them even if named as chairman (which is one reason why this suggestion is crazy),” Krugman wrote.

Congress Is Politicizing the Fed - Teddy Roosevelt once remarked of a financial crisis: "When people have lost their money, they strike out unthinkingly, like a wounded snake, at whoever is most prominent in the line of vision." Late last week, we saw the Senate strike out at Federal Reserve Chairman Ben Bernanke. His nomination for a second term was the first to come into Washington's line of vision in the immediate aftermath of the Massachusetts senatorial election. There are many roadblocks we must overcome to get our economy running again...

The Fed Is Politicizing The Fed - Richard Fisher (President of The Federal Reserve Bank of Dallas) bleats that: There are many roadblocks we must overcome to get our economy running again. Businesses must develop sufficient confidence in the future to begin expanding their order books and payrolls. Banks must be willing and able to lend again. And consumers must regain the wherewithal to open their pocketbooks. Notice what's missing: Households and businesses must have the earnings capacity to be able to borrow based on production, not based on speculative frenzy. The burden of making the tough decisions needed to make our country's economy sound again falls on the sole body responsible for taxing and spending our money: Congress. Really Dick?

Bernanke Divisions in Congress Mirror Public Concerns - The split in the U.S. Senate on Federal Reserve Chairman Ben Bernanke’s nomination for a second term mirrors a divide among the American public, according to the latest Wall Street Journal/NBC News poll.About 18% of those surveyed said they were “positive” about Mr. Bernanke, the same share that said they were “negative.” Of the rest, 19% called themselves “neutral” and 45% said they were unsure. That puts Mr. Bernanke’s ratings slightly ahead of those of Treasury Secretary Timothy Geithner, who had a smaller “positive” share. About 37% of those polled Jan. 23-25 opposed Mr. Bernanke’s reappointment and 34% supported it with the rest not sure. That was little changed from a June poll.

Bernanke Confirmed for Second Term as Fed Chief – NYTimes - The Senate gave Ben S. Bernanke a second four-year term as the head of the Federal Reserve on Thursday after critics excoriated the central bank’s conduct in the years leading up to the financial crisis. The 70-to-30 vote was the weakest endorsement ever extended to a chairman in the Fed’s 96-year history.

Ben Bernanke Reconfirmed: Will He Get the Message? - The large number of negative votes, the concerns that some of the supporters have expressed, and the lukewarm support of the White House until the nomination looked to be in danger ought to send a clear– and correct — message to the Fed. When there is uncertainty about whether to pursue low inflation or low unemployment, low unemployment must prevail. If the Fed moves too fast to unwind the stimulus measures it has in place, increases in interest rates could kill the recovery and employment. But if it moves too slowly, it may have an inflation problem. So far it has not been clear that the unemployment goal is preeminent, and going forward the Fed needs to demonstrate it gives unemployment the highest priority. Inflation must take a back seat whenever there’s any doubt about which goal to pursue.

Bernanke May Have Harder Fight Defending Fed After Confirmation - (Bloomberg) -- Ben S. Bernanke, who won Senate approval for a second term as Federal Reserve chairman over a record number of opponents, may now have a tougher fight against threats to the central bank itself. Lawmakers are considering legislation to remove a shield from congressional audits of monetary policy and strip the Fed of bank-supervision powers, measures that Bernanke opposes. The debate over Bernanke’s performance has focused lawmaker attention on the powers of the institution, said Vincent Reinhart, a former Fed official. The scrutiny comes as politicians respond to voter anger over government bailouts of Wall Street firms, including the Fed’s role in rescues of AIG and Citigroup

A Colossal Failure Of Governance: The Reappointment of Ben Bernanke - Simon Johnson - When representatives of American power encounter officials in less rich countries, they are prone to suggest that any failure to reach the highest standards of living is due in part to weak political governance in general and the failure of effective oversight in particular. Current and former US Treasury officials frequently remark this or that government “lacks the political will” to exercise responsible economic policy or even replace a powerful official who has clearly become a problem.Unfortunately, two massive failures of governance at the level of the Senate also spring to mind: first, the strange case of Alan Greenspan, which stretched over nearly two decades; second, Ben Bernanke, reappointed today (Thursday).

A Modest Proposal for the Fed: Term Limits for Chairmen - WSJ - Ben Bernanke’s bloody confirmation battle is yet another sign that Congress, and the public more broadly, are looking for change at the nation’s central bank. Congress is playing with many different ideas for how to do that: 1) Fire Mr. Bernanke by denying him a second term (something that’s looking less likely as pledges of ‘yes’ votes from the Senate trickle in); 2) Strip the Fed of its power to regulate banks; 3) Give Congress’s Government Accountability Office the power to audit Fed decisions; 4) Give Congress more say on the governance of regional Fed banks. Each of these ideas has a flaw … GAO audits, for instance, could invite congressional meddling on tough decisions about raising interest rates. Taking regulation away from the Fed isn’t necessarily going to make regulation better. Here’s a proposal that hasn’t come up, but maybe ought to be on the table: Term limits for Fed chairmen. Two terms, eight years, and then you step down to a governor’s job, which gets 14 years, or leave.

