Fed balance sheet shrinks in latest week -- Federal Reserve's balance sheet contracted slightly in the latest week, Fed data released on Thursday showed. The Fed's balance sheet stood at $2.861 trillion on March 28, down from $2.8756 trillion on March 21.The Fed's holdings of Treasuries totaled $1.665 trillion as of Wednesday, March 28, versus $1.663 trillion the previous week. The Fed's overnight direct loans to credit-worthy banks via its discount window averaged $4 million a day during the week versus $12 million a day previously. The Fed's ownership of mortgage bonds guaranteed by Fannie Mae, Freddie Mac and the Government National Mortgage Association (Ginnie Mae) was $836.8 billion versus $851.3 billion the previous week. The Fed's holdings of debt issued by Fannie Mae, Freddie Mac and the Federal Home Loan Bank system totaled $96.5 billion, versus $98.99 billion the prior week.

FRB: H.4.1 Release--Factors Affecting Reserve Balances--March 29 2012

Fed's Plosser Calls Fed Balance Sheet Problematic - The Federal Reserve went down a dangerous road when it expanded its balance sheet with more than just Treasury securities in a bid to provide stimulus to the economy, a key central banker said."The balance sheet of the Federal Reserve has changed from one made up almost entirely of short-term U.S. Treasury securities to one that is mostly long-term Treasurys, plus significant quantities of long-term mortgage-backed securities," Federal Reserve Bank of Philadelphia President Charles Plosser said. "This concentration of housing-related securities is problematic because it is a form of credit allocation and thus violates the monetary [and] fiscal policy boundaries' that should guide the proper conduct of Fed policy, he said. When the Fed provides stimulus in the way it has over the course of the financial crisis and the recovery, it degrades the public's perception that the central bank is a neutral player in the economy, Plosser said. "When markets or governments come to believe that a central bank can freely expand its balance sheet without directly impacting the stance of monetary policy, I believe that various political and private interests will come forward with a long list of good causes, or rescues, for which such funds could or should be used," he said.

Fed Chief Bernanke Defends Bond Buys - Federal Reserve Chairman Ben Bernanke ended his college lecture series with a vigorous defense of the central bank's two rounds of bond buying to bolster the economy after the 2008 financial crisis. The Fed's purchases of Treasury securities and mortgage-backed securities were "generally successful" in lowering interest rates and helping to support economic growth, Mr. Bernanke said Thursday in his fourth lecture at George Washington University. The "lower long-term rates have, in my view and in terms of the analysis we do at the Fed, promoted growth and recovery," Mr. Bernanke said. He acknowledged, however, that the Fed's effect on the housing market was "weaker than we would've hoped." Fed officials succeeded in pushing mortgage rates to record lows, but that has failed to spur more home purchases and home construction because of problems in the housing and credit markets, he said. Federal Reserve officials haven't been uniformly supportive of the asset purchases. Among the critics is Richmond Federal Reserve Bank President Jeffrey Lacker, who has expressed doubts that the Fed's second round of bond-buying helped boost economic growth. Both Mr. Lacker and Philadelphia Federal Reserve Bank President Charles Plosser have worried the programs could stoke inflation.

Foreign Banks Borrowing Fewer Dollars - Foreign central banks have borrowed fewer U.S. dollars recently from the Federal Reserve as market conditions have improved, a Fed official said Tuesday in remarks prepared for a congressional hearing. Foreign central banks’ demand to borrow U.S. dollars through the Fed’s swap lines peaked at $109 billion in mid-February and the cost of dollar funding declined, Steven Kamin, the Fed’s director of the international finance division, said in remarks prepared for a Tuesday hearing of a panel of the House Financial Services Committee. “In recent weeks, reflecting the improvement in market conditions, usage of the swap lines has fallen back to about $65 billion,” Kamin said in his opening statement. Kamin’s prepared remarks were largely identical to those he delivered in mid-February to the Senate Banking Committee. He emphasized that the Fed’s swap agreement with other foreign central banks poses very little risk to the Fed and the U.S. taxpayer. The Fed lends the dollars to other central banks, rather than individual foreign financial institutions. The U.S. central bank has not “lost a penny” on any of the swap transactions, Kamin said.

Bernanke’s Speech Has the Market Buzzing with QE3 Hopes - The U.S. economy needs to grow faster to maintain job market momentum, Federal Reserve Chairman Ben Bernanke said in a speech Monday; as a result, the Fed will continue its low-interest rate policy, hoping to spur consumer demand and business investment. Stocks rose on Bernanke’s comments, with some on Wall Street reading hints about a third round of Fed bond purchases, or quantitative easing (QE3). Despite encouraging signs, the labor market still has a very long way to go to get back to pre-recession levels. Two years of consistent but modest job gains have brought the unemployment rate from over 9% down to 8.3%. But the U.S. economy is still 5 million jobs short of the previous peak, Bernanke said, and three percentage points above the average unemployment rate for the last two decades. “Further significant improvements in the unemployment rate will likely require a more rapid expansion of production and demand from consumers and businesses, a process that can be supported by continued accommodative policies,” Bernanke said in a speech to the National Association for Business Economics.

Fed Watch: Bernanke, Bullard, and QE3 - This morning Federal Reserve Chairman Ben Bernanke gave a speech that apparently was identified as proof that QE3 is still in the cards. He argues that while labor markets have shown improvement in recent months, conditions are far from normal. Moreover, he sees the problem of long-term unemployment as largely structural, and delivers what many believed to be the money quote: I will argue today that, while both cyclical and structural forces have doubtless contributed to the increase in long-term unemployment, the continued weakness in aggregate demand is likely the predominant factor. Consequently, the Federal Reserve's accommodative monetary policies, by providing support for demand and for the recovery, should help, over time, to reduce long-term unemployment as well. In my opinion, to interpret this as a call for additional quantitative easing is a bit of a stretch. It sounds like simply a confirmation that Bernanke believes the current policy stance is appropriate and that the existence of long-term unemployment should not be viewed as a reason to believe that we are closing in on a resource constraint that would necessitate a tightening of the policy stance. In essence, Bernanke suggests that the recent rapid improvements in unemployment reflect largely a reversal of out-sized deterioration experienced during the recession. As such, we should not expect a slower pace of improvement given current growth forecasts. Under such conditions, I believe, Bernanke would push for another round of QE. He leaves open the possibility, however, that labor markets will continue to improve at the recent pace, in which I think QE3 is off the table. And that is where Federal Reserve President James Bullard steps in to the picture. He said pretty much the same thing in a CNBC interview:

Bernanke Just Admitted the Fed Failed... Not That More QE Is Coming - So Bernanke provided the “QE is coming” crowd with hope again this morning, using the usual ambiguous language that stock bulls convert into a definitive declaration of more QE. Here’s what Bernanke said: "If this hypothesis is wrong and structural factors are in fact explaining much of the increase in long-term unemployment, then the scope for countercyclical policies to address this problem will be more limited. Even if that proves to be the case, however, we should not conclude that nothing can be done.” It’s the last phrase that has the QE crowd certain QE is coming. Never mind that Bernanke has been stating QE was no longer attractive as a monetary option since MAY 2011, or that the Fed has primarily been engaging in verbal, rather than monetary, intervention for nearly a year (Operation Twist 2 was just a reshuffling of the Fed’s Treasury holdings)… this one statement from Bernanke means more QE is coming.

Fed’s Plosser: ‘Much Easier to Cut Rates Than Raise Them’ - The U.S. economy is on track to grow as much as 3% and unemployment to fall below 8% this year, Federal Reserve Bank of Philadelphia President Charles Plosser said Monday. But even if the economy turns around quickly, it will take time to unwind unconventional measures and get interest rates back up, he said on the sidelines of a conference at the Bank of France. “It’s much easier to cut rates than it is to raise them,” he said.

Fed’s Rosengren: More Stimulus Is Still on the Table - The Federal Reserve should provide additional support to the economy beyond what’s already planned should weakness reemerge, a central bank official said Tuesday. “If real GDP does not grow more rapidly and unemployment remains at its current unacceptably high level, monetary policy may need to be more accommodative,” Federal Reserve Bank of Boston President Eric Rosengren said.

