Fed's Balance Sheet Shrank in Latest Week - The Fed's asset holdings in the week ended Aug. 22 were $2.828 trillion, down from $2.835 trillion a week earlier, it said in a weekly report released Thursday. The Fed's holdings of U.S. Treasury securities fell to $1.637 trillion from $1.646 trillion in the previous week. The central bank's holdings of mortgage-backed securities edged up to $859.31 billion from $854.16 billion a week ago. Thursday's report showed total borrowing from the Fed's discount lending window was $2.85 billion on Wednesday, down from $3.61 billion a week earlier. Commercial banks borrowed $9 million from the discount window, down from $16 million in the previous week. U.S. government securities held in custody on behalf of foreign official accounts totaled $3.565 trillion, compared with $3.553 trillion in the previous week. U.S. Treasurys held in custody on behalf of foreign official accounts was $2.867 trillion, an increase from $2.860 trillion a week earlier. Holdings of federal agency securities rose to $698.39 billion from $693.03 billion in the prior week.

FRB: H.4.1 Release--Factors Affecting Reserve Balances--August 23, 2012

Fed Watch: Self-Fulfilling Prophecies - Is the Federal Reserve doing enough? Joe Gagnon says no: For more than two years, the Fed has dragged its feet and resisted the obvious need for more aggressive action... ...A large majority of the committee projects [pdf] that inflation will be below target over the next two and a half years. If they assign any weight to their employment objective, they should be willing to accept inflation at least modestly above target in order to get a better outcome on employment. The willingness to accept the current state of affairs suggests that fear of the 1970's remains alive and well on Constitution Ave. The risks of inflation simply outweigh the expected benefits of additional easing, at least from the point of view of Federal Reserve Chairman Ben Bernanke. Earlier this spring, Brad DeLong made an insightful observation about the real parallels with the 1970s: The Federal Reserve of today does not take effective steps to reduce unemployment because it thinks any risk of sustained inflation above 2%/year is unacceptable. The Federal Reserve of the 1970s did not take effective steps to control inflation because it thought sustained unemployment above 7% was unacceptable. The Fed is really making the same mistake as they did in the 1970s. Not so says David Altig, who does not see so much of a conflict between the Fed's objective and the actual outcomes:. But if you are willing to accept that employment growth remains on a pace of 150,000 jobs per month—and I see no clear evidence to the contrary—it is not at all obvious that the pace of the recovery is inconsistent with the FOMC's view of achieving its dual mandate...Mark Thoma replies: It sounds as though the Fed has given up -- we've done all that we can, there's nothing more we can do, so we won't even try -- and we're not about to risk even the tiniest bit of inflation to find out if we are wrong...

Fed’s Lockhart: There Are Risks In Asking Too Much Of Monetary Policy -- A key U.S. central bank official worried Tuesday that monetary policy stimulus could be aimed at problems beyond its reach, in comments that acknowledged the continued challenges facing the U.S. economy. “There is a risk to monetary policy being employed too aggressively and without effect to address economic problems that can be resolved only by fiscal reforms that involve making tough choices about the allocation of public resources,” Federal Reserve Bank of Atlanta President Dennis Lockhart said in prepared remarks. “Monetary policy can exert a powerful positive influence on an economy, but as [U.S. Federal Reserve] Chairman [Ben] Bernanke has pointed out, monetary policy is not a panacea,” Mr. Lockhart said.

Lockhart’s Outlook Suggests QE3 Isn’t A Done Deal - A key Federal Reserve official on Tuesday suggested the case for more central bank easing is not the slam dunk so many in the markets now believe. In a speech, Federal Reserve Bank of Atlanta President Dennis Lockhart told a hometown audience that the current stance of monetary policy is “appropriate” to prevailing economic conditions. But he also said “there is a risk to monetary policy being employed too aggressively and without effect to address economic problems” that would be better sorted out by other parts of the government. The voting member of the interest rate-setting Federal Open Market Committee is closely watched because he is considered by many central bankers to have views aligning closely with the FOMC’s consensus outlook. So when an official–who had in recent remarks signaled a growing openness to additional central bank stimulus–flags the risk of the Fed doing too much, markets take notice. Mr. Lockhart also described himself as “undecided” as to what will happen when policymakers next meet in September. And having signaled the uncertain nature of the next meeting, Lockhart placed himself in the company of the core of Fed officials, most of whom have been open to further action without signalling it’s imminent. Only a few officials have definitively come out signaling a preference for easing or doing nothing at all. Mr. Lockhart’s comments appear to suggest more Fed stimulus in the guise of balance sheet-expanding bond purchases “would not fundamentally alter the growth trajectory in this current recovery,”