The Fed cannot inflate. Buy Bonds.- Ben Bernanke is famous for saying that the Fed can always inflate if needs be by "dropping money from helicopters".But the Fed cannot "drop money from helicopters". Only the Treasury can. Helicopter drops of money are fiscal policy, not monetary policy, as they create net new financial assets for the non-Govt sector. The Fed cannot inflate. If you think about the mechanisms the Fed has, it becomes clear that they do not have to tools to create inflation. They can control interest rates, but rates are a double edged sword as the non-Govt sector has both borrowers and lenders. Low rates help borrowers but hurt savers, and high rates do the opposite. At a sector level, the impact of interest rates is muddled at best, there certainly is no clear mechanism to generate inflation.

FT – An early warning system for asset bubbles - As policymakers and business leaders gather in Davos this week, much of their conversation will no doubt focus on how to drive a global economic recovery. Yet they should spend just as much time and energy discussing how to prevent the next devastating financial crisis – specifically, how to spot and prick asset bubbles as they are inflating. For many years, some of the world’s most prominent central bankers said this was impossible. However, new research from the McKinsey Global Institute shows that rising leverage is a good proxy for an asset bubble – and that the right tools could have identified the recent global credit bubble years before the crisis broke. We urge policymakers to develop these tools and use them to ensure a more stable financial system, thereby avoiding more of the widespread pain and suffering caused by the current crisis. Our new MGI report, Debt and deleveraging: The global credit bubble and its economic consequences, details how debt rose rapidly after 2000 to very high levels in mature economies around the world. But to spot a bubble, we need to know how much debt is too much.

Identifying Bubbles - In response to the barrage of criticism that has been aimed at the efficient markets hypothesis recently, Robin Hanson makes a plea: Look, everyone, this game should have rules. EMH (at least the interesting version) says prices are our best estimates, so to deny EMH is to assert that prices are predictably wrong. And for EHM violations to be relevant for regulatory policy, price errors must be so systematic as to allow a government agency to follow some bureaucratic process to identify when prices are too high, vs. too low, and act on that info. The efficient markets hypothesis makes a stronger claim than just price unpredictability; it identifies prices with fundamental values

U.S. One-Month Bill Rate Negative for First Time Since March - Treasury one-month bill rates turned negative for the first time in 10 months, as issuance declines while investors seek the most easily-traded securities amid a renewal of risk aversion. The rate on the four-week security dropped to negative 0.0101 percent, the lowest since it reached negative 0.015 percent on March 26. The Treasury sold $10 billion of four-week bills on Jan. 26 at a rate of zero percent

WHY DEFLATION REMAINS THE GREATER RISK - The tendency is to argue that more money = inflation. After all, the great Milton Friedman said that inflation is always and everywhere a monetary phenomenon so it must be true, right? Not so fast. Friedman lived in a different time. A time when the velocity of money was stable and the gold standard was still a viable idea. Let’s start with the various types of inflation – demand-pull inflation and cost-push inflation. As of now, demand-pull inflation appears unlikely. Recent data shows this is unlikely due to high levels of spare capacity, low capacity utilization rates and generally tepid demand for goods. Despite the oodles of excess money in the system there is nothing in the data that currently suggests this recovery will result in massive demand-pull inflation. In fact, the evidence as of now suggests a potential disinflationary environment. The cost push inflation debate can be answered in one word – jobs.

Dialing back the deflation watch - In the tussle over whether deflation or inflation is the bigger threat I’ve been firmly in the deflation camp. In the last few weeks, though, I’ve tiptoed closer to neutral. Core inflation hasn’t dropped as much as I’d expected to date, and the drop that has occurred seems entirely due to owners’ equivalent rent. Goods prices inflation has been surprisingly sturdy. Yesterday’s report by the Congressional Budget Office also prompted me to reexamine my assumptions. The CBO has raised its CPI inflation rate forecast for 2010 to 2.4% from 1.7%, while leaving the 2011 forecast at a still very low 1.3%. It marked down even more its forecast of inflation as measured by the GDP price index

PIMCO: The US Falls Into The Sovereign Debt Ring Of Fire - In the latest PIMCO investor letter, Bill Gross brings up a chart he likes to call "The Ring of Fire." As you can see, this chart/graph details the amount of debt a country has in relation to their GDP. Countries in the fire zone are headed for hell in a handbasket. PIMCO predicts these countries, which include the U.S., will increase public debt to greater than 90% over the next few years, which will in turn stall growth. The most vulnerable countries in 2010 are shown in PIMCO's chart "The Ring of Fire." These red zone countries are ones with the potential for public debt to exceed 90% of GDP within a few years' time, which would slow GDP by 1% or more. The yellow and green areas are considered to be the most conservative and potentially most solvent, with the potential for higher growth.