Four problems with aggressive monetary policy - Masaaki Shirakawa, the governor of the Bank of Japan, gave a subtle and interesting speech this weekend that may not have been totally comfortable for his hosts at the Federal Reserve.Mr Shirakawa set out four problems with aggressive monetary easing in the wake of a financial crisis. These are closely mirrored in the US debate about Fed policy but on several points he took the argument further:

- (1) Mr Shirakawa’s first point is that loose monetary policy mitigates the pain as households repair their balance sheets, but reduces their incentive to do so quickly, not just for the private sector but for governments as well. However, he also suggests that the effectiveness of loose policy may fall over time as households that weren’t damaged by the crisis bring forward such spending as they want to.

- (2) The second point seems the most dubious to me but would be profoundly important if true. Mr Shirakawa suggests that low interest rates might induce companies to make investments with really low returns – Japan’s endless public works, perhaps – and so low interest rates could actually cause potential growth to go down. (He doesn’t say this but I can’t imagine how this works unless some economic

- (3) Point three is the more standard argument that flattening the yield curve too far for too long will undermine the profitability of the financial sector.

- (4) Mr Shirakawa’s fourth point is an argument about why banks such as the Fed should worry about the effect of easy policy on global commodity prices. In essence, he says that individual central banks that concentrate on domestic inflation targets could end up causing global problems, which in turn make it hard to hit domestic inflation targets. That contrasts with Ben Bernanke’s fairly clear statement in the wake of QE2 [quantative easing] eighteen months ago, that if developing countries want to import US monetary policy, then they will have to live with the consequences.

Fed Watch: Lessons From Japan? - Via Mark Thoma, Robin Harding at the FT Money Supply blog reports on a speech given by Bank of Japan Governor Masaaki Shirakawa. The speech reportedly details the problems that emerge from aggressive monetary policy. FT quotes key sections. The first concern is two-fold: Mr Shirakawa’s first point is that loose monetary policy mitigates the pain as households repair their balance sheets, but reduces their incentive to do so quickly, not just for the private sector but for governments as well. However, he also suggests that the effectiveness of loose policy may fall over time as households that weren’t damaged by the crisis bring forward such spending as they want to. The first sentence sounds like a rehashing of the "liquidationist" approach. We should let the economy collapse rather than provide support during balance sheet adjustment. The second part suggests that there is only so much spending that can be brought forward via low interest rates. But I think this is not really a novel idea, as we pretty much know that the effectiveness of monetary policy fades at the zero bound: At this point, if the BoJ wanted to induce additional spending, they would need to make a credible commitment to a higher inflation target. In other words, the effectiveness of monetary policy did not fade unexpectedly - it is exactly what you would expect given the zero bound problem. The second concern is that a low interest rate environment is hurting potential growth

It's Baaack! Well, really, it never went away. - Robin Harding at FT Money Supply brings to our attention a speech made by the governor of the Bank of Japan, Masaaki Shirakawa, at the Federal Reserve's "Central Banking: Before, During and After the Crisis" conference. Both Robin and Tim Duy have been equally perplexed by some of the statements made by the governor of the BoJ, and I'm going to continue that theme here unfortunately. Firstly, Robin alludes to a view taken by Mr Shirakawa with regards to balance sheet adjustment; "Mr Shirakawa’s first point is that loose monetary policy mitigates the pain as households repair their balance sheets, but reduces their incentive to do so quickly, not just for the private sector but for governments as well. However, he also suggests that the effectiveness of loose policy may fall over time as households that weren’t damaged by the crisis bring forward such spending as they want to. “Needless to say, the effect of low interest rates is extended to those economic entities that have not suffered any damage to their balance sheets. If they bring forward future demand to the present by taking advantage of a low interest rate environment, this leads to an increase in aggregate demand. As balance-sheet adjustment continues for a long period of time, however, the amount of future demand that could be brought forward gradually diminishes even in a low interest rate environment.”" Mr Shirakawa's objection towards central banks assisting in the deleveraging process of the private and household sectors is straight from the early 20th century USA, pre-modern Federal Reserve "needs of trade" doctrine, I (and I'm certainly not alone) simply just do not buy it.

Trichet warns of "behavioral contagion" - Jean-Claude Trichet, the former president of the European Central Bank, said Saturday that he is worried that controversial quantitative easing and other nontraditional steps that global central banks have taken since the financial crisis could be here to stay. The Fed has purchased $2.3 trillion of securities since it cut interest rates to zero in December 2008 in a bid to bring down long-term interest rates and boost economic growth. These actions have led to criticism, especially during the early days of the Republican contest for the 2012 presidential nomination, that Fed Chairman Ben Bernanke was undermining the dollar and creating conditions for a sharp rise in inflation. Speaking to a conference of influential central bankers from around the world and leading academic experts on monetary policy, Trichet said it could still turn out that the bond-buying, asset purchases and liquidity injections by global central banks might go away after the financial system gets back on its feet. That is the optimistic scenario, he said. But Trichet said there was a “less flattering conjecture” that the extraordinary actions will be part of a new “permanent regime.”

BB Gun - As gold holders with fairly comprehensive views of global monetary policies and central banking we were asked to comment about the first of four installations of Ben Bernanke’s lecture series at George Washington University, entitled “The Federal Reserve and the Financial Crisis”. Despite thinking the lecture was woefully incomplete, diversionary and oftentimes quite disingenuous, our initial reaction was to let it go. We think our anticipated macroeconomic outcome will be ignored and denied by public policy makers up until the time they are forced to adopt it and take ownership of it. The math and political expediency behind future inflation and hyperinflation are too compelling to ignore.However, while our business is not to debate publicly, especially the Fed Chairman who must navigate multiple constituencies with various dissenting social, economic and political views, we take seriously false claims that serve to undermine our business. In our opinion the consensus view of the forces behind the general price level, borne from misconceptions about money and banking, is fundamentally wrong. Mr. Bernanke went out of his way last Monday to perpetuate that myth. (That the myth happens to be self-serving for central banks, including the Fed, and for the global banking system should not be dismissed.

The Most Important Idea Bernanke Did Not Discuss in His Lecture - Fed Chairman Ben Bernanke delivered his fourth lecture yesterday. The Chairman covered a lot of ground in his talk but failed to discuss one of the most important ideas in understanding this crisis: the passive tightening of monetary policy. This occurs whenever the Fed passively allows total current dollar spending to fall, either through a endogenous fall in the money supply or through an unchecked decrease in velocity. This failure to act when aggregate demand is falling has the same impact on the stance on monetary policy as does an overt tightening of monetary policy. And the damage done by a passive tightening is no different than that of an overt tightening. The only difference is that the public is more aware of the overt form. Bernanke agrees. Back in late 2010, he acknowledged the possibility of passive tightening and used it as a justification for stabilizing the size of the Fed's balance sheet (my bold): Any further weakening of the economy that resulted in lower longer-term interest rates and a still-faster pace of mortgage refinancing would likely lead in turn to an even more-rapid runoff of MBS from the Fed's balance sheet. Thus, a weakening of the economy might act indirectly to increase the pace of passive policy tightening--a perverse outcome. In response to these concerns, the FOMC agreed to stabilize the quantity of securities held by the Federal Reserve by re-investing payments...By agreeing to keep constant the size of the Federal Reserve's securities portfolio, the Committee avoided an undesirable passive tightening of policy that might otherwise have occurred...

