Fed Balance Sheet Grows To $2.842T For Week Ended Nov 9 - The U.S. Federal Reserve's balance sheet grew a week after the central bank said it would continue with a strategy to stimulate economic growth by adjusting its massive portfolio of securities. The Fed's asset holdings in the week ended Nov. 9 stood at $2.842 trillion, up from the $2.825 trillion reported a week earlier, the central bank said in a report released Thursday. Holdings of U.S. Treasury securities moved up to $1.668 trillion from $1.654 trillion the week before. The central bank's holdings of mortgage-backed securities held steady at $849.26 billion. Thursday's report showed total borrowing from the Fed's discount lending window was $10.61 billion, down from the $10.84 billion a week earlier. Borrowing by commercial banks fell to $9 million from $62 million. The Fed report showed that U.S. marketable securities held in custody on behalf of foreign official accounts stayed at about $3.442 trillion last week. Meanwhile, U.S. Treasurys held in custody on behalf of foreign official accounts dipped to $2.719 trillion, compared to $2.720 trillion the previous week. Holdings of agency securities grew to $723.28 billion from $722.02 billion the prior week.

FRB: H.4.1 Release--Factors Affecting Reserve Balances -- November 10, 2011

Rosengren: Fed needs to act aggressively on economy (Reuters) - The Federal Reserve should continue to act "aggressively" to try to bring down the stubbornly high U.S. jobless rate and boost lagging economic growth, a top Fed official said on Monday. Eric Rosengren, President of the Boston Federal Reserve Bank, said weak labor conditions would help keep inflation below 2 percent over the next several years. "Given the very weak labor market conditions and the low expected inflation rate, the Federal Reserve should in my view continue to take action to aggressively try to reduce the stubbornly high U.S. unemployment rate," Rosengren said. Rosengren touched on policy issues only briefly in prepared remarks to the New England Board of Higher Education conference on higher education and the workforce. He said that economic growth had been lethargic despite the Fed's policy actions, and that at 9 percent in October, the jobless rate remains "unacceptably high."

Rosengren Says Fed Should Act to Bring Down Unemployment Rate (Bloomberg) -- Federal Reserve Bank of Boston President Eric Rosengren said the central bank should act to bring down “stubbornly, and unacceptably, high” joblessness that’s been stuck near 9 percent or above since April 2009. “Given the very weak labor market conditions and the low expected inflation rate, the Federal Reserve should in my view continue to take action to aggressively try to reduce the stubbornly high U.S. unemployment rate,” Rosengren said in the text of remarks given in Boston today. He forecast inflation will be below 2 percent “over the next several years.” The central bank may take new steps to boost growth, such as buying mortgage bonds or changing the way it communicates its policy goals to the public, Fed Chairman Ben S. Bernanke said after the Federal Open Market Committee’s two-day meeting ended Nov. 2. Policy makers last week left unchanged their plans to lengthen the maturity of the Fed’s bond portfolio, known as Operation Twist, and to keep the target federal funds rate near zero through at least mid-2013 as long as unemployment remains high and the inflation outlook remains “subdued.” “The Federal Reserve should continue to use the tools at its disposal to boost demand in the economy,” Rosengren said, without specifying what steps should be taken.

General Ben's marching orders - CHARLIE EVANS of the Chicago Fed has been pressing his colleagues to give employment more weight in monetary policy, arguing for example that even assigning higher weight to inflation, in a classic Taylor Rule, would permit a more aggressively easy policy now. Does Ben Bernanke agree? Judging from his remarks to troops today in Texas, it looks like he’s even more hawkish on employment than Mr Evans: Supporting job creation is half of our marching orders, so to speak; the other half is controlling inflation," he said, adding that while high unemployment remains a challenge, he at least expects inflation to remain low for the "foreseeable future. So I make the coefficient on employment in Mr Bernanke’s Taylor Rule to be equal to that of inflation. That's interesting; Mr Evans’ argued that even if it was just a quarter of that of inflation, more QE was justified.

At Fed, louder calls for action on economy - Federal Reserve officials who advocate new action to try to strengthen the economy are becoming more vocal in their push, taking their arguments to the public and making them more forcefully within the Fed policy committee. But words haven’t resulted in deeds — and the consensus view among the central bank’s top policymakers is that there would need to be clear evidence of new deterioration in the economy to justify any move to pump out more money. A flurry of speeches in recent weeks led some people in the financial markets to conclude that the central bank is in a hair-trigger stance, on the verge of some new action, such as buying hundreds of billions of dollars of mortgage-related securities in a bid to bring down mortgage rates. One Fed policymaker took the unusual step of dissenting in favor of more aggressive action at last week’s meeting. But although there are several influential Fed officials who would be inclined to do just that, the more widely held view on the central bank — reflected in its decision last week to stand pat and take no new action 1— is that the potential benefits are still too modest to be worth the risks. In particular, with mortgage rates already exceptionally low, it is not clear that Fed action would spur any more activity in the housing sector even if it lowered rates further. “Things would have to get noticeably worse before a new round of QE,”

Plosser on Communications - Charles Plosser of the Philadelphia Fed gave a noteworthy speech today on how the US central bank might improve its communication policies.Mr Plosser has always been interesting on this subject — he is a long time advocate for a defined Fed inflation objective — but he is especially worth paying attention to now as a member of the Fed subcommittee that is looking at communications.Mr Plosser is the obvious ‘hawk’ on that committee — the other members are vice chair Janet Yellen, governor Sarah Bloom Raskin, and Chicago Fed president Charles Evans — and its clear that there is a lot of common ground on inflation objectives and on providing more information about the forward path of policy. Where Mr Plosser clearly wants to make a stand is against using any change in communication as a back door to tacit acceptance of higher inflation. Here is part of his speech:

Kocherlakota Says Fed Should Make Public Contingency Plan - Federal Reserve Bank of Minneapolis President Narayana Kocherlakota said the U.S. central bank should develop and make public a contingency plan that would explain how it would react to developments in the economy. Such a contingency plan by the policy-setting Federal Open Market Committee would “provide clear guidance on how it will respond to a variety of relevant scenarios,” Kocherlakota said a contingency plan would reduce uncertainty about the Fed’s actions among consumers and companies, which he said has reduced incentives to spend and hire. It would also enhance the central bank’s credibility and transparency, he said. His comments extend a discussion among members of the FOMC about how to better explain their forecasts and policies to the public. At a press conference last week, Fed Chairman Ben S. Bernanke said options include clarifying the central bank’s long-term inflation goal, publishing the likely path of interest rates, and tying the Fed’s pledge to hold rates low to specific levels of employment and inflation -- a strategy espoused by Chicago Fed President Charles Evans.

Pursuing Financial Stability at the Federal Reserve - Janet Yellen -speech at the Fourteenth Annual International Banking Conference, Federal Reserve Bank of Chicago

Hit With Big Withdrawals, Fed Sells Assets, Borrows Cash - The Fed was hit with withdrawals of $83.3 billion last Wednesday, the largest withdrawals from its deposit accounts that were not associated with quarterly tax payments since February of 2009. $7 billion of that was the net cash transferred to the US Treasury from its note and bond sales less outlays. The Fed still had to meet the other $76 billion. These transactions were revealed in the Fed's weekly H.4.1 report. The Fed was apparently forced to take extraordinary measures to fund these withdrawals. These included the outright sale of nearly $24 billion in its Treasury note and bond holdings from the System Open Market Account. As a result, the Fed's System Open Market Account (SOMA) fell to $2.611 trillion, some $43 billion below the Fed's stated target of $2.654 trillion. Prior to this week, it had not strayed from by more than $7 billion since June. The Fed's action was not only a direct contradiction of its stated policy, but it was done without warning or explanation. The Fed took another unusual and virtually unprecedented action to fund these massive withdrawals. It borrowed $43 billion from foreign central banks (FCBs) through Reverse Repurchase Agreements (reverse repos, or RRPs).

