A Look Inside the Fed’s Balance Sheet - Assets on the Fed’s balance sheet contracted a bit in the latest week, dropping to $2.316 trillion from $2.333 trillion. Most of the decline came from a $7.96 billion reduction in liquidity swaps for foreign central banks. Three weeks ago the Fed re-established the swap lines to ensure access to dollars amid the troubles in Europe debt markets. However, reduced demand indicates that conditions are stable enough that overseas banks aren’t willing to tap into the swaps, which carry a penalty rate over other dollar-funding facilities. Separately, the value of the Fed’s mortgage-backed securities also declined this week. The central bank has stopped new purchases of the securities, but the portfolio valued at more than $1 trillion still posts gains and losses. Direct-bank lending continued its decline, getting closer to the precrisis levels of 2007. In an effort to track the Fed’s actions, Real Time Economics has created an interactive graphic that will mark the expansion of the central bank’s balance sheet. See a full-size version. Click on chart in large version to sort by asset class.

US Fed Total Discount Window Borrowings Wed $74.94 Billion… The Federal Reserve's balance sheet shrunk in the latest week as foreign central banks made little use of new currency swap lines with the U.S. central bank.The Fed's asset holdings in the week ended May 26 fell to $2.338 trillion from $2.354 trillion a week earlier, the Fed said in a report released Thursday.The Fed lent out a total of $1.24 billion to foreign central banks in the week ended Wednesday. Separate data from the New York Fed show the Bank of Japan joined the European Central Bank in using the facility.Meanwhile, the Fed report said total discount window borrowing fell to $74.94 billion on Wednesday from $75.86 billion a week earlier. Borrowing by commercial banks through the Fed's discount window dropped to $4.21 billion on Wednesday from $4.63 billion a week earlier.

FRB: H.4.1 Release--Factors Affecting Reserve Balances--May 27, 2010

Fed Says Asset Sales Will Come After Rates Are Raised (Bloomberg) -- The Federal Reserve doesn’t intend to sell any of its securities, including more than $1.1 trillion in mortgage-backed securities, until after it begins raising interest rates, the central bank said in a report to Congress.“The Federal Reserve currently does not anticipate that it will sell any of its securities holding in the near term, at least until after policy tightening has gotten under way and the economy is clearly in a sustainable recovery,” the Fed in its annual report, which was posted on its Web site today.Fed officials led by Chairman Ben S. Bernanke are debating when to reduce the central bank’s balance sheet and withdraw unprecedented monetary stimulus as the economy recovers. The annual report’s reference to asset sales was in line with minutes of the April Fed meeting and identical to the Fed’s February policy report to Congress.

Dissent within the FOMC - Is this the beginning of a Federal Reserve versus regional bank split? Three regional bank presidents indicated they thought the discount rate should be increased by 25 bp to 1 per cent, according to the minutes of the discount rate meetings, released today. None of the Fed governors voted for the action and the nine regional bank presidents also recommended against increasing the rate.An increase to 100bp would leave it at least 75bp above the current federal funds rate, and not far off from its pre-crisis levels of 100bp above the Fed funds rate. The Fed moved the discount rate off of its crisis lows last February.The Fed has emphasised that they don’t view discount rate increases as monetary tightening, and the increases don’t say anything about the timing of the eventual exit from ultra loose monetary policy. Instead, raising the discount rate sets the stage so that at the point when the Fed wants to tighten monetary policy, it can.

The Case for a Fed Rate Hike -Everywhere there are arguments that we are in a "V"-shaped recovery. And there are signs that in fact that is the case. Today we will look at some of those, and then take up the topic of when the Fed will raise rates. We open the case and look at the evidence. Is there enough to come to a real conviction? I think there is. I don’t have access to a graph of M3, though it is still produced by several groups (the Fed stopped several years ago), but that chart would show that even M3 has gone negative. Now, notice that with both graphs you see a large increase beginning in the middle of 2008 as the Fed pumped the money supply in order to inject liquidity into the system. This was basically the $1.25 trillion purchase of mortgages, but toward the end even that was not boosting the money supply as much as it did in the beginning. Why? Partially, because of the following graph.This shows total commercial lending at US banks. It is down almost 25% in less than a year and a half. Notice that in the last recession commercial lending dropped by “only” 18% in 3.5 years.

Fed’s Bullard: Europe Woes Unlikely to Trigger Another Recession - European financial troubles are unlikely to send the world back into recession, and the U.S. may actually benefit from unsettled markets over the near term as investors look for a safe place to preserve their wealth, a U.S. central bank official said Tuesday.Because the trouble in Europe is rooted in government debt problems, there is good reason to think events “will probably fall short of becoming a worldwide recessionary shock,” Federal Reserve Bank of St. Louis President James Bullard said. The official noted the world has seen these types of events before, and “there is nothing intrinsic about such crises that they need to become important shocks to the broader, global macroeconomy.”“It is always possible that “this time will be different” and maybe it will be, but that would be unusual given the historical evidence,” the central banker said.

Fed to Test Tool It May Use Later to Tighten Credit - The U.S. Federal Reserve said Friday it would soon test a tool it could use later on to tighten credit by soaking up cash from the financial system.Signaling that Europe’s debt crisis isn’t derailing the U.S. central bank’s plans to unwind the huge stimulus pumped in during the financial crisis, the Fed said it has scheduled three small sales of term deposits over the next two months.In term deposits, banks set up interest-bearing deposits at the central bank, similar to certificates of deposits that banks offer to retail customers. The facility gives banks an extra incentive to keep their money at the Fed instead of lending it out to companies and households, making credit harder to get.The Fed isn’t expected to make large use of the tool soon. Though the U.S. economy is picking up, credit remains tight and problems in Europe may hurt lending further. But the U.S. central bank wants to be ready in case the economy’s gains speed up and it needs to prevent an outbreak of inflation.The auctions planned through the Fed’s Term Deposit Facility “are a matter of prudent planning and have no implications for the near-term conduct of monetary policy,” the Fed said in a statement.

Fed’s Next Move Could Be Reduced Rate on Dollar-Euro Swaps - The Federal Reserve has a lever it can pull to help European officials combat a worsening financial crisis: Reducing the interest rate it charges on U.S. dollar loans it makes through the European Central Bank to dollar-starved commercial banks in Europe. The move, though not a cure-all, could relieve some of the strains in European money markets. Federal Reserve Bank of St. Louis President James Bullard said the swap lines are "certainly not tapped out," and could provide much more funding if necessary.The loans currently are priced one percentage point above a market rate called Overnight Indexed Swaps (OIS), which tracks the expected path of the Fed's benchmark federal funds rate. The loans are set above OIS to discourage foreign banks from using the government program too aggressively. But the Fed could reduce that penalty to encourage more borrowing and ease some of the financial strain on foreign banks in need of dollars. Whether it chooses to take this step remains to be seen, and will depend in part on how markets behave in the days ahead.

The Fed’s Swap Loans and Libor – OIS Spread - For about two years—from August 2007 to September 2009—fluctuations in the spread between dollar Libor and the overnight index swap (OIS) served as a valuable quantitative indicator of financial stress in the interbank loan market. It also served as a measure of the impact of various government interventions. As shown in the chart, the dollar Libor-OIS spread rose further during the panic in September-October 2008. It then returned to near pre-crisis levels in September 2009 and stayed there until the new crisis in Europe erupted when it started to increase again, attracting the attention of financial analysts and the financial press. Note, however, that the recent increase—visible in the right part of the chart—is very small compared with the jumps in 2007 and 2008. Nevertheless, as part of the European rescue package, the Fed agreed to provide dollar swap loans to the ECB and other central banks so that they could provide dollar loans in the interbank market. Have these swap loans affected the spreads?