Fed Has Done Enough to Protect U.S. From Europe, Official Says - The Federal Reserve has likely done enough for now to protect the U.S. economy from Europe’s ongoing financial crisis, a top U.S. central bank official told a congressional panel Tuesday. While the Fed is “actively and carefully assessing” what is happening in Europe right now, Federal Reserve Bank of New York President William Dudley said, “I do not anticipate further efforts by the Federal Reserve to address the potential spillover effects of Europe on the United States.” He added, “We will continue to monitor the situation closely.” Dudley was speaking before the House Financial Services Subcommittee on Domestic Monetary Policy and Technology in Washington. The official is vice chairman of the monetary policy setting Federal Open Market Committee, and he didn’t offer any forward guidance about the future direction of monetary policy. The bulk of his remarks were devoted to the European sovereign debt crisis and the Fed’s response so far. The central bank has been criticized by some for the reintroduction of a facility that lends dollars to the word’s major central banks. Some have argued this action amounts to stealth bailout of overseas banks. Fed officials have countered the dollar swap program is an easy way to ensure dollar liquidity remains ample, which in turn helps protect U.S. banks

The Fed Is Losing The "Race To Debase" - As we pointed out about a month ago, in "While You Were Sleeping, Central Banks Flooded The World In Liquidity" as the world was focused on headlines whether or not the Fed would step up as it always does when the market is sliding, and unleash the monetary floodgates, it was not Ben Bernanke, but eveyrone else that hit CTRL+P and took the place of the Fed, of note the primary central banking peers among the Final Four - the ECB, the BOE and the BOJ. And why not: after all the hope was that since electronic money is electronic money, and can be moved from point A to point B at the push of a button, it would be used primarily to reflate stocks around the world, but mostly where the path has least resistance - the US. What was not accounted for was that money would also be used to inflate commodities such as oil - a key factor when delaying further US-based easing in an election year. However, more than even record for this time of year gas prices, there was one even more important outcome from this chain of events. As the following chart from Willem Buiter shows, in its fake attempt to show monetary restraint, the Fed has gone straight into last place in the "race to debase." Needless to say, in a world with $25+trillion in "excess" debt (debt which would need to be eliminated simply to reduce global debt/GDP to a "sustainable" 180% per BCG), last is a very bad place to be...

Bill Gross Predicts QE3 and Operation Mortgage Twist - PIMCO founder and co-CIO Bill Gross spoke with Bloomberg Television's Margaret Brennan today, telling Bloomberg TV that the Fed will likely shift focus to mortgage securities to keep borrowing rates low when Operation Twist ends in June. Link of video: Bill Gross on Pimco ETF Ticker Change, Bonds, Fed. Partial Transcript: "I think the Fed is outcomes-oriented. They want an outcome in terms of a higher stock market, in terms of housing starts and lower unemployment. What [Bernanke] said on Monday, in terms of the employment, he suggested that up until now, we've done very well in terms of reducing unemployment but it’ll be tougher going forward if only because of structural impediments that he outlined. Going forward, he's looking at jobs, at unemployment and the housing markets. You know, future QEs will the outcome-oriented type of strategy which seeks to provide jobs and provide higher housing prices and housing starts to continue on.""I have a sense that they'll continue with the Operation Twist, but not necessarily in terms of buying longer-term bonds and selling shorter dated Treasuries. I think that's basically been played out and the pension market itself in terms of liability structure has been damaged to some extent by lower 30-year yields. I think [Bernanke] will try to do is Twist in the mortgage market. Basically, buy current coupon mortgages in agency spaces and then basically Twist by repo-ing out the Treasuries that they currently own in short-term space. So, you know, a twist on another Twist I suppose, going forward."

Economics Survey: Fed Should Hold Back From QE3 This Year - The Federal Reserve shouldn’t undertake a new round of bond buying this year, an overwhelming majority of a group polled by the National Association for Business Economics said in a survey released Monday. While the majority of the 259 economics professionals polled in the semi-annual survey thought the U.S. central bank’s previous two rounds of asset purchases have been a success, 81% of the group said the Fed shouldn’t launch a third such program this year. Fed officials have suggested they could be open to a third round of bond buying if the economy begins to weaken, but a recent uptick in the labor market may make that less likely. The Fed has nearly tripled its portfolio of assets since the financial crisis as part of its efforts to keep interest rates low to spur spending and investment.

Bernanke Says Accommodative Policy Needed to Cut Joblessness - Federal Reserve Chairman Ben S. Bernanke said while he’s encouraged by the unemployment rate’s decline to 8.3 percent, continued accommodative monetary policy will be needed to make further progress. The drop in unemployment may reflect “a reversal of the unusually large layoffs that occurred” in 2008 and 2009, and this process may now be over, Bernanke said in a speech today in Arlington, Virginia. Reducing the jobless rate further will probably require a quicker expansion of business production and consumer demand, which “can be supported by continued accommodative policies,” he said. Stocks rallied as some investors bet Bernanke’s comments indicate further policy easing is still under consideration. The Federal Open Market Committee on March 13 raised its assessment of the economy while repeating that interest rates are likely to stay low at least through late 2014.

Try overshooting for once, please - The Economist - YESTERDAY, Federal Reserve Chairman Ben Bernanke gave a speech on America's labour market that has central bank tea-leaf readers speculating over its implications for a new round of asset purchases—QE3. Tim Duy has what seems like the most reasonable read of the present FOMC stance.In essence, Bernanke suggests that the recent rapid improvements in unemployment reflect largely a reversal of out-sized deterioration experienced during the recession. As such, we should not expect a slower pace of improvement given current growth forecasts. Under such conditions, I believe, Bernanke would push for another round of QE - although it stills begs the question of why he doesn't push for more now given the existing forecasts. But he hasn't, so we can only infer that he thinks the costs of additional easing outweigh the benefits. Let me restate that. Mr Bernanke thinks that rapid improvement in labour markets over the past three months is a product of catch-up from previous underperformance (given observed growth in GDP). He does not appear to think the Fed's current policy is sufficient to generate labour market improvements as fast as what we've seen over the past three months. If he is wrong and the economy maintains this pace of improvement, then, as Mr Duy says, QE3 is off the table. If, however, he is right, and the pace of improvement slows, then another round of asset purchases is a real possibility.

Setting the Table for Implicit Level Targeting - This seems to be the theme building in Federal Reserve speeches and communication. Ben Bernanke today. To sum up: A wide range of indicators suggests that the job market has been improving, which is a welcome development indeed. Still, conditions remain far from normal, as shown, for example, by the high level of long-term unemployment and the fact that jobs and hours worked remain well below pre-crisis peaks, even without adjusting for growth in the labor force. Moreover, we cannot yet be sure that the recent pace of improvement in the labor market will be sustained. Notably, recent decline in the unemployment rate may reflect, at least in part, a reversal of the unusually large layoffs that occurred during late 2008 and over 2009. To the extent that this reversal has been completed, further significant improvements in the unemployment rate will likely require a more-rapid expansion of production and demand from consumers and businesses, a process that can be supported by continued accommodative policies.Rate are improving, but “conditions remain far from normal” in the level. This links well with “economic conditions are likely to warrant an exceptionally low level for the Federal Funds rate”We are beginning to see a strong implicit recognition that the relevant economic conditions are not the growth rates of real variables but the level of those variables, particularly employment.

Monetarists should be thinking about fiscal policy -"Market monetarists" like Scott Sumner and David Beckworth frequently make the case that countercyclical fiscal policy is unimportant - that we shouldn't be thinking about optimal fiscal policy. They make (at least) two basic arguments: Argument 1: Fiscal policy doesn't matter for aggregate demand because the Fed will just cancel it out. Argument 2: The Fed is much more technocratic than Congress, and also quicker to act, so stabilization policy is best left to the Fed. I've addressed Argument 1 before, so now I want to focus on Argument 2. This is not a new argument, but Scott Sumner states it pretty concisely in this reaction to the new DeLong/Summers fiscal policy paper:

Michael Hudson on the Federal Reserve System - An interview with Michael Hudson published on the Russian website Terra America (TA). Prior to the Federal Reserve’s founding in 1913, U.S. monetary policy was conducted by the Treasury. Like the Fed, it had district sub-treasuries that performed nearly all the financial functions that the Fed later took over: providing credit to move the crops in autumn, managing government debt, and so forth. But after the severe 1907 financial crisis, a National Monetary Commission was reformed. Under the then-Republican administration, it recognized a need for more active government intervention to prevent future financial crises. However, the leading bankers sought to use the crisis as an opportunity to grab power for Wall Street, away from the Treasury. In this sense, the Fed was founded in large part to take monetary control away from Washington’s elected officials and appointees, and privatize the supply of money and credit. So its place in the U.S. financial and economic structure is to allocate credit, primarily to serve Wall Street financial interests. That explains the insistence on the financial class here and abroad in insisting on an “independent” central bank. It means that instead of serving the public interest, it serves the interests of the banking class. The hoped-for transformation of commercial banking into long-term industrial banking was not achieved.