The Fed Needs To Get Ahead of the Eurozone Crisis - Brad DeLong says what I have been thinking for some time:Where is my fed announcement that it will not let chaos in Europe cause a double dip here? Exactly. The Fed needs to be proactive not reactive, otherwise it risks making the same mistakes it made in 2008. Here is what I said along these same lines earlier this year: Nick Rowe is concerned that the collapse of the Eurozone could lead to another Lehman-type event for the global financial system. He is also wondering what central banks should be doing in preparation for such an event. Nick is not the only one concerned. Others have expressed concerned that financial contagion could arise from credit default swaps on Greek bonds or U.S. money market funds that are indirectly linked to the Greek economy through investments in the core Eurozone countries. Even Fed Chairman Ben Bernanke expressed concern in his last press conference about the indirect exposure the U.S. economy has to Greek crisis: So what can the Fed do? Here is a suggestion: the Fed could say if total current dollar spending begins to plummet because concerns about the financial system are causing investors to rapidly buy up safe money-like assets then the Fed would begin buying up less-safe and less-liquid assets until the investors' demand for money-like assets is satiated such that they return total current dollar spending to its previous level.

Economist Sees No Immediate Fed Reaction to Europe - Europe’s financial crisis may be quickening, but an economist at one bank doesn’t expect much of a reaction from the Federal Reserve, at least not yet. At issue are the still existing parts of the Fed’s emergency-response tool kit. Much of what Ben Bernanke’s Fed put in place to address the financial crisis has been dismantled due to a lack of need. The main arrows still in the quiver are the Fed’s dollar liquidity facility for major central banks and its long-standing discount window, which provides emergency loans to deposit-taking banks with appropriate collateral. Eric Green of TD Securities argues in a note Wednesday that continuing troubles in Europe have not reached a point where the Fed feels it needs to make these emergency-lending tools more affordable to use, relative to the de facto zero-percent overnight federal funds rate target and market-based borrowing costs. As Green sees it, perception is the main reason why the Fed is likely to leave its emergency tools unchanged. “The Fed will provide as much dollar liquidity to Europe as necessary,” but it will continue to do so on terms more expensive than the market.

Fed's Yellen warns of low interest rate risks - Federal Reserve Vice Chairman Janet Yellen said in Chicago today that European sovereign debt and banking issues are straining global financial markets and “pose significant downside risks to the U.S. economic outlook.” U.S. banking institutions have “manageable levels of direct exposure to the peripheral European countries, but more substantial links to financial institutions in the larger European economies,” she said. She also raised concerns about U.S. money market funds, emphasizing that international linkages through those funds could “lead to a deterioration of financial conditions in the United States.” Yellen was speaking at the Chicago Federal Reserve International Banking Conference, which is reviewing the financial crisis of the last few years and examining what central bankers throughout the world can do to avoid future systemic risk. She noted that Fed staff is currently in the process of reviewing banking compensation to determine whether it stimulates risky practices.“We want to insure that compensation isn’t a source of risk,” she said.

Video: Sumner Says Nominal GDP Target Can Save the Recovery - WSJ - Bentley University economics professor Scott Sumner says the Federal Reserve ought to be far more aggressive in stimulating the U.S. economy and explains how a nominal GDP target would be a better way to run monetary policy.

Supply Shocks and Nominal GDP Targeting - Adam P is a bit irritated with all the attention being given to nominal GDP targeting and has been tossing some "volatility critique" and "optimality critique" grenades our way. Fortunately, the volatility critique grenade was a dud, though I am still am holding and sizing up the optimality one. Hopefully, it doesn't blow up. His latest bombardment on the nominal GDP camp comes in an attempt to critique what I think is one of the biggest benefits of nominal GDP targeting: how it deals with supply shocks. This latest bombardment, however, is not a dud but ironically ends up blowing apart inflation targeting rather nominal GDP targeting. Here is why. Inflation is the result or symptom of underlying shocks to aggregate demand (AD) and aggregate supply (AS). Monetary policy, however, can only meaningfully influence AD so that is where its focus should be. This cannot happen with strict inflation targeting because it requires the central bank to respond to any change in inflation, regardless of whether it is caused by AD or AS shocks. In other words, inflation targeting causes the central bank to respond to AS shocks when it should only be responding to AD shocks. A nominal GDP target acknowledges this distinction and appropriately focuses monetary policy on the cause (AD shock) not the symptom (inflation). Adam P., therefore, is therefore right to claim that monetary policy cannot "fix" a supply shock, but he has it completely backward when he claims that this does not happen with inflation targeting

Let them eat NGDP -This weekend, at an INET conference, Mike Konczal of Rortybomb made the excellent point that the econ blogosphere is probably adding more new policy ideas to the public discourse right now than academia itself. He identified NGDP targeting as the most important and dramatic example. And boy was he right! NGDP frenzy has reached truly astonishing levels. I have my doubts that the Fed will actually adopt an NGDP target, but there is no denying that the blogosphere and much of the popular press has fallen for this idea like girls at my college fell for Thom Yorke back in 1999 (no I'm not bitter, why do you ask?). These days Scott Sumner says "NGDP" like Herman Cain says "9-9-9." Now, I am all for looser monetary policy, whether it comes in the form of an NGDP target or not. But NGDP has reached the point where, like Radiohead, its cult status is actually starting to annoy me. Take, for example, this post from Matt Yglesias (an extremely sharp dude) on how NGDP is the "actual thing": [I]t seems natural to many people to take [real GDP and inflation] as “given” and understanding NGDP (= GDP + inflation) as somehow constructed and exotic. But actually NGDP is, relatively speaking, the simple quantity here. It measures total spending in the economy. You count everything, add it all up, and you’ve got your NGDP...

Fed's Plosser: Wrong To Let Inflation Rise To Cut Unemployment--A key Federal Reserve official struck back Tuesday against other central bankers willing to tolerate a higher inflation rate as the result of policies that would bring down the unemployment rate, and said improved economic prospects argue against further stimulus. Federal Reserve Bank of Philadelphia Charles Plosser argued strongly that any move to allow inflation to accelerate, regardless of the motivation, is wrong-headed and could result in a repeat of the 1970s stagflation era of high unemployment and high prices. As he has in the past, the voting member of the interest rate-setting Federal Open Market Committee used remarks given in Philadelphia to argue that the central bank should concentrate on making monetary policy with price stability alone in mind, given that is the economic variable the Fed has the most power to control. He also countered rising speculation that high unemployment, weak growth and low inflation will drive the Fed to provide further stimulus to the economy via buying Treasurys and mortgages to grow the central bank balance sheet. "It's not clear to me further action is justified at this time," Plosser said

Can the Fed Stimulate Growth or Only Inflation? - Many economists, myself included, believe that a more aggressive Federal Reserve policy is needed to turn the economy around. Additional fiscal stimulus would also help. As the chairman of the Federal Reserve Board, Ben Bernanke put it at a Nov. 2 news conference, “It would be helpful if we could get assistance from some other parts of the government to work with us to create jobs." However, such assistance will not be coming. President Obama’s jobs package has been blocked by Republicans in Congress, and the order of the day is fiscal tightening, with the Joint Select Committee on Deficit Reduction poised to offer recommendations for $1.5 trillion in additional deficit reduction by Nov. 23. With fiscal stimulus off the table, monetary stimulus is all that is available. But the Republican view is that monetary policy is incapable of stimulating real growth – that it will stimulate only inflation. This view is regularly enforced by The Wall Street Journal editorial page, which establishes the ideological line for Republicans on Fed policy.

Supply-side Policies as a Way to Boost Aggregate Demand - Mankiw - This paper from the Philadelphia Fed makes an important point: This paper examines how supply-side policies may play a role in fighting a low aggregate demand that traps an economy at the zero lower bound (ZLB) of nominal interest rates. Future increases in productivity or reductions in mark-ups triggered by supply-side policies generate a wealth effect that pulls current consumption and output up. Since the economy is at the ZLB, increases in the interest rates do not undo this wealth effect, as we will have in the case outside the ZLB. We illustrate this mechanism with a simple two-period New Keynesian model. We discuss possible objections to this set of policies and the relation of supply-side policies with more conventional monetary and fiscal policies.