Fed’s monetary policy report highlights -The Federal Reserve released its annual monetary policy report to Congress today. It’s good reminder of the year-that-was and provides some modest new insights into the Fed’s plan for the coming years. Here are the highlights: 1. The wealth catch. The Fed reiterated in its annual report that “households’ desire to rebuild wealth” will probably be one of the headwinds to the recovery. And wealth rebuilding - at least in the form of a higher savings rate, has yet to start in earnest. 3. It ain’t over til it’s over. The bulls of the world are taking every fresh housing market indicator to say that the housing collapse is at an end. The bears argue that the high level of foreclosures and the level of housing price increases compare to declines suggests prices have farther to fall. No matter. Even if the bulls are right, municipalities have yet to feel the property value pain, the Fed’s report said. 5. Buyer beware. The Fed knows what happened, but it’s making no claims to know with great confidence where the economy is heading.

The $21bn bail-out item - That’s the amount the Congressional Budget Office estimates the Federal Reserve’s credit programmes cost US taxpayers.Of course, that’s not on a cash basis. The CBO has previously estimated that the Fed will be paying the Treasury around $70bn a year in 2010 and 2011 (compared to payments of between $18bn to $34bn from 2000 to 2008) because of the expected higher yields of the riskier-than-normal assets the US central bank bought to stabilise the economy during the crisis.But, of course, there is risk. They might not pay out. And, in many cases, the Fed paid more for assets than they were worth, discounting for the risk associated with them. And now the CBO has estimated the amount the Fed overpaid - $21bn. Here’s there breakdown.

Fed May Send Record $70 Billion to Treasury, CBO Says (Bloomberg) -- The Federal Reserve will probably transfer record earnings exceeding $70 billion to the U.S. Treasury Department this year on income from assets including mortgage-backed securities, according to the Congressional Budget Office. “The Federal Reserve’s actions to stabilize the financial markets are likely to significantly increase the amount of its remittances over the next few years,” the CBO said in a report released today. It was prepared at the request of Senator Judd Gregg of New Hampshire, the senior Republican on the Senate Budget Committee. The Fed returned $47.4 billion of its income last year, primarily from interest earnings on its assets, according to the Fed’s annual consolidated financial statements. The central bank earns interest income from its holdings of Treasury securities, loans to banks and its holdings of housing debt, the Fed said. The amount returned to the Treasury in 2009 was $15.7 billion higher than in 2008.

The Budgetary Impact and Subsidy Costs of the Federal Reserve’s Actions During the Financial Crisis - CBO Director's Blog - Over the past several years, the nation has experienced its most severe financial crisis since the Great Depression of the 1930s. To stabilize financial markets and institutions, the Federal Reserve System used its traditional policy tools to reduce short-term interest rates and increase the availability of funds to banks, and created a variety of nontraditional credit programs to help restore liquidity and confidence to the financial sector. In doing so, it more than doubled the size of its asset portfolio to over $2 trillion and assumed more risk of losses than it normally takes on. In a study prepared at the request of the Ranking Member of the Senate Budget Committee, CBO describes the various actions by the Federal Reserve and how those actions are likely to affect the federal budget in coming years. The report also presents estimates of the risk-adjusted (or fair-value) subsidies that the Federal Reserve provided to financial institutions through its emergency programs. Unlike the cash treatment of the Federal Reserve in the budget, fair-value subsidies include the cost of the risk that the central bank has assumed. Thus, those subsidies are a more comprehensive measure of the cost of the central bank’s actions

Costs of the Federal Reserve's Actions During the Financial Crisis - CBO (pdf)

Monetary policy: Real policy problems | The Economist - SCOTT SUMNER quotes a Nick Rowe post on the status of orthodox economics: For 70 years we have taught, and believed, that we would never again need to suffer a persistent shortage of demand. We promised ourselves the 1930’s were behind us. We knew how to increase demand, and would do it if we needed to.The orthodox have lost faith in that promise; only the heterodox still believe it.And Mr Sumner says:I have certainly lost faith in the promise that we “would do it if we needed to.” But I still believe it can and should have been done.I basically agree with Mr Sumner in that policymakers had, and continue to have, the ability to reduce the seriousness of the crisis. Central bankers, in particular, seem to have learned only half the lesson of the Depression, and were willing to act boldly enough to halt growth in unemployment, but not enough to try and reverse it.

"NY Fed President: 'The Recovery Is Crumbling,'" From NY Fed President William Dudley's commencement speech at New College of Florida:[T]he recovery is not likely to be as robust as we would like for several reasons.First, households are still in the process of deleveraging. The housing boom created paper wealth that households borrowed against. This pushed the consumption share of nominal gross domestic product to a record high of about 70 percent. When the boom turned into a bust, those paper gains evaporated. Second, the banking system is still under significant stress. This is particularly the case for small- and medium-sized banks that have significant exposure to commercial real estate loans. This stress means that banks have been slow to ease credit standards as the economy has moved from recession to recovery.Third, some of the sources that have supported the nascent recovery are temporary. The big swing from inventory liquidation during the recession back to accumulation will soon end as inventory levels come back into better balance with sales.

More Fed Swap Lines for Europe and the End of Globalization; Comment: Clifford Rossi in Support of the Office of Financial Research- Before we delve into the sublime world of enhanced financial data via the OFR, let us explain our views more generally on reform and the immediate outlook for the US economy. The legislative process in Washington with respect to financial reform is thankfully at an end and the result is even less impressive than the breathless news reports indicate. Most of the supposed reform is actually window dressing, especially those portions of the legislation that afford regulators "discretion" in terms of changes in the behavior of the largest banks and markets. What is the point of greater transparency from "private" banks, companies and markets envisioned by financial reform legislation if the condition of private obligors is being undermined every day by the irresponsible fiscal and monetary policies coming from Washington? What difference does greater financial transparency make when the underlying political economy is built upon false assumptions and outright fallacies about finance and economics that stretch back decades to the WW II and the Bretton Woods agreement?

Senate bill brings new powers, new pressures for Fed - The exact impact of the far-reaching Senate legislation on the Fed is hard to predict, and it will change further as the Senate bill is reconciled with the House version passed last year. But the final bill will clearly reinforce the primacy of the Fed in preventing financial firms from taking risks that endanger the U.S. economy as a whole. Under both bills, Fed leaders would identify firms whose size, complexity or interconnectedness makes them in need of extra oversight and, if a newly established council of financial regulators agreed, the Fed would begin supervising those companies. When a large, complex financial firm is on the verge of failure, the central bank would play a role in shutting it down, outside the bankruptcy process.

Bernanke Says Central Banks Must Be Free of Pressure (Bloomberg) -- Federal Reserve Chairman Ben S. Bernanke said central banks must be free from political pressure as they bolster regulation and try to prevent future financial crises. “In undertaking financial reforms, it is important that we maintain and protect the aspects of central banking that proved to be strengths during the crisis and that will remain essential to the future stability and prosperity of the global economy,” Bernanke said today in a speech at the Bank of Japan in Tokyo. Bernanke and other central bank chiefs have faced mounting political threats to policy independence while combating the worst financial crisis since the Great Depression.

Bernanke Continues to Fight Against Greater Political Scrutiny - WSJ - With Congress getting close to finalizing an overhaul of the nation's financial-regulatory system, Federal Reserve Chairman Ben Bernanke weighed in against provisions in the proposed legislation that would subject the central bank to more political scrutiny. In a speech at the Bank of Japan on Wednesday, the Fed chief argued before an international audience that central banks independent from politics were better at managing the economy. He also detailed the steps the Fed had taken to become more transparent and accountable to the public, two conditions he said were needed in return for greater independence.

Place Political Limits on Overly Compliant Central Banks - In theory I agree that Central Banks should be free from political influence. In practice, I don’t. Why? Central Banks regularly cave into political influence. They are quick to loosen, and slow to tighten. They are happy to let asset bubbles develop, because that is not what they are employed to handle.The truth is, the arguments of Ben Bernanke are a joke (here too). When Central Banks felt no pressure, they happily went along with what the politicians wanted. No one wanted a strict central bank. Thus for all of the Greenspan/Bernanke era, asking to be free from political control is just a show. They want to agree with the politicians, who want easy credit. They don’t want rules that would lead to a better economy in the long run, where their political friends get harmed.Here’s a simple rule, that if put into place, would reduce volatility considerably: if the 3-month T-bill yield is more than 2% lower than the 10-year T-note yield, tighten. If the 3-month T-bill yield is more than 1% higher than the 10-year T-note yield, loosen. When in doubt, set Fed funds rate such that the gap between the 10-year and 3-month T-bill to 0.5%. It’s that simple. We don’t need grotesque yield curve shapes to guide the economy; we do need to limit the amount of excess liquidity in loosening, lest we get asset bubbles.