U.S. Dollar Loves Fed Dissent - WSJ The dollar seems be benefiting from the ever so slightest of hints that the Fed might be prepared to take tiny, baby steps towards tightening. Otherwise, there’s not much to explain why the euro is getting very close to falling under $1.40 in aftermath of the FOMC decision. Hoenig dissented with the rest of the FOMC, believing “economic and financial conditions had changed sufficiently that the expectation of exceptionally low levels of the federal funds rate for an extended period was no longer warranted.” Dissenting votes get a lot of attention. They’re interesting because they show there’s a real debate at the FOMC, and sometimes the position taken by dissenters is more broadly held than the vote really shows.

Unwanted dollars - Another milestone in the financial crisis: the ECB has just reported zero interest in its latest offer of unlimited seven-day dollar liquidity. If I am right, it is only the second time in its 11-year history that this has happened in an ECB liquidity providing operation. The first was in an offer of 84-day dollar liquidity last September. The latest result was not unexpected. At the height of the economic crisis, the joint operations with the US Federal Reserve formed an important part of measures to keep financial markets working. But demand for emergency dollars by eurozone banks has tumbled in recently, as things have returned to normal. The only surprise is that the ECB has not, formally, announced the end of dollar liquidity provision.

Summers Says Dollar to Play Key Role for a Long Time (Bloomberg) -- White House economic adviser Lawrence Summers said the dollar will play a central role in the international financial system for “a long time to come.” Summers, speaking at the World Economic Forum in Davos, Switzerland, said the U.S. must pursue economic policies that will support the “fundamentals” of the currency, including reducing budget deficits. Summers, 56, director of the White House’s National Economic Council, also defended Obama’s plan to impose new rules on bank size and risk, saying they would not interfere with financial institutions’ ability to serve customers

Botox Cures – Part 1 - RGE Monitor -The global economy is currently taking the "botox" cure. A flood of money from central banks and governments – "financial botox" - has temporarily covered up unresolved and deep-seated problems. Bad Risks… In 2009 there was a ‘recovery’ in financial asset prices. The low or zero interest rate policy ("ZIRP") of major central banks helped increase asset prices. Very low returns on cash or near cash assets forced investors to switch to riskier assets in search of return. Even Pimco’s Bill Gross discovered that his cash assets paid near zero returns. The chase for yield drove rallies in debt and equity markets. Low interest rates acted like amphetamine as investors re-risked their investment portfolios. High credit spreads for investment quality companies, driven by the panic of late 2008 and early 2009, subsided and rates returned to pre-Lehman levels.

Botox Cures – Part 2 - RGE Monitor - Bad Fiscals… From late 2008 onwards, Government intervention, on an unprecedented scale, has been a dominant factor in economic matters.Governments have spent aggressively, going into or increasing deficits, to increase demand within the economy to offset weak private sector consumption and investment.Central banks have maintained low interest rates, pumped liquidity into the financial system and "warehoused" toxic assets to support the financial system. In the U.S., Fed holdings of MBS reached around $1 trillion. The purchases provided much needed liquidity to banks and reduced potential write-down on these securities. They also helped keep interest rates low and maintained the supply of housing finance. The takeover of and government support for Government Sponsored Enterprises ("GSE"), such as the Federal National Mortgage Association ("FNMA" or Fannie Mae) and the Federal Home Loan Mortgage Corporation ("FHLMC" or Freddie Mac"), was an integral part of the process. The U.S. Government has now agreed to provided unlimited support to Fannie and Freddie.

Would You Choose Economic Growth Over National Autonomy? - A nation borrowing its way toward financial insolvency is not staging an economic recovery even when GDP picks up. What is this recovery that we supposedly need? It is nothing but debt facilitated GDP growth and asset inflation to create a built-in reward for leveraged mega-investors. That’s how Wall Street banks “create” the money to pay big bonuses. If elites would put the question in fair terms, the American response would not be ambivalent: ‘Would you rather have economic growth or national financial autonomy?’ Most patriotic Americans will vote to put national liberties ahead of economic growth (i.e., “recovery”). On the other hand, Wall Street capitalists with little affinity for America’s religious and cultural traditions will choose economic growth. Many of them want national partitions to crumble so as to facilitate the dominion of capital everywhere throughout the world. Voters need to understand that elites in both parties are positioning the majority of Americans to lose big.

Economists warn federal deficit growing at unsustainable levels - Concerns over the size of the deficit have fueled public anger directed at Congress and the White House and helped create the Tea Party movement dedicated to lower taxes and shrinking the federal government. They also contributed to Republican Scott Brown's upset victory in a Massachusetts Senate race.The gap between the money the nation takes in and what it spends is higher as a share of the economy than it's been since the end of World War II. Unlike that period, however, the nation is not about to enjoy an increased labor force from returning soldiers. Instead, Baby Boomers are retiring and expanding the rolls of Social Security and Medicare.Even after the economy pulls out of the recession, the debt is projected to grow much faster than the economy.