Trouble Ahead: Employment, Inflation, And The Fed - Yesterday the Bureau of Labor Statistics told us that unemployment was still stubbornly high. While it has improved year-over-year, a 9.0% unemployment rate is still high and does not signal an economy in recovery. And that has political and policy implications for the U.S. Also, the Fed's FOMC (Fed Open Market Committee) minutes were released Wednesday and Fed Chairman Ben Bernanke held a press conference as part of the Fed's new openness and desire to clearly communicate policy. They made no policy changes but Bernanke expressed concern about the slow recovery and high unemployment and said "We're prepared to do more and we have the tools to do more." Unemployment, Fed policy, and the coming worldwide economic recession will do more to influence the future of our economy than anything else.

Maybe the problem is Boehner, not Bernanke - The Fed is coming under a lot of criticism from commentators and economists of a Keynesian bent (myself included) for its reluctance to take dramatic action to put the economy on the road to recovery. The economy is stuck in neutral with unemployment at 9 percent; has been pretty much so for a year and a half. The Fed has many tricks it could pull from its sleeve, most promising among them large scale purchases of mortgage backed securities to encourage refinancing under the new HARP rules or announcing a commitment to target nominal GDP or inflation backed up by large scale asset purchases. Ezra Klein says that Obama's decision to reappoint Ben Bernanke may have been a serious mistake; Paul Krugman says he used to think that Bernanke was a dove saddled with more hawkish colleagues on the FOMC, but now he thinks Bernanke just doesn't get it. Tim Duy says the Fed's inaction is "inexplicable." Brad DeLong and Mark Thoma are similarly disappointed. But perhaps the problem is not Ben Bernanke but the political environment in which he is operating.

Why Spotting Bubbles Is Harder Than It Looks - Ever since 1841, when a Scottish journalist named Charles Mackay published the book known today as "Extraordinary Popular Delusions and the Madness of Crowds," the answer has seemed clear. If you watch carefully for signs of euphoria, you can sidestep the damage when markets go mad. But bubble spotting isn't as simple as Mackay made it sound—even, it turns out, for Mackay himself. Investors should always guard against the glib assertions of pundits who claim they can detect bubbles before they burst. It's also a reminder that expecting policy makers to predict the future by popping "bubbles in the making" is probably a bad idea. Although plenty of people claim to have seen bubbles in hindsight, determining when enthusiasm morphs into euphoria is an inexact science at best. Consider today: With the global financial crisis lingering, but initial stock offerings like Groupon buoyant, is the stock market a bubble? When ATMs dispense gold bars, is gold a bubble? When some of the biggest bond investors say they are willing to buy Treasury bills at negative yields that lock in losses, are government securities a bubble?

The negative unnatural rate of interest - David Andolfatto points out that US five-year real interest rates are now negative. Nick Rowe discusses the possibility that the so-called “natural” real interest rate could be negative, referring us to Frances Woolley’s discussion of the drag demographics might exert on real returns. (I’ll respond to Rowe and Woolley specifically in a little appendix to this post, but I want to start more generally.) When we observe negative real rates, they are often attributed to something abnormal. Perhaps it is “depression economics” which has driven interest rates underground, or, as Andolfatto rather charitably considers, a misguided tax and regulatory regime. I think this aberrationist view is quite wrong. I don’t think you can make sense of the last decade without understanding that the so-called real interest rate has been trying to fall through zero for years. Only tireless innovation by the men and women of Wall Street prevented negative rates long before the traumas of 2008. A deep cause of the financial crisis was a simple expectation: That lenders ought to earn a “decent” real, risk-free yield even while a variety of trends — skyrocketing incomes for the 0.1%, the professionalization of investing, leverage-induced risk aversion, China — were creating Ben Bernanke’s famous savings glut. There is no such thing as a “natural” anything in economics. Economic behavior is human artifact and artifice.

The Return Of Secular Stagnation - Krugman - Steve Randy Waldman has a characteristically interesting post on interest rates. He starts from the observation that real rates are now negative — lenders are actually willing to accept a negative yield on inflation-protected bonds: He then argues that the”natural” real rate of interest — the interest rate that would match savings and investment at full employment — has been negative for quite a while, and that we’re only seeing this now because various bubbles and deregulatory schemes have masked the reality. What he doesn’t say, but immediately strikes anyone who knows some of the history here, is that this amounts to a return of the “secular stagnation” hypothesis that was popular in the early postwar years; the hypothesis was that there was a fundamental excess of desired savings over desired investment, and that this would require government intervention on a sustained basis to achieve full employment.That hypothesis proved wrong at the time, but that doesn’t mean it couldn’t be true now. And I’m somewhat sympathetic to the view that it might indeed be true. Waldman goes on to suggest that high income inequality is what’s driving this — he has a little parable involving bakers and bread that ultimately comes down to the rich being satiated while the poor cannot afford to buy.

What Moves the Interest Rate Term Structure? - SF Fed Economic Letter - To understand the effects of news on bond markets, it is instructive to look beyond individual maturities and consider the entire term structure of interest rates. For example, unexpected changes in monthly nonfarm payroll employment numbers cause large movements at short and medium maturities, but do not affect long-term interest rates. Inflation news affects the long end of the term structure. Monetary policy actions vary in their effects on interest rates, but cause volatility at all maturities, including distant forward rates.

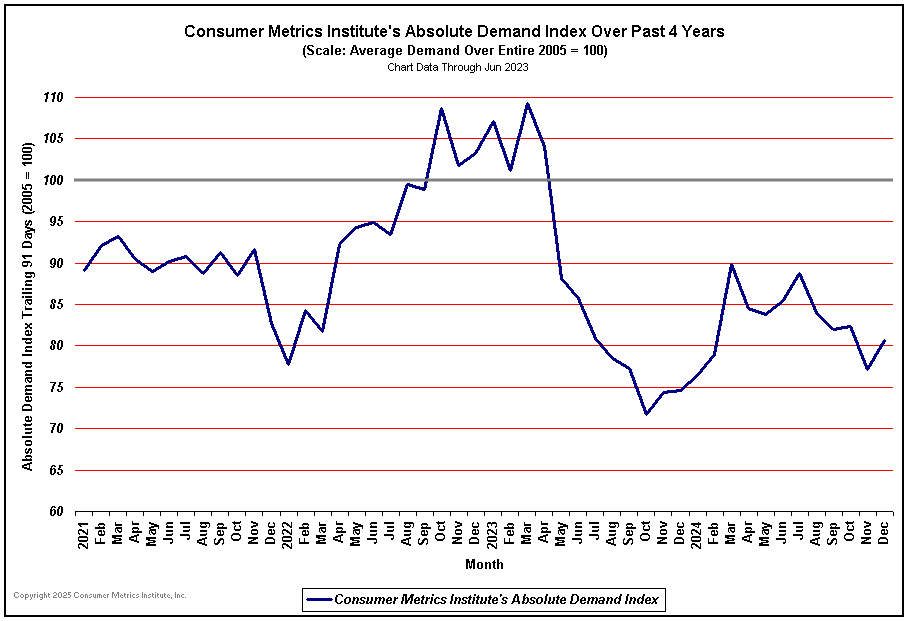

Perfect Storm; Eight Reasons to be Bullish on the US Dollar - One of my much appreciated contacts is Steen Jakobsen, chief economist for Saxo Bank in Copenhagen, Denmark. Today he passed on an "internal note" that he gave permission to share. For ease in reading, I will not follow with my usual indented blockquote format. Steen Writes ... One of my main themes over the last quarter has been a “relative outperformance” of the US economy relative to consensus. This has materialized and our call was almost entirely driven by Consumer Metric data which over the last three years has outperformed any other relevant predictor. This is now slowing down slightly, but still elevated. Meanwhile Europe start election cycle where Spain goes to the election in less than two weeks, while Sarkozy starts his re-election campaign when he is done playing Napoleon in European politics. The outlook for 2012 is a “Perfect Storm” with increased austerity, higher unemployment, and weaker global growth (read: China). My colleague Peter Garnry was kind enough to quickly program a small excel thing which can track changes to growth by consensus using the ECST function on Bloomberg. This is the result.