Durable Goods, Stock Market, Fed in the Driver's Seat & Why - After reading Lee Adler of the Wall Street Examiner's article, I asked him, "Why is it the Fed's job to be propping up the stock market? Doesn't it make the whole market a Fed-controlled game, rather than what it started as - a mechanism for companies to raise money and people to invest in public companies?"Lee answered: "Bernanke has made no bones about it. He sees the stock market as a legitimate instrument of policy manipulation. It's his biggest tool, much bigger than the ones between his ears and his legs. The Fed works for the banks, and the capital markets exist as a means for 'capitalists' to extract wealth from the public. Stock markets weren't started for the purpose of enriching the public, that's for sure... The Fed has two clients, the US Treasury, and the banking system. It operates to make sure that they stay in business."Lee also noted that the history of the Fed is replete with a variety of programs where it tried to manipulate something. "The stock market manipulation is relatively new as an overt policy tool, but the Fed can't manipulate indefinitely. Eventually the unintended consequences will rise up and bite it in the ass."

Who Captured the Fed? - In principle, the Fed could stand up to the bankers, pushing back against all specious arguments. In practice, unfortunately, the New York Fed and the Board of Governors are quite deferential to financial-sector “experts.” Bankers are persuasive; many are smart people, armed with fancy models, and they offer very nice income-earning opportunities to former central bankers. We have lost track of the number of research notes from major banks pleading for easier credit, lower capital requirements, delay in implementing financial reforms or all of the above. In recent decades the Fed has given way completely, at the highest level and with disastrous consequences, when the bankers bring their influence to bear – for example, over deregulating finance, keeping interest rates low in the middle of a boom after 2003, providing unconditional bailouts in 2007-8 and subsequently resisting attempts to raise capital requirements by enough to make a difference. As the American economy begins to improve, influential people in the financial sector will continue to talk about the need for a prolonged period of low interest rates. The Fed will listen. This time will not be different.

Fed's Action Prevented 'Meltdown' - The Federal Reserve's response to the 2008 financial crisis prevented a more severe recession, Chairman Ben Bernanke said in a comprehensive defense of the central bank's actions. The Fed's efforts prevented a "total meltdown" of the financial system at a time when fears of a second Great Depression were "very real," Mr. Bernanke said Tuesday at the third of his four lectures at George Washington University in Washington. "I think the view is increasingly gaining acceptance that without the forceful policy response that stabilized the financial system in 2008 and early 2009, we could've had a much worse outcome in the economy," he said.The Fed chief defended the central bank's intervention to stop investment bank Bear Stearns Cos. and insurer American International Group Inc. from collapsing, saying the Fed's moves prevented greater shocks to the global financial system.

The Dangers of an Interventionist Fed - John Taylor - America has now had nearly a century of decision-making experience under the Federal Reserve Act, first passed in 1913. Thanks to careful empirical research by Milton Friedman, Anna Schwartz and Allan Meltzer, we have plenty of evidence that rules-based monetary policies work and unpredictable discretionary policies don't. Now is the time to act on that evidence. The Fed's mistake of slowing money growth at the onset of the Great Depression is well-known. And from the mid-1960s through the '70s, the Fed intervened with discretionary go-stop changes in money growth that led to frequent recessions, high unemployment, low economic growth, and high inflation. In contrast, through much of the 1980s and '90s and into the past decade the Fed ran a more predictable, rules-based policy with a clear price-stability goal. This eventually led to lower unemployment, lower interest rates, longer expansions, and stronger economic growth. Unfortunately the Fed has returned to its discretionary, unpredictable ways, and the results are not good. Starting in 2003-05, it held interest rates too low for too long and thereby encouraged excessive risk-taking and the housing boom. It then overshot the needed increase in interest rates, which worsened the bust. Now, with inflation and the economy picking up, the Fed is again veering into "too low for too long" territory. Policy indicators suggest the need for higher interest rates, while the Fed signals a zero rate through 2014.

Former Fed Governor Warns of Dangers of Proposed Reforms - Former Federal Reserve governor Laurence Meyer said proposed reforms could handcuff the central bank’s authority to respond to another financial crisis and further infuse politics into what is supposed to be an independent body. In testifying before Congress’s Joint Economic Committee, Meyer said Tuesday that a proposal to end the Fed’s dual mandate to keep prices stable and unemployment low contains “clearly partisan” provisions. “Recognize that the greatest threat to the stability of long-term inflation expectations is an assault on the independence of the Fed’s monetary policy decisions,” Meyer said, according to prepared remarks. He served as a Fed governor from 1996 until 2002. He is now senior managing director at Macroeconomic Advisers. The committee’s vice chairman, Kevin Brady (R., Texas), proposed legislation earlier this month to make controlling inflation the sole focus of the Fed as part of an effort to strengthen the value of the dollar.

Democrats to Seek Confirmation of Fed, FDIC Nominees Before Week’s End - Senate Democrats will push for the confirmation of two nominees to the Federal Reserve Board of Governors as well as three outstanding nominees to the Federal Deposit Insurance Corp. before lawmakers leave Washington for a two-week recess, a senior Democratic leadership aide said Wednesday. In order for the nominees to be confirmed, every single senator must agree not to object, which is generally difficult to accomplish. The Senate Banking Committee will vote on Thursday on the nominations of Jerome Powell and Jeremy Stein to be members of the Fed’s Board of Governors. Given the Democratic majority on the committee, the two are expected to be approved by the panel. Powell, a Republican who served in President George H.W. Bush‘s administration, and Stein, a Democrat who is an economist at Harvard University, were nominated by President Barack Obama in December to serve on the Fed board. Democrats hoped that by packaging the two together, they would encounter less resistance by Republicans. The pending FDIC nominees are Martin Gruenberg to be the agency’s chairman, Thomas Hoenig to be its vice chairman and Jeremiah Norton to be another member of its board. The administration also nominated Thomas Curry to be Comptroller of the Currency, which regulates national banks. The banking committee has already approved the nominations of Gruenberg, Curry and Hoenig, a former president of the Federal Reserve Bank of Kansas City.

Republican Senator to Block Fed Nominees - At least one Republican senator plans to oppose President Barack Obama‘s nominees to fill two vacancies on the Federal Reserve‘s Board of Governors, scuttling their chances of getting confirmed before lawmakers leave Washington for two weeks. Sen. David Vitter (R., La.) will oppose Obama’s two picks for the central bank’s board over concerns that they would hew too closely to Fed Chairman Ben Bernanke, a spokesman for Vitter said Wednesday. “I refuse to provide Chairman Bernanke with two more rubber stamps who approve of the Fed’s activist policies,” Vitter said in a statement to Dow Jones Newswires on Wednesday. Senate Democrats had planned to push for confirmation of the two Fed nominees, as well as three outstanding nominees to the Federal Deposit Insurance Corp., before lawmakers leave Washington for a two-week recess, according to a senior Democratic leadership aide. However, Vitter’s opposition prevents the confirmations from being approved by unanimous consent, which requires all 100 senators to agree on the measure.

Where the Fed’s Profits Come From - Financial documents released by the Federal Reserve last week showed that 2011 was the second-most-profitable year for the U.S. central banking system. Net income totaled $77.4 billion, down only slightly from $81.7 billion in 2010. That’s more than twice what the Fed was earning before the 2008-09 financial crisis. It’s also more than double the amount earned by Exxon, Microsoft or Apple. So why have the Fed’s profits risen so much in the past two years? Two reasons: The Fed has created more money than usual and also has invested it in higher-paying assets. Here’s why that has happened. Besides providing money we use in the form of cash, the Fed adds money to the banking system to adjust the level of interest rates. To stimulate the economy by lowering interest rates, the Fed creates money and uses it to purchase Treasury securities and other government debt, thereby releasing additional money into the banking system. Since the Great Recession began, the Fed’s stimulus policies have tripled the size of its balance sheet.

