Fed Assets Fall to $2.3 Trillion as Mortgage Debt Declines -The Federal Reserve’s total assets fell 0.4 percent to $2.3 trillion during the past week on a decline in its holdings of mortgage-backed securities and federal agency debt. The central bank’s balance sheet decreased by $9.75 billion in the week ended yesterday, according to a weekly release today. The Fed’s holdings of mortgage-backed securities declined by $10.9 billion to $1.09 trillion, while its federal agency securities shrank by $1.98 billion to $154.5 billion. The Fed said last month that as housing debt matures it will purchase new Treasury securities to maintain its total securities holdings at $2.05 trillion. The central bank has purchased $22.9 billion of Treasuries since it began the program on Aug. 17. The Fed’s holdings of Treasury securities increased by $4.75 billion to $794.6 billion in the past week. M2 money supply rose by $11.1 billion in the week ended Aug. 23, the Fed said. That left M2 growing at an annual rate of 2.3 percent for the past 52 weeks, below the target of 5 percent the Fed once set for maximum growth. The Fed no longer has a formal target.

FRB: H.4.1 Release--Factors Affecting Reserve Balances--September 16, 2010 ..

Foreign central bank US debt holdings fall - Fed (Reuters) - Foreign central banks' holdings of U.S. Treasuries and agency securities at the Federal Reserve fell in the latest week, data from the U.S. central bank showed on Thursday. The Fed said its holdings of Treasury and agency debt kept for overseas central banks fell $17.81 billion in the week ended Sept. 15, to stand at $3.196 trillion. The breakdown of custody holdings showed overseas central banks' holdings of Treasury debt rose, however, by $39.63 billion to stand at $2.444 trillion. The foreign institutions' holdings of securities issued or guaranteed by the biggest U.S. mortgage financing agencies, including Fannie Mae (FNMA.OB) and Freddie Mac (FMCC.OB), plunged by $57.44 billion to stand at $752.52 billion. Overseas central banks, particularly those in Asia, have been huge buyers of U.S. debt in recent years, and own over a quarter of marketable Treasuries. China and Japan are the biggest two holders of Treasuries.

NY Fed to Buy $27 Billion in Treasurys Over Next Four Weeks - The Federal Reserve Bank of New York announced Monday that it would buy $27 billion in Treasurys in nine separate operations. The purchases come as the Fed reinvests proceeds from its mortgage holdings into government bonds, as part of a recent decision to keep steady its over $2 trillion portfolio size. (w/ maturation date table)

Why the Federal Reserve MUST Print, Print, Print - The law of unintended consequences continues to wreak havoc with the Fed’s ad-hoc dart throwing exercises plans, as only yesterday, the New York Fed confirmed our expectations that it will have to ramp up its Treasury purchases by 50% over the next month to the tune of $27 billion (our estimate: $25.5 billion)–all, to keep up with the Jones’ refis, defaults and loan mods. It’s easy to lose sight of just how this latest round of so-called QE Lite came to be. And, as this is but a hint of future printing, upon which a hand-bound Fed will find itself with no choice but to embark, a brief recap is appropriate.

Goldman: Fed May Announce New Asset Buys in November - The U.S. Federal Reserve could announce a new program of asset purchases to support a weak economy as early as November, according to Goldman Sachs Group Inc.“We don’t expect this at the Sept. 21 meeting, but in November or December there’s certainly a possibility that it will be announced,” Jan Hatzius, chief economist at the bank, said Tuesday. He added the Fed is likely to buy U.S. Treasurys worth around $1.0 trillion to kick-start the economy.

Richmond Fed’s Lacker Wants High Threshold For More Fed Action - Jeffrey Lacker, president of the Federal Reserve Bank of Richmond, sees modest growth in 2011, little change in inflation and little to spur the Fed to take new actions to support the economy. “The economy is facing very real impediments to growth and there is little monetary policy can do about that,” Mr. Lacker said in an interview with The Wall Street Journal late last week. “So I think our expectations for real growth and for the rate at which unemployment comes down ought to be very modest right now.” Fed officials will consider at their next policy meeting on Sept. 21 whether they should do more to spur growth, in particular by purchasing government or mortgage bonds to drive down long-term interest rates. Mr. Lacker set a high threshold for further action by the Fed, saying the central bank should only do more if it was looking at a real threat of consumer price deflation, something he doesn’t see.

Fed Watch: The Fair - A man takes his son to the county fair; the lights and sounds of the amusement rides are like a magnet to the boy. The boy, however, is penniless. His father, seeing the longing in his son's eyes, hands the boy a dollar for the rides, but quizzically adds "if it looks like you are about to have any fun with that dollar, I will take it back from you." The boy is puzzled. First, a dollar only buys three tickets, and the least expensive ride is four tickets. They are soon joined by the boy's grandfather, who, assessing the situation, says that the father should never have given the son a dollar in the first place. "He will just buy candy, which will cost you more later when you have to take him to the doctor to treat diabetes." The father neither agrees or disagrees. Along comes a trusted uncle, who says to give the boy another dime, but " then if he looks like he will have any fun, take back a quarter." The grandfather and uncle start bickering, loudly, in public, about what to do with the boy and his dollar. Soon another uncle rushes into the fray, proclaiming it is pointless to give the boy a dollar because all the workers are already busy helping other fairgoers. "He can't buy anything anyway, and if he tries, he will just drive up prices for all his cousins." The lights and noise of the fair fade as lines dwindle and the rides grow silent.

Monetary Policy Issues - A key policy question facing us is: Should the Fed, based either on concerns about the inflation rate, the level of real aggregate economic activity, or both, engage in a more accommodating policy? If the answer to that question is yes, the next question is: Does such a policy exist and, if so, what is it? Two days ago, the Wall Street Journal published a "symposium," titled "What Should the Federal Reserve Do Next," with short pieces by John Taylor, Richard Fisher (Dallas Fed President), Frederic Mishkin, Ronald McKinnon, Vincent Reinhart, and Allan Meltzer. The WSJ picked a group of conservative economists with a considerable amount of accumulated policy experience among them, and including one sitting Federal Reserve Bank President (Fisher). One would think we could get something useful out of these guys. Well, apparently not. Let's start with the low point. Fisher should win the bad analogy contest with this: One might assume that with more than $1 trillion in excess bank reserves and significant amounts of cash held by businesses, the gas tank of those who have the capacity to hire is reasonably full.

Should the Fed try to depress long-term yields further? - If the Fed were to buy a large enough volume of long-term debt, it might be able to reduce the net risk exposure of the private sector so as to change slightly that average compensation and flatten the slope of the yield curve. Whether that's indeed possible, and how big a change in rates we might expect to see, is an empirical question. What Cynthia and I found, based on what was observed on average over 1990-2007 in response to modest changes in the maturity composition of publicly held Treasury debt, is that replacing $400 billion in outstanding long-term Treasury debt with short-term debt might lower the 10-year yield by 14 basis points. Our estimates also imply that, in the current environment when short-term rates are essentially zero, if the Fed were to buy about $400 billion in long-term Treasury debt outright with reserves newly created for that purpose, it might still be able to reduce the 10-year yield by about 14 basis points.

Central bankers and banking supervision: Does independence matter? - In response to the global crisis, many countries are implementing – or at least considering – reforms concerning the role of the central bank in banking supervisory regimes. The global crisis has led policymakers in the EU and the US to broaden their central banks' mandates to include greater banking supervision. This column argues that this new responsibility should be seen as an evolution of the central bank specialisation as a monetary agent rather than a reversal of the specialisation trend.

Fed Awaits New Governors and San Francisco President - Even though Janet Yellen, the current president of the Federal Reserve Bank of San Francisco, is still awaiting Senate confirmation for a seat on the Fed’s Board of Governors, the search for a new president in San Francisco is well underway. Under the changes to the selection process made by the new financial-regulatory law, the choice will be made by six of the nine San Francisco Fed directors – the ones who aren’t commercial bankers – subject to the approval of the Fed Board in Washington. Among the candidates for the San Francisco post are Christina Romer, who has just left her post as chair of the White House Council of Economic Advisers to return to a teaching post at the University of California at Berkeley and John C. Williams, currently research director at the San Francisco Fed.