Liquidity Traps And Hawaiian Shirts - Krugman - It’s somewhat awesome to realize that many people in the world of finance are just now awakening to the reality that we’re in a liquidity trap. Here’s the FT:Over the past 30 years, US Treasuries have been in an extraordinary bull market with yields on a near-constant downwards path. But as US yields – and those of Germany and the UK – approached 3 per cent, market commentators were unanimous that 2011 would see equities outperform bonds. Yields had to go up. How foolish such predictions look now.…“In a Japan-like scenario bonds are fair value,” says David Jacob, chief investment officer of Henderson Global Investors. “I think we are in a liquidity trap to some extent and it’s very difficult to climb out of it.”A liquidity trap refers to the inability of monetary policy to stimulate the economy and many investors are worried that central banks may be able to keep government bond yields low but that will have little direct impact on growth. And I thought it was obvious three years ago that we were in a Japan-type liquidity trap.

"What can exports tell us about the economy?" - There has been considerable debate lately about why the U.S. economy continues to struggle. Some have argued that concerns about future taxes and regulation are preventing American businesses from investing and hiring. Other economists have argued that we have inadequate aggregate demand in the economy and that explains slow GDP and employment growth -- not fear of future government policy. Additional evidence comes from something Menzie posted about last week: the strong performance of U.S. exports. One way to sort out the competing explanations is to see what happens when there is substantial demand for U.S. products. In foreign markets where economies are growing quickly, U.S. exports are rising fast. American businesses do not seem to be held back by fear of taxes or regulation; they are hiring and increasing production for sale where there are customers. U.S. exports have surged since the end of the recession. Real exports are up 23% in the 9 quarters since the recession ended (a better performance following a recession than any of the last 3 recessions including the strong early 1980s recovery). Nominal exports are up even more as the price exporters can get on world markets has been rising.

Autos, housing, and the business cycle - Here I offer some observations on what's been holding back the recovery. Two of the most important sectors in U.S. business cycle fluctuations are autos and housing. For example, in the 2007:Q4-2009:Q2 recession, real GDP fell on average at a 2.7% annual rate, with autos and housing accounting for about half of this decline all by themselves. Although autos and housing make a very significant contribution to changes in GDP growth rates over the business cycle, they represent only a small part of the level of total GDP. Over 1947-2011, spending on motor vehicles and parts only amounted to 3.5% of total GDP on average, while housing was less than 4.7%. But the fluctuations in spending on new cars and homes are so volatile, these percentages change quite a bit over the cycle, rising well above average during expansions and falling in contractions. For 2011:Q3, motor vehicles and parts represented 2.4% of the level of GDP, while residential fixed investment was only 2.2%.

Economic Perspectives - If you are an investor the good news is that productivity growth improved sharply. Unit labor cost fell in the third quarter and the spread between pricing and labor cost widened nicely. This implies that earnings growth is accelerating and that my earlier fears that earnings expectations were too high is no longer a problem. The bad news is that with strong productivity, hours worked and income growth weakened. In the third quarter, nominal personal income expanded at under a 1% annual rate, a sharp slowing from the roughly 5% growth over the past year. Moreover, average hourly earnings growth continues to slow. Now at 1.56%, it is approaching an all time record low. The recent improvement in consumer spending did not stem from improved real incomes. Rather it was financed by a drawing down of savings. While the headlines are dominated by Europe’s problems and the market is reacting strongly to these headlines, SEER continues to believe that the biggest market-economic threat is the extremely weak income growth. With such weak income growth, it will be difficult for the consumer to sustain the stronger consumption growth of recent months. Yet increased personal consumption expenditures accounted for 1.72 % of the 2.5% growth in third quarter real GDP. This is especially true if the lower social security tax is not renewed for 2012 and/or if oil prices continue to rebound. SEER’s real retail sales model implies that real retail sales growth should be approaching zero.

Predicting GDP With ARIMA Forecasts - Is the U.S. economy headed for a new recession? The risk is clearly elevated these days, in part because the euro crisis rolls on. The sluggish growth rate in the U.S. isn’t helping either. But with ongoing job growth, albeit at a slow rate, it's not yet clear that we've reached a tipping point. Given all the mixed signals, however, forecasting is unusually tough at the moment. It’s never easy, of course, but it’s always necessary just the same. But how to proceed? The possibilities are endless, but one useful way to begin is with so-called autoregressive integrated moving averages (ARIMA). It sounds rather intimidating, but the basic calculation is straightforward and it's easily performed in a spreadsheet, which helps explain why ARIMA models are so popular in econometrics. A more compelling reason for this technique's widespread use: a number of studies report that ARIMA models have a history of making relatively accurate forecasts compared with the more sophisticated competition.

$99 Oil For 11/11/11 - Presented with little comment - except a reminder that: "every $1 per barrel rise in oil decreases U.S. GDP by $100 billion per year and every 1 cent increase in gasoline decreases U.S. consumer disposable income by about $600 million per year."

Niall Ferguson: It’s the Stupid Economy - Matt Duss introduces this video: “If you thought Niall Ferguson was an insufferable git in print, just wait.”

ECRI Doubles Down on Recession Call; Points to "Contagion of Forward Leading Indicators" - The Economic Cycle Research Institute is the "world's leading authority on business cycles" whose "state-of-the-art analytical framework is unmatched in its ability to forecast cycle turning points."¹ Furthermore, The Economist magazine has stated that they are perhaps "the only organization to give advance warning of each of the past three recessions; just as impressive, it has never issued a false alarm." Two months ago, the ECRI made a very definitive and unwavering recession call going even so far to say that "there’s nothing that policy makers can do to head it off." Since then, the markets have rallied strongly on the heels of recent positive economic data, leading many in the mainstream financial press to accept that the U.S. has narrowly averted an impending recession and will begin to see growth. Not so, says Lakshman Achuthan, ECRI's chief economist and spokesman; citing under no uncertain terms that "nothing has changed our view": (Click here if video does not load)

World Faces Subpar Growth for Next 14 Years - The world economy will struggle to grow above its potential over the next five years as advanced economies recover but the gain is offset by a slowdown in emerging markets, according to a global forecast released Tuesday by the Conference Board. Over time, the emergence of larger middle classes in the developing markets will help global businesses that must adjust to declining demand among struggling middle-class consumers in the advanced nations. The Conference Board’s global forecast expects world gross domestic product to grow 3.2% in 2012 and accelerate to 3.5% from 2013 until 2016. Farther out, growth is projected to average 2.7% from 2017-2025. Each period’s projected pace is less than the 3.6% average during the 1996-2005 period, before the severe recession hit. The board’s forecast was prepared to help its business members adapt to a changing world economy. Dow Jones Newswires and The Wall Street Journal were given exclusive access to the forecast. Click for full-size chart.

Another Layer - In his latest Weekly Market Comment, John Hussman who manages the Hussman Funds, adds another layer of data to the "debate" -- actually, the one-sided argument -- about where things are headed next: Our broadest models (both ensembles and probit models) continue to imply a probability of oncoming recession near 100%. It's important to recognize, though, that there is such a uniformity of recession warnings here (in ECRI head Lakshman Achuthan's words, a "contagion") that even an unsophisticated, unweighted average of evidence indicates a very high likelihood of recession. The following chart presents an unweighted average of 20 binary (1/0) recession flags we follow (e.g. credit spreads widening versus 6 months earlier, S&P 500 lower than 6 months earlier, PMI below 54, ECRI weekly leading index below -5, consumer confidence more than 20 points below its 12-month average, etc, etc). The black brackets represent official recessions. The simple fact is that we've never seen a plurality (>50%) of these measures unfavorable except during or immediately prior to U.S. recessions. Maybe this time is different? We hope so, but we certainly wouldn't invest on that hope.

If Europe is in a recession, how about the U.S.? - My best guess is the U.S. stays out of recession even if Europe is currently in a recession. Of course there are significant downside risks, especially if there is a disorderly end to the euro. If we look at the channels of contagion, it seems the impact from Europe – barring a blow-up – will be fairly small. Of course, with sluggish growth, the U.S. is very susceptible to economic shocks, and it also appears that the U.S. is moving to more austerity in 2012 – and that is an additional concern (If Congress does nothing, taxes will increase on working Americans, and more). What are the channels of contagion from Europe? First, the trade channel – the impact on U.S. exports – is pretty small. Although Europe is a major trading partner, exports only make up a small portion of U.S. GDP. Some of the impact from trade would probably be offset by lower oil prices – and of course lower interest rates as investors seek safety (the European crisis is a key reason the U.S. 10 year bond yield is around 2%). A more significant channel would be tightening of U.S. credit conditions in response to the European crisis.The Fed’s October Senior Loan Officer Opinion Survey on Bank Lending Practices showed “considerable” tightening on lending to European banks, and some tightening to European firms, but the survey showed no tightening in the U.S.