Fed Watch: Inflation: Still Nothing to See Here - The Februrary Personal Income and Outlays report came out this morning, and with it a fresh read on the Federal Reserve's preferred inflation measure, the PCE price index. On a year-over-year basis, headline inflation is trending down to the 2% target, while core is settling in just below that target. As a reminder, the Fed targets headline over the longer run, but watches core as a signal to where headline is headed. Headline is trending down to core, as expected. The Fed was right to dismiss last year's energy-induced headline increase as a temporary phenomenon. Is there any near term trends to be concerned about? The three-month core trend edged down a notch to just above 2%: Still less than the rise experienced in the first part of 2011. What about the path of prices? Still tracking along a trend below that of prior to the recession: Bottom Line: Inflation remains contained - by itself, price trends provide no reason for the Fed to turn hawkish. Moreover, there is nothing here to stop Federal Reserve Chairman Ben Bernanke from easing policy should the US recovery falter.

Floodgates - Krugman - Once again, we’re hearing warnings — including from some people who should know better — that the “floodgates” of inflation may be about to open. It’s funny how repeated total failures of prediction don’t seem to diminish the confidence of inflationistas in their insights. So this may be a waste of time. Still, here’s the Fed’s preferred measure of inflation, the personal consumption expenditures deflator, measured on a 6- month basis (short enough to catch relatively short-term trends, long enough to smooth out the noise): You may recall that early last year there was a huge fuss over a temporary rise in inflation, which was widely portrayed as the harbinger of terrible things to come. Bernanke and others tried to point out that it was mainly about gasoline, with nothing much going on in measures of domestically generated inflation; for this they (and I) were attacked fiercely. But sure enough, inflation came down. Taking a longer view, we’ve had dire warnings about runaway inflation for more than three years at this point. When do people start to consider that maybe they have the wrong model?

Personal Consumption Expenditures: Price Index Update - The monthly Personal Income and Outlays report was published today by the Bureau of Economic Analysis. The first chart shows the monthly year-over-year change in the personal consumption expenditures (PCE) price index since 2000. I've also included an overlay of the Core PCE (less Food and Energy) price index, which is Fed's preferred indicator for gauging inflation. The latest Headline PCE price index YOY rate of 2.32% is a decrease from last month's 2.41% (an upward revision from 2.36%). The Core PCE index of 1.90% is a decrease from the previous month's 1.93% (an upward revision from 1.88%). I've calculated the index data to two decimal points to highlight the change more accurately. It may seem trivial to focus such detail on numbers that will be revised again next month (the three previous months are subject to revision and the annual revision reaches back three years). But PCE is a key measure of inflation for the Federal Reserve, and the price increase in oil and gasoline, although now well off their interim highs, puts consumer behavior in the spotlight. In the past, a core PCE range of 1.75% to 2% is generally mentioned as the target for the Federal Reserve's price-stability mandate. However, the Fed has now explicitly identified 2% as the long-term target:

Bernanke muted on US economic health - A rapid fall in US unemployment may not be sustainable unless the economy starts to grow faster, said Ben Bernanke in a speech on Monday that suggests monetary policy will stay easy. The US Federal Reserve chairman said that the decline in the unemployment rate from 9.1 per cent to 8.3 per cent over the past six months may reflect a one-off bounce back from big job cuts in 2008 and 2009. "To the extent that this reversal has been completed, further significant improvements in the unemployment rate will probably require a more-rapid expansion of production and demand from consumers and businesses, a process that can be supported by continued accommodative policies," said Mr Bernanke in a speech at the National Association of Business Economists conference in Arlington, Virginia. The Fed has been grappling with a divergence between stronger labour market data and weaker numbers on demand and output growth. Mr Bernanke's explanation suggests that both phenomena are real but that the strength of the labour market will be temporary. If underlying growth is quite weak and there is still a lot of slack in the labour market then it makes sense for the Fed to continue with easy monetary policy in order to speed up the recovery.

Bernanke Tells ABC Economic Recovery Has ‘Long Way To Go’ - The U.S. economy is not yet on a certain path to a full recovery, Federal Reserve Chairman Ben Bernanke said in a televised interview with ABC News on Tuesday. “It’s far too early to declare victory,” Bernanke said in an interview with ABC’s Diane Sawyer, according to a transcript of the interview to be aired Tuesday night on “World News.” The Fed chief acknowledged a brightening in the recent economic data, noting that new jobs have been created and that measures of consumer and business sentiment have improved. And Europe’s fragile economy has become less worrisome recently, he said. (Watch an excerpt from the interview.) “The financial system looks stronger and more stable,” Bernanke said. However, he cautioned that the housing market is still “pretty flat,” long-term unemployment remains a problem and that the current 8.3% jobless rate is still too high.“We need to be cautious and make sure this is sustainable,” Bernanke said. “We haven’t quite yet got to the point where we can be completely confident that we’re on a track to full recovery.”

Transcript: Diane Sawyer Interviews Ben Bernanke - ABC News

Bernanke, the Anti-Garbo - Investors are said to hang on every word spoken by the chairman of the Federal Reserve. The current chairman, Ben S. Bernanke, must be testing their patience. So far this week, Mr. Bernanke has delivered a major address on unemployment and lectured students at George Washington University on the Fed’s response to the financial crisis. He is on the cover of the current issue of The Atlantic magazine. An interview with Mr. Bernanke will be broadcast Tuesday night on ABC World News. Last week he delivered lectures at George Washington about the history of the Federal Reserve on Tuesday and Thursday, testified before Congress about the European crisis on Wednesday, and gave a brief speech Friday at a conference on central banking. Previous Fed chairmen gave speeches and appeared before Congress, but otherwise spoke very little in public. Mr. Bernanke has broken cleanly with that tradition, seeking to explain the Fed’s mission and methods through a variety of means, including town hall meetings, television interviews and press conferences.

Chicago Fed: Economic Growth in February "near average" - The Chicago Fed released the national activity index (a composite index of other indicators): Index shows economic growth near average in February Led by weaker production-related indicators, the Chicago Fed National Activity Index decreased to –0.09 in February from +0.33 in January. ... The index’s three-month moving average, CFNAI-MA3, increased from +0.22 in January to +0.30 in February—its highest level since May 2010. February’s CFNAI-MA3 suggests that growth in national economic activity was above its historical trend. The economic growth reflected in this level of the CFNAI-MA3 suggests limited inflationary pressure from economic activity over the coming year. This graph shows the Chicago Fed National Activity Index (three month moving average) since 1967. This suggests growth near trend in February - still not strong growth.

Chicago Fed: US Economic Activity "Near Average" In February - The plot thickens for deciphering the next move for the business cycle… or does it? The Chicago Fed National Activity Index (CFNAI)—a broad measure of the U.S. economy—slipped last month. "Two of the four broad categories of indicators that make up the index deteriorated from January, but of these two, only the production and income category made a negative contribution to the index in February," the Chicago Fed reports. On the other hand, monthly numbers are noisy, which is why we're told to pay closer attention to CFNAI's three-month moving average, which "suggests that growth in national economic activity was above its historical trend." Putting the index's three-month average in historical perspective certainly perks up the case for thinking optimistically. Indeed, this average rose to 0.30 in February from 0.22 in January—the highest in two years. How should we read this information? The Chicago Fed advises that a value below -0.70 after a period of economic expansion "indicates an increasing likelihood that a recession has begun." By that rule, the latest reading suggests that the economy will continue growing for the foreseeable future.

Fourth-quarter GDP unrevised at 3.0 percent -(Reuters) - The economy expanded as expected in the fourth quarter while personal income grew at a much faster pace than previously thought, which should help underpin spending this quarter. Gross domestic product increased at a 3.0 percent annual rate, the quickest pace since the second quarter of 2010, the Commerce Department said in its final estimate on Thursday, unrevised from last month's estimate. That was in line with economists' expectations. The economy grew at a 1.8 percent rate in the third quarter. However, personal income was $13.162 trillion at a seasonally adjusted annual rate, $3.3 billion more than previously reported. Disposable income was $10.6 billion more than previously thought, likely reflecting the strengthening labor market. Gross domestic income, which measures output from the income side, increased at a 4.4 percent rate - the fastest since the first quarter of 2010 - from a 2.6 percent rise in the third quarter. The department also said after-tax profits increased at a 1.1 percent rate, slowing from 2.7 percent the prior quarter. The slowdown in profits reflects the increase in wage costs as companies step up hiring.