Central Bankers Still Seeing Tame Inflation Data - Strains in European financial markets have made it more likely that the Federal Reserve will refrain from raising interest rates until as late as next year. Good thing, then, that inflation pressures remain so modest, sparing policy makers the ugly choice between deciding whether to support growth or combat rising prices. The lack of inflation should also help counter fears in some quarters that the Fed’s massive balance sheet is set to be the engine of an unwanted inflation surge.For some time now, economic data has shown nothing but decidedly low inflation. On Friday, the government reported in its release on April personal spending and income that the core personal consumption expenditures price index, which is stripped of food and energy costs, rose by 0.1% in April and by 1.2% from a year ago.This gauge is the central bank’s preferred inflation barometer, and it continues to range under what officials view as price stability.

FT Alphaville – That receding, deflationary, resurfacing … M3 money supply - When the Federal Reserve decided to get rid of its M3 measure of monetary supply in 2006, it sparked a wave of ‘what are they trying to hide?’ conspiracy theories — most of those centred around inflation.So it’s perhaps with some surprise, that this Bloomberg story has surfaced on Monday:A measure of the U.S. money supply, created but abandoned by the Federal Reserve, has turned negative in the past year and signals disinflation or outright deflation, according to economists who track the figure.The CHART OF THE DAY shows M3 has shrunk 5.4 percent in the past year, an indication the economy may face deflationary pressure as fewer dollars chase the same amount of goods, according to economists Paul Ashworth and Paul Dales at Capital Economics Ltd. in Toronto. They began compiling a measure of M3 after the Fed discontinued it in 2006. And here’s the chart:

Have You Seen M3 Lately? -- Deflation-minded individuals are no doubt cheering the recent M3 data featured today in a Bloomberg “Chart of the Day” along with other measures of the money supply. As for M3, it’s not all good. The broadest measure of the money supply (abandoned by the Federal Reserve back in 2006 but reconstructed elsewhere, for example by Capital Economics above) is now down 5.4 percent from a year ago and the fear of fewer dollars chasing the same amount of goods has more than a few economists thinking that we’ll be seeing lots of minus signs in front of the inflation numbers for some time to come.

US money supply plunges at 1930s pace as Obama eyes fresh stimulus - The M3 money supply in the United States is contracting at an accelerating rate that now matches the average decline seen from 1929 to 1933, despite near zero interest rates and the biggest fiscal blitz in history. The M3 figures - which include broad range of bank accounts and are tracked by British and European monetarists for warning signals about the direction of the US economy a year or so in advance - began shrinking last summer. The pace has since quickened. The stock of money fell from $14.2 trillion to $13.9 trillion in the three months to April, amounting to an annual rate of contraction of 9.6pc. The assets of insitutional money market funds fell at a 37pc rate, the sharpest drop ever. "It’s frightening," said Professor Tim Congdon from International Monetary Research. "The plunge in M3 has no precedent since the Great Depression"

M3 Hysteria and a Look M2, MZM, GDP and PPI I would very much like to have M3 back, but in particular I would like the Fed to be releasing a more accurate and contemporary measure of Eurodollars, the dollar overhang overseas, particularly in light of the huge swings in the DX index, and its almost undeniable relationship to the recent dollar short squeezes on the European banks. The Dollar Rally and the Deflationary Imbalances in the US Dollar Holdings of Overseas Banks...

But alas, we do not have this, so we can only estimate M3, particularly the eurodollar component. But the good news is that we still have both M2 and MZM. Here are the most recent figures for MZM and M2 from the St. Louis Fed, expressed as a percent of change YoY, not adjusted for seasonality. For good measure I have added GDP and PPI Finished Consumer Goods in the mix.MZM is the broadest measure of liquidity, and is very much a creature of the Adjusted Monetary Base. As one can see from the chart, the Fed, using their various policy tools, jams the short term money supply higher in response to a lagging economy, and the broader measures like M2 tend to follow with a lag.

Will the Fed Bring Back M3? - Is the M3 money supply making a comeback? It seems to be gaining attention as Bloomberg, the FT Alphaville, and now Ambrose Evans-Pritchard are discussing the deflationary implications of the dramatic slide in the M3 money supply over the past year. I am not as concerned about deflation as they are, but am sympathetic to their view that M3 is currently a better measure of the U.S. money supply than M1 or M2.* I believe this argument was first made by Gary Gorton in his research on the financial crisis. He makes the case for M3 by noting that an accurate measure of the money supply today should include repurchase agreements (which are not in M1 and M2) because (1) they too are bank liabilities used as money and (2) they have grown increasingly important:

Will The USD Be Replaced By The SDR Or The CNY As The Next Reserve Currency? - Jim O'Neill, who did not make any friends within the bear community earlier today, has written an interesting paper on the IMF's Special Drawing Rights, and whether this hypernational currency can ever become a reserve currency as is, and/or with the CNY as a constituent member. While O'Neill as usual focuses on the angle of the "next paradigm" BRICs, and how they will increasingly dominate global economics, he does pose an important question: with the dollar likely to suffer the side effects of either hyperdeflation, hyperinflation, or hyperstagflation, will the next reserve currency be a diluted melange of other flawed fiat constructs (i.e., the SDR), or the currency of the one country, which for all its flaws, still has the cleanest balance sheet backing its own fiat construct.

Barry Eichengreen Sees a Breakup of the Dollar Zone - Over at The Economist there is an interesting discussion surrounding the future of the Eurozone. Today Barry Eichengreen weighed in and made the case that the dollar zone in the United States will break up in the next 10 years due to state fiscal problems. Coming from Eichengreen, this piece has to be satire. There is no way he really believes the dollar zone will breakup in the next decade. Even I don't believe it and I have published research questioning whether the United States is truly an optimal currency area. I suspect Eichengreen is cleverly making the point that even though there may be problems with the dollar zone, that if taken to their logical conclusion would imply a break up of currency union, it is absurd to think it will actually happen. If so, then ditto for the break up of the Eurozone. Or maybe I am reading too much into this piece. Maybe the Eurozone crisis has Eichengreen in a funk and he has taken to heart the conversation among Paul Krugman, Ryan Avent, and myself that questioned the dollar zone as an optimal currency area. You decide for yourself:

Conventional Madness - Krugman - I’ve had a chance to read the new OECD Economic Outlook. It’s a terrifying document.Why? Not because it offers a grim prospect, although it does — although the OECD has marked up its growth projections, it’s still forecasting extremely high unemployment for years to come. No, what’s scary is the utter folly that now passes for respectable opinion. Here’s the OECD on US monetary policy:In the United States, where some long-term measures of inflation expectations have increased and the labour market has stabilised earlier than expected, the start of normalisation [by which they mean raising interest rates] should not be delayed beyond the last quarter of 2010. Policy interest rates should be well above half-way to neutral by end-2011, but the path of convergence to full normalisation would have to accelerate if long-term inflation expectations were to drift up further.So the OECD wants the Fed to start raising interest rates soon — in the next six months or less — because … well, we can look at the OECD’s own forecast. According to this forecast, in the fourth quarter of 2011 — a year and a half from now — the unemployment rate will still be 8.4 percent. Meanwhile, inflation will be 1 percent — well below the Fed’s implicit target of 2 percent.

More Aggregate Demand Weakness? -The wailing and gnashing of teeth over deflation has begun anew. With the CPI showing a decline in April, folks like Paul Krugman and Greg Ip are concerned about a Japanese-style deflation emerging in the United States. Other observers like Tim Duy and Scott Sumner are similarly concerned as they fear U.S. aggregate demand is going to get increasingly weak. I do not mean to be a contrarian here, but I am having a hard time seeing how these concerns are justified. Yes, the U.S. economy has been plagued by a weak recovery, but the image one gets from this discussion is that we are standing on the precipice of another collapse in spending. If so, the data sure don't show it. Take, for example, monthly retail sales. It grew at a year-on-year rate of almost 10% in April as can be seen in the figure below. The figure also shows domestic demand through 2010:Q1. Given the strong correlation between these two series, it seems likely that the strong growth in current retail sales will also be seen in domestic demand once the numbers are released.(Click on figure to enlarge.)