Help wanted - TWO weeks ago, a Leader warned that with governments bogging down under the weight of debt and political wrangling, central banks might begin to feel as though they are the last defence against deflation and double dips, and therefore try to achieve more than can reasonably be expected of them. When politics fails, one might say, it falls to the politically independent to save the day. President Obama nominated three new governors in April and they were each handily approved by the Senate Banking Committee over the summer, but the Senate has not held confirmation votes, and doesn't appear poised to anytime soon. That's the Washington Post's Neil Irwin. He continues: There is now a strange situation in that the institution in charge of guiding the U.S. economy has only one PhD economist among its top officials, Chairman Ben S. Bernanke. The other three currently serving governors are not monetary policy specialists (they are Tarullo, a former law professor, Duke, a former banker, and Kevin Warsh, a financial markets expert). Two of Obama's nominees are economists, San Francisco Fed president Janet Yellen and MIT professor Peter Diamond. This is, as it happens, a pretty terrible time for the Fed not to have as many smart economists in its upper ranks as possible; the central bank faces a massively consequential decision over the coming months of whether to undertake new steps to try to boost the economy.

A Scary Thought - Here's a scary thought: Let's say the European sovereign debt crisis flares up again, and one or two Euro banks fail. (Not a bank like UBS or Deutsche Bank, but a medium-sized bank like Bank of Greece or a Landesbank.) That, in turn, causes a U.S. money market fund — many of which have large exposures to Euro banks — to "break the buck," which leads to another run on money market funds. The Fed would be powerless to help. The Fed's emergency lending authority (the famed Section 13(3)) requires that any emergency lending facility to non-banks be approved "by the affirmative vote of not less than five members" of the Fed Board of Governors. Currently, there are only four members of the Fed board: Bernanke, Warsh, Elizabeth Duke, and Dan Tarullo. Donald Kohn retired earlier this month, and the Senate has yet to vote on Obama's three nominees (Janet Yellen, Peter Diamond, and Sarah Bloom Raskin).

High Cost of Fed Vacancies - I’ve been harping on the vacancies on the Federal Reserve Board of Governors for a while now primarily because I think they’re contributing to tight money that’s stifling economic growth. But Economics of Contempt raises a different issue, namely that given the current vacancies it’s actually illegal for the Fed to use its Section 13(3) authority to engage in emergency lending to non-bank entities. The creation of any such facilities requires “the affirmative vote of not less than five members” of the Board of Governors and right now there are only four, plus the three vacancies. Why does this matter? Well it matters because in the not-so-distant past such emergency lending was used to prevent economy-paralyzing runs in the money market world. Such runs aren’t likely to recur, but as EOC observes one could imagine something like this happening if European sovereign debt problems recur and break a mid-sized European bank or two. It would be a disaster for the Fed to not intervene simply because Richard Shelby is being a pain in the ass and won’t bring Obama’s nominees up for a vote.

Be prepared - IN THE last couple of weeks, a European banking and financial crisis that seemed to have been extinguished before it could lead to conflagration seemed to be sending out new and ominous smoke signals. Yields on the debt of troubled governments crawled upwards, and the Irish government found itself forced to craft new policy reponses to address a lack of faith in the banking system. What if this deterioration were to continue, leading ultimately to a big bank failure or two and a new financial panic? The Fed would be powerless to help. The Fed's emergency lending authority (the famed Section 13(3)) requires that any emergency lending facility to non-banks be approved "by the affirmative vote of not less than five members" of the Fed Board of Governors. Currently, there are only four members of the Fed board. That's from Economics of Contempt. This is inexcusable. Of course, it's also inexcusable that three members would be sidelined by Congress while the Fed weighs significant action to address the fact that the economy is consistently missing its targets.

White House Renominates Peter Diamond to Fed Board - President Barack Obama on Monday nominated Massachusetts Institute of Technology economist Peter Diamond to the Federal Reserve board, according to a White House press release. Diamond, an expert on social security, pensions and taxation, was previously nominated for the board but has come under scrutiny from Republicans who say he isn’t adequately qualified.

Dodd: Limited Will for Senate Vote on Fed Nominees - U.S. Sen. Christopher Dodd (D., Conn.) said Tuesday he didn’t know how much appetite there was among senators to vote on three nominees to the Federal Reserve’s Board of Governors before the November election, including that of the nominee for the vice chairman of the Fed. Dodd, the chairman of the Senate Banking Committee that has jurisdiction over Federal Reserve nominees, said there was limited time before lawmakers break until November. He said the issue of whether to bring the nominations up for a debate and vote hadn’t been discussed when Senate Democrats met Tuesday afternoon to discuss strategy. “We’ve got a limited amount of time here, I don’t know if there’s going to be any appetite to deal with these Fed nominees,” Dodd said.

Recess Appointments for the Fed? - One journalist who doesn’t underrate the importance of Federal Reserve decision-making is Neil Irwin who reports today on how the prospect of additional monetary stimulus is “likely to be the focus of a vigorous debate at a Fed policy meeting next week, setting the stage for a definitive decision in November or December on whether to purchase hundreds of billions of dollars of bonds in an effort to strengthen the economy.” But who will attend the meeting? As Robin Harding reviews, not Barack Obama’s appointees whose presence would be valuable. On the one hand, their votes would count and “more important than their votes is having their voices at the FOMC to counterbalance more hawkish regional Fed presidents.” This is especially important since Donald Kohn—who, as she observes, is one of the few actual monetary policy specialists on the board—has already stepped down. Brad DeLong suggests it’s time for recess appointments. If so, I’d like to throw my own hat in the ring, since I think tapping some random blogger is likely to raise short-term inflation expectations and currency depreciation all on its own. Realistically, I think it’s hard to imagine the White House going from zero to sixty on this

The Recognition Window - Hussman -One of the things I'm increasingly dismayed to learn is that no matter how much detail, data, and qualification I might include in these commentaries, my conclusions will often be summed up by writers or bloggers in a single sentence that often bears no relation to my point. For instance, my view that quantitative easing will trigger a "jump depreciation" in the dollar has evidently placed me among analysts warning of hyperinflation and Treasury default (a club whose card is nowhere in my wallet). To clarify once again - I emphatically do not anticipate inflationary pressures until the second half of this decade. As I've repeatedly emphasized, the primary driver of inflation - historically and across countries - has been growth in government spending for purposes that do not expand the productive capacity of the economy. Quantitative easing does not pressure the dollar by fueling inflation. It has a much more subtle effect...

The Deflation vs. Hyperinflation Debate On Steroids, Or Mish vs Gonzalo Lira In The Octagon - A recent guest post by Gonzalo Lira on Zero Hedge, providing a theoretical framework for the arrival of hyperinflation, went viral, generating over 75k views and over 1,000 comments, further confirming that the biggest and most confounding debate in all of finance is what will the final outcome of the Fed's market manipulative actions be: deflation, inflation or, and not really comparable, hyperinflation (which is a distinctly different phenomenon from either of the above). The post infuriated some hard core deflationists who continue to refuse to acknowledge the possibility that in its attempt to inspire inflation at all costs, the Fed may just push beyond the tipping point of monetary imprudence away from mere target 2-3% inflation, and create an outright debasement of the world's reserve currency. One among these was none other than Mish himself, who a week ago recorded a podcast on Global Edge with Eric Townsend and Michael Hampton (link here), in which his conclusion was that Hyperinflation is the endgame, "so it is unlikely."

M2 Surges By $30 Billion In Past Week To Highest Ever, Even As Monetary Base Declines - Another week in which the M2 jumped to a fresh all time high, increasing by $30 billion W/W to just under $8.7 trillion. This was only the fourth largest weekly jump in this broad money aggregate in 2010, with the prior biggest ones clustered just around the time of the Greek "out of court" reorganization and the flash crash in May. This was also the 8th sequential increase in the M2 in a row. Oddly enough this occurred even as the Monetary Base (NSA) declined by $11 billion to $1.983 trillion. Currently, the M2-MB ratio stands at 4.4x, close to its all time lows, with the recent decline purely a function of the modest contraction in the Fed's balance sheet as MBS had been rolling off for the past 4 months. With QE Lite in play, expect the Fed's Balance sheet to remain flat, which will likely mean that the ratio of the Fed's asset to the Monetary Base will remain more or less unchanged at its elevated ratio of 1.15x (with a tendency toward declining), compared to the historical average of around 1.00. . Is the recent leakage in M2 higher, coupled with a contraction in MB the critical step that all the inflationists have been dreading (yet at the same time expecting)?