If Rome burns, US will feel the heat --The financial fires raging in Europe threatened to consume Italy Monday, as investors fled the country’s debt, driving up borrowing costs and pressuring Premier Silvio Berlusconi to resign. Unless those fires can be contained, the U.S. and the rest of the world will soon feel the heat. After multiple failed attempts by Berlusconi’s government to reform Italy’s debt-heavy budget and after weekend reports that the government may fall, the financial markets pummeled Italian bonds Monday morning, sending interest rates approaching 7 percent. At those rates, the cost of periodically rolling over Italy’s $2.6 trillion in outstanding debt would quickly swamp its already strained budget. Nearly two years after similar broken reform promises by Greece, the epicenter of the current financial crisis, the widening turmoil poses a much bigger threat. "Italy has much more systemic implications than Greece, its debt is larger than the rest of the periphery put together, it is too big to fail, too big to save,” . To cope with losses expected on Greek debt, European officials are in talks to expand a $320 billion bailout fund to shore up European banks or buy Greek bonds outright. Some analysts have warned that European banks don’t have enough capital to withstand losses on their holdings of Greek debt. A default by Italy, the world’s third largest issuer of government debt behind the U.S. and Japan, would dwarf those losses and swamp even an expanded bailout fund.

The Blooey Factor - Paul Krugman - A thought before tomorrow’s markets open in Europe: might we be seeing Italy go careening off the edge in the next few days? I mean, even more than it has? The FT suggests that we might, writing of a “danger zone”. I’m trying to think about this, so a few observations. First, there is a potential vicious circle in which higher rates raise Italy’s interest burden and push the country into defaulting. This is real; the question is how quickly it can operate given the fairly long maturity of Italian debt. Second, there is the question the FT raises, about whether rising spreads will trigger an increase in required margins. I think of as Shleifer-Vishny, after their classic paper on the limits of arbitrage (pdf). Their point was that a fall in the price of some asset, even if it should in principle present a buying opportunity if the fundamentals haven’t changed, may actually be self-reinforcing instead if there is a limited class of leveraged investors who buy that asset. Most Italian debt may be held by stolid domestic players, but at the margin are financial institutions that are quite possibly going to be forced to cut their holdings if Italian interest rates rise, because this will reduce the value of the bonds they already hold. So things could quite possibly go blooey in the very near future.

Who is Screwing Up More: Europe or the US? - In both Europe and the United States, the current public debt woes are attributable to mistakes made by political leaders going back more than a decade. In both cases the tremendous magnitude of the long-term debt problems has only become evident for all to see recently, by which time it was too late for the straightforward policy solutions that were viable options previously. It is hard to judge whether it is Europe or the United States that has screwed up worse. On the one hand, Europe is now much closer to full-fledged crisis: the debt problems in Mediterranean members are virtually insoluble at current interest rates, are probably pushing Europe back into recession, and could well soon result in one or more countries forced to leave the euro. By contrast, there is no true fiscal crisis here yet; the world’s investors are still buying large quantities of US bonds at low interest rates. On the other hand, the mistakes by US politicians are more gratuitously self-inflicted than on the other side of the Atlantic. In 2001, all we had to do was continue the fiscal progress that had been made during the 1990s: preserve the budget surplus and move on to address the longer term problems of social security and Medicare in a deliberate and balanced manner. Instead we recklessly enacted massive tax cuts and tripled the rate of growth of federal spending, in ways guaranteed to generate serious fiscal troubles in the decade of the 2010s and beyond.

Treasuries Rise as Italy Deposit Requirement Spurs Refuge Demand - Treasury 10-year note yields fell the most in a week on concern Italy will join Greece in struggling to form a regime strong enough to implement austerity measures following the resignation of Prime Minister Silvio Berlusconi. Italian debt securities slumped, driving five- and 10-year yields to more than 7 percent for the first time since the euro was introduced in 1999, even as the European Central Bank was said to be buying the nation’s debt. U.S. 10-year notes rallied before today’s $24 billion sale of the securities. The $32 billion auction of three-year notes yesterday attracted the highest demand since at least 1993. “It’s another tempest ripping through the peripheral market, and people are now concerned because this is one of the bigger dominos they’ve been trying to keep propped up,”

The money scoreboard - MMTers like to say that money is like points and the government is just a scorekeeper. I have never really liked that analogy because the money unit of account is not just about keeping score it is also a government IOU. Nevertheless, the scorekeeper/point analogy has some utility in terms of our institutional arrangements. So I am going to try to use it here. The amount of money or credit in the system does not change the productive capacity of a society at one point in time. A country can produce whatever it can produce based on the available physical and human capital. As Andy Xie noted money contracts introduce a distribution problem, but they do not change the inherent productive capacity of a society. So money is the way that we measure that productive capacity and set prices for wages, consumer goods and services and assets. In most monetary systems including in the euro zone, government has been tasked with setting the currency unit of account to make that measurement. If we were to simultaneously increase the price level of wages, consumer goods and services and assets by 1000-fold, all that we have done is change the nominal amounts, not the actual capacity to produce. The ‘points’, as MMTers would call them, are now worth one one thousandth in productive capacity of what they previously were.

The Argument Against the "First Derivative Mistake" Excuse - Unless you're really stupid, or bending over backwards to find excuses for the Obama Administration's Geithnerian malfeasance, you should be less than impressed with Matt Yglesias's attempt to argue that the Administration saw reason to be happy with overall employment (link to Brad DeLong). If you're Matt Yglesias, you should be even less impressed with your (own) argument. Because Matt Yglesias was paying attention in 2010. He was paying much more attention to Barack Obama's speeches than I was, so he would have heard the 27 January 2010 State of the Union, when Barack Obama said: Our efforts to prevent a second depression have added another $1 trillion to our national debt. . But families across the country are tightening their belts and making tough decisions. The federal government should do the same. (Applause.) So tonight, I'm proposing specific steps to pay for the trillion dollars that it took to rescue the economy last year. Starting in 2011, we are prepared to freeze government spending for three years. (Applause.) And Matt Yglesias, who was paying attention then and has a memory now, would have known that "freezing government spending in 2011" means starting 1 October 2010 (when FY 2011 starts). And Matt Yglesias—not to mention Brad DeLong—would not be at all surprised when the result of those early 2010 policies came home to roost:

Federal Budget Deficit for Fiscal Year 2011: $1.3 Trillion - CBO Director's Blog - Last month, the Treasury Department reported that the federal government incurred a budget deficit of $1.3 trillion for fiscal year 2011, almost identical to the deficit it incurred in 2010. As a share of the nation’s gross domestic product (GDP), the deficit declined slightly—from 9.0 percent in 2010 to 8.7 percent in 2011—but nonetheless it was the third-highest deficit as a share of GDP since 1945. As discussed in CBO’s latest Monthly Budget Review, the deficit in 2011 would have been about $140 billion less than that in 2010 except for three unusual factors: (1) Certain payments that would have been made on October 1, 2011 (that is, in fiscal year 2012) were made in September 2011 because October 1 fell on a weekend; (2) net outlays for deposit insurance were reduced in fiscal year 2010 and increased in 2011 because banks were required prepay about three years’ worth of deposit insurance premiums in December 2009; and (3) the estimated costs of certain credit transactions made in earlier years were revised downward by a large amount in 2010 and by a much smaller amount in 2011. Excluding those factors, the deficit would have declined because outlays would have been almost unchanged from 2010 to 2011, while receipts rose by $141 billion.

Federal Borrowing Mounts While Household Debt Shrinks - The sharp rise in federal borrowing is overwhelming efforts of consumers to reduce debt, leaving the economy deeper in debt than when the recession began in December 2007, a USA TODAY analysis finds. The substitution of government debt for consumer debt helped end the recession and start a recovery, economists say, but it leaves the nation's long-term economic health in peril. Households have reduced debt by $549 billion since 2007, mostly by cutting mortgages through defaults and paying down credit cards. During that time, the federal government has added more than $4 trillion in debt, pushing the country's total borrowing to a record $36.5 trillion, excluding the financial industry, according to the Federal Reserve. "Government will eventually need to reduce the deficit," says Susan Lund, research director at McKinsey Global Institute. "But it's a very difficult balancing act to avoid withdrawing stimulus too soon while stopping before you borrow too much."