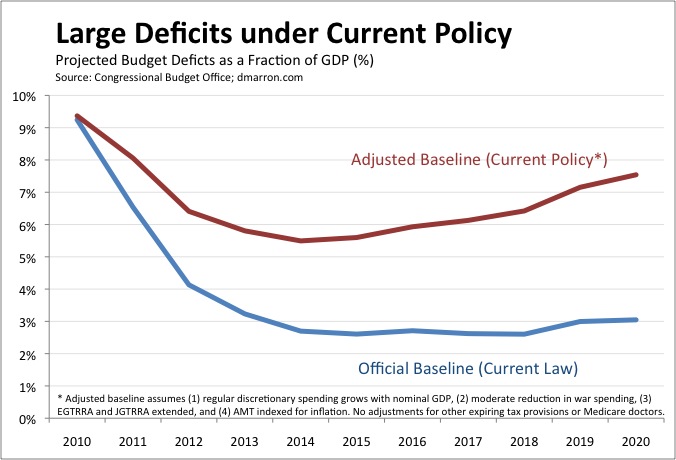

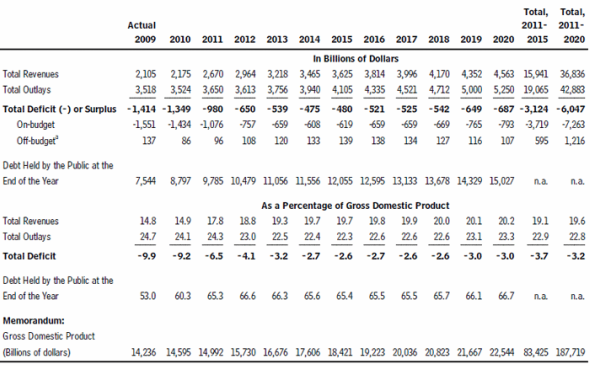

Deficits As Far as the Eye Can See - Today the Congressional Budget Office released its much-anticipated projections for the budget. As usual, the headline figure is CBO’s estimate of the budget deficit, now projected to be $1.35 trillion for the fiscal year, about 9.2% of GDP. That’s slightly better than last year–when $1.4 trillion deficits amounted to 9.9% of GDP–but is still the second-worst since World War II. And, as CBO notes, new legislation could easily lift the 2010 figure higher. For example, Congress will likely consider further extensions to unemployment benefits and more war spending, not to mention a possible jobs bill. CBO also projected deficits for the next decade.(graph) They are large and persistent

Obama Endorses Deficit Task Force - President Barack Obama Saturday endorsed a bipartisan plan to name a special task force charged with coming up with a plan to curb the spiraling budget deficit, though the idea has lots of opposition from both his allies and rivals on Capitol Hill. The bipartisan 18-member panel backed by Obama would study the issue for much of the year and, if 14 members agree, report a deficit reduction blueprint after the November elections that would be voted on before the new Congress convenes next year. The 14 would have to include at least half of the panel's Republicans – a big obstacle. "These deficits did not happen overnight, and they won't be solved overnight," Obama said in a statement. "The only way to solve our long-term fiscal challenge is to solve it together – Democrats and Republicans."

Obama Supports Deficit Commission - Some news about the deficit commission:... Also on Saturday, Mr. Obama endorsed a bill scheduled for a Senate vote on Tuesday which would create a bipartisan budget commission and require that its recommendations for slashing deficits would get a vote in Congress this year. But he remained ready to establish a panel by executive order if the vote falls short on Tuesday, despite his support. ... Brad DeLong explains why he thinks a deficit commission is a bad idea if you want to actually do something about the long-term budget problem: Let's pick ten Republican or near-Republican senators typically called "moderates" (some of whom have retired since 2003): Collins, Domenici, Grassley, Gregg, Hatch, Snowe, Specter, Voinovich, Nelson, and Lincoln. Only two of them opposed the unfunded Medicare Part D. Only one of them opposed the 2003 tax cut, And none of them opposed the 2001 tax cut-- So these aren't deficit hawks. These are something else--deficit chickens, deficit doves, deficit turkey-vultures.

How to Spot a Deficit Peacock: Deficit hawks come in a variety of breeds.... And then there is another species of deficit bird all together: the deficit peacock. Deficit peacocks like to preen and call attention to themselves, but are not sincerely interested in taking the difficult but necessary steps toward a balanced budget. Peacocks prefer scoring political points to solving problems. How can you tell the difference between deficit hawks, those who are serious about the dangers posed by persistent, large deficits and deficit peacocks, those who only use those dangers to preen and score political points? It’s actually fairly simple. Here are four easy ways to tell when someone isn’t taking our budget problems seriously.... 1. They never mention revenues.... 2. They offer easy answers.... 3. They support policies that make the long-term deficit problem worse.... 4. They think our budget woes appeared suddenly in January 2009...

Brad DeLong Gets It When It Comes To A Commission - But Brad DeLong has her number with this post: No Diane, having any budget commission is not necessarily better than not having one. I truly wish this wasn't the case. But when, as Brad points out, a commission is really just an excuse to do less now and a subterfuge for what's really happening, I don't see the value. Given all the failed budget commissions and summits of the past and the fact that the moon and stars don't seem to be in proper alignment for one to succeed now, I'd much rather have members of Congress take their lumps at the next election for not using the power they already have to deal with the deficit than to promise for no apparent reason that somehow a commission is going to be different this time.