The inflation picture - THE Federal Open Market Committee will meet next week to discuss new policy moves. The developing conventional wisdom seems to be that the FOMC will announce new asset purchases, but will not do it this month. But as Mr Bernanke made clear in his August speech, one of the key factors shaping the policy response will be the behaviour of inflation: [T]he FOMC will strongly resist deviations from price stability in the downward direction.. It is worthwhile to note that, if deflation risks were to increase, the benefit-cost tradeoffs of some of our policy tools could become significantly more favorable. So, what have we observed on this front in the month since Mr Bernanke made that comment? Economic data, broadly speaking, has improved just a bit. Has this been reflected in inflation? The Cleveland Fed has analysed the latest data from the Bureau of Labour Statistics and put together some handy charts. Here is trimmed mean CPI through August:

Hyperinflation Special Report -The U.S. economic and systemic solvency crises of the last two years are just precursors to a Great Collapse: a hyperinflationary great depression. Such will reflect a complete collapse in the purchasing power of the U.S. dollar, a collapse in the normal stream of U.S. commercial and economic activity, a collapse in the U.S. financial system as we know it, and a likely realignment of the U.S. political environment. The current U.S. financial markets, financial system and economy remain highly unstable and vulnerable to unexpected shocks. The Federal Reserve is dedicated to preventing deflation, to debasing the U.S. dollar. The results of those efforts are being seen in tentative selling pressures against the U.S. currency and in the rallying price of gold.

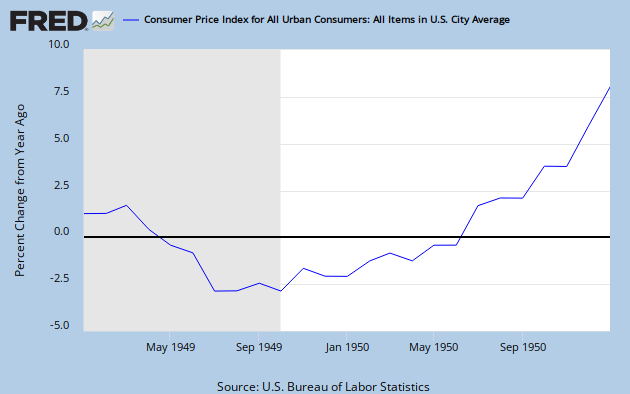

2010, a Year of No Inflation - The lack of inflation this year is a story that deserves more attention than it has received. Over the last two years, inflation has been zero. Over the last year, it has been just 1.3 percent. Over the last six months, it has been below zero — negative 0.7 percent. Since the Labor Department started keeping records in 1947, there have been only six six-month periods when prices have fallen more than that. All of them were in 1950, an unusual time when prices were falling even though the economy was growing.This year’s price declines are clearly a reflection of the economy’s weakness. And yet the Federal Reserve has continued toresist taking aggressive action to lift growth. Remember, the Fed has a dual mission: keep inflation contained and maximize employment. By any measure, inflation is contained, and the economy is millions of job shy of maximum employment. Yet the Fed has taken only minor actions to lift growth and says it stands ready to take more action.

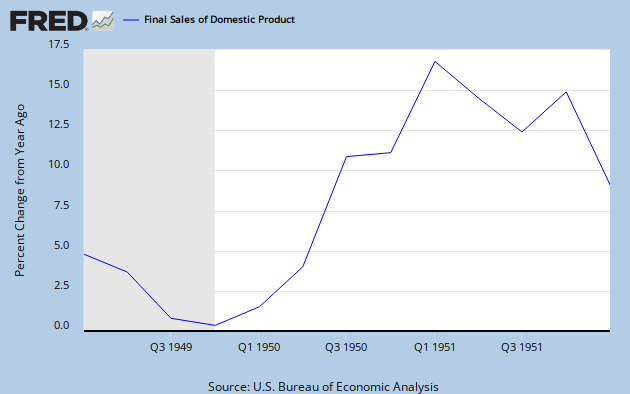

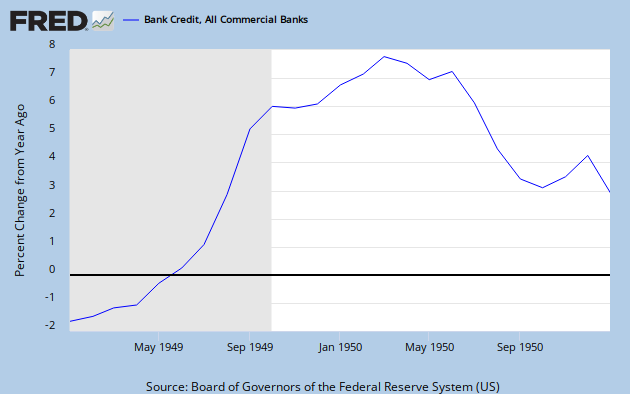

How Can It Be? - Everyone knows that deflation is a horrible thing: the price level declines, profits fall, employment drops, real debt burdens increase, households in turn spend less, prices fall again, and the cycle repeats. Folks like Paul Krugman, Greg Ip, and Barry Ritholtz have been reminding us of these dangers as there seems to be a greater chance that deflation could reemerge soon. David Leonhardt weighs in on this issue and notes that the sustained lack of inflation in the last two years is unprecedented in the postwar period, except for that "unusual" 1950s period: Since the Labor Department started keeping records in 1947, there have been only six six-month periods when prices have fallen more than [the past six months]. All of them were in 1950, an unusual time when prices were falling even though the economy was growing. Gasp. How can it be? Deflation and a growing economy? There must be some mistake because observers like Paul, Greg, and Barry have told us this is impossible. Surely, Leonhardt misread the data. So what the does the data actually show? Let's see, the Fred database shows....gasp. It worse than Leonhardt reports. Looking at the year 1950--the first of these unusual six periods--one finds not only deflation but also solid growth in aggregate demand, corporate profits, employment, and financial intermediation. Oh my, how can this be? Maybe our high priest of central banking, Ben Bernanke, can shed some light on this mystery:

Myths About "What's Economically Important" - Day in and day out I hear it from readers who insist that we are not in deflation and will not be in deflation because prices are rising and continue to rise. Expanding credit (inflation) created an enormous housing bubble, a commercial real estate boom, a rising stock market, and an enormous number of jobs. Contracting credit (deflation), burst the housing bubble, burst the commercial real estate bubble, burst the stock market bubble, resulting in millions of foreclosures and bankruptcies, millions of broken homes, millions on food stamps, 26.2 million unemployed or partially employed, and countless additional millions who are underemployed. In a fiat credit-based economy, where credit dwarfs money supply, changes in credit is what's important, not changes in money supply, not nominal changes in prices.

US CPI August 2010 and real interest rates - These charts are important: <> Commentators I have read seem a little concerned that yearly inflation (chart 2) is still too low for comfort, but the first graph (chart 1) clearly shows that prices for July and August have increased significantly after a three month deflationary period through April to June. The July and August price changes actually represent annualised inflation of 3.70% and 3.05% respectively and are the highest recorded since August 2009. I wouldn't be surprised if US GDP in Q3 was positive now, though there is still room for a decline in Q4. Download the CPI release here. My own charts:

HOW TO REVERSE A DEFLATION: HELICOPTER BEN NEEDS TO DROP SOME MONEY ON MAIN STREET - In 2002, in a speech that earned him the nickname “Helicopter Ben,” then-Fed Governor Bernanke famously said that the government could easily reverse a deflation, just by printing money and dropping it from helicopters. It seems logical enough. If there is insufficient money in the money supply (deflation), the solution is to put more money into it. But if deflation is so easy to fix, then why has the Fed’s massive attempts to date failed to do the job? Chairman Bernanke said he would fight deflation with his whole arsenal, including “quantitative easing” (QE) – purchasing longterm securities with money created on a computer. Yet since 2008, the Fed has added more than $1.2 trillion to “base money” doing just that, and the economy is still in a serious deflationary spiral. In the first quarter of this year, the money supply actually shrank at a record annual rate of 9.6%. Cullen Roche at The Pragmatic Capitalist has an answer to that puzzle. He says that as currently practiced, quantitative easing (QE) is not really a money drop. It is just an asset swap:

The Last Thing Government Will Do - Economist Steve Keen says that the major economies are entering a debt deflationary spiral. The way out of it would be to increase workers' wages which would allow them to pay off their debts and create inflation. But, economic policy makers don't understand this, and therefore, it will be the last thing they do.The entire show is called Global Debt Collapse Dean Baker points out that economists are always quick to blame workers for the economy being depressed rather than the bad judgments of the economic policy makers themselves.