The Debt Ceiling as a Fiscal Rule - NY Fed - A few months ago, the federal government was once again confronted with the need to raise the statutory limit on the amount of debt issued by the Treasury. As in the past, the protracted stalemate and associated uncertainty led to calls to eliminate the debt ceiling. In this post, I make the counterargument. Likely because of its straightforwardness, the debt ceiling has been an effective “fiscal rule.” The reduction of the federal deficit from the mid-1980s to the mid-1990s was due in large part to a series of budget compromises, all of which were accompanied by the need to raise the debt ceiling.

Swelling Government Balance Sheets - Brad has a nice memo on why expanding the government balance sheet is a good idea during a financial crisis. Because of the financial crisis, the private capital market is not functioning as well. Until risks return to normal, the economy should do less intermediation through and financing of private borrowers. It should do more of something else. What is the something else? Well, a credit-worthy government is a perfectly good borrower and a perfectly good financer of economic activity. Its debt is a perfectly good way of transferring wealth from the present in the future—a way is exposed to none of the added risk generated by the financial crisis. The natural conclusion: if finance was at the appropriate balance between private and public borrowing before the financial crisis, we should have less private and more government financing afterwards—even without all the Keynesian and monetarist reasons for expansionary policy in a downturn. For those who are too afraid of government spending to even contemplate raising it ever for any reason, note that all that is necessary is that the government expand its balance sheet. As I have said before, in the extreme, if you look at the numbers the US government could simply suspend the collection of taxes until further notice. Not only would this have the affect of rapidly expanding the outstanding stock of debt but it would serve as an incredible incentive to bring economic transactions forward in time.

Year-end budget busters: $600 billion on the line -- Debt reduction may be consuming Capitol Hill these days, but lawmakers have a number of pricey budget decisions to make before the year's out. Unless Congress steps in, come January payments to Medicare1 doctors will be slashed by nearly 30%. Workers' payroll tax cut2 will expire. And federal unemployment benefits will end for close to 2 million jobless workers. Should lawmakers decide to prevent all that from happening, as many would like, there's the question of how to pay for it with the current budget. The estimated price tag for all three provisions over 10 years would top $600 billion. In September, President Obama proposed extending and expanding3 a temporary payroll tax break from last December. While employees normally pay 6.2% on the first $106,800 of their wages into Social Security, this year they've only been paying 4.2%. That tax break, however, is set to expire by Jan. 1. Obama proposed extending it for another year and cutting the employee share to just 3.1%. He also proposed cutting the employer's portion -- also 6.2% -- in half on the first $5 million that the company pays in wages. The payroll tax proposals combined would mean $289 billion less in revenue, according to the Congressional Budget Office. The hit would be taken by the general revenue pool, however, not the Social Security trust fund.

On Potential Deals in the Super-Committee - Political scientists Regina Smyth and William Bianco have written a pithy and interesting analysis of the sorts of deals that might emerge from the Super-Committee and, perhaps more importantly, the kinds of side-payments that party leaders might have to make if one of those deals is to win enough support in each chamber. Here is their analysis. Here is short excerpt: Our analysis shows that many different deals can emerge from bargaining among SC members. But if negotiations center on deals that are enactable in the House or Senate, then only two kinds of deals are plausible. The first is a deal in which the House leadership is able to use its influence to accommodate the preferences of moderate Senate Democrats. This outcome is most likely in the case that House Republican leadership perceives the political cost of the reversion point as just too high with election a year away, and expects that the blame for a failure to cut the deficit will fall squarely on House Republican incumbents. However, this possibility becomes unlikely insofar as schemes to avoid defense cuts emerge. Conversely, if political costs are thought to be small, and bargaining is driven by policy concerns, then the pressure of the reversion mechanisms is likely to force House and Senate Democrats to agree to a deal that gives House Republicans most of what they want.

Supercommittee Deadline: Sooner Than You Think - Time may be even shorter for Congress’s deficit-cutting supercommittee than generally thought. The committee has until Nov. 23 to approve a recommendation for cutting the deficit by $1.2 trillion, or automatic spending cuts would kick in starting in January 2013. A simple majority of the 12 members would suffice to send the proposal to Congress. But the Nov. 23 deadline could be misleading. The Congressional Budget Office must provide an official estimate of how much the plan would cut the deficit before the committee members can vote on it. How long that would take depends on how novel the proposal is. If it consists of ideas that have been long-discussed and the CBO has already evaluated, the agency’s estimate may only take a few days. If it contains newer ideas, it could take longer. There’s yet another catch. The law creating the supercommittee, the Budget Control Act, says committee members must have 48 hours to look at any proposal before voting on it. That means the CBO must evaluate, or “score,” the proposal by Nov. 21—just 12 days from now.

What I Said On Bloomberg TV This Morning About The Not-So-Super Committee - Stan Collender - Please forgive the short commercial you have to watch before the interview begins.

Super Committee May Be The Real Turkey This Thanksgiving - Stan Collender - I predicted two things in the Sept. 6 Fiscal Fitness — the first published after the Budget Control Act was signed into law this past Aug. 2 — that are coming true faster than I, even on my most cynical days, would have dared to forecast. I say this not to be smug but rather with great sadness. First, I predicted that the across-the-board spending cuts “that are supposed to happen in January 2013 if the Joint Committee on Deficit Reduction can’t agree on anything or if what it proposes isn’t enacted have to be considered especially vulnerable to changes.” As the long-expected deadlock in the anything-but-super committee actually comes ever-closer to being realized, serious efforts are under way to prevent the across-the-board spending cuts from being triggered and to make sure the Pentagon isn’t included if they happen. Second, I said “like all the budget deals that have come before it, this one is already on the skids even if it’s not immediately obvious.” A separate analysis I wrote at that same time predicted that this agreement might not last until Christmas.

Why The Super Committee Is Heading For Super Catastrophe - As of Tuesday morning, betting on the Super Committee to succeed would be playing the odds. A key member of the Senate Democratic leadership team has openly predicted the panel will gridlock and fail, and placed the blame squarely on Republicans. As GOP committee members met privately, Maryland Rep. Chris Van Hollen — a Democrat on the panel — told Bloomberg, “You need to close some of these tax loopholes and you need to generate additional revenue. And so that balance is going to be important. We saw the dueling letters just last week. We had a bipartisan group in the House that said, ‘Look, everything is on the table including revenues - tax revenues.’ And within 24 hours you had 33 [Republican] Senators say, ‘no new net tax revenues.’” Republicans responded with a trial balloon, . “One positive development on taxes taking shape is a deal that could include limiting tax deductions, perhaps by capping write-offs on charities, state and local taxes, and mortgage interest payments as a percentage of each tax filer’s gross income,” he wrote. “In exchange, Democrats would agree to make the Bush income-tax cuts permanent. This would mean preventing top rates from going to 42% from 35% today, and keeping the capital gains and dividend tax rate at 15%, as opposed to plans to raise them to 23.8% or higher after 2013.”

Dems rebuff GOP tax proposal as 'insane' - Republicans say the new revenue would come from limits on itemized tax deductions. The money captured from the tax overhaul would be used to lower the top individual tax rate to 28 percent and toward deficit reduction, aides say. Republicans also want to make the Bush tax cuts permanent. The breakdown, according to aides: $250 billion from limits on itemized tax deductions, such as the mortgage interest deduction on second homes, and about $40 billion in money the government would save by changing the way it calculates who qualifies for government benefits ("chained CPI"). Until now, Republicans have proposed only non-tax related revenue measures such as spectrum sales and increases in FAA fees. As headlines started to trickle out today that Republicans were offering a tax increase proposal to break the supercommittee impasse, Democrats on the committee hit back hard. Kerry told reporters this afternoon he saw a slight change from Republicans but it wasn't nearly enough. "They're anxious to promote a certain concept with all of you. But I'll be very clear that whatever they've put there doesn't get the job done. We've got some distance to travel. We're working very hard to do that. I dont want to go into the details," he said.