Senate Rejects Deficit Commission: President's Budget Panel Voted Down (AP); The Senate has rejected a plan backed by President Barack Obama to create a bipartisan task force to tackle the deficit this year. The special deficit panel would have attempted to produce a plan combining tax cuts and spending curbs that would have been voted on after the midterm elections. But the plan garnered just 53 votes in the 100-member Senate, not enough because 60 votes were required. Anti-tax Republicans joined with Democrats wary of being railroaded into cutting Social Security and Medicare to reject the idea. Obama endorsed the idea after being pressed by moderate Democrats. The proposal was an amendment to a $1.9 trillion hike in the government's ability to borrow to finance its operations.

Rising Criticism for Budget Deficits and Solutions - NYTimes - The proposal for a commission died when its supporters could not muster enough votes in the Senate to push it ahead, reflecting unwillingness among many Republicans to back any move toward tax increases and objections among Democrats to the prospect of deep spending cuts in Medicare and Medicaid. While 53 senators voted for the plan and 46 against, it needed 60 votes to be approved under Senate rules. The alternative panel to be established by Mr. Obama will also come up with recommendations by December to reduce annual budget deficits and slow or reverse the growth of the national debt. But unlike the commission proposal killed by the Senate, Mr. Obama’s executive order could not force Congress to vote on a commission’s suggestions.

Conrad-Gregg Budget Commission Defeat Was A Deficit Smackdown - What does the 53-46 vote mean for the prospects of deficit reduction? The short answer is nothing good. That doesn't mean that the prospects would have been much better had the amendment been adopted and the commission created. It just means we now have a pretty good indication of what the politics of deficit reduction is at the moment. And it's ugly. Although some will try to make a big deal about the fact that the amendment received 53 out of 99 votes and, therefore, got a majority, that argument doesn't really fly in a world where the U.S. needs 60 votes to do almost anything

Why Would You Ever Cut Social Security? - Bruce Bartlett comments on the demise of the Conrad-Gregg statutory budget commission concept (note that more than fifty, but fewer than sixty, senators supported it): As I wrote the other day, I have always been lukewarm to the idea of a budget commission because I don’t think we are ready, politically or economically, for serious deficit reduction. I also have problems with the way the proposed commission would be structured–requiring a supermajority for every recommendation seems like a recipe for gridlock.That said, I have just been appalled by idiocy of the arguments against the commission that appear to have won the day in the Senate. In particular, the idea that revenues should be completely off the table is simply insane. And the idea that Social Security should be completely off limits is only slightly less crazy.I accept, as a matter of political realism, that any budget deal will probably have to include Social Security cuts, primarily because the editorial page of The Washington Post seems to have a hard-on for cutting Social Security. But I don’t understand why you’d ever want to cut Social Security. Consider this chart

Everything is Off The Table - According to Ezra Klein, before the Deficit Commission died in the Senate, a 97-0 vote backed an amendment from Max Baucus that would guarantee that the Commission couldn’t touch Social Security. RNC Chairman Michael Steel has made “protecting Medicare” from cuts a core plank of the GOP. And of course Republicans don’t want to raise taxes or cut defense spending either. But they think the deficit is too high. There’s kind of a problem here.

The $700 Billion U.S. Funding Hole; Desperately Seeking A Very Indiscriminate Treasury Buyer - A month ago we observed that in 2010, the supply/demand picture for US fixed income would be very problematic, as there was no immediate apparent substitute to fill the void resulting from the departure of the constant bid provided by the Federal Reserve's Quantitative Easing in both the UST and the MBS markets. The conclusion was that there would need to be a dramatic increase in demand for debt securities across the board, with an emphasis of Treasuries and MBS. Today, we focus on the most critical segment of debt issuance for 2010 - those ever critical US Treasuries, without whose weekly uptake by various investors, the multitrillion budget deficit will become unfundable. Using estimates from Morgan Stanley for 2010 Treasury supply and demand, the conclusion is that there will be a demand shortfall of at least half a trillion, and realistically $700 billion, to satisfy the roughly $1.7 trillion in net ($2.4 trillion gross) coupon issuance in the upcoming year.

Conservatives Don’t Care About the Deficit - I think that at the moment the DC establishment (and, it seems, the American people) care too much about the deficit. But what’s especially galling is that you can’t get the establishment to see that the conservative movement doesn’t care at all about the deficit. Progressives range from people who care a bit about the deficit to people who care a lot, but conservatives almost to a man don’t care at all. Consider: When Obama tried to reduce the deficit by reducing the growth in Medicare spending, conservatives lambasted him. When he tried to reduce the deficit with higher taxes, conservatives lambasted him. And when he tried to add a very modest dose of restraint to the defense budget, they lambasted him. But there’s simply no other way to reduce the deficit.