A different take on deflationary pressures - DAVID BECKWORTH surveys the crowd of economic writers wringing their hands over lagging inflation and says that they're wrong to see a new crisis looming. Retail sales data in America don't indicate that falling prices are due to falling growth expectations.[B]oth current and expected spending are growing. It may be not be growing as fast as we want, but it is growing and there is no sign of an imminent collapse. Now if aggregate demand is growing and is expected to grow how is it possible to have inflation falling? The simple answer is that aggregate supply must be growing as well. As I noted in my previous post, this spike in the productivity growth rate may be why the unemployment rate has been remained so high. The problem with this is that it's inconsistent with falling markets, which are perfectly consistent with declining growth expectations

Whose your Daddy!!! - This article may seem dire, but one can wonder if it is quite so bad. There is an astonishing number of Experts out there, who see deflation as the fall of Western Civilization. I have often postulated that deflation could possess neutral, if not beneficial, potential scenarios. Deflation tends to reintroduce older cottage industries, reestablish older types of employment, and raise the quality of Product to justify retention of Product prices. The decline in Housing prices were long awaited, and in my mind, should have stabilized somewhere in 2002; later Home pricing being in itself over inflationary. The only problem here was the tie between Credit and Housing Retail. An intelligent Government would have long established a minimum and maximum Interest rate for Mortgages. It is and was a sensible plan to separate Mortgages from the Credit industry, while presenting little initial impact to Credit overall; banks and financial institutions devoting their attention to the viability of the mortgage payment system.

Strippers Declare Inflation Dead as Dealers Revive Zero-Coupon Treasuries - The 18-month slump in Treasury zero- coupon bonds is giving way to rising demand as the rate of inflation falls to a 40-year low, turning so-called Strips into the best performers in the U.S. government debt market. Investment banks increased the securities -- created by separating the interest and principal payments of a bond and selling them at a discount -- by 4.4 percent to $179.4 billion from December through April, according to Treasury Department data. It’s the first time that the market expanded for five straight months since 2006. “We are in some sort of a new normal environment and inflation is not going to be a problem anytime soon,”

Inflation, Deflation, Japan - Krugman - First, here’s a prime example of the fire-in-Noah’s-flood syndrome: Irwin Kellner manages to get all scared about inflation in the face of a deflationary environment. To do this, he has to come up with a novel theory: that the prices that matter are those of things we buy frequently, as opposed to big-ticket items bought less frequently. And the reason for this is …??? (Remember, there’s a very clear reason for excluding food and energy prices; I have no idea why big-ticket items should receive the same treatment.) Yet both logic and experience show that when you’re in a liquidity trap, big rises in the monetary base aren’t inflationary — in fact, they can be virtually irrelevant.Which brings me to a very insightful talk (pdf) by Adam Posen, my favorite Japan expert (and now on the policy board of the BOE). There’s a lot in this talk, but let me just focus on one issue: the effects of Japan’s “quantitative easing” policy, which involved pushing up the monetary base in the hope of getting some traction. (Unlike what we now call quantitative easing, this didn’t involve large purchases of nontraditional assets.)First, here’s the record of increases in narrow money, aka the monetary base

Fed and Bank of Japan reject higher inflation target - FT - The top central bankers at the Federal Reserve and the Bank of Japan said on Wednesday that they oppose higher inflation targets, a measure that would give more scope to cut interest rates in a crisis. Inflation targets of 4 per cent have been floated by Olivier Blanchard, chief economist of the International Monetary Fund, as a way to reduce the danger of deflation caused by central bankers’ inability to cut rates below zero.A higher inflation target would on average lead to higher interest rates. That would mean greater scope to respond to a crisis by cutting rates but must be weighed against the cost of higher inflation in normal times.The opposition of Federal Reserve chairman Ben Bernanke and Bank of Japan governor Masaaki Shirakawa suggests that central banks are unlikely to change their inflation targets despite hitting the zero per cent floor on rates in response to the financial crisis

Hyperinflation Guaranteed - Yes this is it! We have crossed the Rubicon and events in the world economy are now likely to unfold in a totally uncontrollable fashion. Clueless governments still don’t understand that it is their ruinous actions that have created a credit infested and bankrupt world. They will continue to prescribe the same remedy that caused the problem in the first place, namely more credit and more printed money. The consequences are clear; we will have hyperinflation, economic and human misery as well as social unrest.When will the world finally begin to understand that we have reached the point of no return and that “the voyage of their life is bound in shallows and in miseries” (Shakespeare, Julius Caesar)? Sadly, we are probably not very far from that point. It is already starting to happen in many countries.

Enough hot air about inflation—there are other things to worry about right now - Can we please stop worrying about inflation—at least for a few months? Since the onset of the financial crisis in 2008, there has been serious concern that the massive expansion of the Fed's balance sheet, the central bank's policy of zero interest rates, and the large stimulus (and ensuing deficits) would, by some iron law of economics, debase the currency, boost the government's long-term borrowing costs, and ignite inflation. By almost every measure, observed inflation and inflation expectations have remained remarkably contained since the fall of 2008. . And the evidence weighing in favor of deflation—or at least a serious lack of inflation—continues to mount. Last week, the Bureau of Labor Statistics reported that inflation, as measured by the Consumer Price Index, fell 0.1 percent in April. Over the last year, it has risen a tame 2.2 percent. Factor out volatile food and energy prices and the long-term trend was more heartening. In the last 12 months, the core index has risen just 0.9 percent, "the smallest 12-month increase since January 1966." (Check out this inflation chart Krugman posted on his blog on May 19.)

US, Greece, Spain Are in Debt Risk 'Ring of Fire,' Pimco Says (Bloomberg) -- The U.S., Spain and Greece are among developed nations whose borrowings put them in a “ring of fire” amid sovereign debt concerns, said Pacific Investment Management Co., which runs the world’s biggest bond fund.The company is investing in emerging markets that will benefit from high savings rates, the absence of debt bubbles and a greater capacity for government spending, said John Wilson, head of the Australian unit of Newport Beach, California-based Pimco, in an e-mailed statement today. The fund manager is targeting bonds including those in Brazil, Mexico and Russia and retaining holdings of inflation-linked Australian debt, he said. “While the support declared by European leaders and the International Monetary Fund quelled concerns of sovereign risk spreading, Greece’s ability to refinance near-term debt remains a risk,” said Wilson. “Other developed countries in this ‘ring of fire’ are Ireland, Spain, France, U.S., U.K., Italy, Portugal and Japan.”

Loomis' Fuss Cuts All Treasury Holdings, Echoes Gross' Warning (Bloomberg) -- Dan Fuss, whose Loomis Sayles Bond Fund beat 95 percent of competitors the past year, said he sold all of his Treasury holdings because of prospects interest rates will rise as the U.S. borrows unprecedented amounts.“The fundamentals are awful,” Fuss said in a telephone interview yesterday from Boston. “The incremental borrower of funds in the U.S. capital markets is rapidly becoming the U.S. Treasury. Do you really want to buy the debt of the biggest issuer?” Fuss said he doesn’t own Treasuries in any of the investments he is directly involved with after selling the last of them this week.

Debt experts toll recovery warning bell – Debt experts warned a bipartisan White House panel Wednesday that federal borrowing could slow or stall recovery from the recession. Several members of the Fiscal Responsibility Commission then said they should find ways to cut the debt rather than stabilize it.University of Maryland economic historian Carmen Reinhart said that, over the last two centuries, countries have seen debt drag down growth once it reaches 90 percent of national income. Federal debt owed to public creditors and government trust funds is close to that mark at nearly $13 trillion, while GDP is about $14.6 trillion.