Supercommittee Makes Little Progress Amid Sniping - Democrats and Republicans on the congressional supercommittee appeared to make little progress Wednesday toward a deficit-cutting package, instead accusing each other privately of not negotiating in good faith. The two parties each made offers this week that were quickly rejected by the other side. A Democratic plan would raise $1 billion in revenue and cut $1 billion in spending, with much of the revenue coming from changes in the tax code. The GOP plan would cut spending by $700 billion and raise revenue by $500 billion, while cutting taxes dramatically. It would generate some of the revenue by capping deductions that taxpayers can claim on their returns. A Democratic staff analysis says that plan would lower taxes dramatically for the wealthy while raising them for everyone else. Republicans say they’d be willing to retool the plan to address some of these concerns.

Wall Street Doesn't Seem To be Expecting Much From The Not-So-Super Committee - One of the factors that has been leading some to predict that the Joint Select Committee on Deficit Reduction (aka, the super committee) will come up with a deficit reduction plan of its own is the belief that Wall Street will be disappointed if that doesn't happen and that the major averages will suffer immediately and significantly. But while there is some reason to think this could happen (after all, Bank of America Merrill Lynch predicted it several week's ago), the counter argument that Wall Street isn't really expecting much, won't be all that surprised if/when the committee fails, and that the the prediction of a massive negative market reaction is grossly overstated seems to be getting much stronger as the November 23 deadline gets every closer.In a research note released 10 days ago at Moody's Investors Service (sorry, subscription) is one of the major reasons this "it-won't-be-a-big-deal-at-all-if-the-super-committee-fails" attitude is increasing taking hold. According to the comment, investors won't care if the committee doesn't agree in a deficit reduction plan or if its plan isn't agreed to by Congress because of the $1.2 trillion in additional spending cuts that failure would trigger.

My Two Cents (But Worth Trillions of Dollars) to the Super Committee - So, hey!–It’s 11/11/11, and we’re down to not much more than 11 days (ok, darn–it’s technically 12) until the Nov. 23 deadline for the “super committee” to come up with proposals that would achieve $1.5 trillion in deficit reduction–or as close to that while hopefully going over as possible. The confusion on the goal is because the conditions for the triggered automatic cuts and debt limit increases differ depending on whether $1.5 trillion, $1.2 trillion, or less than $1.2 trillion in deficit-reducing policies are actually enacted by December 23. The graphic above is a Concord Coalition slide from one of our chart talks; it is designed to help explain the goals and triggers of the super committee, although it isn’t as readable as a photo image here as it is as a huge powerpoint chart up on a big screen–sorry.

Supercommittee Failure Could Throttle Holiday Spending - Consumers are starting to feel a bit more confident about the economy, according to the latest Thomson Reuters/University of Michigan consumer sentiment index out today. But a cloud forming over Washington threatens to darken the mood. The congressional “Supercommittee” formed as part of the debt-ceiling deal this summer is working to meet a Nov. 23 deadline for submitting a report on how to trim the deficit. The plan—assuming the bipartisan panel reaches a deal—will include at least $1.2 trillion in deficit reduction, expected to be a combination of revenue generators (read: tax increases) and spending cuts. If a deal doesn’t materialize—or if Congress rejects the committee’s recommended measures–a set of automatic spending cuts will go into effect. With less than two weeks to go, there’s no sign of a deal. Economists warn that a failure to produce a comprehensive deficit-reduction plan would further erode the public’s confidence in Washington lawmakers and consumer sentiment, already at very low levels.

Super Dupes - With the Congressional Super Committee required to produce a bipartisan budget-cutting plan by November 23, the best possible outcome would be for the committee to collapse of its own weight. With no deal, automatic cuts would kick in beginning in 2013. Those budget cuts would be excessive, but that question could—and will—be reopened after the election. And in the meantime, $4 trillion in Bush tax cuts will expire, solving most of the deficit problem. If Democrats win, it’s all up for grabs. If Republicans win, the cuts will be even deeper. The 2012 election will be a referendum on whether we want growth or austerity, and whether we want tax fairness. For now, the six Republicans on the Super Committee, predictably, want all of the budget savings to be on the spending side and are adamantly opposed to any tax increases. On Thursday, 33 Senate Republicans sent a letter to their colleagues on the committee warning them not to support any form of tax increase. What’s bizarre, however, is how bad the Democrats’ proposals are. Erskine Bowles, the investment banker and nominal Democrat on the late Bowles-Simpson Commission, testifying before the committee Tuesday, proposed $600 billion in Medicare and Medicaid cuts, deeper cuts even than those in Speaker John Boehner’s final offer to President Obama just before the bipartisan budget deal collapsed last summer.

The Story of Broke - When filmmaker and activist Annie Leonard set out in 2007 to share what she’d learned about the way we make, use and discard "Stuff," she thought 50,000 hits would be a great audience for her "20-minute cartoon about trash." Today, with over 15 million views and counting, The Story of Stuff is one of the most watched environmental videos of all-time. Earlier this year, Leonard came out with The Story of Citizens United, the best short history of the growth of corporate power I've ever read, heard or seen. Now, Leonard is back with The Story of Broke, a new 8-minute animated movie that directly challenges those who argue that America is penniless and incapable of paying its bills, let alone making investments in a more sustainable and fair economy. Released seemingly in perfect harmony with the growth of the Occupy movement, this film explains why the economic crisis we find ourselves in is the result of choices made and how we, the public, can force different decisions. “It turns out this whole “broke” story hides a much bigger story—a story of some really dumb choices being made for us, but that actually work against us,” said Leonard. “The good news is that these are choices, and we can make different ones.”

Deficit Cuts Should Be Linked to Unemployment - Robert Reich - On planet Washington, where reducing the federal budget deficit continues to be more important than creating jobs, everyone is talking about “triggers” that automatically go into effect if certain other things don’t happen. The biggest trigger on the minds of Washington insiders is $1.2 trillion across-the-board cuts that will automatically occur if Congress’s supercommittee doesn’t come up with at least $1.2 trillion of cuts on its own that Congress agrees to by December 23. That automatic trigger seems likelier by the day because at this point the odds of an agreement are roughly zero. Here’s the truly insane thing: The triggered cuts start in 2013, a little over a year from now. Yet no one in their right mind believes unemployment will be lower than 8 percent by then. The cuts will come on top of the expiration of extended unemployment benefits, the end of a payroll tax cut, and continuing reductions in state and local budgets — all when American consumers (whose spending is 70 percent of the economy) will still be reeling from declining jobs and wages and plunging home prices. In other words, what will really be triggered is a deeper recession and higher unemployment.

Will Americans be Allowed to Vote on Supercommittee Austerity Plan? - Congress' "supercommittee" of the 1% is preparing an austerity plan for the 99%. Will We, the People be allowed to vote on this plan, or, like Greece, will the elites just tell us how it is going to be? Our deficits were caused by tax cuts for the rich and huge increases in military spending. But instead of addressing these causes the elite supercommittee is said to be preparing to take money out of the economy by cutting the things We, the People do for each other. That's right, at the very time when 99% of us need more we will get less so that the 1% can enjoy record-low tax rates -- and it looks like We, the People will have no say in it. Last week Greek Prime Minister George Papandreou proposed a referendum on the austerity plan that European governments are preparing for the country. "The markets" -- another name for the 1% -- went berserk in reaction. Pressure was applied, and now the Greek people will not be allowed to vote on their austerity plan after all, they will just be told. So, will We, the People be allowed to have a say over this austerity plan, or will it be like Greece all over again, told by the 1% how it's gonna be?

The Secret Farm Bill - The Republican-manufactured budget crisis of this past summer — remember? — resulted in a “solution” that’s hijacking what little representative democratic process we have left. Equally sad is that the so-called supercommittee — charged with creating an outline for reducing the deficit by $1.2 trillion over 10 years — may preclude full discussion of the farm bill. It’s the farm bill that largely shapes food and agriculture policy, and — though much of it finances good programs — ultimately supports the cynical, profit-at-any-cost food system that drives obesity, astronomical health care costs, ethanol-driven agriculture and more, creating further deficits while punishing the environment. The farm bill is written every five years. Although the current one doesn’t expire until September, the next one may be all but wrapped up by your first bite of turkey, because the leaders of the House and Senate agriculture committees — a group of four, representing Oklahoma, Michigan, Minnesota and Kansas (do you see a pattern here?) — are working feverishly to draw up a proposal in time to submit it to the supercommittee before the Nov. 23 deadline.

Tax Break for Hiring Jobless Veterans Heads Toward Passage - It looks like one plank of President Barack Obama’s jobs bill might actually pass Congress: a tax break for companies that hire unemployed veterans.It could be that the parties are feeling pressure to actually produce something. It might be that it’s hard to vote against measures that help veterans. And, it may be that the measure’s cost is so modest that higher taxes aren’t required to pay for it. The bill will also offer a variety of other provisions aimed at helping veterans in the workplace, for a total cost of about $1 billion. A version of the bill has already passed the House, and Senate leadership aides in both parties expect a slightly different version to clear the Senate this week. Tucked into the package will be the Obama tax credits, estimated to cost just $120 million over two years. It all will be paid for by extending a soon-to-expire mortgage fee charged by a housing program run by the Veterans Administration. A vote is planned for Thursday.

An unbridged divide takes its toll - Yet it would be hard to argue that Congress does not deserve it (the disdain rather than the immolation). Its approval rating recently fell to a record low of 9 per cent, which means support has shrunk to “blood relatives and paid staffers”, as a much safer joke goes. It seems that, every few days, America’s first branch of government does something to put off even its hardiest of apologists. Last week’s Senate decision to kill a modest $60bn bill to upgrade America’s infrastructure before it came to debate may have exceeded even that august chamber’s recent record. The package, which included $10bn in seed money for a public infrastructure bank, was blocked by every Republican and two Democrats. They objected because it would have been funded by a 0.7 per cent surtax on earnings over $1m. And that was that. At a time when US businesses prefer to hoard rather than invest their cash, and when long-term interest rates are so low the money is virtually free, the political system is unable to accomplish what ought to be a no-brainer. Until now, America has never faced an ideological divide on infrastructure: both parties accepted the need to upgrade roads, dams, bridges, energy and water systems.

Shovel ready - Some infrastructure spending is more stimulative than others.Yoshiyasu Ono of Osaka University had an interesting article in the Journal of Money, Credit and Banking this June on The Keynesian Multiplier Effect Reconsidered. In it he analyzes the special case of government spending on projects that are literally useless, such as paying people to dig a hole in the ground and then fill it back up. Although that's not proposed as an accurate characterization of any actual government programs, the extreme case of literally useless spending helps shed light on some of the issues involved. According to traditional Keynesian models, even for the case of a completely useless government project, if we were to raise private-sector taxes by just the amount needed to pay the salaries of the hole-diggers, GDP would increase, with a balanced-budget multiplier of one. Yet, Professor Ono asks, how could paying the crew a salary to dig a useless hole possibly lead to an improvement in welfare relative to simply handing them a direct transfer and allowing them to spend more time safely and comfortably at home with the family? And, to make things very simple, if the source of funds for paying the workers was in fact a tax levied on those same individuals, how could we possibly conclude that the enterprise has increased total national income?

Turning Our Backs on the Unemployed - Senators, Republicans and two Democrats in particular, have not received anywhere near enough criticism for this: Last week’s Senate decision to kill a modest $60bn bill to upgrade America’s infrastructure before it came to debate may have exceeded even that august chamber’s recent record. The package, which included $10bn in seed money for a public infrastructure bank, was blocked by every Republican and two Democrats. They objected because it would have been funded by a 0.7 per cent surtax on earnings over $1m. And that was that. At a time when US businesses prefer to hoard rather than invest their cash, and when long-term interest rates are so low the money is virtually free, the political system is unable to accomplish what ought to be a no-brainer. Until now, America has never faced an ideological divide on infrastructure: both parties accepted the need to upgrade roads, dams, bridges, energy and water systems.

Infrastructure gamesmanship puts wealthy ahead of jobs, good bridges, and country – Linda Beale -For those who are paying attention to the House and Senate these days, it seems like a frustrating exercise. Mostly it is one of watching the "do-nothing" Republicans find excuses for never requiring millionaires and billionaires to pay their fair share of taxes while making up excuses for not doing anything of the varied real approaches to stimulating the economy in ways that will create jobs for ordinary Americans. Take the vote on the infrastructure bills. The Senate leadership asked the Senate to vote for funding $60 billion of much needed infrastructure projects (just a tip of the iceberg of everything that is needed to bring this country's infrastructure into nonembarassment). The GOP refused, because it was funded by a de minimis tax on millionaires. There's no end to things that can be said about this further evidence of the craven state of the GOP in the US today. Political advantage for the wealthy class is to be given primary importance, no matter what happens to the vast majority of Americans and the country we all love. Jim Maule has it right, in The Tax and Spending Stalemate: Can It Destroy the Nation?, When partisan loyalties mean more than the nation’s well-being, when money means more to wealthy “world citizens” than does the long-term physical security of the nation, and when protection of millionaires who fund campaign treasure chests means more than the lives and safety of the rest of America, the literal physical survival of the nation is imperiled. ...

Bridge our divide by building bridges – Liberals and conservatives agree on little these days, and in the matter of the federal budget, virtually nothing. Recently, however, people from opposite sides of the aisle — the two of us — thought we had found an exception. Our nation's infrastructure is in tatters. The American Society of Civil Engineers7has identified $2.2 trillion8 worth of repairs needed on bridges, roads, dams, schools and water and sewage systems. And that's just overdue maintenance, never mind addition or replacement. Be it stimulus to the good, or deficit to the ill, the case for undertaking these projects immediately is compelling. Postponement is dangerous and expensive. Falling bridges, crumbling roads, bursting dams, moldy schools, contaminated water and leaking sewage are on no one's agenda for cutting government costs or increasing government benefits. And to delay infrastructure expenditure is to inflate it. For example, take a badly worn stretch of Interstate 80 in Nevada. The state's Department of Transportation9 says fixing it today would cost $6 million, but waiting two years would cause the roadbed to be so degraded by traffic and weather that the price would rise fivefold, to $30 million.

The real reasons Americans distrust government - What if distrust of government is running so high partly because Congress is failing to pass job creation policies, including tax increases on the rich, that have broad public support, and has prioritized the deficit for months when Americans want the top priority to be unemployment? If so, it’s hard to see how this supports the conservative storyline. National Journal has now released a fascinating new poll that sheds new light on this possibility: It finds solid support for Democratic ideas on the economy but also high public pessimism that those ideas will be implemented. Solid majorities want Congress to pass new federal spending on infrastructure and schools; deficit reduction through a combination of tax increases on the rich and spending cuts; and new legislation to make mortgage refinancing easier. By contrast, only minorities favor deficit reduction with just cuts to federal programs, including entitlements. But here’s the real rub. Only 27 percent think infrastructure spending will ... actually happen. Only 37 percent think deficit reduction through spending cuts and tax hikes will ... actually happen. Only 39 percent think legislation to make mortage refinancing easier will ... actually happen.

Expansionary Contraction Theory Takes Another Hit - When it comes to cutting our way to prosperity, you can’t get there from here. Whether it’s here in the US, where stimulus is fading too soon, in the UK, where austerity measures have led to slower growth, or evidence from research by the IMF and others evaluating the early work on this idea: it doesn’t work. Most of this analysis, including an influential early paper by Perroti himself (w/Alesina), has been done through statistical modeling or taking averages over lots of economies over many time periods. But in an interesting new paper, Perotti takes a case study approach, which makes a lot of sense given the nuances in the historical record. The statistical work, for example, can mess up on causality grounds, like when an expansion is underway and fiscal tightening occurs—the models can misinterpret that as growth caused by fiscal tightening.

Keynes vs. Hayek: An Economics Debate - Was John Maynard Keynes correct, can government fix the mass unemployment generated by a financial slump? Or is that a dangerous delusion as argued by his arch critic, Friedrich von Hayek? Sir Harold Evans chairs this Oxford-style debate, which focuses on the publication of Nicholas Wapshott’s Keynes Hayek: The Clash That Defined Modern Economics.