Attention: Liberals and Progressives - Take it as given that U.S. fiscal policy is unsustainable. It was unsustainable before Obama became President, and one can argue that he has made it worse. It was unsustainable before Bush became President, and one can argue that he made it worse. That is not the issue here.The issue is whether this unsustainability should be considered a moral problem. What "unsustainable" means is that the current government is making promises that it cannot reasonably expect to keep. The promises that are being made to future beneficiaries of Medicare and Social Security, to bondholders, and to others will not all be kept. In other words, our leaders in Congress and the Administration are lying, but we are not sure at this point who is going to bear the burden of those lies.

The US’s shrinking - and then growing - deficit - The Congressional Budget Office today released its outlook for the budget deficit. No surprise: the deficit, as a proportion of GDP, is expected to fall considerably from 9.9 per cent in 2009 to 2.6 per cent in 2015, after which it will rise again. (see table) What’s going to make it go up after 2015? Health care, of course. Here’s a pretty phenomenal graph from the Center for Economic and Policy Research based on the CBO’s projections from last year (which have changed slightly, but the overall trend is still the same).

CBO: Federal deficit projected at $1.35T - The Senate on Tuesday rejected a plan backed by President Barack Obama to create a bipartisan task force to tackle the federal deficit this year, despite glaring new figures showing the enormity of the red-ink threat.The special deficit panel would have attempted to produce a plan combining tax increases and spending curbs to be voted on after the November elections. The measure went down because anti-tax Republicans joined in opposition with Democrats wary of being railroaded into cutting Social Security and Medicare.The vote to kill the deficit task force came hours after the nonpartisan Congressional Budget Office predicted a $1.35 trillion deficit — $4,500 for every American — for this year as the economy continues to slowly recover from the recession. The budget deficits facing Obama and Congress are large and intractable, and the CBO's new deficit prediction is roughly equal to last year's record $1.4 trillion ocean of red ink. That means the government is borrowing to cover 40 percent of the cost of its programs.

The CBO’s look at the numbers (the Director’s Blog post) suggest it isn’t going to work out too well for the Obama Administration and whatever administration follows on. Now granted this is just a projection and quite a bit could happen between now and 2020. However, the idea that the Obama Administration is going to reduce the deficit by half simply isn’t all that likely without playing fast and loose with the numbers sort of reminiscent of the Bush Administration (projecting a high deficit number so that when the actual deficit comes in lower credit can be taken for reducing the deficit). And the long term effects of this debt will act as a drag on the economy.Those accumulating deficits will push federal debt held by the public to significantly higher levels. At the end of 2009, debt held by the public was $7.5 trillion, or 53 percent of GDP; by the end of 2020, debt is projected to climb to $15 trillion, or 67 percent of GDP. With such a large increase in debt, plus an expected increase in interest rates as the economic recovery strengthens, interest payments on the debt are poised to skyrocket. CBO projects that the government’s annual spending on net interest will more than triple between 2010 and 2020 in nominal terms (from $207 billion to $723 billion) and will more than double as a share of GDP (from 1.4 percent to 3.2 percent).

CBO Testifies before the House and Senate Budget Committees on the Budget and Economic Outlook - Director's Blog - I testified about CBO’s Budget and Economic Outlook to the House Budget Committee yesterday morning and to the Senate Budget Committee this morning. In both testimonies I highlighted several points from the Outlook...

Senate Approves Amendment to Raise Debt Ceiling by $1.9 Trillion- The Senate approved legislation Thursday increasing the federal government's borrowing limit by $1.9 trillion, enough to enable the Treasury to pay its bills through 2010. The 60-39 vote was strictly along party lines with no Republicans joining the Democratic majority to approve the legislation. Once the increase is signed into law, the federal government will be able to borrow up to $14.3 trillion, by far the highest amount of debt it has ever held on its books. The current limit of around $12.4 trillion would have been breached by the end of February. House lawmakers must still take up the legislation and are expected to do so next week, according to a senior House Democratic aide.

Our Debt Is Getting Scary - But overhanging his ambitious agenda is a darkening cloud of debt as we were reminded Thursday when the senate voted to raise the nation's debt limit by $1.9 trillion. The CBO director recently noted that debt held by the public totaled $7.5 trillion, or 53% of GDP, at the end of 2009. Of perhaps greater concern, this frightening percentage only looks to get worse. By the end of 2020 the debt is expected to climb to $15 trillion, or 67% of GDP. America is a resourceful country but these projections are beginning to look scary. America's enormous debt has consequences, says one money manager who stopped by my office on Thursday. He sees America's debt burden driving up Government bond yields because, he believes, foreign buyers will demand it— not because they expect an outright default by the U.S. but because they know America's way is the more subtle 'inflation default'. Higher bond yields will be the first of many penalties Americans pay because we have allowed the nation's debt to grow and grow

Why we should expect low growth amid debt- Reinhart & Rogoff: (FT) -As government debt levels explode in the aftermath of the financial crisis, there is growing uncertainty about how quickly to exit from today’s extraordinary fiscal stimulus. Our research on the long history of financial crises suggests that choices are not easy, no matter how much one wants to believe the present illusion of normalcy in markets. Unless this time is different – which so far has not been the case – yesterday’s financial crisis could easily morph into tomorrow’s government debt crisis. In previous cycles, international banking crises have often led to a wave of sovereign defaults a few years later. The dynamic is hardly surprising, since public debt soars after a financial crisis, rising by an average of over 80 per cent within three years. Public debt burdens soar owing to bail-outs, fiscal stimulus and the collapse in tax revenues. Not every banking crisis ends in default, but whenever there is a huge international wave of crises as we have just seen, some governments choose this route.