Anticipating the End of a Weak Recovery - By most estimates, the statistical recovery which began in the second half of 2009 in the US has been weak. Many had been talking about a V-shaped recovery early this year. However, given the magnitude of the imbalances in the U.S. leading up to recession, the underperformance of this technical recovery is not surprising. Now, in April 2009 I said this would be a fake recovery even before it began. My issue was that the economy would be ‘ginned up by stimulus’ if you will but that we would get a supply side credit shock nonetheless. The systemic problems in the banking sector would still spell weak credit growth – even as banks recorded record profits. This seems to be what has occurred. And none of the systemic problems have gone away, not least the underwater second mortgages. The household sector is troubled by indebtedness, which created a demand side shock for credit. In 2008 and 2009, consumers were reducing their debt loads in a manner consistent with the fall in nominal GDP, meaning debt to GDP levels were not falling that much. However, household debt to GDP levels have continued to fall even as the economy has grown over the past year.

America's economy: Are we there yet? - The Economist - “WHITHER goest thou, America?” That question, posed by Jack Kerouac on behalf of the Beat generation half a century ago, is the biggest uncertainty hanging over the world economy. And it reflects the foremost worry for American voters, who go to the polls for the congressional mid-term elections on November 2nd with the country’s unemployment rate stubbornly stuck at nearly one in ten. They should prepare themselves for a long, hard ride. The most wrenching recession since the 1930s ended a year ago. But the recovery—none too powerful to begin with—slowed sharply earlier this year. GDP grew by a feeble 1.6% at an annual pace in the second quarter, and seems to have been stuck somewhere similar since. The housing market slumped after temporary tax incentives to buy a home expired. So few private jobs were being created that unemployment looked likelier to rise than fall. Fears grew over the summer that if this deceleration continued, America’s economy would slip back into recession.

EROI, Insidious Feedbacks, and the End of Economic Growth - The following is a brief portion of a paper of the same title that we wrote and that is currently under peer-review. I will be presenting on this topic at this year’s ASPO conference in Washington, D.C.- Numerous theories attempting to explain business cycles have been posited over the past century, each offering a unique explanation for the causes of--and solutions to--recessions, including: Keynesian Theory, the Monetarist Model, the Rational Expectations Model, Real Business Cycle Models, New (Neo-) Keynesian models, etc… Yet, for all the differences amongst these theories, they all share one implicit assumption: a return to a growing economy, i.e. growing GDP, is in fact possible. But if you believe as I do that the world is entering a unique period defined by flattening and then declining oil supplies, then for the first time in history we may be asked to grow the economy while simultaneously decreasing oil consumption, something that has yet to occur in the U.S. In this post I attempt to answer the following question: Is a return to long term economic growth possible?

When Giants Fall: 'America Is Moving "from the Jetsons to the Flintstones"' - Numerous studies have shown that humans don't do a particularly good when it comes to assessing their own capabilities. In fact, psychologists refer to this phenomenon as "illusory superiority," a cognitive bias that causes people to overestimate their positive qualities and abilities and to underestimate their negative qualities, relative to others," according to Wikipedia. That is one reason why those who are entrusted with ensuring that mission critical systems function as planned are vetted beforehand by someone other than themselves. It might also help explain why a Canadian publication, MacLean's, in an article entitled "Third World America," can paint a portrait of today's America that many Americans are unable (or unwilling) to see:

Investment Contributions to GDP: Leading and Lagging Sectors - The following graph shows the rolling 4 quarter contribution to GDP from residential investment, equipment and software, and nonresidential structures. This is important to follow because residential investment tends to lead the economy, equipment and software is generally coincident, and nonresidential structure investment trails the economy. For the following graph, red is residential, green is equipment and software, and blue is investment in non-residential structures. The usual pattern - both into and out of recessions is - red, green, blue. Residential Investment (RI) made a positive contribution to GDP in the Q2 2010, but RI will be a drag on GDP again in Q3. RI was positively impacted in Q2 by the housing tax credit in two ways: first, builders rushed to complete homes by the end of June, and, second, real estate agent commissions were boosted in Q2 and will decline sharply in Q3 (just look at existing home sales in July). Equipment and software investment has made a significant positive contribution to GDP for four straight quarters (it is coincident).

Hussman: Watch the lagging indicators - John Hussman is not buying the recent risk-on sentiment that has developed since September began. In Hussman’s view, recent jobs numbers point to further downside ahead.He says the normal impulse response to the large job destruction of 2008 and 2009 would be further job losses for a time. But we are well past the propagation point for those job losses. Rather, in a normal recovery, 460,000 to 500,000 jobs would be created. So, we are well short of this. Why? Clearly this has something to do with consumer deleveraging and/or industrial recalculation as labour shifts away from depressed sectors of the economy awaiting the pick up in new growth sectors. This is not a V-shaped recovery. And Hussman says we need to watch the lagging indicators to ascertain what sort of impulse response the fresh batch of employment weakness will have on the real economy. The ISM numbers should be of particular note not just here in the US but in Asia where there has been softness.

Update: Regional Fed Surveys and ISM - By request - now that the Empire State and Philly Fed manufacturing surveys for September have been released - here is an update to the graph I posted last month: For this graph I averaged the New York and Philly Fed surveys (dashed green, through September), and averaged five surveys including New York, Philly, Richmond, Dallas and Kansas City (blue, through August). The Institute for Supply Management (ISM) PMI (red) is through August (right axis). Last month, when the ISM survey came in slightly better than expected, I wrote: "Based on this graph, I'd expect either the Fed surveys to bounce back in September - or the ISM to decline." So far there has been little "bounce back" in the Fed surveys.

From zombie banks to zombie mortgages - Japan's recent demotion to world's third-largest economy, behind China, triggered two distinctly different feelings in the United States. One was Schadenfreude. At the end of the 1980s Japan was a contender for the No. 1 spot. It was the rich world's fastest growing big country. Its companies dominated electronics, steel, automobiles and even banking. Its political and business leaders were paragons of long-term strategic thinking, while budget and trade surpluses left it rich with cash. Meanwhile, the U.S. was on the brink of recession, its corporate managers obsessed with short-term profits and its politicians incapable of mustering a coherent industrial strategy.What happened next, of course, is history. Japanese property and stock prices cratered, its banking system seized up, and a decade (actually, two now) of economic stagnation followed. The second feeling Japan's misfortunes evoked is dread. The U.S. has gone through its own spectacular property crash and banking crisis and is now mired in a painfully weak recovery. Does it face a long period of stagnation as Japan did?

US debt surges, leaving nation with difficult choices ahead-- The federal debt almost doubled during the George W. Bush administration, and it has increased more than 25 percent during President Barack Obama's first two years in office. The more than $13 trillion the nation owes -- about $43,000 per person -- is casting a long shadow over this year's election, fueling the tea party movement for a smaller government and increasing voter anxiety about the future. Many congressional candidates are talking about the nation's shaky economy but are using it more to score political points than to explain the difficult choices ahead. Republicans assert the nation has a "spending crisis" and the debt should be brought under control by cutting spending, not raising taxes. But most Republicans are not specifying exactly what spending they would cut while reducing taxes. Democrats accuse Republicans of wanting to dismantle safety-net programs such as Social Security and Medicare, but most Democrats aren't saying how they would pay for the large projected growth in those programs.

The Economist: when should we start worrying about the deficit… I’m not of the school that screams for a balanced budget at all costs. There are times in the business cycle when deficit spending is quite appropriate. The government can borrow to help replace private spending when it collapses during a serious recession through increased infrastructure spending as well as expanded unemployment and welfare benefits. Many of the recent actions of the Treasury, the Federal Reserve and Congress were necessary in the face of the impending collapse of the international financial system in 2007 and 2008.But deficit spending – having appropriations exceed tax revenues – during economic booms is not appropriate. Our federal budget has been in deficit for 46 of the last 50 years. Through good times and bad, through the three longest expansions in our nation’s history, we have spent more than we collected in tax revenues, leaving it to later generations to worry about paying off the debt.