The National Debt and National Security - The Washington Post has an important column today by David Ignatius on the concerns that senior members of the military have about our national debt and those of our allies. It's easy to see why this is the case from the following table. It shows two things. First, our defense spending as a share of the economy is far above our allies. As pressure to deal with our debt situation mounts, it is inevitable that there is going to be massive political pressure to cut the defense budget. Second, given the low level of defense spending by our allies, many of which are struggling to deal with debt problems worse than ours, there is no possibility that they will be able to pick up the slack if we are forced to pull back our defense commitments.

PIMCO - Bill Gross - Three Will Get You Two (or) Two Will Get You Three - Debt will get you in trouble – on both sides of the dollar bill as Shakespeare wisely counseled long ago: Neither a lender nor a borrower be. How much debt is too much? How little growth is too little? No one knows for sure. Economic historians such as Kenneth Rogoff point out that at debt levels of 80-90% of GDP, a country’s real growth becomes stunted, and the sixteen tons become more and more difficult to bear. Greece is well past that standard, which is one of the reasons why lenders are balking at extending a private-market helping hand. When not only government but corporate and household debt is included, the waters become murkier, because historical statistics are less available, and corporations are more multinational than ever before. Common sense observation tells you, though, that the debt super cycle trend in the U.S. shown in the following chart is reaching unsustainable proportions and that the “growth” required to service it if real interest rates were ever to go up instead of down would be insufficient. That is why lenders balked 18 months ago during events surrounding the Lehman liquidity crisis and why they’re beginning to balk once again. Too much debt/too little growth makes for a “three will get you two” moment, and they refuse to extend credit under those circumstances.

The real cost of US debt - The current national debt estimate of $14 trillion is misleading. The government’s deceptive accounting practices fail to include its ownership in the automotive and financial sectors as part of the national debt, which would increase it by trillions of dollars.It’s time for this administration to bring transparency to the federal budget process by properly accounting for companies now held by the federal government through the Troubled Asset Relief Program (TARP).When Office of Management and Budget Director Peter Orszag ran the Congressional Budget Office, he unsuccessfully nudged the Bush administration to include the debt of federally backed mortgage enterprises Fannie Mae and Freddie Mac in the national budget. His position was that two principles of government accounting require such debts to be on the government’s books: principle one, we control these companies; principle two, we guarantee their debt.

Government Takeover Facts - Statistics on Public Ownership 2010… graphic

U.S. Dollar Drop Is Bigger Risk Than Default, HSBC's King Says (Bloomberg) -- U.S. dollar investors face a greater risk of the government allowing the currency to devalue rather than the nation failing to make good on its debts, HSBC Holdings Plc Chief Economist Stephen King said. "If there's a dollar decline and you put your money back in say, renminbi, then you lose out because you lent to the U.S. in dollars rather than in your own currency, so you are at risk," King told reporters at an event in Dubai yesterday. "The big risk is not that they'll default, the big risk is that the U.S. engineers at some point a dollar decline that works in its own favor."

But, You Sputtered, I'm Just A Hack....That is, with all my pesky math and charts like this: Remember that I've been preaching for a while that we embedded a roughly $500-600 billion structural deficit into the economy post-2000? And that now, in response to this recession (and in a refusal to admit that we have been playing credit drunk) we've now embedded a roughly 10% structural deficit - three times the former? Before you consider me a chucklehead for having the temerity to look at the math you might take it up with the BIS - the Bank of International Settlements, or the "bankers' bank" - which agrees with me: According to the Bank for International Settlements, the United States’ structural deficit — the amount of our deficit adjusted for the economic cycle — has increased from 3.1 percent of gross domestic product in 2007 to 9.2 percent in 2010. Gee, you mean they looked at the same chart I've been preaching from? This stuff isn't hard folks!

Deficit hawks ignore the R-word - Of all the gaps between elite and mass opinion in America today, perhaps the greatest is this: The elites don't really believe we're still in recession. Or maybe, they just don't care. How else to explain the continual harping on the deficit by editorialists, centrist think tanks and the like when the nation is still enmeshed in the most serious economic downturn since the 1930s? How else to understand the growing opposition to the jobs bills Congress is set to vote on this week, particularly when nobody has identified any future engine of American economic growth save countercyclical public investment? It's not that the American people aren't concerned about the deficit. But in poll after poll, they make clear that their No. 1 concern is jobs. Forty-seven percent of respondents to a Fox News poll this month, for instance, said they were concerned with the economy and jobs, while just 15 percent acknowledged concern over the deficit and spending. "There is no significant difference across party lines," Pew reported.

Deficit Hawk Hypocrisy - Harold Meyerson is spot on: “Of all the gaps between elite and mass opinion in America today, perhaps the greatest is this: The elites don’t really believe we’re still in recession. Or maybe, they just don’t care.” What is even more galling is that, having been the greatest beneficiaries of the government’s largesse over the past 2 years, these very same people now decry the government’s “irresponsible” and “unsustainable” fiscal policy. The collective amnesia and moral turpitude of these elites is truly mind-boggling.Why do we have a deficit of about 10% of GDP right now when it was less than 2% about 3 years ago? The reasons are: the Obama stimulus, the TARP, and the slower economy (which arose in response to a major financial crisis, not because the government began an irrational and irresponsible spending binge). A slower economy leads to lower revenues (less income=less taxes paid since most tax revenue is based on income, and lower tax brackets) and higher spending on the social safety net.

Moody’s Reiterates U.S. Spending Risks Credit Rating - The U.S. government’s Aaa bond rating will come under pressure in the future unless additional measures are taken to reduce projected record budget deficits, according to Moody’s Investors Service Inc....The government’s finances have been “substantially worsened by the credit crisis, recession, and government spending to address these shocks,” Moody’s analysts lead by Steven A. Hess wrote. “The ratios of general government debt to GDP and to revenue are deteriorating sharply, and after the crisis they are likely to be higher than the ratios of other Aaa-rated countries.” Debt to revenue has more than doubled over the past three years and is now over 400 percent, which could lead to “potential stress” on finances, the report said.

Is There Such a Thing As an Unsustainable Level of Debt? - My short answer is: “no.” Debt is a stock concept, not a flow one. To determine whether something is “sustainable” or not (whether it be the government’s fiscal condition, a family’s personal finances, environmental quality, one’s physical health, or even personal relationships) requires a look at the dynamics of the situation, not just a snapshot.I mention this because there’s been a lot of buzz among fiscal policy economists over the past couple days, ever since the President’s fiscal commission discussed the idea of setting a specific level of gross federal debt to GDP as a policy goal. Experts from all sides attacked this notion immediately, focusing on the “gross” part. They emphasize that economically, it’s really net debt, or debt held by the public (investors whether American or foreign), that matters. Jim Horney of the (left-leaning) Center on Budget and Policy Priorities explains this very well, and Andrew Biggs of the (right-leaning) American Enterprise Institute agrees. My objection is on the emphasis of a particular level of debt–whether gross or net, actually–as some sort of magical number that would trigger a particular set of bad economic outcomes if we were to reach it.

The safe asset shortage - Ricardo Caballero has an interesting idea: the fundamental problem in the current global macroeconomic and financial equilibrium is one of asset shortages. In particular, there is a shortage of safe “AAA” assets. The world seems to need more US Treasury-like instruments than are available.This shortage of safe assets existed before the crisis, but it is even worse today. The demand for these assets has expanded as a result of the fear triggered by the crisis – as it did for emerging markets after the 1997-1998 crisis. But this time the private sector industry created to supply these safe assets – the securitisation and complex-assets production industry – is severely damaged.Broadly I think that he is right. The demand for safe assets was one of the key enablers of the credit crunch

Extending unemployment insurance is the fiscally responsible thing to do - Unemployment insurance (UI) not only provides a vital safety net to workers who lose their jobs, it also serves as a valuable stimulus, which puts money back into the economy and helps create jobs during recessions. Yet at a time of the worst job crisis in a generation, with unemployment at 9.9%, more than five unemployed workers for every job opening, and record levels of long-term unemployment, millions of workers are at risk of losing their UI benefits.On May 26, EPI hosted Long-Term Unemployment: Causes, Consequences, and Solutions, a panel featuring several leading labor market economists discussing the unprecedented rates of long-term unemployment and showing why extending UI benefits to those workers would help them maintain some consumption during a time of economic distress and help create more jobs. The economists provided an array of evidence disputing the contention that extending unemployment insurance raises the unemployment rate in any meaningful way

Debt worries prompt House to trim jobless-benefits bill - Under fire from rank-and-file Democrats worried about the soaring national debt, congressional leaders reached a tentative agreement yesterday to scale back a package that would have devoted nearly $200 billion to jobless benefits and other economic provisions while postponing a scheduled pay cut for doctors who see Medicare patients.After struggling throughout the day to reach a compromise, House leaders scheduled a vote today on the slimmed-down package in hopes of pushing it through both chambers before the 10-day Memorial Day recess, which is scheduled to begin Friday.Unless lawmakers act before Wednesday, millions of people could cease to be eligible for up to 99 weeks of jobless benefits and doctors' Medicare payments could fall by 20 percent.