GDI: An Alternate Measure Showing Stronger U.S. Growth - The Commerce Department has (at least) two ways to measure the growth and size of the overall U.S. economy. One is to add up all the value of all the goods and services produced in the economy in a quarter or a year. That’s the gross domestic product, or GDP. The other is to add up all the income received in the economy, wages and interest and profits and so on. That’s gross domestic income, or GDI. They should tell the same story, but because it’s so hard to accurately measure a $15-trillion economy, and because the two measures rely on different data sources, they don’t always match. The GDP gets all the attention (partly because it comes out earlier), but some economists argue that the GDI may be a more meaningful measure, particularly at turning points in the economy. “Placing an increased focus on GDI may be useful in assessing the current state of the economy,” Federal Reserve Board economist Jeremy J. Nalewaik wrote in a 2006 working paper. With its third revision of fourth-quarter GDP, issued Thursday, the agency also released its GDI estimates. Here’s what they show:

- GDP Q4 up 3.0% GDI Q4 up 4.4%

- GDP Q3 up 1.8% GDI Q3 up 2.6%

- FULL YEAR 2011 GDP: up 1.7% FULL YEAR 2011 GDI: up 2.1%

Q4 GDP and GDI - Early this morning the BEA released the third estimate of Q4 GDP. The BEA reported that Real gross domestic product "increased at an annual rate of 3.0 percent in the fourth quarter of 2011", the same as the previous estimate. Also in the release, the BEA reported the real gross domestic income (GDI) increased at a 4.4% annualized rate in Q4. There are really two measures of GDP: 1) real GDP, and 2) real Gross Domestic Income (GDI). A research paper in 2010 suggested that GDI is often more accurate than GDP. For a discussion on GDI, see from Fed economist Jeremy Nalewaik, “Income and Product Side Estimates of US Output Growth,” Brookings Papers on Economic Activity. During the worst period of the recession, GDI fell more than GDP as Nalewaik noted. In subsequent revisions, GDP was revised down showing the economy contracted more than originally reported - and closer to the original GDI reports. The opposite has happened over the last two quarters - GDI is showing stronger growth than GDP - and this suggests that 2nd half 2011 GDP might be revised up with the next annual revision that will be released on July 27th (Revised Estimates will be provided for years 2009 through 2011).

Discrepancies Between National Income and GDP, by Dean Baker: Binyamin Appelbaum has a NYT blogpost suggesting that the economy may be growing more rapidly than the GDP imply based on the fact that national income has grown more rapidly in recent quarters. ... Appelbaum points to a new paper that suggests that we should be taking an average of GDP growth and income growth as our actual measure of economic growth. If we go this route, then it implies that the recovery has been somewhat stronger (and the recession steeper) than the standard measure of GDP growth. There is an alternative story. David Rosnick and I analyzed the movement of the statistical discrepancy and found a strong inverse correlation between the size of the statistical discrepancy and capital gains in the stock market and housing. This meant, for example there was a large negative statistical discrepancy in 1999 and 2000 at the peak of the stock bubble (i.e. income exceeded output) which disappeared after the bubble burst. The same thing happened in the peak years of the housing bubble, 2004-2007. In that case also, the large gap between the income side measure and the output side measure disappeared after the bubble burst.

Will the 'Real' GDP Please Stand Up? - How do you get from Nominal GDP to Real GDP? You subtract inflation. The Bureau of Economic Analysis (BEA) uses its own GDP deflator for this purpose, which is somewhat different from the BEA's deflator for Personal Consumption Expenditures and quite a bit different from the better-known Bureau of Labor Statistics' inflation gauge, the Consumer Price Index. Now that we have the third estimate on Q4 GDP, I've updated my charts showing quarterly Real GDP since 1960 with the official and three variant adjustment techniques. The first chart is the official series as calculated by the BEA with the GDP deflator. The second starts with nominal GDP and adjusts using the PCE Deflator, which is also a product of the BEA. The third adjusts nominal GDP with the BLS (Bureau of Labor Statistics) Consumer Price Index for Urban Consumers (CPI-U, or as I prefer, just CPI). The forth chart, prompted by several requests, adjusts nominal GDP using the Alternate CPI published by economist John Williams at shadowstats.com. Suggestion: Click on any of the charts below and use the links at the top of the chart page to toggle between the versions for a closer comparison.

No, Really, Austerity is A Really Stupid Idea - Now that we've gotten the final revision to 4Q GDP, let's take a look at the data for the last two years to see where we're growing and where we're not. The above chart simply shows the percentage change in GDP from the previous quarter. The first two quarters of 2010 were good, but then we saw a slowdown in the second half 2010. The first half of 2011 was very slow, but we see a pick-up towards the end of the year. Overall, we've seen PCEs bounce all over the place. First, notice that durables goods have grown by strong amounts on a quarter to quarter basis for the last two years. In contrast, non-durable goods purchases have been weak for the last year, as have service expenditures. Remember that durable goods purchases comprise the smallest amount of PCEs, coming in about 12%. This charts tells me that people are doing more for themselves -- that is, instead of hiring a landscape service, they're mowing their own yards, etc.. Investment also provides some interesting insight. First, we see decent quarter to quarter figures in equipment and software (the gold line). However, investment in CRE (the blue line) is fairly weak. Residential investment (the green line) is terrible, save for the 2Q10 and last quarter.

Fed Watch: Slow and Steady - Looking at the spending component of this morning's Personal Income and Outlays report for February, it still pays to focus on the path of spending rather than to become terribly hopeful or despondent about the twists and turns along that path: The 0.5% gain in February compensated for some earlier weakness in the numbers, while the overall trend holds - spending is rising about 0.18 percent per month compared to 0.24 percent prior to the recession. Spending was supported by a drop in the saving rate, down to 3.7% from 4.3% the previous month. This likely reflects borrowing for new auto purchases - note the stronger trend in durable goods spending: The acceleration in auto sales is clearly supporting this trend since the middle of last year. Apparently, what's good for Detroit is still good for America. The importance of autos in sustaining spending begs the question of what will occur when pent up demand is satisfied? Hopefully, income growth will accelerate as the labor market improves. Otherwise, households will need to take on additional debt or running down saving rates to hold the current trend in place. Bottom Line: Consumer spending continues to rise, although the sustainability is still called into question because of the reliance of pent-up demand and falling saving rates to support underlying trends.

CEOs Expects Marked Economic Improvement This Year - U.S. corporate leaders are expecting to see a marked improvement in the economy this year as more chief executives expect sales, investment and hiring to grow in the next six months. Business Roundtable‘s first-quarter survey of 128 CEOs, released Wednesday, found that 81% expect sales to increase in the next six months–a 12 percentage point gain over the prior quarter’s survey–and 48% say their firms will increase U.S. capital spending, a 16 point jump. And 85% of those polled said staffing at their firms will hold steady or grow in the coming months. The outlook survey’s index–a composite of CEO expectations for the next six months of sales, capital spending and employment–increased to 96.9 in the first quarter of this year, from 77.9 in the fourth quarter of 2011. Readings above 50 reflect growth. The survey results “indicate greater overall economic optimism among member CEOs compared to last quarter,” Boeing Co. CEO Jim McNerney said in a statement. McNerney is chairman of the Business Roundtable.

Improving Housing Market Driving Economy: Jamie Dimon - The U.S. housing market is very close to a bottom and there are already signs its improvement is giving a boost to the overall economy, JPMorgan Chase CEO Jamie Dimon told CNBC Wednesday. "I believe we’re very close to the inflection point. People look at prices that are still coming down but all the other signs are flashing green," Dimon said during a job fair in New York for hiring veterans. ... "the shadow inventory everyone talks about is lower today than it was 12 months ago. It will be a lot lower 12 months from now," he said. Distressed inventory "is actually coming down, not going up. Homes for sale are about half what they were four years ago. You could come up with a pretty bullish case. If the economy grows, housing gets better, quicker."