Don’t Worry About China, Japan Will Finance U.S. Debt - China has been diversifying its $2.5 trillion reserves away from the dollar, causing some to worry that less Chinese buying of Treasurys would cause U.S. interest rates to rise and make it more difficult for the government to borrow. But Japan’s dollar buying in currency markets Wednesday shows Chinese reserve diversification might actually lead to even more demand for Treasurys. As China diversifies out of U.S. dollar-denominated assets such as Treasurys, it is buying debt denominated in the currencies of some of its biggest trading partners. Not wanting to lose competitiveness themselves, those trading partners in turn buy dollars to keep their currencies cheap. As part of the diversification push, China has been a major buyer of yen, snapping up $27 billion in yen so far this year according to Japanese Ministry of Finance. Analysts say China’s buying has helped an already strong yen get stronger. Now, Japan, feeling under pressure to weaken its currency, turned around and bought dollars, most likely in the form of Treasurys.

The Real Conundrum: Why the Hell Do We Care if China Manipulates Its Currency in Our Favor? - Here's a little editing fun of Harold Meyerson's article in today's Washington Post: "This week, committees on both sides of Capitol Hill will plumb the conundrum of Chinese currency manipulation. The conundrum isn't that -- or why -- China is manipulating its currency: By undervaluing it, China is systematically able to underprice its exports, putting American (and other nations') manufacturing consumers and businesses that purchase China’ cheap imports at a significant disadvantage. The conundrum is why the hell the United States isn't doing thinks it should do anything about it. There are certainly plenty of senators and congressmen -- and Main Street Americans U.S. producers that compete with China -- who'd like to see the White House place some tariffs taxes on American consumers and businesses who purchase the underpriced low-priced Chinese imports. If the administration doesn't act, Congress may just consider mandating some tariffs punitive taxes against American consumers and business on its own."

Fed Watch: Yen Intervention - At the beginning of August, I wrote: suppose Japanese officials believe that intervention is required regardless of the G-20. Presumably, they will give US Treasury Secretary Timothy Geithner a phone call to at least keep him in the loop, if not to receive his implicit consent. One wonders if Geithner will recognize what he would be consenting to: Japanese intervention, if it occurs, means that Chinese authorities managed to get Japan to acquire their Dollar reserves for them. Instead of buying Dollars, China buys Yen, which in turn induce Japan to buy Dollars. This maintains the artificial capital flows to the US while allowing China to escape accusations of being a “currency manipulator.” Since then, Japan’s currency challenge only intensified, culminating in last week’s almost comical complaint from Japanese policymakers: Japan’s government said it will seek discussions with China over the nation’s record purchases of Japanese bonds as an appreciating yen threatens to undermine an economic recovery. Did policymakers recognize the irony of their situation? It is not exactly a secret that Japan has made frequents excursions into the currency markets. But apparently they feel that intervention should be limited to Dollar purchases. Surely another Asian nation wouldn’t play the same game on them?

Beggar, then sneakily enrich, thy neighbour - AMONG today's big news items is the word that Japan is now actively selling yen in order to improve its exchange rate against other major currencies. The yen has risen sharply in recent months, dealing a blow to Japanese exporters and slowing Japanese recovery. The move has led to some fretting that a period of competitive devaluation is nigh. Here's Tim Duy, for instance: There apparently is no motivation for global central banks to stop directing capital inflows at the US in an effort to support mercantilist objectives. If it isn’t China, it will be some other economy. And equally apparent, there is no motivation among US policymakers to address such government directed capital flows. Which will leave politicians falling back on ultimately harmful trade barriers. The absolute inability of US policymakers to seriously address a global financial architecture where a rule of the game is "when in doubt, by Dollars" will ultimately have serious consequences via disruptive adjustment when the system can no longer be maintained, via either external or internal forces.

Why Japan's yen policy is bad for the world - After threatening to intervene for weeks, Japan's economic policymakers finally jumped into the currency markets to depress the value of the surging yen. The intervention was Tokyo's first in six years, and had an immediate impact, softening the yen from under 83 to the dollar to around 85 by the afternoon. The Japanese have been freaking out over the strengthening yen, which hit another 15-year high this week against the dollar, fearing that it makes Japanese exports more expensive and less competitive on world markets, thus undermining Japan's already feeble recovery from the Great Recession. Finance Minister Yoshihiko Noda, explained the government's decision while confirming the intervention to reporters: Deflation is continuing, and we are in severe economic conditions. Under those circumstances, recent movements [in the yen] will have adverse effects on the stability of economic and financial conditions, and we can't overlook them. However, in my opinion, Tokyo's decision is bad, bad, bad – for Japan, and just about everyone else.

Bernanke Shadow of Easing Limits BOJ Success With Yen Weakness -- Bank of Japan Governor Masaaki Shirakawa’s success in weakening the yen may hinge on Ben S. Bernanke. Japan said two days ago it sold yen for the first time since 2004 because the currency’s surge to a 15-year high versus the dollar imperiled the nation’s export-led recovery. Meantime, pressure is growing on U.S. Federal Reserve Chairman Bernanke to print more dollars to bolster America’s flagging economy, a policy that contributed to a weaker greenback in 2009. “Because of speculation of further monetary easing by the Fed, it may be impossible for Japan alone to turn around the yen-appreciation trend” through unilateral currency intervention, said Hiroaki Muto, a senior economist at Sumitomo Mitsui Asset Management Co. in Tokyo. The firm is a unit of Japan’s third-largest banking group.

China should cut dollars if U.S. too loose: sovereign fund (Reuters) - China should sell dollars and diversify its foreign exchange reserves if the United States sticks to loose monetary policy, the head of the Chinese sovereign wealth fund said in an article published this week. Lou Jiwei, chairman of the $300 billion China Investment Corp, also offered policy advice to the United States, saying the best course of action would be for it to tighten monetary conditions while ramping up stimulus spending. He said the United States did not have much to gain from monetary easing, because little cash was entering the real economy and a large amount was leaving the country via dollar-funded carry trades. Under such conditions, the dollar would steadily depreciate, and Asian economies and oil exporters might lose faith in it as a global reserve currency, he said. "For China, the chief tools to reduce economic risks are to strengthen regulation of capital flows, control liquidity through cash management, monitor asset markets and divert foreign exchange reserves to non-dollar assets," Lou said.

$1.26T deficit on pace as second-highest on record - The federal government is on track to record the second-highest deficit of all time with one month left in the budget year. The deficit totaled $1.26 trillion through August, the Treasury Department said yesterday. That puts it on pace to total $1.3 trillion when the budget year ends Sept. 30, slightly below last year’s record $1.4 trillion deficit. The Obama administration contends the record deficits were necessary to combat the most serious economic crisis since the Great Depression. About one-third of the higher deficits are a result of a drop in government tax revenues. The other two-thirds of the deficit increases reflect higher government spending to stabilize the financial system and boost the economy. Deficits of $1 trillion in a single year had never happened until two years ago. The $1.4 trillion deficit in 2009 was more than three times the size of the previous record-holder, a $454.8 billion deficit recorded in 2008.

Citigroup Says No Developed Government Securities Are `Completely Safe' - Bonds issued by developed countries, including those with the highest credit ratings such as Germany and the U.S., are not “completely safe” as demand for public spending is growing faster than revenue, Citigroup Inc. said. Greece is the country most at risk of default, followed by Ireland, Portugal and Spain, the bank said. The U.S. may also face repayment challenges “at horizons longer than five years. We conclude that no sovereign debt can and should be considered completely safe,” London-based economists Willem Buiter and Ebrahim Rahbari wrote “We still consider it unlikely that there will be a sovereign default during the next five years by more than a couple of advanced economies.”

It's More Than The Deficit - By John Mauldin - We talked earlier about how increasing government debt crowds out the necessary savings for private investment, which is the real factor in increasing productivity. But there is another part of that equation, and that is the percentage of government spending in relationship to the overall economy. Let’s look at some recent analysis by Charles Gave of GaveKal Research. It seems that bigger government leads to slower growth. The chart below is for France, but the general principle holds across countries. It shows the ratio of the private sector to the public sector and relates it to growth. The correlation is high. (In the book we will show the same graph for other countries.)That is not to say that the best environment for growth is a 0% government. There is clearly a role for government, but government does cost and that takes money from the productive private sector.