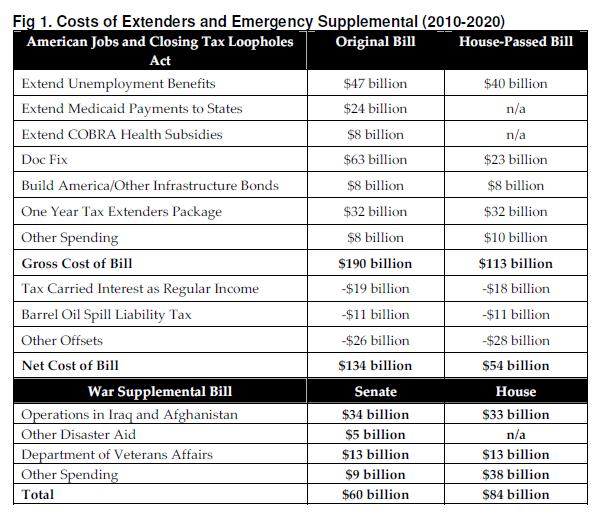

Senate Approves Nearly $60 Billion for Wars - The Senate on Thursday approved a nearly $60 billion measure to pay for contin uing military operations in Afghanistan and Iraq as House Democrats struggled to round up votes for a major package of business tax breaks and safety-net programs for the long-term unemployed.Senators delivered a bipartisan 67-to-28 vote for the war financing bill after rejecting a series of Republican proposals on border protection as well as a plan by Senator Russ Feingold, Democrat of Wisconsin, to require President Obama to produce a timetable for withdrawing from Afghanistan. With lawmakers eager to begin a Memorial Day recess, House Democratic leaders ran into stiff resistance from rank-and-file members uneasy about supporting the approximately $143 billion tax and unemployment measure. More than $80 billion of it would be deficit spending — a hot-button issue in the midterm Congressional campaigns and an increasingly frequent line of Republican attack.

A Question That Needs Answering: Who Will Be Hurt by Deficit Reduction? - The progressive message on the deficit has to be very clear: first, don't do anything that will endanger our economic recovery, because the best way to solve the deficit is to improve our economic health (see: the 1990s). Secondly, when you ask for sacrifices, they shouldn't be all or mostly from the middle class and poor. This is a pretty key point, since many of the deficit hawks seem to be zeroing in on cuts in Social Security and a Value Added Tax, both of which overwhelmingly impact the poor and middle class far more than they do the wealthy.What these proposals are is an attempt to make middle and lower income people pay for the sins of the wealthy who have benefited from the deficit. Middle class incomes have been stagnant over the last decade, while the costs of their groceries, gas, utilities, and college education for their kids has skyrocketed. Middle class housing prices have plummeted the last three years, with foreclosures and bankruptcies increasing exponentially. Middle class folks haven't gotten the big tax cuts the wealthy have over the last 10 years, and when taxes are raised at the local level, its almost always regressive taxes like the sales tax that impact poor and middle class people the most. Meanwhile, public school teachers, social services for the poor, parks, libraries, community colleges, programs to help handicapped kids - all of those programs that matter to working families are the things that get cut.

In Defense of Deficits - The Simpson-Bowles Commission, just established by the president, will no doubt deliver an attack on Social Security and Medicare dressed up in the sanctimonious rhetoric of deficit reduction. (Back in his salad days, former Senator Alan Simpson was a regular schemer to cut Social Security.) The Obama spending freeze is another symbolic sacrifice to the deficit gods. Most observers believe neither will amount to much, and one can hope that they are right. But what would be the economic consequences if they did? The answer is that a big deficit-reduction program would destroy the economy, or what remains of it, two years into the Great Crisis.

Op-Ed - Easy Money, Hard Truths - NYTimes - Before this recession it appeared that absent action, the government’s long-term commitments would become a problem in a few decades. I believe the government response to the recession has created budgetary stress sufficient to bring about the crisis much sooner. Our generation — not our grandchildren’s — will have to deal with the consequences. According to the Bank for International Settlements, the United States’ structural deficit — the amount of our deficit adjusted for the economic cycle — has increased from 3.1 percent of gross domestic product in 2007 to 9.2 percent in 2010. This does not take into account the very large liabilities the government has taken on by socializing losses in the housing market. We have not seen the bills for bailing out Fannie Mae and Freddie Mac and even more so the Federal Housing Administration, which is issuing government-guaranteed loans to non-creditworthy borrowers on terms easier than anything offered during the housing bubble. Government accounting is done on a cash basis, so promises to pay in the future — whether Social Security benefits or loan guarantees — do not count in the budget until the money goes out the door.

On writing fiction - The New York Times carried an Op-Ed article – Easy Money, Hard Truths – on May 26, 2010 written by a hedge fund president, one David Einhorn.It was not just the poor economics that was on display but also a mis-use of statistics to try to reinforce the poor economics that was notable.Einhorn asks his fellow US citizens – “(a)re you worried that we are passing our debt on to future generations?” Answer: “Well, you need not worry.” Why? Because the:… the government response to the recession has created budgetary stress sufficient to bring about the crisis much sooner. Our generation – not our grandchildren’s – will have to deal with the consequences. He claims “the United States’ structural deficit – the amount of our deficit adjusted for the economic cycle – has increased from 3.1 percent of gross domestic product in 2007 to 9.2 percent in 2010″. I have written cautionary blogs about structural deficit measurement before – for example, Structural deficits – the great con job!

Be Optimistic About Euro Fiscal Situation; Not US - Courtesy of the Wall Street Journal, here we have a laundry list of PIIGS' efforts to adjust to an age of diminished expectations - Reuters also has a similar list, albeit a bit more detailed. Meanwhile, the "safe haven" of America? You must be joking. Having crashed through the $13 trillion debt mark according to the US National Debt Clock with offhand ease, Uncle Sam is gorging like your typical blubbery American at an all you can eat buffet. (Speaking of which, this analogy is a great one.) From the Associated Press:

Is the World Broke? Entitlements, Spending May Spell Doom - Fox -What started as a cautious eye toward problems in a marginally important economy in Greece became a full-blown crisis, when ratings firms cut debt outlooks for fellow eurozone economies Spain and Portugal. There were concerns that the euro itself would collapse, or at least break into pieces, either because Greece was thrown out or more stable economies like Germany pulled out. But it isn’t just a European problem. Spending in the U.S. threatens to leverage the domestic economy so much that it faces, within just a few years, a debt level that represents the country’s entire gross domestic product. And, since the U.S. is a relatively strong world economy, even with unemployment near 10% and uneven signs of recovery, American taxpayers have been forced to dig deep to help out the rest of the world. Indeed, the bailout of Greece couldn’t happen without two American contributions: the U.S.’s funding of nearly 20% of the International Monetary Fund, which is helping to keep Greece afloat, and the move by the Federal Reserve to swap dollars for euros, thus helping prop up European banks. So how did we get here?