What a Potentially Sustainable Budget Outlook Looks Like - This is a chart from CBO’s new outlook report. Note that deficits get down to the 2 1/2 to 3 percent of GDP range within five years. Note that revenues rise and spending falls, but that revenues do most of the heavy lifting (5 percent of GDP out of the 7 percent of GDP reduction in the deficit). Note that this assumes CBO’s “current law baseline” where tax cuts expire as written in current law. Hold that thought.Here's Concord's press release reacting to the CBO report. More to say tomorrow, but here's the one-minute version: to get to sustainability, within the first five years it's all about revenue policy and avoiding the deficit-financed extension of tax cuts, and beyond that (but still, ideally sooner rather than later), we'll have to figure out how to bend that darned health cost curve, because even with a reformed tax system, we won't be able to keep up with health spending on its current path.]

Officials say stimulus bill to cost $75B more - Last year’s $787 billion economic stimulus bill is going to be even more expensive – $75 billion more. That’s the finding in Tuesday’s Congressional Budget Office estimate of the costs of the economic stimulus bill, which mixed tax cuts and lots of spending in an effort to jump-start the economy. The estimate provides more ammunition for Republicans who say the stimulus has been long on spending and short on creating promised jobs. Almost half of the additional cost, $34 billion, is because the food stamp program won’t be able to take advantage of lower-than-expected inflation rates and will instead have benefits set by the stimulus bill.

Democrats look to new budget rules to tame deficit - Democrats are trying to toughen budget rules to make it more difficult to run up the deficit with new tax cuts or federal benefit programs, a move Republicans say is a recipe for tax increases. The proposal by Senate Majority Leader Harry Reid, D-Nev., would make it harder to extend permanently some tax cuts that expire at the end of this year, renew health care subsidies for laid-off workers that expire next month, or offer more help to states for Medicaid for the poor.Some middle-class tax cuts would not be affected, and extended unemployment benefits for the long-term jobless may also be exempt.

Not liberal or conservative, just incoherent - IN ITS updated global forecast released this morning, the IMF warns against “premature and incoherent exit” from government support for the economy. “Incoherent” nicely describes the policy debate in Washington. Partisans have aimed their poison at the Federal Reserve and at the government's fiscal policy choices but what, exactly, do they want? The logical implications of their complaints are contradictory at best and dangerous at worst. Start with the Fed. On the right, they’re angry about quantitative easing which they say is monetising deficits. On the left, they’re angry about lax regulation of banks. Both are furious at bail-outs of banks and AIG, and both think the Fed created a bubble with its low interest rates. So the Fed, presumably, should shrink its balance sheet, end its asset purchases and liquidity programmes, order banks to raise underwriting standards and raise rates to nip the next bubble in the bud. And this is going to bring unemployment down?

Doing As Much As We Can Do, Now - I expect that some fiscal-hawkish senators will still let the perfect be the enemy of the good, claiming to be voting against the amendments that they would have written differently, that they think (or claim to think) do not go far enough. But imperfections aside, we should keep in mind that these three types of measures–caps for annual discretionary spending, PAYGO for new mandatory spending and tax cuts, and a commission for reforms to the existing entitlement and tax systems–are complementary, not competing, proposals, and that if we really want to make progress on reducing the deficit anytime in the next decade as well as sustainably over the longer run, we really need all three and then some

Value-Added Tax: No Easy Fix for the Deficit - There is a growing call by backers of bigger government for Congress to impose a value-added tax (VAT) on top of all the other taxes Americans already pay. A VAT is similar to a national retail sales tax but is collected at every stage of business production until its entire burden ultimately falls on the consumer. VATs are common in other countries, especially in the European Union (EU).[2] Despite the perception that VATs are difficult to evade, data show that fraud to avoid the VAT is widespread in the EU. In fact, the fraud is causing revenue shortfalls large enough that many EU countries are scrambling to prevent the abuse.[3]

Officials: Obama will propose three-year spending freeze - President Barack Obama will propose a three-year freeze in non-security discretionary spending, senior administration officials said Monday. His budget proposal, to be unveiled in part with Wednesday's State of the Union speech and in detail next week, will urge Congress to keep overall spending at $447 billion a year for agencies other than those charged with national security and mandatory-spending programs such as Social Security and Medicare. The freeze would take effect with the 2011 fiscal year starting Oct. 1 ...