The hypocrisy of most deficit discussions - Congress seems incapable of setting aside electioneering rhetoric and talking straight about taxes and deficits. The GOP claims that it thinks deficits are bad things while at the same time it proposes no spending cuts (except to important safety net programs) and does propose further tax cuts. Back in the old days of the Bush regime, the tax cutters tended to claim that tax cuts would create jobs and raise (not lower) government revenues. They didn't. The Bush administration had anemic job growth, certainly seeing no boost from the humongous tax cuts enacted in 2001, 2003, and 2004 (and smaller cuts throughout the term). And we have enough experience with tax cut programs from Reagan to Bush I to Bush II to see that revenues do not miraculously go up when the taxing provisions that are intended to raise revenues are cut back. Sometimes there are a few localized effects--such as increased selling of capital stocks to take advantage of a new and lower rate because it is expected that higher rates will have to be enacted later. But tax cuts cut revenues.

The Budgetary Impact of Fannie Mae and Freddie Mac - CBO Director's Blog - In September 2008, the federal government took control of Fannie Mae and Freddie Mac—two government sponsored enterprises (GSEs) that provide credit guarantees on more than half of the outstanding residential mortgages in the United States. Although they are not legally federal agencies, the government operates them to fulfill the public purpose of supporting the housing and mortgage markets. Therefore, CBO believes that it is appropriate to include the GSEs’ financial transactions in the federal budget. In its August 2010 baseline projections, CBO included an estimated $53 billion in costs for new mortgage guarantees that Fannie Mae and Freddie Mac will make over the 2011–2020 period. That estimate was made using a so-called “fair-value” basis of accounting, which differs from the way most federal credit programs are reflected in the budget. In a letter sent today to Congressman Barney Frank, CBO discusses that estimate and compares it with the budgetary impact that would be estimated using the procedures specified in the Federal Credit Reform Act of 1990

It's Demand, Stupid - Krugman - I’ve said this before, but Catherine Rampell has a very nice chart making the point: if you ask businesses — as opposed to their lobbyists — what their problem is, you find no hint of the stories the usual suspects are telling you about government interference, political uncertainty, etc.. Businesses aren’t hiring because of poor sales, period, end of story: And the best thing government could do to help business would be to spend more, increasing demand. The fact that it’s not going to happen doesn’t change the fact that it’s the simple truth.

Hey Boomers: Leave a Big Bequest—to the Government -This post is part of our forum on Baby Boomers and what they owe the country. Follow the debate here. I am sympathetic to Michael Kinsley's argument that Baby Boomers like ourselves should leave something more than debts behind to the next generation, even if, as he correctly points out, much of the debt was really left to us by entitlement programs that have benefited the so-called Greatest Generation far more than subsequent generations. Basically, the Greatest Generation paid almost nothing in terms of payroll taxes and got benefits that were vastly greater than their contributions; later generations will be lucky to get back what they put in.The critical point, I think, is that the Boomers also inherited some of the Greatest Generation's sense of entitlement without having paid the dues of going through the Great Depression and World War II that may have justified it. And as Kinsley notes, it's really too late for Boomers to shoulder similar burdens even if the opportunity suddenly presented itself.

Believe It Or Not, There's Serious Talk About A Government Shutdown In 2011 - Even though the common wisdom is that the two government shutdowns in 1995 and 1996 were unmitigated political disasters for congressional Republicans, there is serious increasing talk about it being a prime strategy next year if the GOP is in the majority in the House and Senate. Former House Speaker Newt Gingrich, who was one of the architects of the failed shut-the-government strategy back in the 1990s, raised the idea back in April in connection with health care. Rep. Lynn Westmoreland (R-GA), a vice chairman of the National Republican Congressional Committee, spoke about it publicly last week. I'll have much more to say about this on Tuesday when my Roll Call column is published. For now, just a few vignettes from the last time the GOP thought that closing the government was a good way to win the hearts and minds of voters and force the president to do its bidding.

How would a government shutdown work? - Because I don't get it. The U.S. government operates on a Fiscal Year basis meaning that next year starts on Sept 30th. Which means, far as I know that government operations, including implementation of HCR, are funded right through the next Sept 30th (because I don't think there are important Appropriations bills hanging, nor would R's have control prior). And while I don't see any Constitutional bar to a new Republican majority passing legislation to actively stop some government spending simple inaction wouldn't seem to have any effect. And there would not seem to be enough of a political opening to push anything through in light of the ability of a Democratic Senate filibuster (not that I think the Dems will lose the Senate) or a Presidential veto to block action. From Republican rhetoric you would think they have the option to change the name plates on the Office of the Speaker one day and then turn out the lights of DC the next. But from where I sit and from what I know it just doesn't work that way. Are these guys just blowing smoke? Or just inhaling deeply on some really great ganja? As I said I don't get this at all. The politics maybe, the mechanics though? Not seeing it.

The Republican Threat to Shut Down the Federal Government - Robert Reich - Newt Gingrich is saying if Republicans win back control of Congress and reach a budget impasse with the President, they should shut down the government again. GOP pollster Dick Morris is echoing those sentiments, as is Rep. Lynn Westmoreland (R. Ga), and Alaska GOP Senate candidate Joe Miller. I am continuously amazed at the GOP’s ability to snatch defeat out of the jaws of potential victory. It is the gift that keeps giving. I was there November 14, 1995 when Newt Gingrich pulled the plug on the federal government the first time. It proved to be the stupidest political move in recent history. Not only did it help Bill Clinton win reelection but it was a boon to almost all other Democrats in 1996 (Gingrich’s photo was widely used in negative ads), and the move damaged Republicans for years.

A GOP-Led Shutdown Could Be A Disaster For The GOP - Almost anyone who has been involved with the federal budget for a while has strong memories of House Budget Chairman John Kasich (R-Ohio) saying repeatedly in 1995 that the newly elected Republican majority was prepared to shut down the government to buck the Clinton administration and get its way with the budget. Kasich’s big line — that he doubted anyone would even notice whether federal departments were forced to shut their doors — was a great sound bite; it clearly implied that much of Washington’s work was of so little value that no one would, or should, care if it just stopped. Unfortunately for Kasich and the others most responsible for the shutdown strategy — Speaker Newt Gingrich (R-Ga.) and Majority Leader Dick Armey (R-Texas) — many Americans did notice People who had made reservations a year or more in advance to camp at the national parks were beyond furious when they couldn’t enter because the gates were closed. Government contractors howled when there was no one to process invoices, write checks or sign contracts, and they warned that layoffs were imminent if the situation didn’t quickly change.

Fiscal Policy Choices in Uncertain Times - CBO Director's Blog - In summary, the economic recovery will probably proceed at a modest pace—leaving total output well below its sustainable level, and the unemployment rate well above its sustainable level, for a number of years. In CBO’s judgment, the available monetary and fiscal tools, if applied at sufficient scale, would improve economic conditions during the next few years—though with costs and risks in the medium and long term. Policymakers need to address those trade-offs.

Uncertainty over New Deals - Lot's of chatter these days about what role the uncertainty over future policy regimes is playing in holding back a complete economic recovery. On the one side, we have the usual suspects claiming that the problem has little, if anything, to do with policy uncertainty. Instead, it is a lack of "aggregate demand." Mark Thoma provides a link to an interesting study here that appears to support this hypothesis. The study highlights the fact that small businesses are citing a lack of sales volume as their main source of trouble. Well, sure. If I'm a supplier of home furnishings, I'm going to cite a lack of demand for my product. But does this necessarily mean that the macro problem is a lack of aggregate demand? Possibly--but not necessarily. In an earlier post, I entertained the idea of investment demand falling off the cliff in response to fundamentally bad news relating to the future return to capital spending; see here. I still think there is some merit in this idea, though the data I presented here has led me to re-think this position. I could be wrong, but I think this data presents a similar difficulty for standard Keynesian interpretations of investment spending collapse.