Blue Dogs Bit Off Some Deficit Today - For over a year House Blue Dog Democrats took a back seat to President Obama's top priorities, a $787 billion stimulus bill and a health reform bill that CBO scored as paid for, but about which many have their doubts. This week the Blue Dogs bit off almost $80 billion from the extenders bill, H.R.4213, most of which passed the House this afternoon on two separate votes. The good news is that those fighting larger deficits in the House are gaining power. The bad news is that the Senate will undoubtedly add back some of that spending when it takes up the bill during the week of June 7. Taking away $8 billion of COBRA health benefits for the unemployed, $24 billion of Medicaid aid for the states, and $40 billion from the Medicare physician reimbursement hits the vulnerable, which I'm not comfortable with, but I've learned the hard way that there are no easy deficit cuts.

Reasons To Despair - Krugman - For some reason today’s papers made me feel especially grim about the prospects for economic recovery — not the economic news so much as what one sees about the mindset of policy makers.Well, we could have more fiscal stimulus — but Congress is balking even at the idea of extending aid for the ever-growing ranks of the long-term unemployed. Fiscal responsibility, you see — hey, and let’s make sure estate taxes stay low! We could get tough with China, which continues its currency manipulation and, in the face of a world of grossly inadequate demand, is actually tightening monetary policy to avoid an overheating economy . So given China’s outrageous behavior, Geithner went to China, got nothing .. and pronounced himself very pleased.We could do more through monetary policy. Macro theory suggests that the theoretically right answer, if you can do it, is to get central banks to commit to a higher inflation target. But the Fed and the Bank of Japan say no, because … well, that’s not what central bankers do.

Great Depression 2.0. Bet on it! - Deficits create demand. Demand generates spending. Spending generates economic activity. Economic activity generates growth. Growth generates jobs, increases government revenues, reduces deficits and ends recessions. Simple, right? When consumers have too much debt, they will not spend no matter how low interest rates are. This is not theory, this is fact. If the government cuts spending at the same time as consumers, then overall spending declines and the economy slips into recession. This is what the deficit hawks want–a return to recession. This is politics, not economics. Increasing the deficits, lowers the deficitsThe deficit hawks say “You can’t solve a debt problem by adding more debt”. This is a very persuasive argument, but it’s wrong. Increasing the deficits, lowers the deficits. This sounds wrong, but its right. Here’s proof from a recent article by economist Marshall Auerback:

More On National Security Spending Reductions And The Deficit - As a follow-up to Bruce's post below on the likelihood that the Pentagon budget will be under intense pressure in any deficit reduction plan, take a look at this interview I did last week with Gordon Adams and Cindy Williams, the co-authors of the new book, Buying National Security: How America Plans and Pays for Its Global Role and Safety at Home. In addition to being a good friend, Gordon is the former head of national security for the Office of Management and Budget, the founder of the Center for Strategic and Budgetary Assessements, and one of the most respected military and foreign affairs experts in Washington. In the interview, Gordon and Cindy both agree that neither the Pentagon, State Department, and Department of Homeland Security will be able to avoid being part of a deficit reduction package

I Wish It Were Only Butter - Maxine Udall (girl economist) - The metaphor of guns and butter is used in macro 101 to convey the tradeoffs a nation and it's economy must make. More spent on national defense means less available to spend on consumer goods at home. Oh, would that it were just consumer goods! Unfortunately, the choices seem to be guns and education and jobs.The problem here is that education, much like health, can be thought of as an investment good. It's something that enables higher rates of production both in this generation and for our children and grandchildren. We do not need people who hawk deficit reduction strategies with the style and substance of a carny barker. We need deficit falconers. Sensible, informed people. Not just policy makers and politicians, but the electorate, too. We are going to have to spend some money to get out of this hole. How we spend it will matter immensely both for us in the near term and for our children and grandchildren. We should be giving up some butter if we must. We should not give up education or health investment (or infrastructure or the environment (hello, BP). They may be the only legacies of any value that we pass on to our children and grandchildren.

The Effects of Automatic Stabilizers on the Federal Budget - CBO 11 pp pdf

The $123 Billion Tab For Job And Tax Bill – 24/7 Wall St.- The bill known as H.R. 4213, The American Jobs and Closing Tax Loopholes Act, may clear Congress in the next few days. It would extend eligibility for unemployment insurance benefits, COBRA health care tax credits and other critical programs that families and communities depend on through December 31, 2010. In other words, it would help millions of the unemployed. Another major part of the legislation would close tax loopholes for wealthy investment fund managers and foreign operations of multinational companies.The goals of the programs may be noble, but they will cost taxpayers $123 billion over the next two years. None of this money is in the budget. It is hard to gauge how many times voters will countenance Congress increasing unemployment payments. The new bill provides for 52-week weeks of extended benefits. The Emergency Unemployment Compensation (EUC) program will be extended through the end of the year.

What About the Jobs Deficit? - CBPP -Members of Congress who are opposing the pending jobs legislation on the grounds that it isn’t fully paid for are focusing on the wrong deficit. Yes, we have a long-term budget deficit that we need to take very seriously. But the deficit to worry about right now is the jobs deficit.If Congress leaves town without extending the temporary unemployment insurance benefits set to expire next week, the unemployment insurance map will change from this:..to this: (For an explanation of the different types of unemployment insurance expansions cited in the maps, see here.) Letting these benefits expire wouldn’t just impose unnecessary hardship and uncertainty on the unemployed. It would also slow the recovery by depriving the economy of a needed boost that would encourage stronger job creation. As my colleague Paul Van de Water and I have argued, this is too high a price to pay to avoid the very small long-term deficit impact from passing the full jobs bill.

Why Deficit Hawks Are Killing the Recovery, by Robert Reich: Consumer spending is 70 percent of the American economy, so if consumers can’t or won’t spend we’re back in the soup. Yet the government just reported that consumer spending stalled in April – the first month consumers didn’t up their spending since last September. Instead, consumers boosted their savings, probably because they’re worried about the slow pace of job growth..., as well as a lackluster “recovery.” They’re also still carrying enormous debt burdens. One in four home owners is still underwater. And median wages are going nowhere. So what’s Congress doing to stoke the economy as consumers pull back? In a word, nothing. Democratic House leaders yesterday shrank their jobs bill to a droplet. They jettisoned proposed subsidies to help the unemployed buy health insurance, as well as higher matching funds for state-run health programs such as Medicaid. And they trimmed extended unemployment insurance. Deficit-cutting fever has also struck the Senate – except when it comes to the military, of course. Last night the Senate okayed a $60 billion war-funding bill for Afghanistan.

We’re Not Greece, But That’s No Consolation - Both Bruce Bartlett and the Brookings Institution (Economic Studies directors Karen Dynan and Ted Gayer) warn this week that although the U.S. is no “Greece,” we still should be worried about our fiscal situation.From Bruce’s Forbes column: Many doomsayers believe that our fiscal profligacy will end in a bang, as happened recently to Greece and previously to many other countries. However, it’s very unlikely that the U.S. would ever suffer the sort of abrupt inability to sell its bonds that triggered a fiscal crisis in other countries. And Karen and Ted (of Brookings) express a similar mix of reassurance and warning:So no, we’re not that much like Greece, but at the same time we’re a lot more like the Greece now than the U.S. we used to be.

Are We Japan 2.0? - A balance sheet recession is different from a normal recession. It's caused not by inventory cycles or monetary manipulation by the Fed, but by a debt fueled boom that eventually bursts and leaves the economy in the doldrums until debt levels get back to normal. That's the kind of recession we went through last year, and it's the kind of recession that wracked Japan in 90s. Mike Konczal points us today to a paper written a few months ago by Richard Koo of Nomura Research that compares what we're going through today to Japan's earlier experience: As Koo argues, the economy will not enter self-sustaining growth until the private sector balance sheets are repaired. Even with zero interest rates, there are no borrowers of newly generated savings and debt repayments. With no borrowers, the economy will continue to lose aggregate demand. And how long will it take for balance sheets to get back to normal? Here's Koo on Japan's experience:

Lies, Damned Lies, and Growth - Krugman - Scott Sumner says that I’m wrong about taxes, regulation, and growth, because although American growth has slowed since deregulation and all that, the growth has been better than we might have expected. We can try to parse whether that’s true — but in any case it’s not a response to my original point. That was about the claim, quite common on the right, that the US economy was stagnant until Reagan did away with those nasty New Deal policies — a claim that is simply, flatly, false. The era of strong unions, high minimum wages, high top marginal tax rates, etc. was also a period of rapid growth and rising living standards. That doesn’t prove causation; it does disprove the widespread dogma that these things are always economically devastating. And it’s telling that so many on the right have airbrushed the whole postwar generation out of history. Given all that, what do we learn from the fact that since 1980 the United States has more or less maintained its relative GDP per capita, after substantial decline previously?