Fed Watch: Chances of QE3 Diminishing - I have made the case that neither the doves nor the hawks that are important for the course of monetary policy. It is the center that is the key, and that center needs to be pulled in one direction or the other by Federal Reserve Chairman Ben Bernanke. If the 2Q12 slowdown proved to be temporary, I doubt Bernanke is inclined to pursue more QE in the absence of clear financial market disruption. And with that in mind, although economic performance continues to be no better than lackluster, recent data has dispelled the worst fears that we are heading into recession. This combined with stable financial markets argues against additional easing in September. If the center is the key, we need to see where the center is moving. This should provide some insight into Bernanke's leanings as well. On July 13, Atlanta Federal Reserve President Dennis Lockhart said: my support for the current stance of policy rests on a forecast that sees a step-up of output and employment growth by year-end and into 2013. If the economy continues on the track indicated by the most recent incoming data and information, that forecast will become untenable, as will the policy premises underlying it. So, as I said at the outset, this is a challenging juncture for policymaking. The data since that time has shifted Lockhart's views, with likely no small part of that change due to the employment report. Today: There is a risk to monetary policy being employed too aggressively and without effect to address economic problems that can be resolved only by fiscal reforms that involve making tough choices about the allocation of public resources. Monetary policy can exert a powerful positive influence on an economy, but as Chairman Bernanke has pointed out, monetary policy is not a panacea. It is not that Lockhart believes the economy is surging forward. It is muddling along. But muddling along at a rate that does not justify additional easing. Nor is it clear that such easing would be effective as the remaining problems are beyond the scope of monetary policy.

Many at Fed Ready to Act if Growth Doesn’t Pick Up - Many Federal Reserve officials at their most recent policy meeting pushed for further actions to support the economy if the recovery failed to strengthen over the summer, an official account released on Wednesday showed. “Many members judged that additional monetary accommodation would likely be warranted fairly soon unless incoming information pointed to a substantial and sustainable strengthening in the pace of the economic recovery,” according to the minutes of the meeting, which ended Aug. 1. After that meeting, the Fed issued a statement that included stronger language to signal its commitment to helping the recovery. The minutes revealed that the committee had carefully chosen to say it “will provide additional accommodation as needed.” In June, it used softer phrasing, saying that the committee “is prepared to take further action as appropriate.” At the time, economists and analysts noted the change as a sign that the bank was more likely to act. The next chance for the Fed’s policy-making committee to introduce measures is in September. The committee is to meet Sept. 12-13, and Ben S. Bernanke, the chairman, is also scheduled to hold a news conference.

Fed Signals Readiness to Ease Without U.S. Growth Pickup - Federal Reserve policy makers signaled readiness to boost record stimulus unless they are convinced the economy is poised to rebound. Recent signs of strength may not be enough to satisfy them. Sponsored Links Many members of the policy-setting Federal Open Market Committee said further action would probably be needed “fairly soon” without evidence of “substantial and sustainable” improvement in the recovery, according to minutes of the July 31-Aug. 1 meeting released yesterday in Washington. Attention now turns to Fed Chairman Ben S. Bernanke’s Aug. 31 speech in Jackson Hole, Wyoming, where he may clarify his thinking on the need for stimulus in view of recent reports showing gains in retail sales and housing. Many participants at the Fed’s meeting said a new large- scale asset-purchase program “could provide additional support for the economic recovery,” according to the minutes. Policy makers said in a statement after the meeting that they will step up record stimulus if needed to spur growth and cut a jobless rate stuck above 8 percent since February 2009.

Further easing ‘warranted soon’, Fed says - The US Federal Reserve is set to ease policy unless there is a sharp change in economic data after the minutes of its August meeting revealed a strong consensus for action. “Many members judged that additional monetary accommodation would likely be warranted fairly soon unless incoming information pointed to a substantial and sustainable strengthening in the pace of the economic recovery,” say the minutes of the rate-setting Federal Open Market Committee That is an unusually clear statement of the FOMC’s views about future action and sets a tough condition for it to change course and keep policy on hold. Some better recent data – notably stronger retail sales and the creation of 163,000 jobs in July – had begun to raise doubts about whether the economy might improve enough to stay the Fed’s hand. Payrolls data for August will be released shortly before the Fed’s September meeting, but even if jobs growth is better, it is unlikely to amount to “a substantial and sustainable strengthening” in the pace of recovery. In another indication that the FOMC is ready to act, it discussed a range of tools with which to ease monetary policy further, including a possible third round of quantitative easing. Under QE3, the Fed would buy more long-term assets.

FOMC Minutes: Discussion of policy tools the FOMC "might employ" - Here is a key sentence: "Many members judged that additional monetary accommodation would likely be warranted fairly soon unless incoming information pointed to a substantial and sustainable strengthening in the pace of the economic recovery" From the Fed: Minutes of the Federal Open Market Committee, July 31-August 1, 2012. Excerpt: Participants discussed a number of policy tools that the Committee might employ if it decided to provide additional monetary accommodation to support a stronger economic recovery in a context of price stability. One of the policy options discussed was an extension of the period over which the Committee expected to maintain its target range for the federal funds rate at 0 to 1/4 percent. It was noted that such an extension might be particularly effective if done in conjunction with a statement indicating that a highly accommodative stance of monetary policy was likely to be maintained even as the recovery progressed. Given the uncertainty attending the economic outlook, a few participants questioned whether the conditionality of the forward guidance was sufficiently clear, and they suggested that the Committee should consider replacing the calendar date with guidance that was linked more directly to the economic factors that the Committee would consider in deciding to raise its target for the federal funds rate, or omit the forward guidance language entirely.Participants also exchanged views on the likely benefits and costs of a new large-scale asset purchase program. Many participants expected that such a program could provide additional support for the economic recovery both by putting downward pressure on longer-term interest rates and by contributing to easier financial conditions more broadly.