The U.S. Needs a New and Improved New Deal - “What the country needs is a “new and improved new deal” that reduces the risks associated with structural change, and does a better job of preventing and easing cyclical downturns. The original New Deal, shaped by the experience of the Great Depression, was designed to overcome problems associated with large cyclical fluctuations in the economy. The “three Rs” that served as its guiding principles – relief, recovery and reform – reflected this emphasis. We also see the focus on cyclical problems in the development of monetary and fiscal policy tools as countercyclical stabilization devices, and in the automatic stabilizers that have been built into the economy. Both monetary and fiscal policy have helped to ease the cyclical downturn we are experiencing, but as our present experience makes all too clear, we can do better. Part of a new and improved new deal should focus on doing more to prevent problems before they occur and limiting the damage when cyclical downturns do occur despite our efforts.

Ezra Klein - Two graphs that should really scare us - Both of these come from the International Monetary Fund's new paper (pdf) on employment, which is graph-tastic. The first looks at the long-term effect unemployment has on the average male's long-term earnings. So a 25-year-old worker whose firm went under in 2008 will still be earning less than the guy in the office park across from him whose firm barely rode out the recession. We tend to think of employment as being binary: You have a job, or you don't. But it's more complicated than that. Losing a job has lingering effects, and not just on income. It also raises your risk of death going forward: This is one reason that jobs-sharing proposals like the one Germany implemented make some real sense: Keeping the maximum number of people in their jobs -- even if you temporarily reduce their hours or wages -- means fewer people losing their jobs altogether. That means their skills don't deteriorate, it means they're less likely to have to take a new job that they're not as good at or where they're paid a lot less, it means they don't have to explain away their unemployment to prospective employers, and so on.

IMF urges stimulus to help "dire" job market (Reuters) - The world's rich countries need to extend fiscal stimulus and job growth initiatives to fix a "dire" labor market that could threaten entire societies, the International Monetary Fund said on Monday. At a conference co-hosted by the IMF and the International Labor Organization, visiting Spanish Prime Minister Jose Luis Rodriquez Zapatero said high unemployment may trigger a "crisis of confidence" in Europe. The IMF said more and more workers worldwide were unable to find jobs for longer periods, weakening social cohesion and raising risks of unrest and even undermining democracy

The International Monetary Fund Is Not Insane – Krugman - That shouldn’t be startling; but these days it is. Given the way conventional madness has overtaken so many international institutions, the IMF’s reasonable, if much too cautious, new paper on employment (pdf) is actually a welcome surprise. “A recovery in aggregate demand is the single best cure for unemployment” — what a relief to see the Fund actually saying that. Also, note this passage: There is a risk of hysteresis in some countries, particularly in the United States and Spain, given the sharp increase in the duration of unemployment and the persistent nature of the shocks (e.g. to the housing sector) that lie behind the cyclical weakness in the economy and hence the increase in unemployment (see Benes et al., 2010 and Vitek, 2010). Hence to the extent that countries have fiscal space, exploiting it when there is a risk of hysteresis may create jobs in the short run without hurting the medium-run fiscal outlook. That’s written in international organization speak, but it seems like a response to this post; and it even seems as if the IMF may be sorta kinda endorsing the view that austerity in times like these may be self-defeating,

Biden Finds 100 Reasons to Like the Stimulus - The White House hit back today at critics of the stimulus plan with a report on 100 infrastructure and research projects funded by the plan it said “are changing America.” The White House is countering a list of 100 projects funded by the plan that Republican Sens. John McCain and Tom Coburn said “give taxpayers the blues.” Where Coburn and McCain went after spending on silly-sounding scientific research, little-used public infrastructure and leisure facilities, the White House has highlighted funding for research into cancer and autism, troop accommodation and treatment on military bases, and tunnels and roads. Read the White House report in full here. Vice President Joe Biden said in a statement accompanying the report that “with Recovery Act projects like these, we’re starting to turn the page on a decade of failed economic policies and rebuild our economy on a new foundation that creates good middle class jobs for American families.”

Opinion: Time to build a better stimulus - Joseph E. Stiglitz - A well-designed program would have a portfolio of measures that stimulates investment in the public and private sectors and helps those suffering most, both because of today’s recession and the stagnation of middle-class incomes for the past decade. A combination of help to small businesses, tax breaks for firms that actually invest, increased infrastructure spending, extended unemployment benefits and the continuation of the 2001/2003 middle-class tax cuts — the kind of program that Obama is now putting forward — is the right medicine for the economy today. Though we can quibble about the details (and details do matter), the president’s program is on target. But extending the tax cuts for America’s wealthiest 2 percent would be a big mistake. Resources are scarce — even in a rich country — and this is not the way to spend the government’s scarce dollars

9/10/10 OBAMA PRESS CONFERENCE TRANSCRIPT

Time for This Big Dog to Bite Back - NO, he can’t. President Obama can’t reverse the unemployment numbers by Election Day. He can’t get even a modest new stimulus bill past the Party of No, and even if he could, there would be few jobs to show for it until (maybe) 2011. Nor can he rewrite the history of his administration. Its signal accomplishments to date are an initial stimulus package that was overrun by the calamity at hand and a marathon health care battle as yet better known for its unseemly orgy of backroom wrangling than its concrete results. While that brawl raged, the White House seemed indifferent to the mounting number of Americans being tossed onto the Great Recession scrapheap.

The political failure of Obama’s stimulus package - When President Obama unveiled an array of new tax-cut and spending proposals last week, one word was noticeably missing from his speeches: “stimulus.” Republicans, meanwhile, energetically set about decrying the plan as “more of the same failed ‘stimulus’ ” and as simply a “second stimulus”—as if the word itself were a damning indictment. The idea of using countercyclical fiscal policy to help get a weak economy moving is hardly radical. But in Washington stimulus has become the policy that dare not speak its name. This wouldn’t be surprising if we were talking about a failed program. But, by any reasonable measure, the $800-billion stimulus package that Congress passed in the winter of 2009 was a clear, if limited, success. The Congressional Budget Office estimates that it reduced unemployment by somewhere between 0.8 and 1.7 per cent in recent months. Economists at various Wall Street houses suggest that it boosted G.D.P. by more than two per cent. And a recent study by Mark Zandi and Alan Blinder, economists from, respectively, Moody’s and Princeton, argues that, in the absence of the stimulus, unemployment would have risen above eleven per cent and that G.D.P. would have been almost half a trillion dollars lower.

Q&A: Geithner on the Economy, Tax Cuts and China - Treasury Secretary Timothy Geithner sat down with The Wall Street Journal to talk about the administration’s plans to help a sluggish economy. Here are some excerpts of the interview, which took place in his office at the U.S. Treasury Department Friday.

Geithner: "Important to avoid premature policy restraint" - A few excerpts from a WSJ interview with Treasury Secretary Timothy Geithner: Geithner Urges Action on Economy "[The] typical error most countries make coming out of a financial crisis is they shift too quickly to premature restraint. ... It is very important for us to avoid that mistake. If the government does nothing going forward, then the impact of policy in Washington will shift from supporting economic growth to hurting economic growth." And on tax cuts for high income earners: "We just don't think it would be responsible for this country, given the size of our future deficits, and given the substantial burden the middle class has been bearing over the past decade in particular, to go out and borrow $700 billion from our children so we can sustain those Bush tax cuts that only go to the wealthiest 2% of Americans." I agree with Geithner on both points.

The Optimal Level of Government Investment in the High-Tech World of 2010, not 1810 - In response to Stephen Williamson's opus magnum last week, I left a series of comments that actually exceeded his word count. I encourage you to read them and the whole discussion. I think there are a lot of important points and insights. But I especially think this part is important, and so will reprint it here with modifications and expansions to my original comment.

Fun With George Will - The Washington Post likes to run columns that are chock full of mistakes so that readers can have fun picking them apart. That is why George Will's columns appear twice a week. Let's have a little fun with the latest, which is an attack on President Obama's economic agenda. First, Will is anxious to tell readers that Democrats are telling the public that stimulus did not work because many think we need more stimulus. Actually, people who think we need more stimulus simply note that the stimulus was helpful, but not large enough for the task. According to the Congressional Budget Office, the stimulus added between 1.7 and 4.5 percent to GDP since its enactment (that's between $240 billion and $740 billion in additional output). It also lowered the unemployment rate by between 0.7 and 1.8 percentage points.