Whose Recovery? - Robert Reich - The Commerce Department reported Thursday that the economy grew at a 3 percent annual rate last quarter (far better than the measly 1.8 percent third quarter growth). Personal income also jumped. Americans raked in over $13 trillion, $3.3 billion more than previously thought. Yet it’s almost a certainly that all the gains went to the top 10 percent, and the lion’s share to the top 1 percent. Over a third of the gains went to 15,600 super-rich households in the top one-tenth of one percent. We don’t know this for sure because all the data aren’t in for 2011. But this is what happened in 2010, the most recent year for which we have reliable data, and there’s no reason to believe the trajectory changed in 2011 or that it will change this year. In fact, recoveries are becoming more and more lopsided. The top 1 percent got 45 percent of Clinton-era economic growth, and 65 percent of the economic growth during the Bush era. According to an analysis of tax returns by Emmanuel Saez and Thomas Pikkety, the top 1 percent pocketed 93 percent of the gains in 2010. 37 percent of the gains went to the top one-tenth of one percent. No one below the richest 10 percent saw any gain at all.

Gas Prices Have Taken Air Out of US Recovery: Welch - What looked to be a fairly robust economic recovery has turned lackluster thanks to rising gas prices and uncertainty over demand, according to author and former General Electric CEO Jack Welch. When gross domestic product growth registered a surprising 3 percent for the fourth quarter last year, Welch figured the U.S. economy was about to embark on strong growth that would outpace many of its global competitors. But since then, an unexpected surge of prices at the pump coupled with continuing tightness in credit has him rethinking his position. "It's not taking off. We're sort of relatively strong but not booming," Welch said in a CNBC interview. "I am normally to one extreme or another and I'm a little shaken about not knowing where this is going." Gasoline is nearing $4 a gallon nationwide, with the peak driving season still to come. At $3.91 a gallon, gas is up 22 cents over the past month and 33 cents from a year ago, according to AAA. The price is just 20 cents from its record high in July 2008. Despite the rise, consumer confidence had been increasing steadily. But new numbers released Tuesday showed fear creeping in about energy inflation, and the stock market registered what has become a rare losing day amid the economic unease.

Gasoline Prices and the Economy - Mark Zandi - Nothing is worse for our economy than rising energy prices. They act like a pernicious tax increase, forcing us to spend more filling up and leaving less for everything else. But unlike taxes, money spent on auto fuel doesn't pay teachers' salaries, pave roads, or lower the national debt. Indeed, much of it ends up in the Middle East. Every penny increase in the cost of a gallon of gas costs American consumers $1.25 billion over the subsequent year. With gas prices up almost 60 cents per gallon since the end of 2011, U.S. pocketbooks are set to take a hit of approximately $75 billion this year. By comparison, the 2 percentage-point cut in payroll taxes that took effect in January 2011 is worth about $100 billion. If gasoline goes much higher, the payroll tax break will essentially cover the higher cost of fuel. Gasoline prices always rise at this time of year, because demand picks up as people begin to travel more, and refiners blend in summer additives to protect the environment. This year, moreover, refining capacity is in shorter supply; refiners have been shutting plants, seeing slimmer profits down the road. Two large Philadelphia refineries are only the latest examples.

The Economy’s Great Fall: Are the Losses Permanent? -- DeLong and Summers, the debate over potential output, and whether Bernanke has the courage, foresight, and persuasiveness to follow Greenspan's lead: The Economy’s Great Fall: Are the Losses Permanent? I wrote this before Bernanke's speech on the labor market on Monday. He says, echoing the topic of the column:Is the current high level of long-term unemployment primarily the result of cyclical factors, such as insufficient aggregate demand, or of structural changes, such as a worsening mismatch between workers' skills and employers' requirements? ... I will argue today that ... the continued weakness in aggregate demand is likely the predominant factor. So maybe the structural impediment, inflation hawk types at the Fed will be vanquished after all. We shall see. [See Tim Duy's comments on as well.]

Bill Gross: "The Game As We All Have Known It Appears To Be Over" - First it was Bob Janjuah throwing in the towel in the face of central planning, now we get the same sense from Bill Gross who in his latest letter once again laments the forced transfer of risk from the private to the public sector: "The game as we all have known it appears to be over... moving for the moment from private to public balance sheets, but even there facing investor and political limits. Actually global financial markets are only selectively delevering. Gross' long-term view is well-known - inflation is coming: "The total amount of debt however is daunting and continued credit expansion will produce accelerating global inflation and slower growth in PIMCO’s most likely outcome." The primary reason for Pimco's pessimism, which is nothing new, is that in a world of deleveraging there will be no packets of leverage within the primary traditional source of cheap credit-money growth: financial firms. " it is your duty to try to escape today’s repression. Your living conditions are OK for now – the food and in this case the returns are good – but they aren’t enough to get you what you need to cover liabilities. You need to think of an escape route that gets you back home yet at the same time doesn’t get you killed in the process. You need a Great Escape to deliver in this financial repressive world." In the meantime Gross advises readers to do just what we have been saying for years: buy commodities and real (non-dilutable) assets: "Commodities and real assets become ascendant, certainly in relative terms, as we by necessity delever or lever less."

Financial Armageddon: 'The American Economic Model Is Broken': A new survey of U.S. household finances by British research firm Absolute Strategy Research suggests that Americans are not only pooh-poohing the notion that an economic recovery is at hand, they are becoming resigned to the fact that the longer-term outlook isn't all that much better. A staggering 63% of respondents across the political spectrum feel that the American economic model is broken. Individuals surveyed do not agree that the prevailing paradigm facilitates equal opportunity, or that hard work and skill are rewarded. This grim view of the status quo is also represented in respondents' concerns about fairness and the distribution of wealth: a quarter of those surveyed say the next administration should make closing the gap between the rich and poor a top policy priority, and half want the next administration to make sure the wealthiest Americans pay a “fair share” of taxes. And a mere 20% of those polled believe wealth and income is distributed fairly. This survey also highlights the extent to which Americans are dissatisfied with those responsible for managing the American economy. Respondents across the political spectrum agree that policymakers have not done a good job in handling the economy over the last year, and that a focus on stimulating economic growth should be the top priority for the next administration. Republicans and Independents are the most critical of economic policymakers, but two thirds of Democrats are also critical of the handling of the economy.

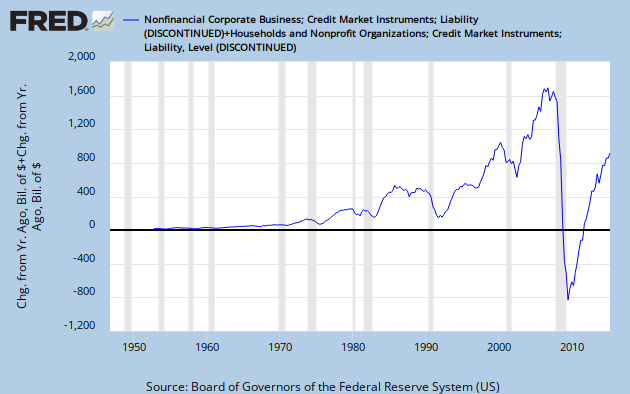

The balance sheet recession, charted - Nomura’s Richard Koo has been banging on about the similarities between Japan’s balance sheet recession and the current financial malaise for a long while. His main point has always been that the financial system won’t recover unless corporates and households complete their deleveraging journey. On Wednesday he provides some charts to help illustrate the journey’s progress thus far. But there’s also the point that there was never really the same corporate issue in the US, as there was in Japan. Hence it’s the following chart, depicting the US household deleveraging journey, which is perhaps much more pertinent to the comparison: Indeed, the similarities strike us as much more evident. As Koo himself notes: Let us now look at the situation at US households with their damaged balance sheets. As Figure 4 shows, their behavior since 2008 has mirrored that of Japanese households and companies over the last decade and a half: they are both reducing financial liabilities (paying down debt) and increasing financial assets (savings) in spite of zero interest rates. Together, the household and corporate sectors are now net savers to the tune of 5.8% of GDP. That this surplus of private savings is occurring at a time when interest rates are at zero is a clear indication the US is in a balance sheet recession triggered by the first crash in house prices in seven decades. All of which supports the idea that lessons from Japan’s Great Depression should be respected, we would say.

