Foreign Central Bank Custody Holdings At $3.066 Trillion As of Wed -Fed - The U.S. Federal Reserve's balance sheet contracted slightly in the latest week as discount window borrowing by commercial banks posted yet another decline. The Fed's asset holdings in the week ended April 28 slid to $2.334 trillion from $2.341 trillion a week earlier, the Fed said in a report released Thursday.Total discount window borrowing slipped to $78.37 billion on Wednesday from $ 78.42 billion a week earlier.Borrowing by commercial banks through the Fed's discount window fell to $5.51 billion on Wednesday from $6.11 billion a week earlier.U.S. government securities held in custody on behalf of foreign official accounts rose to $3.066 trillion from $3.052 trillion in the previous week. Treasurys held in custody on behalf of foreign official accounts as of Wednesday climbed to $2.277 trillion from $2.267 trillion in the previous week.Holdings of agency securities rose to $789.18 billion from the prior week's $ 785.60 billion. Further data on the Fed's balance sheet, including a breakdown of district-by- district discount window borrowing, can be found at http://www.federalreserve.gov/releases/h41/Current/h41.pdf.

U.S. Fed's balance sheet dips in latest week (Reuters) - The U.S. Federal Reserve's balance sheet fell slightly in the latest week, Fed data released on Thursday showed. The Fed's balance sheet -- a broad gauge of its lending to the financial system -- decreased to $2.313 trillion in the week ended April 28 from $2.320 trillion in the previous week. For a graphic on the Fed's balance sheet data, see link.reuters.com/vuq99j

Former Fed Staff on 2011 Rate Hikes, Balance Sheet Woes - The Wall Street Journal had a chance to moderate a panel on the outlook for Federal Reserve policy at the Milken Institute’s global conference in Los Angeles yesterday with a group of astute Fed watchers. Here are the highlights and a link to a video of the full discussion: IN SUM: Tightening policy is going to be enormously complicated. The path of least resistance for the Fed is to sit still for as long as it can. The economy might give it reason to do just that. Futures markets are pricing in a Fed rate increase by the end of the year, but the smart money inside the Beverly Hills Hilton had its doubts. We asked the audience — filled with money managers and bankers — for a show of hands on when the Fed was likely to raise rates. Fewer than a third shot up for 2010 and much of the rest went up for 2011 or later.

Fed Authorizes Tool to Drain Liquidity - The Federal Reserve authorized a tool that could be used to drain some of the liquidity it injected into the economy to fight the financial crisis.The Fed on Friday said it approved the offering of term deposits for lenders who are eligible to collect earnings on their balances at the Fed’s Reserve Banks. The tool could be used by the Fed if needed to sop up money built up in the banking system before the money excites inflation. The Fed’s total portfolio of loans and securities expanded after the financial crisis struck. The central bank proposed the term deposits in December and asked for public comment. Term deposits have specified maturity dates and are held by eligible institutions at Reserve Banks. The deposits will be offered through a term deposit facility.

Fed Intends to Keep Rates Low - The Federal Reserve's policy making committee still has its lasers focused on the weak points in this economic recovery. In the minutes of the open market committee meeting, released today, the Fed noted that the economy is improving but it also noted ongoing weakness in the labor market and the fact that bank lending continues to contract. It didn't need to say anything about the debt crisis rolling across Europe--that's the elephant in the room. The bottom line: Don't worry about inflation or interest rates; worry about the economic recovery. And, thankfully, that's just what they are doing. The Fed is not only keeping the Fed Funds rate near zero, there is also no evidence that they have begun to shrink their balance sheet, nor are they anywhere close to selling off the $1.5 trillion in mortgage securities that they are sitting on. The good news there is that both long and short-term interest rates should stay tame for the foreseeable future.

Parsing the Fed: How the Statement Changed - The Fed’s statement following the April meeting was nearly identical to March’s remarks. The central bank continues to see economic improvement, but makes no signal that rates are going to rise in the near term. April included the third consecutive dissent over the language used to describe low rates. (Read the full April statement.)

Alford: Fed Talk As Policy - The Fed believes that it has succeeded in making monetary policy significantly more transparent. Furthermore, the Fed believes that by being transparent it can influence market expectations and the behavior of the real economy. This is the basis for the emphasis on “talk as policy”. However, one can ask: has rhetorical guidance regarding the Fed funds target made policy significantly more transparent than in the past? Assume for the moment that, in an effort to make its next statement less repetitive, the Committee decided to replace the word “extended” with a synonym – “prolonged” Is there any doubt that the markets would react to the changing of the word “extended”, even if it was only to replace with one of its synonyms?

The Lone Dissenter: Another Month, Another Hoenig Dissent - The long-serving official again opposed the central bank’s decision to keep rates very low for an extended period on Wednesday, his third such action in three straight policy gatherings. While the Fed officials who endorse that view say the rate outlook ultimately depends on how the economy performs, financial markets see the language as a pledge the current 0% interest rate policy stance will be maintained for months to come, perhaps even into next year. Hoenig worries the Fed is creating the conditions for future financial imbalances, and he frets the central bank is limiting its flexibility. In comments this year, Hoenig has also suggested the Fed should get around to raising rates sooner rather than later, arguing even a modest tightening would still leave monetary policy very supportive of growth. It should be noted that Hoenig’s dissent is tied to the language, not the policy decision. The statement doesn’t indicate that he wants rates to be higher, just that he wants to remove the “extended period” language to give the Fed more flexibility.

Do you notice the end of ZIRP? - There was not much reaction to the latest Federal Open Market Committee statement on Wednesday – and nor should there have been. After all, there’s been no real change in the language employed. But examine this chart, mapping the overnight Fed Funds rate in the US over recent months: The official range, established in December 2008, may remain at “zero to 0.25 per cent” – but the actual price of money is most definitely trending higher. In fact, a little over 20 basis points is now typical in overnight trade. That might be a small rise, in nominal terms, from the 10 bps or so seen earlier in the crisis – but it’s certainly a shift away from the zero interest rate policy. America has stopped turning Japanese.

The Fed at a Crossroads - Here's the video from The Fed at a Crossroads panel discussion that I said I'd post:

How the Fed Will Read Latest GDP Numbers - Federal Reserve officials have made it clear in recent weeks that their decision about when to raise interest rates will depend heavily on how the economy performs vis-à-vis their forecast for growth and inflation. If growth underperforms or inflation comes in below expectations, the odds of a rate hike go down. The odds go up if the opposite happens. So what do the first quarter forecast tell us about how the economy is doing? Growth is coming in around as expected though it’s still not convincing growth. Inflation is low and has the potential to come in well below the Fed’s forecast. The Fed expects gross domestic product to grow at an annual rate between 2.8% and 3.5% this year. At 3.2%, the first quarter came in right on target. However, it is still heavily weighted toward inventory rebuilding. The Fed wants to see more sustained consumer spending and investment before being convinced the recovery is healthy and self-reinforcing.

Obama to Nominate Yellen, Raskin, Diamond to Fed Board - WSJ -President Barack Obama plans to nominate two economists and a lawyer to the Federal Reserve Board on Thursday, reshaping the central bank's top ranks at a critical period for financial regulation and monetary policy. The White House on Thursday will tap Janet Yellen, president of the San Francisco Federal Reserve Bank, to be the board's vice chairman, and Massachusetts Institute of Technology economist Peter Diamond and Maryland state banking regulator Sarah Bloom Raskin to sit on the seven-member board, according to people familiar with the mater. The Senate is likely to confirm them.

Obama Nominates Yellen as Fed Vice Chairman - Putting a bigger stamp on the Federal Reserve, President Barack Obama on Thursday chose Janet Yellen as vice chairwoman of the central bank and filled two other vacancies on the board, which has enormous power over Americans' pocketbooks. His moves come as the Fed, whose decisions influence economic activity, employment and inflation, is facing political and economic challenges. The Fed is steering the economy out of the worst recession since the 1930s, and legislation to overhaul the financial system would eliminate some of the Fed's authority while giving it new responsibilities. Some lawmakers think the Fed overstepped its authority by bailing out some big financial firms during the 2008 financial crisis.

Yellen Touts “Maximum Employment” - Interesting catch from Annie Lowrey who notes that Janet Yellen put the Fed’s jobs mandate first when officially acknowledging her appointment as Vice Chair of the Board of Governors: I’m honored that President Obama has asked me to serve in that capacity. If confirmed by the Senate, I am looking forward to working even more closely with Chairman Bernanke and the other governors, and continuing to collaborate with my colleagues throughout the Federal Reserve System to conduct policies that foster economic prosperity and ensure a stable financial system. I am strongly committed to pursuing the dual goals that Congress has assigned us: maximum employment and price stability and, if confirmed, I will work to ensure that policy promotes job creation and keeps inflation in check.

Diamond nominated for Federal Reserve post - MIT News - MIT economist and Institute Professor Peter Diamond PhD ’63 has been nominated by U.S. President Barack Obama to serve on the Board of Governors of the Federal Reserve, the central bank of the United States. If confirmed to what would be a 14-year term, Diamond would be one of seven governors on the board. As a member of the Fed’s board, Diamond would automatically serve on the Federal Open Market Committee (FOMC), the group that influences economic activity, employment and inflation by setting key interest rates. At the moment, interest rates are low in an effort to spur lending, investment and growth following the deep recession that began in late 2007. In addition to nominating Diamond, Obama today announced he was naming two others to serve on the Federal Reserve’s central board: Janet Yellen, currently president of the Federal Reserve Bank of San Francisco (nominated to be vice chair of the Fed), and Sarah Raskin, a lawyer who is Maryland’s commissioner of financial regulation.

Understanding central bank operations - On the plane coming over, among other things, I read a paper written a couple of years ago by the Federal Reserve Bank of New York about the way in which monetary policy can be “divorced” from bank reserves. It is a useful paper at the operational level because it brings out a number of important points about bank reserves and the way central banks can manipulate them or ignore them. That is what this blog is about. In the September 2008 edition of the Federal Reserve Bank of New York Economic Policy Review there was an interesting article published entitled – Divorcing Money from Monetary Policy. It demonstrated why the account of monetary policy in mainstream macroeconomics textbooks (such as Mankiw etc) from which the overwhelming majority of economics students get their understandings about how the monetary system operates is totally flawed.

"I Don't Think They've Learned Anything"Those are the words of David Roche of Independent Strategies, who is "well known for his outspoken but prescient views" according to his website. Roche is referring to the U.S. government in general and the Federal Reserve in particular. He believes our beloved Central Bank should be raising rates now, not waiting for an "extended period." He's right, of course, but the U.S. economy still requires emergency life-support. Without that intervention, we would have the Depression we so richly deserve after a 25-year credit bubble. First the CNBC video and some selected quotes followed by some commentary. Roche: What they’re trying to do is start off more bubbles. If you look at consumer spending, it is picking up. Of course it’s picking up. U.S. households now get more money from the government than they pay in taxes … So, what the authorities are trying to do is actually to add state leverage, government bond leverage to private sector leverage so that the bubbles go on and the consumption goes on.

The Fed’s Hollowing Out Of U.S. Banks - Have the Federal Reserve’s unprecedented market and banking interventions fundamentally weakened America’s banks? In this article, we will illustrate how the Federal Reserve has been hollowing out the US banking system. We will show how the Fed has been creating a banking industry shell that looks strong on the surface, but is increasingly empty beneath that facade, with less and less economic strength, and an ever greater reliance on the Federal Reserve’s monetary creation ability. Using a single loan as an example, we will explore in step by step detail how almost 10 percent of US bank assets have been hollowed out, with former investments in the economy being replaced by excess reserve balances at the Federal Reserve. On paper, these balances are the highest quality assets which a bank can own, yet in economic reality, they represent an investment in nothing at all.

Goldman: Despite The Recovery, America Is Screwed Without More Easy Money From The Fed - Our analysis suggests that fiscal policy should start to “exit” from its current easy stance well before monetary policy, for two reasons. First, the link between an easy fiscal policy now—i.e., a large deficit—and a high debt stock in the future is virtually automatic. In contrast, the link between an easy monetary policy now and a financial asset bubble in the future is much less tight, though low interest rates and large Fed asset purchases do raise the odds of excessive housing and equity valuations. Our conclusion: very large benefits from continued easy monetary policy and—at least for now—small costs in terms of the risk of renewed asset bubbles strongly support our forecast that the federal funds rate will stay at its current near-zero level for much longer than generally expected. However, the case for fiscal policy is less clear-cut. While the benefits of continued accommodation are large, the costs look increasingly sizable as well. Hence, the fiscal “exit” should come well before the monetary one.

The Search for a Reserve Currency - Currency, like all forms of abstract value, is based on trust. And trust itself is based - except among the most naïve - on experience, and the repetitive demonstration of fidelity, whether positive or negative. At present, the US dollar, which had experienced a gradual rise during the 20th Century to the position gained well into the Cold War of being the trading world’s reserve currency. It had the mass, in terms of volumes of available currency; it had the backing of an indisputably wealthy national asset base to move away from the gold standard; it had stable governmental backing. All of that is evaporating. Not, in absolute terms, as far as the mass of currency available, because that has dramatically expanded in recent years, and particularly during the past year of the Administration of Pres. Barack Obama

Rich world may face next downturn with dull weapons |(Reuters) - Rich countries may not be able to resharpen their crisis-fighting tools fast enough to get them ready for the next downturn, leaving them increasingly reliant on cash-rich emerging powerhouses to ensure stability. Before the latest upheaval struck, advanced economies had enjoyed a relatively peaceful stretch dating back to the early 1990s. Aside from the 2001 recession, which proved to be mild, the financial trauma was largely centered in emerging markets. That has changed. As the International Monetary Fund has stressed in the run-up to this week's meetings of world finance officials in Washington, the biggest threats to the global recovery are concentrated in advanced economies now. Emerging markets, scarred by debt crises of the late 1990s, have built up an estimated $5.5 trillion in reserves as a form of self-insurance against future problems, but the rich world has no such cushion.

Do bank purchase of 10 and 30 year Treasurys spell trouble? - One of the notable observations in recent Treasury auctions has been the increasing participation by commercial banks in taking down 10 and 30 Year Treasury auctions - traditionally two parts on the curve banks have historically avoided like the plague. We present some observations on why this may be happening as well as some troubling conclusions, both of which indicate trouble, namely that liquidity is and has been the name of the game for the past 13 months, and that commercial banks, or presumably some of the smarter money around, are seeing economic distress ahead. Here are the preliminary observations from Morgan Stanley, the one outlier bank which sees rates jumping to 5.5% by the end of the year, and 4.5% by the end of June (by way of context):

Higher Inflation, Not Hyperinflation - Forbes - Last year the federal budget deficit was $1.4 trillion, or 10% of GDP, the largest "peacetime" deficit on record. This year will show some improvement, but not much, with a deficit in the vicinity of 8% of GDP. Meanwhile, the Obama administration projects that under its own policies--including higher taxes for the "rich" and an end to hostilities in Iraq--the deficit will never get down to the 3% of GDP it believes is sustainable over the long run, much less the 1.2% that prevailed as recently as 2007. Some analysts have proposed inflating/devaluing our way out of this debt crisis. These arguments have increased the fear of hyperinflation. The theory is that with deficits already so large and no immediate prospects for spending control, the U.S. government may have to resort to an Argentina-style monetary policy to pay for its largesse. At first glance, this is not so far-fetched. Overspending in Greece has created a fiscal crisis there, and some analysts think Greece would be better off leaving the euro so it could devalue its debt. While we are worried about rising inflation, we think the odds of hyperinflation in the U.S. are near zero.

Update on the Inflation Debate - Brian Wesbury and Scott Grannis remain concerned about inflation, citing the recent Producer Price report from the BLS. I remain an inflation skeptic based on the two charts above, which show that the 10-15% producer price inflation in the 1970s (bottom chart) was accompanied by much, much higher money growth (top chart). The core ingredient of inflation (producer or consumer) is money growth, and there just doesn't seem to be enough M2 money growth to generate 1970s-era inflation.

Achieving Fiscal Sustainability - Chairman Ben S. Bernanke Speech At the National Commission on Fiscal Responsibility and Reform, Washington, D.C. April 27, 2010 17 KB PDF

Bernanke: U.S. Needs Deficit Reduction Plan - Federal Reserve Chairman Ben Bernanke Tuesday said the U.S. needs to soon come up with a plan to cut the budget deficit, telling a White House debt commission it should look at how the tax system could be changed. Mr. Bernanke’s remarks kicked off the first meeting of an 18-member White House panel charged with drafting ideas to reduce the country’s $1.4 trillion deficit. President Barack Obama created the panel, which includes Republicans and Democrats from the House of Representatives and the Senate, and its focus is on determining the biggest threats America’s fiscal health. Mr. Bernanke has not spoken about taxes for a while. However, the Fed chief is being more cautious than his predecessor, Alan Greenspan, who made the controversial move of endorsing President George W. Bush’s tax cuts in 2001.

Bernanke Is Getting Scared.... You have to love this sort of utter claptrap... “Achieving long-term fiscal sustainability will be difficult, but the costs of failing to do so could be very high,” Bernanke said in remarks prepared for a speech today to a White House commission on the budget deficit. “Increasing levels of government debt relative to the size of the economy can lead to higher interest rates, which inhibit capital formation and productivity growth -- and might even put the current economic recovery at risk.” Really Ben? We need to review a few graphs again. Let's start with this one: This is the true deficit, measured simply by the amount of Treasury debt (including intergovernmental games) outstanding. Of note is that it has never decreased materially since 2001. Why is this important? Because every dollar that the government borrows and spends is one dollar that pulls forward demand from tomorrow and spends it today.

Bernanke: Path To Fiscal Salvation Requires Slash And Burn On Entitlements And Higher Taxes - Fed Chair Ben Bernanke likes to couch his language so that it doesn't look like he's saying anything dramatic, but the nut of his speech today on fiscal reform lays it out pretty plainly near the end: The ultimate goal of the commission's efforts should be to put us on a path to fiscal sustainability. One widely accepted criterion for sustainability is that the ratio of federal debt held by the public to national income remain at least stable (or perhaps even decline) in the longer term. This goal can be achieved by bringing spending, excluding interest payments, roughly into line with revenues. Unfortunately, most projections suggest that we are far from this goal, and that without significant changes to current policy, the ratio of federal debt to national income will continue to rise sharply. Thus, the reality is that the Congress, the Administration, and the American people will have to choose among making modifications to entitlement programs such as Medicare and Social Security, restraining federal spending on everything else, accepting higher taxes, or some combination thereof.

Tsunami of Red Ink - Global Look at National Debt and Who Owns US Debt - The Chicago Tribune had an excellent set of charts this weekend in A Tsunami of Red Ink regarding US government debt and who owns it, and also a comparison of US debt to the national debt of other countries.Click on the link at the top to see foreign holders of US debt country by country. The top three US debt holders are China, Japan, and the UK. Some will not believe those figures on debt to GDP comparisons. I don't either. For starters the numbers are from 2009. The footnote also says, if intragovernmental debt is included the figure is 83%. That number is approximately correct in my opinion (as of 2009). Some will want to count unfunded Social Security and Medicare liabilities out to 2050 or whatever. This is simply wrong. That would be like counting a car you intend to buy 3 years from now as part of your debt now.

The national debt and Washington's deficit of will - Bill Gross is used to buying bonds in multibillion-dollar batches. But when it comes to U.S. Treasury bills, he's getting nervous. Gross, a founder of the investment giant Pimco, is so concerned about America's national debt that he has started unloading some of his holdings of U.S. government bonds in favor of bonds from such countries as Germany, Canada and France. He's simply worried that Washington's habit of spending today the money it hopes to collect tomorrow is getting worse and worse. It even has elements of a Ponzi scheme, Gross told me. "In order to pay the interest and the bill when it comes due, we'll simply have to issue more IOUs. That, to me, is Ponzi-like," Gross said. "It's a game that can never be finished."

U.S Government Debt Since World War II - Below is some analysis of how the ratio of government debt to GDP has evolved in the United States since World War II. The data come from tables B-78 and B-80 of the 2010 Economic Report of the President. I deleted the "transition quarter" in 1977. The change in the ratio of debt to GDP can be broken into two components. One is the ratio of the primary deficit to to the current debt. The other is what I call the "erosion factor," which is the nominal interest rate minus the GDP growth rate. In a previous post, I suggested an analogy with a owning a rental property. The primary deficit is the operating loss on the property--rental income minus expenses, but not including interest. The "erosion factor" is the interest rate minus the price appreciation of the property.* As of 1946, the ratio of debt to GDP was 108.67 percent. From 1947 to 1970, it fell to 27.96 percent

The Federal Debt/Income Ratio - Think of Country X as a simplified version of the U.S. and Country Y as a simplified version of a European country with a higher debt/GDP ratio but a much smaller state and local sector. My point here is that debt/GDP, which shows country Y in much worse shape than country X, may not be the right way to compare the two countries. Instead, if you think in terms of debt/income ratio at the Federal level, they are in the same position. My point is that the fiscal adjustments in the U.S. needed to get the Federal debt down relative to GDP might be much larger relative to the current Federal budget than is the case in Europe. I hope that point is not lost in the various ways in which the example diverges from reality.

The Federal Debt: How To Lose A Trillion Dollars (NPR) Everyone knows that the federal deficit is a real and growing problem. It's so large, however — $12 trillion and spiking rapidly — that it can seem abstract. That's about to change. Serious consequences associated with deficit spending have long seemed like far-off problems, but they are now likely to hit the country with considerable force within the next several years. One is servicing the debt itself. Most people don't pay much attention to the interest payments the federal government makes every year. They haven't had to. Debt service has been manageable, thanks to low interest rates and consistent economic growth. But, according to the Congressional Budget Office, annual debt payments — currently about $200 billion — are set to skyrocket. CBO estimates that interest payments on the federal debt will total $916 billion by the year 2020

Déjà Vu All Over Again: On the Dismal Prospects for the Federal Budget - PDF Abstract - We provide new estimates of the federal budget outlook over 10-year and long-term horizons under three sets of assumptions: the Congressional Budget Office baseline, which assumes no changes in current law; an extended policy scenario, in which it is assumed that future Congresses act more or less like previous Congresses in extending expiring provisions; and the Administration budget. Under either the extended policy or the Obama policy scenarios, deficits are high and rising over the second half of the decade, despite the assumption that the economy is in full employment. In 2020, the deficit is projected to be between 5 and 7 percent of GDP and the debt/GDP ratio is projected to exceed 90 percent. These figures only deteriorate with the passage of time. The long-term fiscal gap – the size of the immediate and permanent change in spending or taxes needed to keep the long-term debt/GDP ratio at its current level – is in the range of 6-9 percent of GDP. Further health care reform can be an important part of reducing the fiscal gap, but the problem is far too large to be solved by plausible reductions in health care spending alone. Postponing the onset of a fiscal package will make the problem even harder: even just a 5-year delay in implementation would raise the required fiscal adjustment by about 0.4 percent of GDP, or almost $60 billion per year.

Treasury Redeems A Gargantuan $643 Billion In Treasuries In April - A week ago we were practically speechless when we showed that the Treasury had redeemed nearly $494 billion in Bills in April. A truly stunning number and an indication of just how much cash the Treasury needs to have access to to keep rolling its ridiculously short average maturity debt load. Today we stand even more speechless: according to today's DTS, the Treasury has now redeemed $596 billion in Bills in Aprils: an all time world record, even when accounting for the Fed's steroid abuse period of SFP 1 (we are currently in the second iteration). Add $47 billion in Notes and there are almost $650 billion in redemptions. This number is simply ridiculous. Forget the interest expense: this ever increasing roll is the number one danger to the US and world economy. Should the Treasury be unable to keep issuing shorter and shorter dated debt (and it already is skirting away from even the belly of the curve), it is for all intents and purposes game over.

Is the US Facing a Cash Crunch? - The US government is caught in a cash vise and is being squeezed between too slow a rebound in tax revenues and the limitations on how quickly it can realistically take its funding requirements to the US Treasury auction. The US Treasury was saved in March by what the government reports as “proprietary receipts.” Those receipts require an explanation that isn’t well publicized since it begs the question of what happens next month without the $117 billion journal entry. The March cash management numbers from the US Treasury’s Financial Management Service are alarming and in my estimation have become perilous. The economy is simply taking much too long to recover, which is affecting urgently required tax receipts. If the US Treasury issues even higher debt supply to the market too fast, it threatens driving up interest rates prematurely and thereby elevating already strained government financing costs despite already increased supply.

Sovereign Risk Prompts Review of Investment Strategies (WSJ) - Some money managers are preparing for the next stage of the global financial crisis -- a world where the traditional perception of risk has been turned on its head. Sovereign debt from the industrialized countries, particularly the U.S., the euro zone and Japan, was once perceived as the safest of investments and the benchmark by which to measure all other assets. But massive debt loads as a result of the global banking crisis eroded sovereign debt creditworthiness, meaning investors have to rethink long-held beliefs and investment strategies. Assets that were once perceived as risky -- such as emerging markets or corporate debt -- are now viewed as less risky than debt sold by large developed economies such as Spain. Greece's downgrade by Standard Poor's into junk territory this week is merely the tipping point in what is likely to be a fundamental adjustment process that will last much longer than most realize.

Goldman's Essay On Why The U.S. Debt Load Is "Not Too Concerning" - After losing all credibility (or whatever they had) with the markets, the objective media and Main Street, but not their clients, who were the ones losing the most for interacting with the squid, yet refuse to take their business elsewhere for fear of being locked out from the market monopolist with the greatest amount of inventory (yes, economies of scale when compounded with not so subtle forced liquidations of key competitors end up in monopolistic outcomes), now their economic team is taking a gamble with its own reputation (this is the team that won the best big bank economic team aware for 2009). In a note distributed to clients, entitled "What's the Right Measure of US Government Debt?" Andrew Tilton and Alec Phillips try to present the case that contrary to what you may have heard, the $12.8 trillion of US debt is not really worth losing sleep over. In fact the next time Goldman needs a bailout and the resultant $2-20 trillion of new debt are added to the make the 2s30s at about 100%, that should not be a source of concern either.

"Budget For A Declining Nation" - That was the title of today's luncheon talk to the National Economists Club by Urban Institute Fellow and former Deputy Assistant Treasury Secretary Gene Steuerle. A video and slides will be posted here. These are the main points he made. "What makes this fiscal crisis unique is that we can no longer depend upon economic growth to get out of it.""World War II is always held up as an example of running the national debt over 100%, but no one remembers that we drove it down below 70% within 6 years by the end of the Truman Administration." "The enormous budget squeeze of 2009 saw revenues fail to cover entitlement spending and interest for the first time.""We have a budget for a declining nation because we're increasing federal spending on consumption, and we're cutting federal spending for education and investment."

The Obama Deficit Commission: Five Issues to Watch - President Obama’s Bipartisan Commission on Fiscal Responsibility and Reform is having its first meeting today. As I peer at my bookshelf full of well-meaning policy prescriptions produced by similar panels over the years, I am skeptical at best. These enterprises are, as Dr. Johnson said of second marriages, “a triumph of hope over experience.” Still, you never know. As my colleague Gene Steuerle reminds me, few thought tax reform would get off the ground in 1984-85. Yet, by mid-1986, it had happened. As you consider the deliberations of the latest panel—a bipartisan gang of 18 that has until Dec. 1 to send Congress a non-binding deficit reduction proposal—here are five issues to watch.

Deficit reduction: argument by authority - The deficit hawks are going into high gear with their drive to cut social security and Medicare. President Obama's deficit commission is having a big public event on Tuesday in which many of the country's most prominent deficit hawks will tout the need to reduce the budget deficit. The next day, Wall Street investment banker Peter Peterson will be hosting a "summit on fiscal responsibility", which will feature more luminaries touting the need to get deficits under control. What will be missing from both of these events is any serious debate on the extent of the deficit problem and its causes. These affairs are not about promoting a real exchange of views on issues like the future of social security, Medicare, and public support for education, research and infrastructure, the purpose of these events is to tell the public that everyone agrees, we have to cut the deficit. And, this means cutting social security and Medicare. This is argument by authority.

Budget deficit: Economic stimulus is key in a recession - latimes - Tuesday was the opening meeting of President Obama's National Commission on Fiscal Responsibility and Reform. And Wednesday, the billion-dollar Peter G. Peterson Foundation convened its National Fiscal Summit, featuring prominent budgetary conservatives from both political parties, including key administration officials. Both groups are likely to come to the same conclusion: If Congress fails to hit a specific deficit target, then a cap on federal spending should kick in. Budget hawks tend to blame outlays such as Social Security and Medicare, and they are eager to put a lid on them.But there's a problem with all this fiscal alarmism. It confuses three entirely separate concerns: the current large deficits, which are caused by the deep recession; the long-term health of Social Security; and the inexorably rising costs of Medicare and of healthcare generally. If you unpack these issues, a different picture and set of choices emerges.

ND20 Bloggers Ready to Take On Deficit Hawks at D.C. Counter-Conference - The deafening screams of deficit hawks have reached a fever pitch as the Peter G. Peterson Foundation announces that it will hold a special summit “to launch a national bipartisan dialogue on America’s fiscal challenges.” The list of featured speakers reads like a FCIC subpoena, with Alan Greenspan and Robert Rubin set to stoke populist fear and proclaim the evils of government spending; ...There is pushback, however, and the Peterson Summit–along with the cronyism it represents–is being challenged. The Fiscal Sustainability Teach-In Counter-Conference, as it is being called, will be held the same day as the Peterson Summit — April 28th — at George Washington University in D.C. The purpose of the teach-in is to offer a counter-narrative to the recycled neoliberal arguments sure to be spouted at the Peterson Conference. Unlike the Peterson Conference, the teach-in is free and open to the public, with the goal of expanding economic debate, not constricting it to the status quo.

Notes from the Fiscal Sustainability Teach-In - I just got back from the Fiscal Sustainability Teach-In organized by letsgetitdone, selise and others who regularly post and comment here at The Seminal. The event is a bottom-up grassroots response to Pete Peterson and the President’s "catfood commission" – which is already talking about putting things like Medicaid and Social Security on the chopping block in the name of reducing the deficit. If you were able to attend the teach-in, or if you follow the noted economists and presenters who appeared there, you might know that things like full employment are much more important than national deficits, and that the U.S.’s fiscal policy on things like Social Security isn’t nearly as much of a cause for alarm as the right-wing "deficit hawks" might have you believe

Hard To Take New Peterson Foundation Deficit Reduction Survey Seriously - In advance of the "fiscal summit" it's holding today, The Peter G. Peterson Foundation yesterday released a survey that it says shows “broad agreement” for a serious deficit reduction effort. Except that it doesn't. The survey is of 58 of the "most senior economic officials from the last eight administrations and Congressional leaders from the past 30 years." Frankly, I'm not sure how seriously anyone should take the opinion this group about the current need to reduce the deficit and national debt given that all of them were responsible in some way for adding to or not dealing with it when they were in office and actually had an opportunity to do something about it. But putting aside that admittedly snarky comment, the survey results are suspect for a number of reasons.

Bond Traders Declare Inflation Dead After Yields Fall (Bloomberg) -- The bond vigilantes who punished governments for profligate spending in past years have gone into hiding. Sovereign bonds yield an average 2.385 percent, about the same as a year ago and below the average of 3.08 percent in 2008 when the credit market seizure led investors to seek the safety of government debt, according to Bank of America Merrill Lynch index data. The cost to borrow is steady even though the amount of bonds in the index that includes nations from the U.S. to Germany and Japan has grown to $17.4 trillion from $13.4 trillion two years ago. While the debt helped the global economy recover from its first recession since World War II, yields show bond investors aren’t troubled that the growth will spur inflation..

The Tax That Hides in Your Paycheck - NY Times: Every year at tax time, libertarians indignantly denounce government income transfers from rich to poor. Society’s income distribution, they argue, should reflect as closely as possible what people would earn in unregulated private markets. ... As closer scrutiny of that premise will make clear, the libertarian denunciation of income transfers fails on its own terms. The main problem is that private pay patterns embody an implicit tax that is actually far more progressive than the federal income tax. To understand why, first consider some background about the way these patterns work. Economic theory holds that in competitive labor markets, workers are paid the market value of what they produce. In actual markets, pay does rise with productivity, but not by much. The most productive worker, for example, might produce twice as much as his least productive colleague, but is rarely paid even 30 percent more.

When We Will Get a VAT - The recent mini-boomlet for a value-added tax (VAT) that was kicked off a few weeks ago when former Federal Reserve chairman Paul Volcker indicated support for the idea is now officially over. Jackie Calmes of the New York Times quotes him this morning as dismissing the VAT for the time being. "I don't think it's on the political table for now or for the indefinite future, but that's the kind of thing you have to look at," Volcker said. Since his brief comment of support on April 6, the right-wing crazies have been having a field day denouncing it. No doubt, millions of pieces of direct mail have already been dropped to raise money for an all-out war against the VAT. Thousands of little old ladies will be induced to sign over their Social Security checks for dubious campaigns against a tax that has no chance whatsoever of being enacted for many years. Since there is nothing to keep at bay, all such contributions will simply go into the pockets of executives at the organizations sponsoring these direct mail campaigns and the companies that do the mailing.

Dividends Tax Rate Next Year? - Congress is beginning to realize how expensive it will be to cap the dividends tax rate at 20% for those earning over $250,000 beyond the end of this year. Yesterday, House Ways and Means Chair Sander Levin (D-MI) told the Bureau of National Affairs that it would be "very expensive" and that there was no provision for exempting it under the Budget Act or for "paying for" it at a cost of $138 b. FY11-FY20. Congressional taxwriters have spent the last few months struggling to find ways to "pay for" $31 b. of extensions of expired tax provisions and would have a much more difficult time finding $138 b. worth. President Obama has proposed setting the dividends and capital gains rates at 20% for all taxpayers. So far, there have been no signs that Congress is ready to grapple with the issue of extending the 2001 and 2003 Bush tax cuts. It could easily fall over until a lame duck session after the election.

More American Expatriates Give Up Citizenship — Amid mounting frustration over taxation and banking problems, small but growing numbers of overseas Americans are taking the weighty step of renouncing their citizenship. “What we have seen is a substantial change in mentality among the overseas community in the past two years,” said Jackie Bugnion, director of American Citizens Abroad, an advocacy group based in Geneva. “Before, no one would dare mention to other Americans that they were even thinking of renouncing their U.S. nationality. Now, it is an openly discussed issue.”

Finding the “Relatively Easy” in a World of Hard Choices - A Wall Street Journal article by Corey Boles describes the tough work cut out for the President’s fiscal commission, meeting on Tuesday for the first time:“We’re afraid the solutions they focus on will be entitlement cuts which are completely unwarranted,” Roger Hickey, co-director for the Campaign for America’s Future, an umbrella organization of liberal groups...Brian Darling, director of Senate relations at the Heritage Foundation, a conservative think tank, said he feared the Obama administration would use the panel to justify tax increases.“The bottom line is if you give politicians an easy way out they will take it,” . “And the easy way out in this case is tax increases and not cutting spending programs.” Well, tax increases are certainly not the “easy way out.” Just ask the Democrats in Congress why they weren’t lining up to sign onto Senator Conrad’s budget resolution

A Democratic Cry For Help - I have periodically advocated a "Megan Tax" for certain consumer goods which are, I believe, God's way of telling you that you have too much money for your own good. It is my belief that if you buy a $20,000 Hermes handbag (after putting yourself on a waiting list for some), or a Harrier, this is a sort of cry for help. Your money is overcrowding your life so much that you have become unable to deploy it wisely. In the event of such a tragedy, I have suggested, the government should swoop in, take half your money, and donate it to the Children's Scholarship Fund. You will breathe freer, and some poor kids will get a shot at a decent education. Gains from trade!

Fair and Substantial—Taxing the Financial Sector - iMFdirect - We knew we were in for a tough time when the leaders of the Group of Twenty (G-20) asked the IMF to give them our views, at their summit coming up in June 2010, on “… the range of options countries have adopted or are considering as to how the financial sector could make a fair and substantial contribution toward paying for any burden associated with government interventions to repair the banking system.”Everyone has strong feelings these days on the taxation of the financial sector. Taxpayers who financed the rescue of the financial sector during the recent crisis want their money back—or at least not to get caught again. Some want to see more of the money coursing through the financial system turned to public use.

All for One Tax and One Tax for All? - Rogoff - Recently, the IMF proposed a new global tax on financial institutions loosely in proportion to their size, as well as a tax on banks’ profits and bonuses.The Fund’s proposal has been greeted with predictable disdain and derision by the financial industry. More interesting and significant are the mixed reviews from G-20 presidents and finance ministers. Governments at the epicenter of the recent financial crisis, especially the United States and the United Kingdom, are downright enthusiastic, particularly about the tax on size. Countries that did not experience recent bank meltdowns, such as Canada, Australia, China, Brazil, and India, are unenthusiastic. Why should they change systems that proved so resilient? But the IMF’s big-picture diagnosis of the problem gets a lot right. Financial systems are bloated by implicit taxpayer guarantees, which allow banks, particularly large ones, to borrow money at interest rates that do not fully reflect the risks they take in search of outsized profits. Since that risk is then passed on to taxpayers, imposing taxes on financial firms in proportion to their borrowing is a simple way to ensure fairness.

Who's Afraid of a Bank Tax? You won’t be surprised to learn that Wall Street doesn’t like the idea of a bank tax. Wall Street lobbyists argue that a tax on banks — meant to discourage risky investments and cover the costs of financial crises — will keep banks from being able to lend to worthy borrowers. That’s not theoretically impossible, but it doesn’t seem very likely. The taxes under discussion would have a low rate. It’s also worth remembering that Wall Street’s lobbyists often claim that they are just looking out for the interests of borrowers A more surprising bit of opposition comes from regulators in Canada and Australia. Those countries survived the bust better than most, in part because of tougher oversight of their financial sectors. Now, with the International Monetary Fund suggesting a globally coordinated bank tax, Canadian and Australian officials are saying that their banks shouldn’t be punished alongside American and European banks.

Deja Vu Time: G-20 as Bretton Woods Rehash - To its credit, the G-20 process seems to be making meaningful progress on fronts I thought would be sacrosanct only a few months ago: cracking down on tax havens; increasing transparency of hedge fund positions; regulating "systemically important" banks; and even a then-unheard one of charging these banks for the public service of bailouts going forward. We now know that the current IMF head has proclaimed the death of the Washington Consensus, while its quest for ever-freer capital flows has been abandoned (for now). Now, Eric Helleiner makes an number of salient points, First, the Bretton Woods conference was itself a UN-sponsored event. Second, as we often forget, the World Bank and IMF are nominally under the umbrella of the UN system. Thus, UN bodies alike UNCTAD should have a way in how these institutions function. Third, many of the issues we face today--regulating capital flows, accommodating heterodox (read: contra Washington Consensus) policies, and what else have you were also the points of debate at Bretton Woods.

The carry trade is back – The shift in global economic conditions to an “expected growth” mode brings into play the traditional carry trade. This trade works by selling or borrowing low interest currencies and buying the higher interest paying currencies. It is a play on interest rate differentials. In a sense, there always will be a carry trade as long as there are differences in interest rates between countries. In pre-crisis years, the Japanese yen was the favorite carry trade currency, as the yen held the status of the lowest interest rate currency. This was followed to a lesser degree by the use of the Swiss franc and even the U.S. dollar. Forex traders would play the carry trade by selling these currencies against currencies offering higher rates such as the British pound, Australian and New Zealand dollars. The world became afloat in borrowed yen and U.S. dollars. This trade strategy collapsed as trillions of yen and U.S. dollars had to be quickly bought back during the global de-leveraging that occurred. However, now with global conditions changing toward growth, the carry trade is back.

Q&A: Volcker on Bank Regulations - Former Federal Reserve Chairman Paul Volcker relishes tough assignments. As Federal Reserve Chairman from 1979 to 1987, he tamed inflation by pushing interest rates to 20% — and withstood withering criticism as the economy sank into recession. Since then he has investigated corruption at the United Nations and World Bank and uncovered tens of thousands of Swiss bank accounts that may have belonged to victims of the Holocaust. His once intimidating presence has softened now — he long ago gave up smoking cigars and lets his mischievous side show through. But at 82, he’s taken on another big assignment: remaking global banking regulation.. He sat down for a conversation with The Wall Street Journal’s Bob Davis, before the controversy over Goldman Sachs dominated the headlines. Below is an edited transcript.

The Rules of the Game? -Maxine Udall (girl economist) - I've been thinking about "the rules of the game." Consider this from a recent ProPublica article on Magnetar: there was nothing illegal in what Magnetar did; it was playing by the rules in place at the time. “The rules in place,” I said to myself. “What does this remind me of?” And then I remembered: "There is one and only one social responsibility of business—to use its resources and engage in activities designed to increase its profits so long as it stays within the rules of the game, which is to say, engages in open and free competition without deception and fraud." --Milton Friedman. The rules of the game must be changed. They must be changed now. And they must be changed in ways that serve the public interest. Investment banks and bankers must be regulated. Leverage, transparency, size. I'm sure there is more. Toxic assets, toxic instruments, and toxic casino-like speculation are no different from toxic patent medicines. They harm us all.

Brains on Drugs - As it considers how to regulate the financial sector, Congress should heed the lessons of the Food and Drug Administration. As this issue goes to press, congressional deliberations on the mammoth financial reform bill have entered the trench-warfare stage, over a seemingly obscure question: where to put the new Consumer Financial Protection Agency (CFPA), which will centralize the writing and (to some degree) enforcement of federal financial regulations on such things as mortgages, savings accounts, and consumer debt. Should it be an independent agency, like the Securities and Exchange Commission, or a subunit of the Treasury Department or the Federal Reserve?

Jimmy Stewart is dead: Break up the banks... I think the undoing of Goldman will be that its execs, just like those at Morgan Stanley, or GE, or GM, have failed to understand that their own personal wealth can only last as long as the "lower classes" have at least a decent life. A chance to feed their kids and send them to a proper school, to get proper medical treatment for their families if and when required, and, when they age, to draw sufficient retirement funds not to suffer from hunger and cold. The Blankfeins and Jamie Dimons of the planet have no idea who these people are, or what they think, what they're going through, many hundreds waiting in line for an entire day for a handful of low-paid jobs. See, if you make $20,000 a year, and many wish they'd make that much, you have to worth for 500 years to get to that $10 million. Lloyd Blankfein made over $400 million in the past decade.

Can't Anybody Here Play This Game? – Krugman - Bear with me while I vent for a moment. On financial reform, there are clear villains in the political process: But at this point I’m accustomed to that sort of thing. What’s frustrating is the way people who favor reform keep getting pulled off into side issues and obvious misinterpretations. If you want to push too-big-to-fail as a key issue, fine; but please don’t say that resolution authority is encouraging too-big-to-fail, because we don’t have anything like that for smaller banks; it’s just not true: the whole point of resolution authority is to recreate for shadow banks the same kind of authority the FDIC already has for smaller, old-fashioned banks. If you want to argue that Wall Street is corrupt, fine; but don’t use emails showing Goldman employees crowing over their success in shorting housing — which is ugly but doesn’t amount to wrongdoing — to make your point.

How the Ratings Agencies Lost the Will to Say 'No' - Friday's congressional hearing on the role of the ratings agencies in the financial crisis featured three panels: The first, filled with ex-employees of Standard & Poors (MHP) and Moody's (MCO), told a dark, detailed tale of how the ratings agencies produced inflated ratings. Rather than claim management deliberately required inflated ratings, the ex-employees suggested that massive underfunding and understaffing of the ratings departments coupled with a shift to a customer-satisfaction culture -- customer being defined as the banks issuing the securities, not the market at large -- inexorably led to inflated ratings.

Senate Subcommittee cracks down on credit rating agencies… A slew of internal e-mails from the leading credit rating agencies show employees at those firms knew of the dangers in subprime mortgages, but gave them the seal of approval anyway. "Let's hope we are all wealthy and retired by the time this house of cards falters. :o)," wrote an employee from Standard & Poor's Rating Agency in an internal e-mail in December of 2006.This is frightening. It wreaks of greed, unregulated brokers, and 'not so prudent' lenders," said one S&P internal e-mail dated September 2006. And another from that same month: "...this is like another banking crisis potentially looming!!" The e-mails and other documents were presented as evidence at a hearing on Capitol Hill Friday, part of an 18-month investigation by the Senate Permanent Subcommittee on Investigations, led by Senator Carl Levin, examining the causes of the financial crisis.

Berating the Raters – Krugman - Let’s hear it for the Senate’s Permanent Subcommittee on Investigations. Its work on the financial crisis is increasingly looking like the 21st-century version of the Pecora hearings, which helped usher in New Deal-era financial regulation. In the past few days scandalous Wall Street e-mail messages released by the subcommittee have made headlines.That’s the good news. The bad news is that most of the headlines were about the wrong e-mails. When Goldman Sachs employees bragged about the money they had made by shorting the housing market, it was ugly, but that didn’t amount to wrongdoing.No, the e-mail messages you should be focusing on are the ones from employees at the credit rating agencies, which bestowed AAA ratings on hundreds of billions of dollars’ worth of dubious assets, nearly all of which have since turned out to be toxic waste. And no, that’s not hyperbole: of AAA-rated subprime-mortgage-backed securities issued in 2006, 93 percent — 93 percent! — have now been downgraded to junk status.

What to do about CDO ratings II - I have two proposals (last time I only had one). One is to give up on the ratings agencies. They were geese that laid golden eggs providing an immensely valuable service for a tiny fee, but we've killed them. Regulations could be based on firms which put a whole lot of money where their mouth is. Those would be firms which write CDSs. Personally I trust the vampire squid. If G-S is willing to write CDSs with huge notional value on something and sell them for y basis points per year, I'd guess they are pretty safe. GS may or may not be evil but they sure aren't stupid. This reform would have to wait until the idiot CDS writer problem is solved (can you say AIG-FP ?).Short of that, I'd say it would work fine to require the agencies to insure 0.01% of anything they rated. It takes a long time for instruments to actually default, but if the agencies balance sheets included CDS written and marked to market, they would be much much more careful. A problem with this proposal is that the incentives are too long term. The solution is to make compensation above say $500,000 a year of officers of, for example, ratings agencies be paid only in stock which can't be sold for 10 years.

Time to rein in the ratings agencies - The organisations on political trial last Friday were the ratings agencies Moody’s and Standard & Poor’s, which played a more central role than any investment bank in the failure of so many investment-grade securities. If all the subprime mortgage securities they rated triple A had not turned to junk, no bail-outs would have been required. The stories that former Moody’s and S&P employees told at that hearing – of the agencies trying to please investment banks that were paying big fees to get high ratings – cast doubt on a central plank of how the fixed-income markets are supposed to work. Why should investors place faith in these over-rated bond market guardians again?

Watching the Watchers - Credit-rating agencies exist to evaluate the safety of debt securities. Imagine for a moment that they had done their job when financial go-getters began churning out bonds backed by sketchy loans and the dream of endlessly rising home prices. Properly labeled as junk, those bonds would have found few buyers. Denied access to the vast reservoirs of capital held in mutual, money-market, and pension funds, the go-getters would have ended up as minor players. And millions of Americans might still have the jobs, homes, retirement savings, and economic security they lost. The first imperative of reform, then, is to align the incentives of these badly corrupted entities with their mission.

Ratings failure - I should say upfront that I absolutely loathe rating agencies. I do not think rating agencies should even exist. However, people blame rating agencies for a lot of stuff that is not exactly their fault. There seems to be a lot of confusion about what exactly constitutes a “ratings failure.” Take this column by John Gapper in the Financial Times, for example: The ratings failures went beyond synthetic mortgage CDOs. BMS’s audit committee had questioned treasury staff about whether they were making any risky investments.“They said everything was in treasuries and nothing more than 90 days [maturity], triple A. What were they in to the tune of $800m? Auction rate notes, triple-A rated by the agencies,” he said. Mr. Robinson said that this cost BMS $600m when the auction rate note market collapsed in February 2008.One cannot fault the rating agencies for the collapse of the auction rate securities market. Auction rate securities typically had long-term nominal maturities, but with rates that were periodically reset at short-term intervals through an auction process. So long as there was sufficient investor demand for the securities, these securities were liquid investments.

Ezra Klein - Should we nationalize the ratings agencies? - Kevin Drum says that the issue with the ratings agencies is more complicated than people realize. Obviously it's a problem that the ratings agencies are paid by the banks whose products they're rating. But, Drum says, the common solution -- to have a regulator assign the ratings agencies rather than letting the bank do it -- will create problems of its own. If you do this, the ratings agencies no longer have any incentives to do much of anything; their incentive would be to hire the cheapest possible analysts and cut costs to the bone. Actually, why not? This is a question I've asked for a long time and never gotten a really good answer to. The ratings agency business has two apparent settings: Hopeless conflict of interest or heavily regulated utility with an incentive to cut costs. But they play a very important role in the system. So why not make them -- or some basic version of them -- public? It would be better for both accountability and incentives.

The Case for Ratings Agency Deregulation (vimeo) The term “deregulation” is normally associated with the right, but there’s a long tradition of progressive deregulation in this country aimed at bolstering competition and forcing firms to be disciplined by each other rather than by captured regulators. Ted Kennedy, for example, played a key role in bringing price competition to air travel and trucking. And via Tim Fernholz, here’s a proposal in that spirit from Lawrence Wright at the Roosevelt Institute to unravel the regulatory cartel that keeps the ratings agencies in business no matter how badly they screw up.

Goners - Until last week, I'd never heard of "IBGYBG." But during the Senate Permanent Subcommittee on Investigations' eye-opening hearings into ratings agency malfeasance, former Moody's senior credit officer Richard Michalek introduced me to it while testifying about the perverse incentives that dominated the industry. On the investment bank side, he said, bankers were looking to score the one-time fee from whatever securitization deal they were asking the agency to rate, and move on to the next deal. The incentives for the bank, Michalek said in prepared testimony, were clear: "get the deal closed, and if there's a problem later on, it was just another case of IBGYBG--I'll be gone, you'll be gone."

Out of the Black Hole - This crisis was caused in large part by the opaque and unregulated over-the-counter (OTC) derivatives, or "swaps," market, which was then estimated to have a value of almost $600 trillion, or 10 times the world's gross domestic product. Approximately one-tenth of the unregulated OTC market was made up of the now-infamous credit-default swaps, a product that Wall Street sold to "insure" sub-prime mortgage investments but which lacked regulation and, therefore, the capital required to support these "guarantees." When sub-prime investments failed, the "insurance" payments were triggered. Only the multitrillion-dollar U.S. taxpayer interventions to save Wall Street prevented a worldwide depression.

The Corporate Derivatives Slander? Or The Big Derivative Secret? - Today, in the Financial Times,George Soros repeats a claim that I have been hearing a lot lately, The five big banks which serve as marketmakers and account for over 95 per cent of the US's outstanding over-the-counter transactions are likely to oppose it because it would hit their profits. It is more puzzling that some multinational corporations are also opposed. The only explanation is that tailor-made derivatives can facilitate tax avoidance and manipulation of earnings. In recent weeks, the Wall Street Journal has reported on big banks use of the repo market to hide its debts whenever they need to report to investors. Could it be that large non-financial corporations want to keep the derivatives market in the dark because they use derivatives to deceive investors or the IRS? And if so, who is doing this?

Warren Buffett Fails To Get Derivatives Loophole - Just because you're one of the world's best-known billionaires and close to President Barack Obama's White House doesn't mean you always get your way. At least, that's what appears to be the case from a Wall Street Journal story. WSJ.com reports that Warren Buffett's Berkshire Hathaway was seeking legislative language in the financial derivatives regulation bill produced by the Senate Agriculture Committee that would've kept the company from needing to put up more money as collateral for billions of dollars in derivative positions the company has. But the provision Berkshire lusted after was removed

Potential Derivative Loophole #1: Trading Facility - It’s Friday, so for fun let’s play financial reform loophole detective. Here’s the definition of a “swap execution facility” in Senator Lincoln’s original bill (p. 47): This language was passed out of the Ag Committee. Here is the Ag Committee’s language merged into the Dodd Bill that will be debated next week (p. 773-774). Can you find a difference? The word “trading” has been removed from the Dodd Bill. Specifically, a swap execution facility no longer means a “trading facility” but just a “facility.” I thought this might not mean much, until I just saw this Bloomberg report from Matthew Leising that this might in fact be a big deal: A one-word deletion in the 1,565- page Senate financial reform bill may help banks and inter- dealer brokers maintain how they trade swaps in the unregulated $605 trillion over-the-counter derivatives market…. The latest version deletes the word “trading” from the term “trading facility,” according to a copy of the revised bill obtained by Bloomberg News.

Clinton on Derivatives: ‘Too Much Has No Economic Purpose’ - WSJ - Former President Bill Clinton said he’s not certain Goldman Sachs broke the law in setting up the deal that drew civil fraud charges from the SEC, but he questioned the merit of financial firms' deals that amount to bets on things they don't own. “I think too much of this stuff has no economic purpose,” Clinton said at a financial summit, referring to the use of derivatives. He did say that derivatives for farmers and agriculture companies to hedge bets on their own crops is a different matter.Clinton said use of derivatives is part of a broader problem in the economy. “Too much of our growth in the last decade was in finance,” he said.

The silver lining to synthetic CDOs - One of the more thought-provoking bits of the Shleifer paper on financial innovation is this part of the model: Optimism about the profitability of the new claim at t = 0 encourages the intermediary to over-invest in an unproductive activity, eventually triggering a loss… Investment in A occurs only if new securities can be engineered, so financial innovation bears sole responsibility for unproductive investment. It can be argued that the expansion in the supply of housing in the last decade was an example of such inefficient investment needed to meet the growing demand for securitization of mortgages. To put it another way, it was the excessive and irrational demand for collateralized debt obligations which caused all those Miami condos and Phoenix tract homes to be built in the first place. That makes sense to me, but it raises an interesting question about the damage caused by synthetic CDOs. Here’s Jesse Eisinger and Jake Bernstein, from their investigation of Magnetar:

Any Regulation of Risk Increases Risk - That is the contentious title of a new paper from Philip Z. Maymin and Zakhar G. Maymin, which is significantly less contentious than their abstract: We show that any objective risk measurement algorithm mandated by central banks for regulated financial entities will result in more risk being taken on by those financial entities than would otherwise be the case… This result leaves three directions for the future of financial regulation: continue regulating by enforcing risk measurement algorithms at the cost of occasional severe crises, regulate more severely and subjectively by fully nationalizing all financial entities, or abolish all central banking regulations including deposit insurance..

Financial innovation: Give me a number | The Economist - FELIX SALMON interviews Glenn Yago: Felix Salmon and Glenn Yago on financial innovation from Felix Salmon on Vimeo. It's an interesting little conversation, but I continue to be frustrated by the lack of empirical specificity among innovation defenders. Yes, it's easy to come up with ways that innovation might generate benefits, just as it's easy to point out the very real economic damage done by crises associated with innovation. What's missing is any real empirical evidence that there are net benefits to a free-wheeling, innocent until proven guilty approach to financial innovation.

SAFE Banking Act, What it Does in 2D - Let’s talk about the SAFE Banking Act. First up, what does it do? Well, it caps deposits at 10% of total deposits, non-deposit liabilities at 2% of GDP for banks and 3% of GDP for non-banks. Huh? Let’s put it on a 2d graph: Banks take in money, and lend out money. The riskier the money they take in, the more likely it is you’ll have a bank run. On the y-axis we have the amount of deposits a firm has. Because of FDIC insurance and the federal reserve window, deposits are fairly sticky, even in a crisis (have you worried about a bank run?). This bill would reinforce that one bank can’t have more than 10% of the total deposit base, which is around $800 billion. But what about non-deposits? What about liabilities like obligations in the repo market and other shadow deposits, liabilities very subject to shadow bank runs? That will be on our x-axis. The SAFE Banking Act would limit this to 2% of GDP for banks, and 3% of GDP for non-banks. Right now that is about $280 billion, and $420 billion respectively.

Too Big for Us to Fail - Financial regulatory reform was on few people's minds when Barack Obama launched his presidential campaign in February 2007. But with the near collapse of the global financial system in 2008, leading to high unemployment and high government deficits for years to come, it became frighteningly obvious that something had to change. However, in one respect -- the politics of financial reform -- nothing has changed. We agree with many of its proposals, including a strong Consumer Financial Protection Agency, dedicated oversight of systemic risk, and new requirements to move derivatives onto exchanges and central clearinghouses. At the same time, we do not think the administration has gone far enough to curb the behavior of "too big to fail" institutions and mitigate the risk that they pose to the financial system and the economy. But these reasonable debates over how the regulatory system should be overhauled are peripheral to a more fundamental issue: the political power of the financial sector, which determines how the regulatory system will be overhauled, if at all.

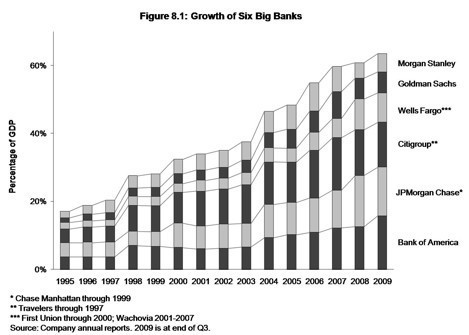

Relying on the Big Banks to Save the Economy - It is irritating but not especially surprising when Goldman Sachs CEO Lloyd Blankfein says things like "they are doing God's work", or claims that attacking Goldman is "hurting America." I'm sure people like him really believe they are good people just doing their best to help the world economy, in the same way Ayn Rand really believed that selfishness is a virtue and the Gordon Gecko character in Wall Street really believed that greed was good. What is disturbing is when Obama administration officials believe it too -- or at least believe that these massive mega-banks (the top six controlling assets equal to 63% of our nation's GDP) are needed to keep our economy going...Summers quote: "that was the approach America took to banking before the depression. That was the approach America took to lending in the thrift sector, before we had the S&L crisis. Most observers who study this believe that to try to break banks up into a lot of little pieces would hurt our ability to serve large companies, and hurt the competitiveness of the United States. But that's not the important issue, they believe that it would actually make us less stable."

Why Does Larry Summers Like Big Banks So Much? - The internets are buzzing with the news that Larry Summers told PBS Newshour that breaking up the banks is a bad idea. It's not clear to me that the core of his argument is actually wrong--100,000 small banks going hog wild on subprime mortgages would not have been obviously better than 100 big ones. Indeed, it would have been . . . the savings and loan crisis. However, when the time came to bail out those behemoths, regulators did not go into a lengthy disquisition on the mystery of capital flows, and asset-price bubbles. They said the institutions they were bailing out were "Too big to fail" without explaining that the risk wouldn't necessarily have been any safer for the economy if it had been more evenly throughout the banking system.

Why Can’t Reform Apply to the Biggest Banks? - NYTimes - Too big to fail is alive and well, alas. Indeed, several aspects of the legislative proposals sanction and codify the special status conferred on institutions that are seen as systemically important. Instead of reducing the number of behemoth firms assigned this special status, the bills would encourage smaller companies to grow large and dangerous so that they, too, could have a seat at the bailout buffet. Here’s an example of this special treatment: Both bills would establish a specific process to resolve big-bank failures. Smaller institutions, by contrast, would be allowed to go bankrupt without a new resolution scheme. This special resolution system is not only unfair; it also sends a pernicious signal to the market about large and intertwined institutions. The message is this: Subject as they will be to a newly codified “resolution authority,” these institutions and their investors and lenders can expect to be rescued if they get into trouble.

Growth of the Six Big Banks (chart)

Maybe it's time to break up the banks - As the Senate takes up debate on financial industry overhaul, there is one issue above all others that is imperative to work out: how to deal with institutions that are Too Big To Fail. The reason the government stepped in with taxpayer money at firms like Citigroup and AIG is still alive and well. Our financial giants are so behemoth and interconnected that should one quickly go out of business, the entire system could be at risk.Unfortunately, as an increasing number of commentators are pointing out, the solution Congress is currently contemplating will likely do little to change that. This solution has a number of problems. The core one is that it doesn't actually address the fact that companies are too large and interconnected. It merely sketches out a process for dealing with any potential fall-out.

Provision would break up nine biggest banks.- Nine of the largest financial institutions including Bank of America Corp., Citigroup Inc. and J.P. Morgan Chase & Co. would have to scale down by about 40%, according to legislation introduced by a group of eight Democrats on Thursday. The group is hoping the measure will be approved as part of sweeping bank reform legislation under consideration on Capitol Hill. The measure limits the size of non-deposit liabilities at financial institutions to 2% of U.S. gross domestic product, or about $300 billion. It's unclear whether congressional leaders will allow the measure to be voted upon by the full Senate or whether lawmakers would approve it.

US banks pouring millions into bid to kill Barack Obama’s finance reform bill - In the face of deep public anger over the financial crisis and government bailouts, banks have flooded Congress with lobbyists seeking to curtail key parts of the sweeping regulatory bill – such as provisions to create an office for consumer protection and more strongly regulate the vast derivatives market.JP Morgan Chase is at the forefront of lobby spending with $1.5m (£980,000) in the first quarter of this year alone – a sharp rise on the same period in 2009 – followed closely by Citigroup. Credit Suisse and Goldman Sachs have also spent more than $1m on lobbying Congress this year, more than double their previous spending. The banking industry is second only to healthcare interests in the amount it spends on political lobbying. Last year, America's eight leading banks and finance houses spent $30m to influence legislation. The broader financial industry has more than 2,600 lobbyists registered with Congress.

Swiftboating Finance Reform - Robert Reich Republicans are blocking a Senate vote on the Dodd bill, seeking to build public support by misleading the public. They’re claiming to want a stronger bill when in fact they’re doing the Street’s bidding by seeking a weaker one. Evidence of their tactics comes in the form of a shady anti-financial reform group called “Stop Too Big To Fail” which today announced a new TV advertising push in three key states. The ad features an out-of-context quote from me to bolster its case to kill financial reform.As TPMmuckraker has reported, Stop Too Big To Fail is the project of a veteran astroturf operation called Consumers for Competitive Choice, and it’s using the services of an ad agency that worked with the Swift Boat Vets For Truth in 2004. TPMmuckraker says the group has already spent $1.6 million on anti-reform ads and won’t say who’s funding the group’s efforts. “Stop Too Big To Fail” has previously featured MIT economist Simon Johnson in one of its media conference calls before Johnson realized the goals of the outfit and demanded it stop using his name. Now, “Stop Too Big To Fail” is using me. I demand it stop using my name