Government Spending and Economic Expansions - It is conventional wisdom that raising taxes, particularly during and just after a recession, will harm the economy. Last week I checked whether that was true. (The post appeared in the Presimetrics blog and the Angry Bear blog.) The post looked at every recession since 1929, and it showed that recessions that were accompanied by marginal tax rate cuts were followed by shorter, slower expansions than recessions that weren't accompanied by marginal tax rate cuts. (Expansion, btw, is the term for the period between recessions.) This week I will look at the effect of cutting back on government spending during and just after a recession. I'm going to do that with three graphs. The first shows the length (in months) of every expansion since 1929. The second looks at the annualized growth in real GDP per capita for each expansion period, and the third looks at the total growth rate in real GDP per capita over the length of the expansion period. In each graph, recoveries are divided into three groups based on what happened to the federal government's spending as a share of GDP from the start of the recession to the period one year after the end of the recession.

Bad Analysis At The Deficit Commission -Krugman - The Center on Budget and Policy Priorities worries that the Obama budget commission is already giving ammunition to the deficit crazies; it cites testimony by Carmen Reinhart claiming that gross debt, not debt owed to the public, is the right measure. I agree that this is off base. But there’s actually a worse problem: I’m a great admirer of the Reinhart-Rogoff work on crises — but NOT of their work claiming that 90 percent debt/GDP ratios constitute a red line, which isn’t at all up to the standard of the other material. It’s based on a crude correlation — and as soon as you look at specific examples, it starts to look all wrong. I wrote about it here. Reinhart and Rogoff specifically cite data from the United States showing slower growth when debt was above 90 percent of GDP. But if you know the data at all, you know that so far, the only years in which US debt was above 90 was in the immediate postwar period, when growth was indeed slow — but not because of the debt burden; instead, the US was demobilizing after the war, with many women leaving the paid work force. So it’s a terrible example to use. And I suspect that much of the rest of their result reflects reverse causation:

Summers: The Fiscal Questions Don’t Change, The Answers Do. -This year’s U.S. federal budget deficit is projected at $1.5 trillion, but Mr. Summers said that a recovering economy and President Barack Obama’s policy proposals — like the freeze in non-security spending and the expiration of the high-income tax cuts — will cut this budget deficit in half as a share of the economy. But deficits, on current projections, will still be in the 4% to 5% of GDP implying steady and unsustainable and unacceptable increases in the ratio of our national debt to our income.So what to do? “In the tradition of the two-handed economists,” Mr. Summers said, “I emphasize both the seriousness of our current cyclical situation and the magnitude of the budget challenge we face because I am convinced that is impossible to sensibly address either challenge in isolation

A sticky gas-pedal - The Economist -The “American Jobs and Closing Tax Loopholes Act” is a typical piece of congressional sausage-making originally projected to add $134 billion to the federal deficit. Only $79 billion of that qualifies as true stimulus: extended unemployment benefits, health subsidies for the unemployed and more Medicaid money for the states. Most of its hundred-odd other provisions are goodies for assorted constituents from Indian reservation property developers to cotton shirt manufacturers and routine extensions of expiring provisions such as the research tax credit.

Pork Barrel Tax Provisions in the Extenders Bill - Reading through the tax provisions of the misnamed "American Jobs and Closing Tax Loopholes Act of 2010" is like reading a pork barrel laden appropriations bill. The vast majority of the so-called tax cuts are essentially earmarked spending through the tax code. Below is a short list of some of the more glaring giveaways in the bill. Some of the bigger winners are local governments who will benefit from taxpayer-subsidized bond authority and the alternative energy industry who are getting a windfall of targeted tax credits. The more curious "business" tax breaks are the tax benefit for "certain motorsports entertainment complexes" and the special expensing rules for film and television productions.

To extend or not to extend, Pew (do you) Trust - The Pew Trust has published a study of the cost of extending the Bush tax cuts: Decision Time: The Fiscal Effects of Extending the 2001 and 2003 Tax Cuts. As surely all ataxingmatter (and Angry Bear) readers are aware, the Bush tax cuts were enacted with sunset dates. Some of those sunsets were 2008 but were extended to 2010. The Bush Congress intended to make the cuts permanent, but knew the price tag would be too high. So instead they used the sunset gimmick to pretend that the tax cut wasn't really a major cause of increasing deficits. Now the bill is due. And of course, Congress is today debating an "extender" bill for many of those cuts, that will be financed, at least, by other revenue increases, unlike the original Bush cuts.

Why I Changed My Mind about Tax Cuts – Thoma - The experience from the first attempt at using tax changes to stimulate the economy, the Bush tax rebate of Spring of 2008, suggests that temporary tax cuts of this variety are largely saved. Here’s an estimate of the effect of the Bush tax rebates from the Congressional Budget Office. It shows that the rebates drove income up quite a bit, but consumption hardly budged:The lack of impact on aggregate demand (consumption) is due to how the tax rebates were distributed. The tax rebates went to a lot of people who really didn’t need them, and they chose to save the extra money.But better targeting can fix this. Thus, I thought that the best way to do the second stimulus package, the one Obama put into place a little over a year ago, would be to have well-targeted tax cuts go into effect as fast as possible to give the economy an initial jolt. This would be followed by government spending, which takes a bit longer to put into place. As this spending came online it would sustain or even strengthen the impact on aggregate demand provided initially by the tax cuts, and, importantly, the spending would be sustained until the economy was clearly on its way to recovery.

Why Not Impoundment? -The Obama administration has announced another effort to give the president some sort of line-item veto authority. Since the Supreme Court has made clear that a statutory line-item veto is unconstitutional--Republicans gave it to Bill Clinton in 1996 and it was ruled unconstitutional in 1998--Obama is asking for enhanced rescission authority. Basically, the president would ask for spending cuts and Congress would be forced to vote upon them as a package.I have no problem with this legislation; I do believe that insofar as the budget is concerned that the president needs more authority vis a vis Congress. However, I think there really is a much simpler way of getting around the constitutional problem--just repeal the part of the Budget Act which prohibits impoundment. In essence, impoundment means that if the president doesn't want to spend money appropriated by Congress he simply impounds it; i.e., doesn't spend it. It has exactly the same effect as a line-item veto and is unquestionably constitutional--every president up until Nixon had and routinely used impoundment to control spending.

Last Word on Impoundment - I don't want to get into an argument with Stan, whose knowledge of the Budget Act is certainly superior to my own. Nor am I in the mood to research the legislative history of that legislation. But I do think that Stan misunderstands the precise meaning of the word impoundment. In this respect, I quote Justice Scalia from Clinton v. New York, the 1998 case that found statutory line-item veto unconstitutional:.. Given that impoundment was used by virtually every president dating back to the earliest days of the Republic, I think it's a stretch for Stan to say the practice was illegal. On the other hand, impoundment is clearly a less satisfactory means of controlling spending than a line-item veto, which explains why Grant, FDR and JFK all asked Congress for line-item veto authority.

Spending Through The Tax Code - Forbes.- Conservatives are united in their belief that government spends much too much and that spending ought to be cut sharply. But they almost universally ignore de facto spending through the Tax Code even though many tax provisions are functionally identical to spending. These "tax expenditures" not only hemorrhage revenue unnecessarily, but they distort private decision-making, create unfairness and reduce economic growth. in 1961 the top marginal income tax rate was 91%, meaning that reducing one's taxable income by $1 saved 91 cents in taxes for those in the top bracket, while earning $1 of additional income netted them only 9 cents. For some people it was worth spending 90 cents to reduce their taxable income by $1, which gave rise to many wasteful tax shelters designed to produce nothing except tax deductions.