Economics: Bad economists - The Economist - Mr Mulligan thinks that fiscal stimulus can't boost the private sector, and he wants to find some support for this belief. He therefore considers this year's temporary census hiring, which added over half a million workers to the federal payroll for a few months in the spring in summer. If stimulus worked, Mr Mulligan says, this hiring should have had a multiplier effect on private hiring.Did it? To find out, Mr Mulligan charts total employment and employment ex-census. He says the census-driven spike in the former should produce an echo of a spike in the latter. He eyeballs it, and concludes: In fact, the spike..., if any, is pretty subtle. Science! Obviously, if one were actually interested in seeing what impact census hiring had on demand, one would probably make an effort to control for lots of other variables that might obscure monthly shifts (actually, if one were really interested in this question, one would probably stick with published research involving careful statistical analyses of larger samples of events)

Casey at the Blog: Joy in Recession Land - Professor Mulligan thinks that he can show that stimulus does not work by examining the job impact of the workers temporarily employed to carry through the 2010 Census. Mulligan notes the assumption of stimulus proponents that the there would be a multiplier effect of 1.6 for each job directly created by the stimulus. This means that for every person directly employed as a result of stimulus spending there would be 0.6 jobs created as a result of the spending out of this worker’s wages. Mulligan applies this arithmetic to the hiring of temporary Census employees earlier this year. Census employment peaked at just under this 600,000. The 0.6 multiplier would imply a jump in 360,000 non-Census related jobs. Mulligan looks at the data and cannot find any evidence of this sort of jump and believes that he has an important piece of evidence against the stimulus. Let’s think about this a bit more closely. The Census jobs were very temporary and part-time jobs. There was a short spike in Census employment that then fell off very rapidly. Employment peaked at 586,000 in the first week in May, but the peak four-week average employment was just 571,000. The average for the prior four weeks was 156,000, and in the subsequent four weeks employment was 376,000, falling to 188,000 in the next four week period. So the vast majority of Census workers were employed for less than two months.

Greenspan calls for tax hike -Greenspan advocated that U.S. officials drop their bias for stimulus and move toward the stance seen in recent months in Europe, where governments have focused on cutting spending in a bid to put their finances on a more sustainable footing. He said delaying so-called fiscal consolidation for two years to allow the economy to recover, and the deficit to deepen, risks a debilitating shift in psychology. He said this happened in 1979, when Treasury rates spiked as inflation fears took off. and he warned that policymakers must take steps now to prevent a recurrence. "I don't think we have time to wait," Greenspan said. "Our choice is not between good and bad, it's between terrible and worse."

Orszag Takes Another Swipe at Obama - For the second time in a week, Peter Orszag has zinged his former boss. Orszag, who just left his job as President Barack Obamas budget chief, said Sunday the presidents policy of making the Bush-era tax cuts permanent for middle-income families would jeopardize the nation's finances. Last week, he made the same argument in a New York Times column that took the White House by surprise. “We, unfortunately, can’t afford the tax cuts over the medium and long term,” Orszag said on CNN’s “Fareed Zakaria GPS.” “We face too large a deficit out in 2015, 2018, 2020.” Orszag called for extending all of the Bush-era cuts for two more years and then letting all of them expire. He emphasized that the temporary extension should apply to all income earners, even the wealthy – another point on which the White House disagrees. Obama has said he wants the tax cuts to lapse for families with incomes above $250,000.

Fate of tax cuts is key issue as Congress returns - Congress is returning for a final pre-election legislative session on Monday to confront the thorny issue of potentially raising taxes during an economic downturn, with neither party showing clear consensus on a solution. The main order of business in the coming weeks will be debating the fate of income tax cuts approved under the George W. Bush administration in 2001 and 2003 that are scheduled to expire at the end of this year. House Minority Leader John A. Boehner (R-Ohio) surprised Democrats on Sunday when he said he might not oppose President Obama's plan to extend the cuts for all but the wealthiest households, although he reiterated his preference for keeping the lower rates in place for all income groups. Boehner's comments, made on the CBS program "Face the Nation," altered the landscape of the tax debate by suggesting that Republicans might not obstruct Democratic efforts to raise taxes on the top earners.

Boehner Agrees with Keynesians, Signals He’s Open to Obama Tax Cut - Is Boehner backing off his position that the tax cuts for the wealthy must be extended?: House G.O.P. Leader Signals He’s Open to Obama Tax Cut, NY Times: The House Republican leader, Representative John A. Boehner of Ohio, said on Sunday that he was prepared to vote in favor of legislation that would let the Bush-era tax cuts expire for the wealthiest Americans if Democrats insisted on continuing the lower rates only for families earning less than $250,000 a year. Mr. Boehner ... said... “I think raising taxes in a very weak economy is a really, really bad idea,” ... That's very Keynesian of him to have the concern that "raising taxes in a very weak economy is a really, really bad idea," and there's an easy response for Democrats, one I discuss here. The Democrats say okay, if that's your concern, why not transfer the tax cuts, temporarily, to lower income groups who are much more likely to spend the money, or use it to backfill state and local budgets to stop further job losses?

House’s Boehner Says He Would Vote for Middle-Class Tax Cuts… -- U.S. House Republican Leader John Boehner said he would vote for middle-class tax cuts sought by the Democratic Obama administration even if it means eliminating reductions for wealthier Americans. Boehner would support extending tax cuts for those making less than $250,000 a year “if that’s what we can get done, but I think that’s bad policy,” he said yesterday on CBS’s “Face the Nation” program. “If the only option I have is to vote for some of those tax reductions, I’ll vote for it.” “I’m going to do everything I can to fight to make sure that we extend the current tax rates for all Americans,” Taxes are expected to dominate the agenda when Congress returns this week. Boehner’s remarks came after House Democrat Chris Van Hollen said he would consider extending the Bush-era tax cuts for wealthier Americans for a year if Republicans would agree to make the reductions permanent for the middle class.

Those “Best-for-Nothing” Bush/Obama Tax Cuts -First, isn’t it “special” that House Minority Leader John Boehner and President Obama might be ready to “compromise” on what to do about the Bush tax cuts? From a story by Shailagh Murray and Lori Montgomery in today’s Washington Post: House Minority Leader John A. Boehner (R-Ohio) surprised Democrats on Sunday when he said he might not oppose President Obama’s plan to extend the cuts for all but the wealthiest households, although he reiterated his preference for keeping the lower rates in place for all income groups. But read on in the same Washington Post story. Boehner didn’t say he would support letting the top-end cuts expire. He said he wouldn’t oppose extending all the rest of the tax cuts President Obama is already proposing to extend:

Zandi: Keep Tax Cuts Until Economy Mends - “High unemployment has cast a shadow on Americans’ collective psyche that will only darken with higher taxes, raising the already-uncomfortable odds that the economy will suffer a double-dip recession,” says the new analysis by Mark Zandi of Moody’s Economy.com, who has been an adviser to House Democrats and to 2008 GOP presidential nominee John McCain. By contrast, “allowing the tax cuts for high-income households to expire over, say, a three-year period would not harm the economy,” the analysis says. Wednesday’s analysis concludes that the plan by Democratic leaders to end current tax levels for families making more than $250,000 could do serious harm, reducing real gross domestic product by 0.4 of a percentage point in 2011, cutting payroll employment by 770,000 and raising the unemployment rate by almost 0.4 of a percentage point by mid-2012, the peak of the impact. And the real-world response by higher earners could make the impact somewhat worse, the analysis concludes, particularly in consumer spending, where higher-income earners account for about one-fourth of all U.S. personal outlays.

The Tax-Cut Racket, by Paul Krugman -“Nice middle class you got here,” said Mitch McConnell, the Senate minority leader. “It would be a shame if something happened to it.” O.K., he didn’t actually say that. But he might as well have, because that’s what the current confrontation over taxes amounts to. Mr. McConnell, who was self-righteously denouncing the budget deficit just the other day, now wants to blow that deficit up with big tax cuts for the rich. But he doesn’t have the votes. So he’s trying to get what he wants by pointing a gun at the heads of middle-class families, threatening to force a jump in their taxes unless he gets paid off with hugely expensive tax breaks for the wealthy. How did we get to this point? The Bush administration bundled huge tax cuts for wealthy Americans with much smaller tax cuts for the middle class, then pretended that it was mainly offering tax breaks to ordinary families. Meanwhile, it circumvented Senate rules intended to prevent irresponsible fiscal actions by putting an expiration date of Dec. 31, 2010, on the whole bill. And the witching hour is now upon us.