Chicago Fed President Charles Evans has an ingenious plan to save the American economy. Listen to it, Ben Bernanke. - Can talking differently boost the economy? It sounds like a silly idea, but as long as the talkers have the right jobs, there’s considerable theoretical reason to believe they can make a huge difference. New research from the Federal Reserve Bank of Chicago shows that talk does matter and that the Fed could significantly improve the economy by choosing its words better. The messenger for all this was Charles Evans, the president of the Chicago Fed, who is waging a low-profile war to revive the economy by changing how the Fed speaks. Last week, at the annual Brookings Papers on Economic Activity conference, Evans tried to make this case to an elite audience of economists and policymakers. His paper, “Macroeconomic Effects of FOMC Forward Guidance,” co-written with Chicago Fed staffers, is one of the most important policy arguments out there today, arguing that the central bank could significantly stimulate the economy simply by rephrasing its statement that “economic conditions—including low rates of resource utilization and a subdued outlook for inflation over the medium run—are likely to warrant exceptionally low levels of the federal funds rate through late 2014.”

Demand, not Supply is Holding Back the Recovery - Federal Reserve Chairman Ben Bernanke said on Monday that he believes our unemployment problem is due mainly to lack of economic demand: Is the current high level of long-term unemployment primarily the result of cyclical factors, such as insufficient aggregate demand, or of structural changes, such as a worsening mismatch between workers' skills and employers' requirements? ... I will argue today that, while both cyclical and structural forces have doubtless contributed to the increase in long-term unemployment, the continued weakness in aggregate demand is likely the predominant factor. This is an important debate because if the fall in unemployment is mostly structural, there's little that monetary and fiscal policy can do to help to speed the recovery. But if lack of demand is the main culprit, then replacing the lost demand through aggressive policy can help us recover faster

What we need for economic recovery - Consider three leading explanations for the current weak economic conditions. First, a new paper from James Stock and Mark Watson identifies demographic shifts as an important determinant of poor current economic conditions, and a likely problem going forward: …barring a new increase in female labor force participation or a significant increase in the growth rate of the population, these demographic factors point towards a further decline in trend growth of employment and hours in the coming decades. Applying this demographic view to recessions and recoveries suggests that the future recessions with historically typical cyclical behavior will have steeper declines and slower recoveries in output and employment. Second, as Karl has argued, the economy is waiting for “the kick” of an increase in sales of durables like housing and autos. Third, you have low house prices in holding back the economy by weakening household balance sheets. My question is this: do not all of these factors point towards more immigration to drive both a recovery now and a recovery from the decline in the long term economic trends? In The Great Stagnation, Tyler Cowen identified lots of immigration as one of the three main kinds of low hanging fruit that helped drive our earlier growth:

Banking Mysticism - Krugman - Reading the comments on my Steve Keen post, I had an insight: banking is where left and right meet. Both the Austrians — who believe that whatever the market does is right, unless it’s fractional reserve banking, which is somehow terrible — and the self-proclaimed true Minskyites view banks as institutions that are somehow outside the rules that apply to the rest of the economy, as having unique powers for good and/or evil. I guess I don’t see it that way. As I (and I think many other economists) see it, banks are a clever but somewhat dangerous form of financial intermediary, one that exploits the law of large numbers to offer a better tradeoff between liquidity and returns, but does so at the cost of taking on very high leverage, with all the risks that entails.The super-high leverage of banks, and the role of bank deposits as a key form of liquid assets, means that banks broadly defined are usually central players in financial crises. But that’s a quantitative thing, not a qualitative thing. I know I’ll get the usual barrage of claims that I don’t understand banking; actually, I think I do, and it’s the mystics who have it wrong.

Philip Pilkington: Krugman Makes Accusations of Fundamentalism to Defend His Own Dogma - You’re at a party and you’re having a conversation. One person interrupts, giving his view without engaging with what you’re saying. It is a presumptuous act based on the assumption that he – the speaker – already know everything there is to know about the conversation and so can simply steamroll over what everyone else says. Paul Krugman has just done the intellectual equivalent on a blog ‘contesting’ Steve Keen’s recent piece criticising his model of debt dynamics. Keen has raised these issues before and Krugman has politely ignored them. Not surprising. But while ignoring a critique is one thing, shouting over one is quite another altogether. Keen, on the other hand, has read Krugman’s paper in depth and raised criticisms that are absolutely fundamental. Krugman, it appears, simply scanned Keen’s post and then wrote up a short post accusing Keen of some sort of Minskyian ‘fundamentalism’. Keen’s criticism is that Krugman has not understood Minsky’s argument about debt dynamics at all and this has led him to construct an inaccurate debt model. Krugman claims that Keen is attacking him because Keen somehow thinks that Minsky’s analysis is Holy Writ. This is complete nonsense. Keen is attacking Krugman because his frankly lazy reading of Minsky has led him to construct a vastly inferior model to the one that Minsky’ work suggests. The essence of the problem is that Krugman assumes a ‘loanable funds’ model. Banks do not, in fact, need reserves in order to make loans. They make loans first – ex nihilo, if you will – and raise the reserves later. This means that the only real constraint on bank lending is the interest rate as set by the central bank.

The Central Flaw in Krugman’s Argument Against Keen - The key failing in Krugman’s response to Steve Keen’s response to Krugman’s paper (PDF) is here: If I decide to cut back on my spending and stash the funds in a bank, which lends them out to someone else, this doesn’t have to represent a net increase in demand. Krugman assumes here that people have to save (spend less) in order for other people to borrow. It’s actually the fundamental assumption, the sine qua non, of his paper (and of Krugman’s beloved IS-LM — the linch-pin of “New” Keynesianism — created by Hicks to subsume Keynes into neoclassicism, and later disclaimed and discredited by Hicks as a “classroom gadget”; see my post, and Philip Pilkington here). But that’s not how things work (and it’s the very assumption that Keen is disputing). I tried to explain this in clear and simple terms here: Think about it: You get $100,000 in wages. Your employers’ bank account is debited, and yours is credited. Your bank can lend against your higher balance; your employer’s bank can’t. Net zero.* You spend $75,000. It’s transferred from your account to other people’s/businesses’ bank accounts. Their banks can lend more, yours can lend less. Is the total stock of loanable funds affected by whether the money is on deposit at your bank, your employer’s bank, or the banks of people you bought stuff from? No.

On bank lending’s creating deposits and Paul Krugman’s response - Steve Keen - Paul Krugman has just commented (twice) on my most recent blog about my paper for INET. In one sense, I’m delighted. The Neoclassical Establishment (yes Paul, you’re part of the Establishment) has ignored non-Neoclassical researchers like me for decades, so it’s good to see engagement rather than wilful (or more probably blind) ignorance of alternative approaches. There is a bizarre asymmetry in economics: critics of Neoclassical economics like myself read Neoclassical literature avidly, no because we agree with it—far from it—but because we feel obliged to understand why they hold to their counterfactual views on the economy. Most Neoclassical economists, on the other hand, don’t even bother to consider critics within their own ranks—let alone critics from without. So to have a paper referred to is definitely a plus. In another sense, I’m appalled, because Krugman’s comments put on display that very ignorance of Neoclassical literature—let alone of alternative economic thought.

Lending, Velocity, and Aggregate Demand - JKH likes this line in Keen’s response to Krugman:The endogenous increase in the stock of money caused by the banking sector creating new money is a far larger determinant of changes in aggregate demand than changes in the velocity of an unchanging stock of money. It struck me as an empirical question: how do those changes compare in magnitude? I didn’t know offhand. Let’s start with MZM (money of zero maturity, the broadest definition of money), and GDP: There’s about $10 trillion in MZM right now, and GDP (annual spending) is at about $14 trillion.* The money stock turns over about 1.4 times per year. If money supply was unchanged — no new net lending/borrowing — but the musical chairs/logrolling game sped up so money turnover increased by 5%, because people were more optimistic — ready to take chances, consume now while worrying less about later, invest in new housing and productive capacity, etc. (“animal spirits”) — that would add $.7 trillion to aggregate demand. (5% is quite a GDP jump given no new net lending…) Now lets look at annual net borrowing/lending — annual change in debt outstanding for households and nonfinancial firms: