U.S. Fed balance sheet shrinks in latest week (Reuters) - The U.S. Federal Reserve's balance sheet contracted slightly in the latest week, Fed data released on Thursday showed. The Fed's balance sheet stood at $2.91 trillion on Feb. 22, down from $2.92 trillion on Feb. 15. The Fed's holdings of Treasuries totaled $1.657 trillion as of Wednesday, Feb. 22, versus $1.667 trillion the previous week. The Fed's overnight direct loans to credit-worthy banks via its discount window averaged $4 million a day during the week versus $7 million a day previously. The Fed's ownership of mortgage bonds guaranteed by Fannie Mae, Freddie Mac and the Government National Mortgage Association (Ginnie Mae) was $853.05 billion versus $847.8 billion the previous week. The Fed's holdings of debt issued by Fannie Mae, Freddie Mac and the Federal Home Loan Bank system totaled $100.8 billion, versus $101.5 billion the prior week.

FRB: H.4.1 Release--Factors Affecting Reserve Balances -- February 23, 2012

Will the Central Bank Bailouts Ever End? - Guess which US bank holds assets equal to a fifth of US GDP. Now guess what percent of its assets have extremely long maturities, greater than ten years: a) 10%; b) 20%; c) 30%; d) 40%; e) 50%. Answer: The Fed, and e) 50% of its assets have ten years or more to maturity. Recap. The global financial crisis (GFC) began about four years ago. The Fed pulled out all the stops to save the biggest banks. As I discussed previously the Fed engaged in “deal-making” designed to protect creditors of failing banks, and used Section 13(3) to create Special Purpose Vehicles that engaged in legally questionable lending and asset purchases to save banks and shadow banks. Four years later, the Fed’s balance sheet is still humongous and it is even increasing its interventions in recent weeks through loans to foreign central banks. A recent speech by Herve Hannoun at the Bank for International Settlements, “Monetary policy in the crisis: testing the limits of monetary policy” (link below) shows that ramping up the role for central banks has taken place all over the world. Indeed, in emerging market economies, the central banks have assets equal to 40% of GDP. But the intervention by central banks during this GFC is entirely unprecedented–and is starting to worry most observers, who are asking when, or if, this will ever end.

Where Did All That Printed Money Go? - Normally when we think of printing money, we are talking about the Fed buying Treasuries, or some other securities from the Primary Dealers. The PDs then take the cash and buy Treasuries from the government. The Fed’s asset base is thereby increased, and an offsetting liability, bank reserves on the Fed’s balance sheet, also increases. The Fed’s been getting away with this kind of printing for a long time now, but there’s been some seepage of money into financial assets, driving prices of bonds to the stratosphere and triggering “beneficial” rallies in stocks, and more malevolent rallies in commodities, particularly crude oil, but “core” consumer prices have lain more or less dormant..But there’s another, different, type of “printing”, and this one is literal, honest-to-god printing! Dr. Bernankenstein wasn’t joking when he said the Fed had a printing press in the basement (cue evil laughter). The kind of “printing” I’m talking about is the actual printing of currency–cash, Benjamins et. al. Each week the district Fed banks usually print a total of a billion to several billion in cash, load it in armored trucks, and ship it out to the hinterlands, places like Staten Island, Cleveland, and Afghanistan. The cash shows up as a liability–Federal Reserve Notes–on the Fed’s balance sheet because cash. Also on the Liability side of the Fed’s balance sheet as reported weekly in the Fed’s H.4.1 statement are Treasury deposits, deposits by banks, also known as reserve deposits, reverse repos, Term Deposits of banks when the Fed offers them, and a mysterious category called Other deposits....

FRB: Press Release--Minutes of Board discount rate meeting on January 23, 2012 -- February 21, 2012: The Federal Reserve Board on Tuesday released the minutes of its discount rate meeting on January 23, 2012. The minutes are attached. Attachment (10 KB PDF)

When will the Fed hike rates? - TYLER COWEN points us to the blogger at Sober Look, who thinks markets aren't buying the Fed's low-rate communications:Misconceptions still persist that the Fed is on hold with respect to rates until at least late 2014. The markets would disagree. The Fed Funds futures have the first rate hike (25bp) centered around August of next year and the second hike (to 50bp) on July of 2014.... The market is fully ignoring the FOMC's prolonged zero rate forecast. If Bernanke tried to lower short-term rate expectations by the announcement, he failed miserably, as the rate expectations are now even higher than prior to the announcement. Why is the market pricing in higher short-term rates (an early rate hike)? The answer has to do with relatively strong economic data coming out of the US and rising commodity prices. All of this is driving up inflation expectations. The chart below shows TIPS implied 2-year forward inflation expectation now comfortably above 2%, the Fed's inflation target. This strikes me as mistaken in a few different ways. First, the market's expectations for the timing of rate hikes is almost perfectly consistent with the Fed's own projections. The language of the statement suggests the Federal Open Market Committee:

Dudley Sees Higher U.S. Interest Costs, Making Fiscal Repairs ‘Essential’ - Federal Reserve Bank of New York President William C. Dudley warned that interest costs on government debt will eventually increase as the central bank raises borrowing costs, and he said it is “essential” for the U.S. to start aiming for fiscal balance. “We are in an unusual period in which net interest expense is temporarily depressed,” he said. “This will not last and the fiscal authorities need to factor this in when considering what needs to be done to put the federal budget deficit and the nation’s debt burden on a sustainable path.” Dudley repeated last month’s statement by the Federal Open Market Committee that low rates of resource use and subdued inflation “are likely to warrant exceptionally low levels for the federal funds rate at least through late 2014.” He is a permanent voting member of the panel. “These unusually low interest rates are the result of monetary policy actions taken by the FOMC,” Dudley said in remarks prepared for the U.S. Monetary Policy Forum hosted by the University of Chicago Booth School of Business. “The sole purpose of these actions has been to promote the dual mandate objectives of maximum employment and price stability in the wake of the financial crisis.”

Why We Can't Believe the Fed - The Federal Reserve's interest rate-setting Open Market Committee recently broke new ground in Chairman Ben Bernanke's transparency campaign by proffering predictions of its own behavior over the next three years. This is a huge innovation for the Fed, which has never predicted economic data it directly controls. The idea was first to anchor market expectations that short-term rates will stay at historic lows, thereby encouraging investors and companies to move more aggressively into longer-term, riskier assets with higher expected returns—which the Fed hopes will fuel economic growth. But the Fed also set for itself a formal, long-run inflation target of 2%. If the Fed has a good handle on where the economy is heading over the next several years, then its pledges of extended low rates and a 2% inflation target imply little risk of its needing to change course and jar the markets. But how good is the Fed's actual track record on predicting the economy? The Fed studied its own staff's forecasting performance over the period 1986 to 2006. It found that the average root mean squared error—or the deviation from the actual result—for the staff's next-year gross domestic product (GDP) forecasts was 1.34, compared with 1.29 by what the Fed describes as a "large group" of private forecasters. That is, the Fed's predicting performance was worse than that of market-watchers outside the Fed. For next-year CPI forecasts, the error term was 1.03 for Fed staff, and only 0.93 for private forecasters. The Fed's conclusion? In its own words, its "historical forecast errors are large in economic terms."

Christina Romer: We Need A Regime Change at the Fed - Christina Romer does the Five Books interview and one of her recommended reads is a famous article by Peter Temin and Barry Wigmore titled "The End of One Big Deflation." Here is Romer discussing the implications of this article for today: What we learned from the Temin and Wigmore paper is that one way out of a recession at the zero lower bound is by changing expectations. To do that, often what is needed is a very strong change in policy – something economists call a “regime shift”. The most effective way to shake an economy out of a terrible downturn when we’re at the zero lower bound is an aggressive change in policy that makes people wake up, say “this is a new day” and change their expectations. What the Fed has done since early 2009 is much more of an incremental change. In other words, the Fed has failed to appropriately manage expectations and so we are stuck in a slump. So what would in the current environment rise to the level of a "regime shift"? What would change expectations enough to catalyze a broad-based recovery in aggregate demand? Here is Romer's answer: I think that what the Fed needs instead is a regime shift. A number of economists have suggested that the Fed adopt a new framework for monetary policy, like targeting a path for nominal GDP. Pledging to get back to the pre-crisis path for nominal GDP would commit the Fed to much more aggressive policy. Such a strong change in the policy framework could have a dramatic effect on expectations, and hence on the behavior of consumers and businesses.

Bigger beast, thicker chains - ECONOMISTS take central bank independence very seriously, and generally consider anything that undermines it bad policy. Its importance stems from the trade-off between the long-term and the short-term. The policies that generate temporary stimulus today can lead to uncertainty and reduced growth in the future. Politicians, with frequent election cycles, tend to be short-sided. Monetary policy can only balance the needs of the long- and the short-term when it’s not hostage to the political process. Independence also ensures that the central bank can act swiftly during financial crisis. But as John Cochrane points out, independent power must be limited: The price of independence is limited power. Central banks that only try to control inflation, and only using one tool, such as purchases and sales of Treasury debt, can be walled off from the political process. As a country, we can decide that the price level will not be used for political purposes and assign its maintenance to technocrats. Since the financial crisis the scope of the Fed’s regulatory duties have increased, and Mr Cochrane frets that this will ultimately undermine its independence.The more powerful it becomes, the more accountable it needs to be.

Republican House bill would strip US Fed's jobs mandate (Reuters) - Seeking to make good on past threats in Congress to rein in the Federal Reserve's powers, a prominent Republican lawmaker said on Thursday he will introduce legislation to focus the U.S. central bank on a single mandate to fight inflation and protect the dollar's value. Representative Kevin Brady, vice chairman of the Joint Economic Committee, said in a statement his "Sound Dollar Act" aims to "maintain the purchasing power of the dollar in order to foster long-term economic growth and stability." He plans to formally introduce it in early March. The Fed since the 1970s has had two mandates - to maintain stability and promote maximum employment - but the latter came under fire from some members of Congress after the Fed started buying hundreds of billions of dollars worth of Treasury and mortgage bonds to push down borrowing rates. Many Republicans have derided the so-called quantitative easing program as "printing money" and say it has devalued the dollar, driving up commodity prices and setting the stage for a nasty bout of future inflation.

Why Won’t The Federal Reserve Board Talk To Financial Reform Advocates? - Simon Johnson - The Federal Reserve has great power in modern American society, including the ability to move the economy and, at least indirectly, to create or destroy fortunes. Its powers operate in two ways: through control over monetary policy, meaning interest rates and credit conditions more broadly, and through its influence over how the financial system is regulated generally and how specific large banks are treated. The secrecy of our central bank has long been a source of controversy. In line with changes at central banks in other countries over recent decades, the Fed’s chairman, Ben Bernanke, has pushed for more transparency regarding how individual members of the Federal Open Market Committee view the economy – and thus how they are thinking about the future course of interest rates (and the Fed keeps us posted). This is a commendable change, helping people throughout the economy understand what the Fed is trying to do and why. Under pressure from both left and right – for example, in the unlikely alliance of Senator Bernie Sanders of Vermont and Representative Ron Paul of Texas – the Fed has also, after the fact, disclosed more of its actions during the recent financial crisis. But in terms of its process for determining financial-sector regulation, the Federal Reserve – at least at the level of the Board of Governors in Washington – is moving in the wrong direction.

New York Fed Said to Plan Sale of AIG-Linked Mortgage Bonds - The Federal Reserve Bank of New York is seeking bids for more of the mortgage bonds assumed in the government rescue of American International Group Inc. as prices on the debt rally, two people with knowledge of the plan said. After it was approached by a potential buyer, the New York Fed may sell the remaining assets in its Maiden Lane II LLC vehicle, totaling about $6 billion in face value, said the people, who asked not to be identified because the deal is private. Maiden Lane II was created in 2008 to buy holdings that AIG handed the central bank in exchange for a cash injection.The New York Fed has used two previous sales this year totaling about $13 billion to retire its loan to Maiden Lane II. Those transactions were in response to unsolicited bids, after the New York Fed halted regular and more public auctions last year of about $10 billion that were blamed for damaging prices in credit markets. The latest sales haven’t curbed a rally in home-loan bonds.

More on the Output Gap - As I said, Bullard’s thinking on the output gap mirrors that of a lot folks. Tyler Cowen points to this from Sober Outlook. A key part of the post says This output gap, thought often taken for granted, may in fact be much smaller. Some recent work by Barclays Capital has already shown that the potential GDP (red line) is basically extrapolating the bubble of the pre-crisis era and is therefore unreliable. The CBO number crunchers wish to believe in their ability to compute the potential GDP of the US economy. The reality is that nobody knows how much output the US economy is truly capable of. But there are signs that the gap may now be below the CBO’s assertion. In one sense the paragraph is true. No one knows for sure exactly what you could get out of the US economy, especially if you want to get the highest value added production. This is part because its not completely clear what “highest valued added production” might even mean in thoroughly consistent way. However, it we take a step back and ask more or less how much could you squeeze out the US economy, in terms of easily recognizable production we could probably back of the envelope this without too, too much trouble.

NGDP Targeting News Roundup - Just when you thought interest in nominal GDP (NGDP) might be waning there is more, including some discussions of it from central bank officials.

-

First, Mark Carney, Governor of the Bank of Canada delivered a speech where he discussed what would be a monetary policy for all seasons. He had some nice things to say about NGDP targeting, but ultimately comes out in favor of flexible inflation targeting as the top choice.

-

Second, Renee Holtom of the Richmond Fed has a nice article examining the implications of the Fed tolerating higher inflation as a way to kick start a robust recovery. She discusses all the reasons for doing so, including a NGDP target..

-

Third, in what appears to be the latest convert to Market Monetarism, Jason Rave does a good review of NGDP targeting.

What is Money? - Nick Rowe says we should not think of money as a store of wealth: Money is what money does. There are two functions of money that define what is and what is not used as money: medium of exchange; and medium of account. That's it... We need to start worrying a lot more about how money works as a medium of exchange. We need to understand a lot better than we do how money works as a coordinating device in a decentralised economy. And we need to understand a lot better than we do how money can sometimes fail as a coordinating device. Because, outside a very simple economy, people can't barter their way back to full employment if the monetary exchange system fails. We need to stop thinking of money as a store of wealth, just like all the others. And let's start by changing the textbook definition of money, by deleting that bit about money being a store of wealth. I agree, but would add that we also need to start thinking about money at all levels of transactions. Most textbooks and many economists think of money assets at only the retail level (i.e. the M2 money supply). This crisis has taught us that institutional money assets--those assets like treasuries, commercial paper, and repos that facilitate transactions in the financial system--matter too. The bank run on the shadow banking system was a bank run using institutional money assets. If we really want to understand money and its implications for the economy we need to be thinking about these money assets too.

Updated Seasonal Factors Remove Much of the Volatility from 2011 Monthly CPI Data - 2011 was a roller coaster ride for U.S. consumer price inflation—or was it? If you went by the releases from the Bureau of Labor Statistics, monthly CPI inflation, stated as annual rates, bounced from over 6 percent in February, down to under -2 percent by June, and then back up over 6 percent in July. That made life hard for policy makers, forecasters, and anyone trying to use the CPI to index payments. It turns out, though, that inflation was not so volatile after all. As part of yesterday’s CPI report for January, the BLS released revised seasonal adjustment factors. When we apply the new adjustment factors to data for the last two years, as in the following chart, much of the month-to-month variation in inflation disappears. The smoothing of the June-to-July bounce in inflation is especially noticeable. The revision of seasonal adjustments does not affect year-on-year inflation. Meanwhile, the inflation report for January shows a modest upturn, as we would expect from other signs of a strengthening economy. The uptick of inflation is broadly based. The headline all-items CPI and the core CPI, which omits food and energy prices, both rose to a 2.4 percent annual rate, just above the Fed’s now-official inflation target. The Cleveland Fed’s 16 percent trimmed mean CPI also notched upward to a rate above 2 percent.

Is It Time to Start Worrying About Inflation Again? - People tend to forget about inflation during a recession, because it typically abates until a recovery gets under way. But now inflation appears to be coming back. Ignore the monthly numbers – they’re too volatile to be reliable. But Friday’s inflation report showed that consumer prices have risen 2.9% over the 12 months through the end of January. Moreover, there’s an even more worrying pattern if you look at the same measure at half-year intervals since the start of 2009. The series goes: minus 0.6%, minus 0.1%, 2.1%, 1.2%, 2.8%, 3.5%. With only one interruption, that trend shows inflation on the rise. Some commentators argue that inflation isn’t a problem yet for several reasons: First, the consumer price index typically gives higher inflation readings than some other measures. Second, the economy is still relatively weak and unemployment remains high. That means any short-term price increases are likely to die out rather than fueling a self-sustaining inflation spiral. And third, policymakers have to balance the risks of inflation against the need to keep the economic recovery going and reduce unemployment. As long as unemployment is above 7%, inflation is a lesser risk than slipping back into recession.

Weighing the risks to the inflation outlook: Two views - Atlanta Fed's macroblog - The Federal Reserve Bank of Atlanta's Survey of Business Inflation Expectations released earlier today showed a continuation of rather modest expectations for unit cost pressures over the coming 12 months. In February, our panel of firms reported a 1.9 percent average expected rise in unit costs over the coming year, still within the very narrow 1.8 percent to 2 percent range the group has been reporting over the past five months. That's the good news. Now for some (potentially) bad news. In a special question this month, we asked the panel to weigh in on their expectations for annual unit cost increases over the longer term—specifically, the next 5 to 10 years. The group's expectation was a percentage point higher, at 2.9 percent. The reason for the higher expectation for unit costs over the longer term can be seen in the following chart, which compares how the group assigns probabilities to unit cost changes over the next 12 months to how they judge these probabilities over the longer term. In both instances, the Atlanta Fed's Business Inflation Expectations panel of firms puts the greatest likelihood that unit costs will rise in the 1 percent to 3 percent range—in a range that matches the Federal Open Market Committee's longer-term inflation objective.

Atlanta Fed Survey Finds Long-Term Inflation Worry - Most Federal Reserve officials are fond of observing that even as they pursue a very aggressive and unprecedented monetary-policy path, their actions aren’t stirring up inflation. In doing so, they’re countering critics who worry the central bank has gone too far in efforts to stimulate growth, and that current policies are running a significant risk of generating a future surge in price pressures. Fed officials have countered they have the tools to make sure their actions don’t fuel a break out in prices. They also note the data doesn’t show much worry about future inflation gains. But a new survey of local businesses conducted by the Federal Reserve Bank of Atlanta, released Wednesday, suggests South-Eastern region business leaders may not share the Fed’s confidence about future inflation. The survey of 168 firms found an average expectation inflation would hang close to the Fed’s target at 1.9% over the next 12 months.The short run was not where the potential problem lies. Survey respondents predict inflation over the next five to 10 years to rise by 2.9%, a level that would problematic to the Fed. Of those who answered the question, the bias of regional companies clearly points to expectations that long term inflation risks are rising. Respondents said there was a 38% chance prices will rise between 1.1% to 3%, and a 29% chance of a gain between 3.1% and 5%. Those surveyed put a one in five chance on inflation rising by 5% or higher over the next five to 10 years.

Inflation: Life on the Phillips curve | The Economist - VIA Modeled Behavior, I see that Arnold Kling has written a post which reads: Mainstream macro in the 1970s (which a lot of people seem to have gone back to) held that there was a NAIRU, meaning the non-accelerating inflation rate of unemployment. If unemployment was above that, inflation would fall. If it was below that, inflation would increase. So, policy should shoot for the NAIRU. These days, unemployment is 8.3 percent, and inflation is increasing. Just sayin’. Just sayin'...what, exactly? Don't imply, man, argue! Follow the point through to its conclusion and see if it actually holds together! Mr Kling says that according to this theory a rate of unemployment below NAIRU will trigger an increase in inflation. He then observes that with 8.3% unemployment, inflation is increasing. And he deploys the just sayin' line to imply that the economy is therefore below NAIRU—that is, at structural full employment, suggesting that further demand stimulus is undesirable. He is wrong on multiple levels.

Restraining unit labour costs is a right-wing conspiracy - In an otherwise excellent post, Matt Yglesias commits one of the deadly sins of monetary policy: [M]y favorite indicator of inflation is “unit labor costs”… Unit labor costs are basically wages divided [by] productivity. It’s not the price of labor, in other words, but the price of labor output. If productivity is rising faster than wages, then even if wages themselves are rising unit labor costs are falling. Conversely, if wages rise faster than prodictivity than unit labor costs are going up. Clearly there’s nothing wrong with a little increase in unit labor costs here or there. But over the long term, growth in unit labor costs needs to be constrained or else it becomes impossible to employ anyone. And you can see that in the seventies it’s not just that gasoline got more expensive, we had an anomalous spate of high unit labor cost growth. That was inflation and it’s what led to the regime change that’s governed for the past thirty years. That all sounds reasonable. But Yglesias has fallen into a trap. Unit labor costs are not “basically wages divided [by] productivity”. That’s not the right definition at all. Unit labor costs are nominal wages per unit of output. An increase in unit labor costs can mean one of two things. It can reflect an increase in the price level — inflation — or it can reflect an increase in labor’s share of output. The Federal Reserve is properly in the business of restraining the price level. It has no business whatsoever tilting the scales in the division of income between labor and capital.

Debt and Regret: Inflation Edition - Mike Konczal posts a summary of a working paper by Mason and Jayadev. The leader: Changes in debt-income ratios can be attributed to primary borrowing, interest rates, growth, and inflation. In a new working paper, we apply such a decomposition to the evolution of U.S. household debt. This shows that changes in borrowing behavior has played a smaller role in the growth of household leverage than is widely believed. I think the authors are essentially correct – declines in inflation are the key driver behind high household indeptedness. What they are not as explicit about is that indeptedness is fundamentally a nominal phenomenon. Its always difficult for me to lucidly explain this even to myself but these two graphs should help. First, look at how household debt has grown. An almost inexorable rise since the early 1980s. Even now we are barely back to 2005 levels. Now compare that to debt service payments. Though by 1995 the level of debt-to-income had gone up by about 50%, debt service payments were almost as low as the through in the 1980s. And, today while debt-to-income is just shy of 200% of early 1980s levels, debt service payment are not that far off the bottom. This is because inflation causes your debt-to-income ratio to fall faster, but it does this by requiring a higher payment at even given level of debt. So even though debt-to-income was much lower in 1985, for example, debt payments were higher. One of the things I think these means – but I haven’t worked it out – is that low inflation creates a fundamentally more precarious economy, even without thinking about the zero lower bound.

Is the Fed Responsible for High Oil Prices? - Finding novel ways to blame the Federal Reserve for America's economic woes has become a favorite parlor game on both the political left and right. And now that the rising price of oil is threatening to slow down or possibly derail the recovery, it was probably only a matter of time before someone tried to blame Ben Bernake & Co. for the cost of crude. Today, The Wall Street Journal's editorial board took a brief stab at it while they were busy lambasting President Obama's energy policies. To its (limited) credit, the Journal does acknowledge that there might be a few other factors pushing up global crude prices, such as instability in the Middle East and rising demand in China and Brazil. But for various reasons, those can't possibly be the root of the problem, it argues. The more likely culprit, the paper says? U.S. monetary policy. Oil is traded in dollars, and its price therefore rises when the value of the dollar falls, all else being equal. The Federal Reserve throughout Mr. Obama's term has pursued the easiest monetary policy in modern times, expressly to revive the housing market. It has done so with the private support and urging of the White House and through Mr. Obama's appointees who are now a majority on the Fed's Board of Governors.

The Fed Can’t Print Oil But It Can Print Money - Rising oil price remain my principle concern regarding the recovery. My thesis is that rising oil prices are a monetary contraction because the funds are just parked in T-Bills. Imagine for example if rising oil prices caused Oil Producing countries to buy more Boeings or Catepalliar Equipment. Would we expect oil prices to be contractionary? Or would they simply shift production away from consumption and towards exports? Economists naturally think of international trade as pure exchange but of course its not. Dollar denominated assets are accumulated. This means it has monetary effects particularly at the zero lower bound. If we were in a normal world the appropriate response to higher oil prices would be to cut interest rates as T-Bills are seeing higher demand. Otherwise, the Fed will have to slow the growth of the money supply in order to maintain the Funds rate – which must wash with the T-Bill rate – and would otherwise fall. My advice would be to go with something like this: Higher oil prices represent headwinds for the US economy and may justify more accommodative action to prevent job growth from slowing.

Chicago Fed Nat'l Activity Index Is Positive For 2nd Straight Month - For the first time in a year, the Chicago Fed National Activity Index (CFNAI)—a broad measure of the U.S. economy—posted a positive reading for the second month in a row. Nonetheless, the pace slowed, with CFNAI slipping to +0.22 for January from December’s +0.54. Meanwhile, the three-month moving average (CFNAI-MA3) rose slightly to +0.14 last month, up from +0.06 in December, which the Chicago Fed advises is a sign "that growth in national economic activity was slightly above its historical trend." CFNAI is a weighted average of 85 indicators of U.S. economic activity. The Chicago Fed recommends reading its 3-month moving average (CFNAI-MA3) as follows: a value below -0.70 after a period of economic expansion "indicates an increasing likelihood that a recession has begun." By that rule, the January CFNAI-MA3 reading of +0.14 suggests that the economy will continue growing for the foreseeable future.

Chicago Fed: Economic Growth in January above Average -The Chicago Fed released the national activity index (a composite index of other indicators): Index shows economic growth in January again above average:The Chicago Fed National Activity Index decreased to +0.22 in January from +0.54 in December, but remained positive for the second straight month for the first time in a year. ... This graph shows the Chicago Fed National Activity Index (three month moving average) since 1967. This suggests growth slightly above trend in January - but still not strong growth. According to the Chicago Fed: A zero value for the index indicates that the national economy is expanding at its historical trend rate of growth; negative values indicate below-average growth; and positive values indicate above-average growth.

Fed’s Bullard Optimistic On Economy, Labor Market Gains - St. Louis Federal Reserve Bank President James Bullard expressed optimism over the economic recovery on Friday, saying he saw a “real gain” in the recent decline in the unemployment rate. The Fed official also distanced himself from the specific language in the central bank’s latest policy statement. Last month the Fed said it expected to keep interest rates at exceptionally low levels until late 2014. Bullard said that he would have preferred not to include a “calendar date” in the statement. “Way out at the end of 2014, we don’t know what the economy’s going to look like and it over-emphasizes our forecasting ability, which isn’t that good,” Bullard told reporters at a conference on Friday held by the University of Chicago Booth School of Business. Bullard was largely hopeful about the economy’s prospects in 2012. “It’s reasonable to be optimistic,” he said. “Just because you had some bad shocks and things went badly in 2011 doesn’t mean that’s what’s going to happen in 2012,” he said. The probability of a severe meltdown in Europe is now lower, compared to last fall, he said.

Threats to the Current Recovery - Let’s take a well-deserved break from manufacturing and tax policy and cheer things up with a post on threats to the current recovery. As I’ve stressed, IMHO we’re not yet into the virtuous cycle where we can count on above-trend growth to generate jobs, which boosts paychecks, which supports consumption, which signals investors to get into the game, which leads to more growth, etc. But we’re headed there. The best evidence for that is the improving job market—that’s been the missing link in the above cycle. Outside of public sector job losses—there’s your first ongoing threat—net payroll gains have accelerated in recent months and that’s helped to nudge down the unemployment rate which has ticked down by one or two tenths every month since last September. In that spirit, the first two figures show steady, favorable trends in the four-week average of unemployment insurance claims, closing in on pre-recession levels, and the number of job-seekers per job opening, which has recovered about half of its losses since the downturn.

Why The U.S. Economy Could Go Haywire - Americans participating in a recent Gallup poll showed the highest level of confidence in an economic recovery in a year. Sounds great, but you can’t ignore the nearly 13 million unemployed, the 46 million people on food stamps and the roughly 29% of the country’s homeowners whose mortgages are under water. They would find it hard to subscribe to the poll’s sunny conclusion. On the other hand, there’s no getting away from a bevy of seemingly increasingly favorable economic data, which, more recently, includes falling weekly jobless claims, four consecutive monthly gains in the leading economic indicators, somewhat perkier retail sales and a pickup in housing starts and business permits. Pounding home this cheerful view is the media’s growing drumbeat of increased economic vigor. Confused? How can you not be? But President Obama has to be elated at this widely perceived peppier economy. During much of his presidency, he’s been roasted by some critics as an economic illiterate, with one Internet poster recently reading: “Obama had a dream and we got a nightmare.” Now, though, thanks to the public’s growing acceptance of the idea that things are getting better, Obama’s approval ratings are on the rise. Even a number of his Wall Street critics are starting to acknowledge his chances of winning a second term have greatly improved and some believe he’s almost a shoo-in should the current economy continue to pick up steam.

False Recovery 2.0: It's Beginning to Look a Lot Like 2011 - Let's play "Name That Year of the Recovery." In the first quarter of this Mystery Year, the economy adds more than 200,000 jobs in consecutive months. Manufacturing is roaring. Investors are giddy and stocks improve for the third month in a row. The Dow breaks 12,000 for the first time since 2008. Economists are screaming, "Recovery Winter!" Surprise! It's 2011. The economy accelerated around the '10-'11 bend with practically every conceivable tailwind: accelerating employment, strong industrial production, and a decent, if spotty, normalization in housing. But you all remember what came after. Unrest in the Middle East sent oil over $100 a barrel. Europe's crisis weighed on banks, confidence, and exports. A showdown over the debt ceiling made a mockery of Washington. By the summer, the boomlet has wilted, job creation has slowed to a pathetic trickle, and economists were talking seriously about a double-dip recession. Fast-forward to 2012. The economy has added more than 200,000 jobs in consecutive months. Manufacturing is roaring. Investors are giddy. Stocks have hit 2008 highs. Economists are screaming, "Recovery Winter!"

Austerity. China. The Housing Market. The Middle East. Four reasons to stay gloomy about the global economy. - Since late last year, a series of positive developments has boosted investor confidence and led to a sharp rally in risky assets, starting with global equities and commodities. Macroeconomic data from the United States improved; blue-chip companies in advanced economies remained highly profitable; China and emerging markets slowed only moderately; and the risk of a disorderly default and/or exit by some members of the eurozone declined. Moreover, the European Central Bank, under its new president, Mario Draghi, appears willing to do anything necessary to reduce stress on the eurozone’s banking system and governments, as well as to lower interest rates. Central banks in both advanced and emerging economies have provided massive injections of liquidity. Volatility is down, confidence is up, and risk aversion is much lower—for now.But at least four downside risks are likely to materialize this year, undermining global growth and eventually negatively affecting investor confidence and market valuations of risky assets.

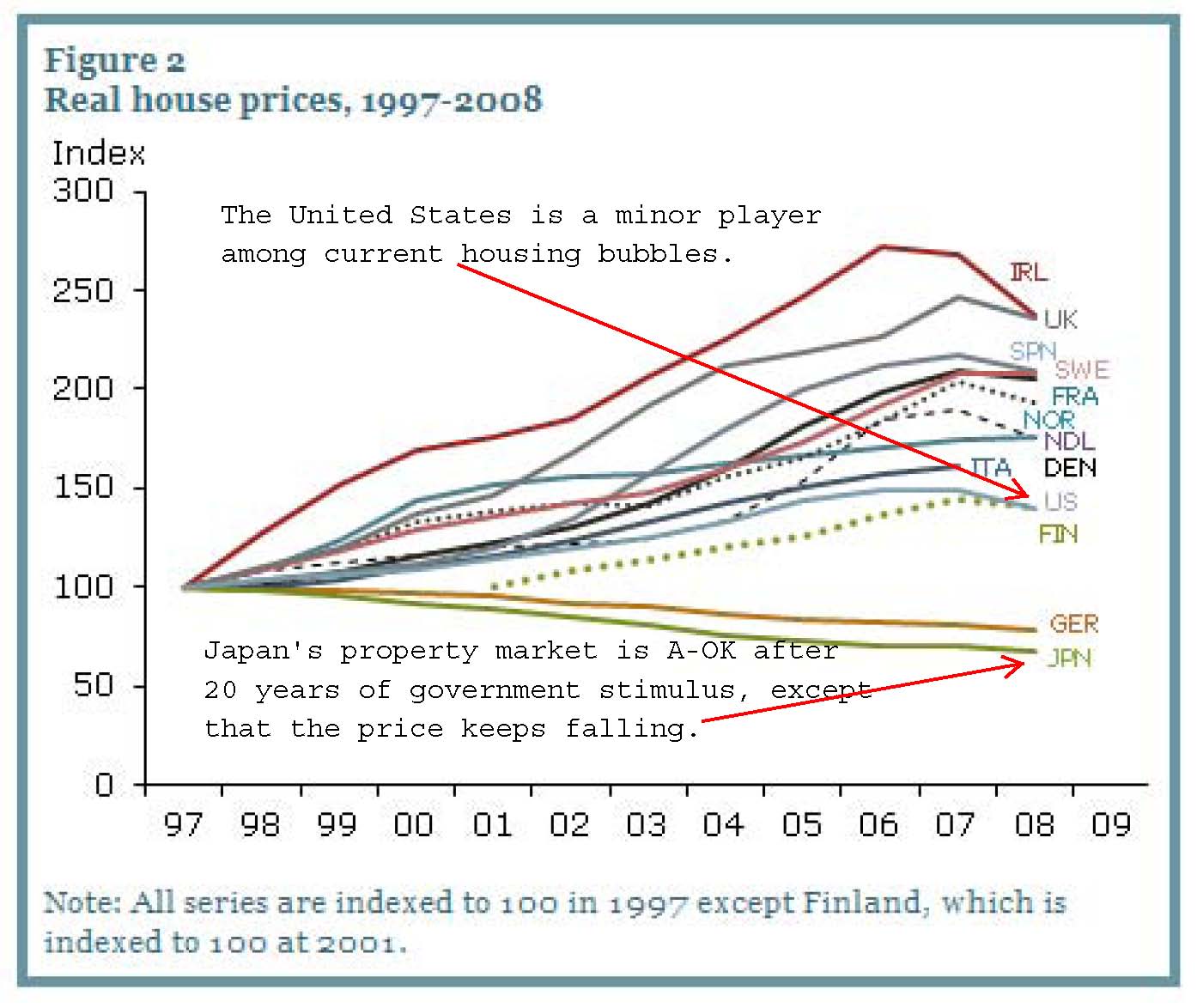

Measuring Housing's Drag on the Economy - Here’s a reminder about a problem that still doesn’t get the attention that it deserves: Housing has blown a giant smoking hole in the middle of our economy, and the consequences continue to impede the pace of recovery.A new paper presented Friday at a monetary policy conference in New York puts some interesting new numbers on the scope of the problem. The pace of recovery since the financial crisis has been less than half as fast as after the last two major recessions, which ended in 1975 and 1982. In first 10 quarters after those recessions, the economy grew by 13.4 percent; in the wake of this recession, the economy grew by only 6.2 percent. And, the paper says, “more than half the underperformance in this recovery is associated with housing-related sectors.” Yes, that’s right. Housing is more than half of our problem.

Modern Monetary Theory, an unconventional take on economic strategy - About 11 years ago, James K. “Jamie” Galbraith recalls, hundreds of his fellow economists laughed at him. To his face. In the White House. It was April 2000, and Galbraith had been invited by President Bill Clinton to speak on a panel about the budget surplus. But if Galbraith stood out on the panel, it was because of his offbeat message. Most viewed the budget surplus as opportune: a chance to pay down the national debt, cut taxes, shore up entitlements or pursue new spending programs. He viewed it as a danger: If the government is running a surplus, money is accruing in government coffers rather than in the hands of ordinary people and companies, where it might be spent and help the economy. “I said economists used to understand that the running of a surplus was fiscal (economic) drag,” he said, “and with 250 economists, they giggled.” Galbraith says the 2001 recession — which followed a few years of surpluses — proves he was right. A decade later, as the soaring federal budget deficit has sharpened political and economic differences in Washington, Galbraith is mostly concerned about the dangers of keeping it too small. He’s a key figure in a core debate among economists about whether deficits are important and in what way. The issue has divided the nation’s best-known economists and inspired pockets of passion in academic circles. Any embrace by policymakers of one view or the other could affect everything from employment to the price of goods to the tax code.

The Washington Post Goes “Unconventional” - Dylan Matthews had a piece on Modern Monetary Theory in the Washington Post yesterday that featured Levy Institute scholars James Galbraith and Randall Wray. WaPo also put together a “family tree” that displays some Post Keynesian and New Keynesian lineages. The piece has been bouncing around the internet, first with some supportive comments by Jared Bernstein. Both Dean Baker and Kevin Drum ask what’s so special about MMT, with Drum suggesting a focus on views about inflation. According to Drum, this is the central question: So should we focus instead on a genuine target of 4% unemployment, reining in budget deficits only when we fall well below that? That depends a lot on what you think the productive capacity of the country really is, and the mainstream estimate of NAIRU, the highest unemployment rate consistent with stable inflation, is around 5.5% right now. … Of course, you might also want to consider MPT, or Modern Petro-Monetary Theory. Rather than asking what level of economic growth kicks off unacceptable inflation, it asks what level of economic growth kicks off an oil price spike that produces a recession and higher unemployment. In comments at Mother Jones, Galbraith engages with Drum’s “MPT” point: Kevin – your instinct on the oil price is on target, in my view. The inflation threat that we face doesn’t come from deficits or high employment — it comes from the cost and price of energy. But managing this is not within the competence of the Federal Reserve.

Otherwise Good WaPo Article on Modern Monetary Theory Marred by Undeserved Praise of Roosevelt Institute - Yves Smith - In the “wonders never cease” category, the Washington Post, which is normally firmly in the camp of orthodox economic thinking and budget hawkery, ran a very well researched and complementary article by Dylan Matthews on Modern Monetary Theory. This may be a sign of MMT moving out of being regarded in policy circles as fringe (some might say lunatic fringe) to a useful part of an economist’s toolkit. Given that the piece did a good job of naming most of the major thinkers and writers on MMT (Marshall Auerback, and Rob Parenteau, creator of the term, “austerian,” were not mentioned, sadly), and also gave a nice shout out to Naked Capitalism as one of the blogs showcasing MMT writers, I feel a bit churlish criticizing the article. But one misconstruction stands out. It mentions the Roosevelt Institute’s New Deal 2.0 blog as another MMT friendly venue, when that is not longer the case, and for reasons that do not reflect well on the Roosevelt Institute.

Izabella Kaminska: Why MMT is Like an Autostereogram - We’ve discussed MMT’s recent foray into the mainstream, and the confusion it has consequently courted. But that’s the funny thing about the theory. It is naturally divisive because most of the time it fails to communicate its message succinctly. Which is weird, since the premise is actually fairly simple to understand. We’d say it’s akin to looking at an autostereogram. Once you get it, you never see things quite the same way again. But at the same time, try as they might, some people will never be able to see the image. Ever. And it all rests on one key fact (at least as far as we can tell!) . Rather than treating money as an object of wealth or somebody else’s debt, a means to trade … MMT treats money as a claim on wealth, a product of trade. This one view makes all the difference. Unlike the first viewpoint, which assumes that debt and money came out of trade, MMT believes debt, or more specifically monetary credit, pre-dates trade. Coinage and all forms of monetary token are thus just a physical representation of what is actually an innate credit system. In and of itself, money — the token — has no value. And this is largely why a fiat monetary system can work. The monetary unit doesn’t need to be a ‘valuable’ piece of metal. It’s who guarantees the token that matters. In modern times, that means the state. What’s more, suppress the credit system (which in the case of the United States is represented by the government’s debt) and inevitably you suppress an economy’s ability to trade. And this, by the way, is why MMTers believe government debt can never really constrain an economy whose government controls the official currency. Furthermore, this is also why in a time of crisis they believe you need more government guarantees, not less — hence their support of higher debt limits. If one chart sums up the theory best we think it’s this one from Stephanie Kelton:

In Which I Disagree With Izabella Kaminska - Well sort of, She writes This was exciting news for fans of the alternative economic school, more popularly known as MMT, which asks people to think of money, credit and tax in a completely different way to what is usually considered conventional in economics. All in all, we have to say, the article did a good job, at least when it comes to explaining the origins and basics of the theory. As a primer it worked well. . . .The reaction, of course, is interesting because it shows to what degree MMT really does represent a paradigm shift in economics. If you can’t flip your brain into MMT mode, try as you might, you’ll never really understand what they’re going on about. So earlier I made some disparaging comments about folks who don’t get the basic ideas that either the MMTers or the MMers are pushing. That was at minimum inappropriate. Still, I think it’s a mistake to talk about MMT as if it is some grand new way of looking at the world. Its basically just understanding how Central Banks with a little bit of progressive liberalism sprinkled on top for extra fun.

Krugman Embraces Keynesian Label to Defend Government Spending -- Nobel-prize winning economist Paul Krugman maintained his calls for government spending to create jobs after being labeled a “crude Keynesian” by fellow academic Jeffrey Sachs. “The job of the government” is “to step in,” Krugman, a professor at Princeton University, said at a panel discussion at New York’s Metropolitan Museum of Art yesterday. Sachs, an economics professor at Columbia University who also spoke on the panel, criticized Krugman earlier this month for not paying enough attention to the growing federal debt. Sachs said the government should focus more on investing in long-term programs like education instead of short-term stimulus measures. “We need plans, we need decade-long investments,” said Sachs, whose books include “The Price of Civilization” and “The End of Poverty.” Instead, he said, “We get year-to-year improvisation that passes for some kind of stimulus.” Krugman, 58, said more spending is needed to battle unemployment, which has held above 8 percent since February 2009, the longest such run since the monthly record-keeping began in 1948. Nonetheless, the rate is starting to drop, reaching a three-year low of 8.3 percent in January.

The Memo that Larry Summers Didn’t Want Obama to See - For the past three years, Washington journalists and politicos have obsessed over a 57-page memo that Barack Obama’s incoming economic team prepared for him in late 2008. The document has achieved such totemic status for good reason: It decisively shaped the Obama administration’s initial response to the economic crisis. The memo outlined the president-elect’s options for dealing with the teetering banks, the cash-strapped automakers, and the country’s tidal wave of foreclosures. Above all, the memo laid out options for a massive stimulus package—the mix of tax cuts and government spending designed to end the recession and boost employment. The economic team presented the contents of the memo to Obama at his transition headquarters on December 16, 2008, at which point they collectively settled on a proposed stimulus of nearly $800 billion. Last month, my friend and former colleague, Ryan Lizza, wrote a much-discussed piece in The New Yorker based on a copy of this and several other previously-unpublished memos. The piece and the corresponding memo described the stimulus options that Obama’s team—including Larry Summers, his top economic adviser, and Christy Romer, soon to be his chief White House economist—ultimately sent him. The options ranged from about $550 billion to just under $900 billion. Intriguingly, Lizza also noted that Romer “was frustrated that she wasn’t allowed to present an even larger option,” suggesting that while the memo he obtained may have been the end of the story, it was far from the whole story.

Shifting the Center of the Political Debate - I want to follow up on Paul Krugman's post about the shifting Overton window in the UK toward the political right (think of the Overton window as a view into the center of a debate). As Krugman would be the first to tell you, it's not just in the UK. For example, consider the current discussion over the president's proposed budget, a budget that is touted as "broadly consistent with the bipartisan deficit reduction proposals put forward by the Bowles-Simpson Commission." I thought the recommendations for balancing the budget that came out of the Bowles-Simpson committee gave far too much to the GOP - the solutions that were proposed were much further to the right of the political spectrum than I would have preferred. My recollection is that people such as Paul Krugman and Dean Baker were critical as well (and recall that there was no official report because four Democrats and three Republicans on the seventeen member committee could not agree to the recommendations on the table -- instead we got an unofficial report from the committee chairs, Bowles and Simpson). However, Republicans have shifted the debate so far to the right that Bowles-Simpson is now being portrayed by the administration and others as a model of balance, reason, and compromise that both sides ought to embrace.

The Moving of the Overton Window on Fiscal Policy - I liked this Mark Thoma piece about the shifting of the Overton Window. I think I alluded to this with my story on a new round of tax cuts being humped by the GOP, and the new bipartisan consensus on the virtue of tax cuts as a stimulus measure. I know exactly what the Administration would say, they’re trying to get things done, and a payroll tax cut mimics a wage increase. And on the merits, that’s fine. But the point I made earlier is that it’s the ideological drift that you get when you fight on the other side’s turf that becomes the problem. This is what Thoma gets at in his piece: ” I thought the recommendations for balancing the budget that came out of the Bowles-Simpson committee gave far too much to the GOP – the solutions that were proposed were much further to the right of the political spectrum than I would have preferred. Republicans have shifted the debate so far to the right that Bowles-Simpson is now being portrayed by the administration and others as a model of balance, reason, and compromise that both sides ought to embrace. Thoma adds that Tim Geithner actually backed off of one aspect of Bowles-Simpson, the Social Security changes, because they were, in Geithner’s words, too tilted on the side of benefit cuts. But the problem lies in making Bowles-Simpson as the wise middle ground in the debate. When the President reached out to John Boehner with a deficit plan that was actually to the right of Bowles-Simpson, again playing on the opposing turf, then it was foreordained that Bowles-Simpson would become the moderate compromise, even though it couldn’t even get a vote on its own committee.

Give People Shares of GDP - We can solve the debt crisis by replacing T-bills with “Trills.” - Robert Shiller - Corporations use a combination of debt and equity to finance their investments and operations. Nations, in contrast, rely exclusively on debt. When a nation’s economy stalls and its debt continues to grow—you may have noticed this happening a lot recently—disaster looms for the country’s taxpayers. This is why Europe is in turmoil right now. But things don’t have to work this way. Here’s an audacious alternative: Countries should replace much of their existing national debt with shares of the “earnings” of their economies. This would allow them to better manage their financial obligations and could help prevent future financial crises. It might even lower countries’ borrowing costs in the long run. National shares would function much like corporate shares traded on stock exchanges. They would pay dividends regularly. Ideally, they’d be perpetual, although a country could always buy its shares back on the open market. The price of a share would fluctuate from day to day as new information about a country’s economy came out. The opportunity to participate in the uncertain economic growth of the issuer might well excite, rather than scare off, investors—just as it does in the stock market.

Difference on Deficit Reduction is not about “How Much?” but “Who Pays?” – Treasury blog - The Budget released by the President this week uses a balanced approach to achieve more than $4 trillion in deficit reduction over the next 10 years. This level of savings and the manner in which they are accomplished are broadly consistent with the bipartisan deficit reduction proposals put forward by the Bowles-Simpson Commission and the Senate’s bipartisan “Gang of Six.” Using this balanced approach, the President’s Budget reduces deficits from about 9 percent of GDP in 2011 to below 3 percent by 2018, and stabilizes the debt as a share of the economy by the middle of the decade.In general, there is little disagreement on the magnitude of savings that are needed over the next decade to put us on a sustainable fiscal course. Rather, the main difference between the President and Republicans is related to the composition of these savings .As Secretary Geithner made clear in testimony on the Budget this week, the greatest impediment to bipartisan progress on reducing deficits is the unwillingness by Republicans in Congress to take a balanced approach. Instead, they have sought to achieve budget savings solely through cuts to critical programs like Medicare and Medicaid, without asking the most fortunate citizens to contribute anything more than they do today.

Is the Administration Joining Team Balance-Sheet Recession? - There’s a mini-debate going on over the relationship between the housing crash and weak demand. As Cardiff Garcia of FT Alphaville recently summarized it: “This reminded us of the debate last year about whether the sluggishness in consumer spending was the result of households wanting to deleverage or was caused by the big negative wealth effect caused by the huge crash in home prices.” See this from James Surowiecki on the wealth effect and the Q&A I did with Amir Sufi on deleveraging. Which is the main driver, deleveraging balance sheets or a wealth effect? I’m more on team balance sheet. It must seem like an esoteric debate, but it has some consequences. If it’s about deleveraging balance sheets, the problem is an income/debt issue. It can be solved by reducing debt through forgiveness, lower interest rates and refinancing, equity swaps, a jubilee, and many other options. The models used in these stories indicate that any kind of transfer from creditors to debtors will make the economy better off. If it’s a wealth effect, forgiving debt is likely to be less important — it’s not the root of the problem. Redistribution between creditors and debtors is unlikely to have a major impact outside of marginal propensities to consume. You’d need to get housing prices back up for there to be a significant adjustment.

It's February 21: Do You Know Where The Obama 2013 Budget Is? - I've been in the budget business for a long time, and I have to admit that few presidential budget have disappeared from view as fast as the one the Obama administration submitted to Congress last Monday. By last Tuesday — that is, by the day after it was released — you had trouble finding the Obama administration’s fiscal 2013 budget. I don’t mean that hackers made it impossible to download the budget from the Office of Management and Budget’s website or that the Government Printing Office bookstore near you was sold out of the four volumes. But even in a city like Washington, D.C. — where “long term” generally means after lunch tomorrow — the speed with which the Obama budget went from lead story to old news was impressive. It was also a great indication of what this year’s budget debate will be like. No doubt part of the disappearing act was planned. Although the word from deep within the administration was that the release of the budget was delayed a week from the Feb. 6 Congressional Budget Act deadline because of a last-minute change affecting military spending, it now seems possible that the White House was also looking at the calendar when it decided to wait until Feb. 13.

Obama’s Plan to Save the Military From Cuts—at the Expense of Domestic Programs - As budget wonks comb over President Obama’s outline for fiscal year 2013, a startling White House plan has become clear: the administration is seeking to undo some mandatory cuts to the Pentagon at the expense of critical domestic programs. This wasn’t a featured part of the White House budget rollout, and for good reason—it undercuts the administration’s carefully crafted message of benevolent government action and economic fairness. The process for this shift is complicated, and has been flagged by the Center on Budget and Policy Priorities. Essentially, Obama wants to eliminate individual spending caps for both military and non-military spending, and institute one single discretionary spending cap instead. To understand how deep the retreat really is, one first needs to understand the difference between security spending and defense spending. Spending on defense applies to the “National Defense Function”—that is, the entire Pentagon budget, plus $24 billion for nuclear weaponry and environmental cleanup programs at the Department of Energy, the defense activities of the FBI, and a small handful of other defense programs. Security spending, on the other hand, excludes some of the Department of Energy money, along with some of the other FBI and small program funding—but includes the Department of Veterans Affairs, the Department of Homeland Security and the “International Affairs” part of the budget, which is mainly State Department funding and foreign aid.

Competitiveness, and the Bush Tax Cuts and Deficits, by Menzie Chinn: The Administration released the annual Economic Report of the President on Friday. Many topics were covered, but here I’ll remark upon a few issues, motivated by several graphs. First is price markup over unit labor cost. The interesting trend since 2001 has been the rise in this variable. From this graph, one would be hard pressed to find American business in terrible shape. Productivity has increased, labor compensation growth has been modest, so that it’s obvious where profits have come from. This also means (to me) that there is substantial space for rising wages to be absorbed without a commensurate wage-price spiral. As I noted in this recent post, rapid productivity growth combined with slow compensation growth has improved American competitiveness. Nominal dollar depreciation over that period emphasized that improvement. The next graph decomposes the budget deficit into its constituent components, going forward. The graph highlights the impact of the 2001 and 2003 tax cuts on the Nation’s fiscal prospects. In a word, disastrous.

America needs its own infrastructure bank - America needs to invest in infrastructure. Despite signs of improvement, our economy is still in crisis. We could create millions of jobs by rebuilding our transport and water systems – ending the congestion that stifles our ports, airports, railroads and highways; increasing productivity; and empowering the US to compete with countries that are investing in infrastructure on a massive scale. Infrastructure financing tools are available, providing Washington wants to use them. They could bolster investment by leveraging hundreds of billions of dollars in private and international capital. The potential tools include a national infrastructure bank and other relatively minor legislative changes to encourage private investors off the sidelines. American mutual funds, pension funds and retail investors allocate relatively small portions of their $37,000bn in capital to new infrastructure initiatives. Congresswoman Rosa DeLauro has introduced a House bill to create one, and Senators Kay Bailey Hutchison and John Kerry co-sponsored similar legislation in the Senate. President Obama also supports a such a project. So do the AFL-CIO labour group and the US Chamber of Commerce, organisations that differ sharply on many issues but unite in calling for the US to rebuild. A national infrastructure bank could be independent and transparent. Government-owned but not government-run, it would have a bipartisan board and a staff of experts and engineers to plan projects based on quality and public need, not on politics. The infrastructure bank also should have authority to finance projects by issuing bonds with maturities of up to 50 years. These long-duration bonds would align the financing of infrastructure investments with the benefits they create, and their repayment would allow the bank to be self-financing.

By Request: More On Budget Process Changes - Last Wednesday I got an email challenging my comments about House Budget Committee Chairman Paul Ryan's (R-WI) poor decision to move ahead with changes in the congressional budget process. For those who don't remember, I posted that there's no doubt that the current system isn't working and that changes are needed, but that the way Ryan was trying to do it wouldn't work because he was putting the federal budget cart before the fiscal policy horse. The person who emailed me thought that the Ryan changes were good, that I was wrong (He used a very different word), and that my heritage needed to be questioned. As I've said many times before, including in testimony before the House Rules Committee a number of years ago, you shouldn't change the budget process until you know what you're trying to accomplish. Once you get an agreement on that -- reduce spending, lower the deficit, lower the debt, set revenues-to-GDP at a certain level, etc.) -- it's relatively easy to come up with a process that will get you there from here. Doing it the other way -- process changes before there's an agreement on the goal -- is a sure way to get the process ignored, waived, or simply defied.

Budget Gimmicks Are Alive and Well in the Payroll Tax Cut - The other day, I criticized the unwillingness of Congress to finance the latest extension of the payroll tax cut. Since that blog, the Congressional Budget Office released its estimates of the cost of the entire mini-stimulus, including the so-called “doc fix” and changes in unemployment compensation. And the games were even worse than I feared. Congress made no pretense of paying for the payroll tax cut itself. But it did claim it would pay for the rest of the package. Hint: It didn’t. There are two bits of legerdemain happening here. Both are functions of the 10-year budget window the Congressional Budget Office and the Joint Committee on Taxation use to score legislation. The first gimmick allows Congress to pretend tax cuts or new spending are temporary, when it is obvious to all they are not. The second is a sort of congressional lay-away plan. Lawmakers get to buy politically popular policies today but avoid paying for them until years from now. There is nothing new in all this. Congress has been playing games with the 10-year budget window (or its cousin the 5-year window) for decades. But the mini-stimulus showed business as usual is alive and well on Capitol Hill, despite the best efforts of the tea party caucus.

Payroll tax cut undermines Social Security's security - The accepted response to the economic deal reached in Congress last week, extending the Social Security payroll tax holiday and unemployment insurance and maintaining reimbursement levels for Medicare doctors, is huzzah! So why should we consider this action cause for despair? It's because with every extension of the payroll tax holiday, which was first enacted in 2010, the prospect that Congress will ever restore the tax to its statutory 6.2% of covered income recedes a little bit further over the horizon. And that's bad medicine for Social Security. To be fair, thus far the payroll tax holiday hasn't impaired Social Security's fiscal resources one bit. By law, 100% of the cut must be compensated for by transfers from the general fund; those transfers have come to about $130 billion since 2010, covering the original "temporary" one-year holiday and a two-month extension passed late last year. The new extension will require a further transfer of about $94 billion, according to the Congressional Budget Office. Yet because of the unique features of the program's financing, tampering with its revenue stream is playing with fire. The payroll tax is currently set at 12.4% of wages, split equally between employer and employee, up to a maximum of $110,100. The tax holiday cuts the employee's 6.2% share to 4.2%.

Just How Big is the Payroll Tax Cut? - The 2-percentage-point payroll tax cut extended by Congress in December and again last week will save workers a total of $114 billion this year, according to the Joint Committee on Taxation. Spread over nearly 160 million workers, that’s an average tax cut of $714. Yet the typical news report says “the average worker earning $50,000 [will] take home an extra $1,000.” That’s a big difference. What’s going on? The calculation implicit in the news report is simple arithmetic—2 percent of $50,000 is $1,000. But the average worker earns much less—just under $40,000 in 2010, according to the Social Security Administration. That suggests that the average tax saving would be about $800, still more than $714. The remaining difference results from the Social Security tax cap–$110,100 this year. Since incomes over the cap go into the overall wage average, the average wage subject to the Social Security tax is less than the average for all pay, roughly 10 percent less.

Tax-Cut Bill Includes Changes to Jobless Benefits - Tucked into a $140 billion bill extending emergency jobless benefits and a temporary cut to payroll taxes are several provisions intended to modernize the country’s outdated unemployment insurance system. Experts described the little-noticed changes as marginal improvements, but important ones, and said they promised to aid the long-term jobless and help hold down the unemployment rate in future recessions. “We’ve had the same unemployment insurance system since the 1930s, and it really was designed for a different time,” Alan B. Krueger, the chairman of the White House Council of Economic Advisers, said in an interview. “Most people on unemployment insurance back then had been temporarily laid off from manufacturing jobs. Obviously, that’s not true now — these are people who are often moving into a whole new industry.” The bill, which passed Congress on Friday and President Obama has said he will sign, allows states to use unemployment insurance money for programs that help move the jobless back into the work force. Such programs, like Georgia Works, often offer employers wage subsidies for taking on and retraining jobless workers. The bill also requires states to reassess the eligibility of workers for their unemployment insurance — confirming, for instance, that a person receiving long-term benefits is actively searching for a job.

Intergenerational Accounting at the Public Mutual Fund and Insurance Company - The government is not literally a mutual fund and insurance company. But in many ways, it operates like one, and greater awareness of the parallels would improve the quality of public debate over public spending. Most discussions of taxes and benefits treat either one or the other in isolation. This is not helpful. Imagine telling investors what they pay for shares of a company without explaining what they get in dividends or capital gains, or explaining the costs of insurance without specifying the benefits. What both investors and taxpayers should focus on is the difference between costs and benefits, appropriately discounted to reflect differences in their timing. But most discussions of taxes focus only on what is paid rather than net taxes (the difference between taxes paid and benefits received). Many focus even more narrowly on federal income taxes, ignoring state and local taxes and Social Security contributions. Likewise, many discussions of the social safety net describe the benefits that individuals receive without asking what taxes they have paid or will pay in the future. When comparisons are made, as in a fascinating report last week in The New York Times, they are often limited to federal taxes and benefits within programs such as Social Security and Medicare.

Who Actually Benefits From Federal Benefits? - Republican candidates have lately been parroting Charles Murray's argument that our "entitlement society" has created a nation of deadbeats who would rather live off government benefits than find a job. In response, the Center on Budget and Policy Priorities (CBPP) released a study earlier this week showing the fraction of government benefits that go to able-bodied workers. Their estimate is about 9 percent. I linked to the CBPP study on Monday, and since their methodology was fairly complex, I added a back-of-the-envelope version that simply added up the benefits of programs that don't serve the elderly, disabled, or working poor. The next day I got an email from Arloc Sherman, one of the authors of the study. You can't just add up these programs, he told me, because even a lot of programs that people think of as "welfare" actually serve the elderly, disabled, and working poor too. Medicaid is the biggest example: Most of us think of Medicaid as a program for the poor, but more than half of all Medicaid spending actually goes to the elderly and the disabled. So what percent of each program goes to the elderly, disabled, or working poor? The bulk of both Medicare and Social Security goes to the elderly and most of the balance goes to the disabled. But what about the others? I was surprised when I saw the complete breakdown, and you might be too. Here it is:

Tax Code Not Aligned With Basic Principles - As I pointed out last week, tax burdens depend a lot on how one defines “income.” In particular, the tax law makes a sharp distinction between income earned through wages and salaries, sometimes called “earned” income, on the one hand, and income from capital, or “unearned” income. Wage income is very heavily taxed because both the income tax and payroll tax apply to it. The lower one’s income is, the more likely that it consists solely of wages. Therefore, the heavy taxation of labor necessarily hits hard those with low and middle incomes. By contrast, income from capital is lightly taxed. Unrealized capital gains are untaxed, realized gains are taxed at a maximum rate of just 15 percent, and gains held until death are never taxed. Moreover, wealthy hedge fund managers are permitted to treat their managerial fees as if they are capital gains, something that is called “carried interest.” Dividends on corporate stock are also taxed at a maximum rate of 15 percent. The wealthier one is, the less his or her income is derived from labor. According to the Tax Policy Center, households in the middle three quintiles get about 70 percent of their total income from wages and salaries. For those in the top 1 percent of the income distribution, only about 30 percent of their income comes from labor and for those in the top tenth of 1 percent, just 20 percent of their income comes from labor.

Obama to propose lowering corporate tax rate to 28 percent - President Obama on Wednesday plans to propose a major overhaul of the nation’s corporate tax code, an election-year gambit that is likely to draw a contrast over a key policy issue with the Republicans vying to replace him. Obama will propose lowering the nation’s tax rate to 28 percent. At the same time, however, he will seek to increase the amount of revenues raised overall through corporate taxation by eliminating numerous deductions and loopholes that save companies tens of billions of dollars a year on their tax bills, according to a senior administration official. Today, the U.S. corporate tax rate of 35 percent is one of the highest in the world, but an abundance of loopholes and deductions means that many companies pay far less than that — or nothing at all. Companies in the United States pay almost half the taxes than companies do in other rich countries, compared to the size of the economy, according to the Organization for Economic Cooperation and Development.

Obama Offers to Cut Corporate Tax Rate to 28%— President Obama will ask Congress to scrub the corporate tax code of dozens of loopholes and subsidies to reduce the top rate to 28 percent, down from 35 percent, while giving preferences to manufacturers that would set their maximum effective rate at 25 percent, a senior administration official said on Tuesday. Mr. Obama also would establish a minimum tax on multinational corporations’ foreign earnings, the official said, to discourage “accounting games to shift profits abroad” or actual relocation of production overseas. With the framework for changes that the Treasury secretary, Timothy F. Geithner, will outline on Wednesday, Mr. Obama will enter an election-year debate with Republicans in Congress and in the presidential race who seek even lower taxes for businesses. But an overhaul of the corporate code is unlikely this year, given that political backdrop and the complexity of an undertaking that would generate a lobbying frenzy as businesses vie to defend old tax breaks or win new ones.

Corporate tax cut: Good idea, but won't stimulate economy… The White House is proposing to cut corporate income taxes from 35 percent to 28 percent. President Obama also recommends that manufacturers get a further cut, to 25 percent, and he wants to impose a minimum rate on foreign earnings to discourage the use of tax shelters. There would other less substantive changes as well under his plan. The cut in the statutory tax rate, however, may not have as large an effect on the corporate sector as many anticipate. The reason is that this is intended as a revenue neutral change in taxes. To accomplish revenue neutrality, the cut in the tax rate will be accompanied be closing loopholes, i.e. a broadening of the base. Thus, every company receiving a tax break will be matched somewhere else by companies experiencing a tax increase. Thus, while some firms will benefit, others will get hit harder by these taxes and the net effect overall should be roughly a wash.

Tax Breaks: A Primer - On Wednesday the Obama administration released its proposal to revamp corporate taxes, partly by cutting “loopholes and subsidies” that enable so many savvy companies to pay so little. The proposal also happens to add its own new loopholes and subsidies, most prominently for manufacturing companies. Such “loopholes and subsidies” are formally called tax expenditures. The name comes from the fact that they are arithmetically equivalent to spending government money. Here’s how: Charging a company one dollar less in taxes is effectively the same as giving a company one dollar; both leave the government with one dollar less, and the company with one dollar more. But politically, calling the subsidy a “tax break” sounds a lot better than calling it a “spending” gift. Economists generally discourage the use of tax expenditures, for three basic reasons. First, tax expenditures distort market behavior — which they’re sometimes designed to do, and sometimes not. Second, they junk up the tax code, causing taxpayers to spend more time and money just to comply with tax law, and to a large extent help people rich enough to hire sophisticated accounting firms. Third, tax expenditures add up to a ton of money.

Inside Obama’s Framework for Business Tax Reform - Here’s what I love about President Obama’s Framework for Business Tax Reform: His diagnosis of the problem is spot on. In just a few pages, the Treasury Department does a marvelous job describing what’s wrong with the way the U.S. taxes business. Anybody interested in understanding why the tax code is such a mess should read this. Here’s what I don’t like: After doing a great job explaining the problem, Obama often flops when it comes to a cure. Sure, he proposes cutting the corporate rate. These days, who doesn’t? But when it comes to which tax preferences he’d dump, Obama often ducks the tough choices. More troubling, some of his proposed cures may make the disease worse. Here are a couple of examples. The joint White House and Treasury Department paper explains what’s wrong with business subsidies and high tax rates. One big flaw: this toxic brew distorts business decisions. It encourages firms to finance with debt instead of equity, it drives firms to organize as pass-throughs such as partnerships to avoid paying taxes twice on corporate profits, and it drives investment to low-tax industries and away from high-tax industries. Obama’s cure: He proposes to cut rates for all non-manufacturing corporations from today’s top rate of 35 percent to a flat 28 percent. Manufacturers would enjoy a more generous 25 percent rate, and “advanced manufacturing”, whatever that is, would receive an even lower rate. But wait a minute, didn’t the president just tell us that it is bad thing to use the tax code to distort investment decisions?