President Obama concedes defeat - On an exciting phone call with progressive internet writers earlier this evening, a senior administration official outlined the Obama administration’s plan to call for a freeze in non-security discretionary spending spending starting with the Fiscal Year 2011 budget. Described as an effort to balance concern with a “massive GDP gap” in the short run and “very substantial budget deficits out over time,” the plan calls for the FY 2011 budget to be higher than the FY 2010 budget, but then for non-security discretionary spending to be held constant in FY 2012 and FY 2013. (Let me note right here that all of the reporters on the call, myself included, screwed up and forgot to seek clarification as to whether this is a nominal freeze or a real dollar freeze).The freeze would not apply to the Department of Defense, the Department of Veterans Affairs, the Department of Homeland Security, or to the foreign operations budget of the State Department. So is this an across-the-board freeze like we’ve heard Republicans call for?

Obama, Deficits, Freezes, and Commissions - It has been an interesting day for us fiscal policy wonks. Over my morning muffin, I digested President Obama’s plan to freeze some domestic spending for the next three years as well as his package of aid to the middle-class. Then, I spent a few hours chewing over the CBO’s latest budget projections. Finally, I watched the Senate trash the bipartisan budget commission. Add it all up, and we are pretty much where we started, although some important issues are becoming clearer. To take things slightly out of order, In today's budget update, CBO figures the 2010 deficit will be about $1.35 trillion, or 9.2 percent of GDP. We could cut the deficit in half by 2012 if Congress allows the Bush tax cuts to expire, lets the Alternative Minimum Tax bite 30 million middle-class Americans etc.—none of which is going to happen.

Obama Wants to Limit Government Spending Despite High Unemployment and a Fragile Economy - The long-term budget problem is due to primarily one thing, rising health care costs. Everything else is dwarfed by that problem. If we solve the health care cost problem, the rest is easy. If we don't solve it the rest won't matter. This was an opportunity for Obama to explain the importance of health care reform and how it relates to the long-term debt problem. Why not emphasize this?: Instead we get cheap political tricks that are likely to backfire. How will this look, for example, if there's a double dip recession, or if unemployment follows the dismal path that the administration itself has forecast? This seems to be a case of the former Clinton people in the administration (or wannabees) trying to relive their glory days instead of realizing that those days are gone, the world is different now and it calls for different solutions.

Barack Herbert Hoover Obama? - DeLong: For some time I have been worried about fifty little Herbert Hoovers at the state level. Right now it looks like I have to worry about one big one. What we are talking about is $25 billion of fiscal drag in 2011, $50 billion in 2012, and $75 billion in 2013. By 2013 things will hopefully be better enough that the Federal Reserve will be raising interest rates and will be able to offset the damage to employment and output. But in 2011 GDP will be lower by $35 billion--employment lower by 350,000 or so--and in 2012 GDP will be lower by $70 billion--employment lower by 700,000 or so--than it would have been had non-defense discretionary grown at its normal rate. (And if you think, as I do, that the federal government really ought to be filling state budget deficit gaps over the next two years to the tune of $200 billion per year, the employment numbers are more like 3.3 and 3.7 million in 2011 and 2012, respectively.)

This Is Such a Disaster in the Making II - DeLong - The Economist: "I understand the arguments from supporters... this is a political gambit... it won't actually amount to much... a tool with which to co-opt the president's moderate antagonists.... If this is the best the president can do, Democrats, and the country, are in for a very long few years": RA: There really is no good way to interpret this turn of events. From the standpoint of the purely economical, this is a huge mistake. Even if we assume that the economy will be strong enough in 2011 to handle budget balancing, this proposal is practically worthless. The administration has said this will produce $250 billion in savings over ten years, but as The Economist noted in November, the fiscal deficit will be over $700 billion in 2014 alone, and will grow from there. Non-defence discretionary spending is nothing; those who are serious about long-term budget sustainability talk about defence, they talk about entitlements, and they talk about revenues. In other words, this will do very little about the deficit, and it will do even less to convince markets of the credibility of the American effort to trim the deficit.

Obama Liquidates Himself - A spending freeze? That’s the brilliant response of the Obama team to their first serious political setback? It’s appalling on every level. It’s bad economics, depressing demand when the economy is still suffering from mass unemployment. Jonathan Zasloff writes that Obama seems to have decided to fire Tim Geithner and replace him with “the rotting corpse of Andrew Mellon” (Mellon was Herbert Hoover’s Treasury Secretary, who according to Hoover told him to “liquidate the workers, liquidate the farmers, purge the rottenness”.) It’s bad long-run fiscal policy, shifting attention away from the essential need to reform health care and focusing on small change instead.

Don't mention the war spending - I was already bristling at the implication that while plenty of waste could be found on the non-defence side of the budget, every last dollar spent at Defence, State, Homeland Security, and Veterans Affairs was crucial in preventing attacks. But then Mr Nabors addressed a question concerning how the freeze would be carried out. And in noting that not all programmes would be treated equally—that some would face budget cuts while others enjoyed spending increases—he compared the selective trimming to the president's decision last year to cut funding for...the F-22.