Economists React: Fed ‘Is Itching’ to Take More Action - Economists and others weigh in on the minutes from the latest Federal Reserve meeting. –With the exception of one member, the Minutes underscored the willingness among FOMC voters to engage in another round of [large-scale asset purchases], with the report stating that “many members judged that additional monetary accommodation would likely be warranted fairly soon unless incoming information pointed to a substantial and sustainable strengthening in the pace of the economic recovery.” This reference is key as it reinforces our long-standing belief that the burden of proof has remained on the data to prove that further policy easing will not be required.–If there was any doubt about how close the FOMC is to easing, the minutes to the most recent meeting should dispel those concerns. Many members suggested that additional easing would be warranted unless a “substantial and sustainable” pickup in economic activity materialized. And how many took the other side? According to the minutes, one member said additional accommodation would not improve the outlook. –The FOMC is once again itching to ease. I was surprised that they were able to resist the urge at this meeting, but the minutes made clear that they took a pass for two reasons. First, after having adopted a second round of Twist in June and hyping that as a major move, the FOMC couldn’t very well come back 6 weeks later and do something else and claim that was big too. In the FOMC’s words, “more time was seen as necessary to evaluate the effects of that decision.” Second, and more importantly, as laid out above, they were revving up to do something in September. I would be shocked if the next FOMC meeting came and went without something.

Fed to Deliver More Stimulus "Fairly Soon"; How Much Stimulus Does It Take? - Analysts poring over the July 31 - August 1, 2012 Fed Minutes quickly honed in on the following paragraph. The Committee had provided additional accommodation at its previous meeting by announcing the continuation of the maturity extension program through the end of the year, and more time was seen as necessary to evaluate the effects of that decision. Nonetheless, many members expected that at the end of 2014, the unemployment rate would still be well above their estimates of its longer-term normal rate and that inflation would be at or below the Committee's longer-run objective of 2 percent. A number of them indicated that additional accommodation could help foster a more rapid improvement in labor market conditions in an environment in which price pressures were likely to be subdued. Many members judged that additional monetary accommodation would likely be warranted fairly soon unless incoming information pointed to a substantial and sustainable strengthening in the pace of the economic recovery. What's the Definition of Many? There are 12 voting members on the FOMC. Is "many" three, four, or seven? I think the wording of the Fed minutes was purposely vague, hoping to get a "bang for no buck".

Minutes minutiae and open(-ended) questions - There was a seemingly minor item in the FOMC minutes released yesterday that didn’t get much attention but that, naturally, interested us quite a bit. The participants noted that the Fed staff had presented an analysis showing “substantial capacity for additional purchases without disrupting market functioning”. But the staff part of the minutes offered no details of this analysis. We’d sure love to see it. Not that we question its findings, whatever they were. It’s because we remain curious to get some details about exactly what Bernanke meant when he said that further easing shouldn’t be undertaken lightly because it would pose a risk to “market functioning” and “financial stability”. This is something we tackled in previous posts (try here and here) suggesting some possibilities, and the NYT’s Binyamin Appelbaum took a good look here. But we’re still not sure.

Markets Push Expectations for First Fed Rate Increase Out Past 2014 - Interest-rate futures extended gains Thursday as traders continued to push out the timing of the Federal Reserve‘s first policy-rate increase. After details from the last Fed meeting were released midday Wednesday, traders have become more comfortable with the notion that the central bank’s next move will be to prolong its low-rate intentions. Rate strategists at Bank of America Merrill Lynch see a “strong” likelihood the Fed will push out that guidance to late 2015 from its current late 2014 timetable.

Fed Watch: It's All About the Data - The minutes of the July 31 - August 1 FOMC meeting are out. In my opinion, they reiterated the importance of the data flow in assessing the Fed's next move. The money quote was: Many members judged that additional monetary accommodation would likely be warranted fairly soon unless incoming information pointed to a substantial and sustainable strengthening in the pace of the economic recovery. At first blush, this can be taken to indicate that easing is imminent, as early as September, in direct contradiction to what I wrote yesterday. The key, however, is how have conditions changed since the last meeting? The next line in the FOMC minutes is: Several members noted the benefits of accumulating further information that could help clarify the contours of the outlook for economic activity and inflation as well as the need for further policy action. Recall that as we headed into this meeting, the data had turned particularly weak. The pace of job growth had fallen dramatically from the start of the year, retail sales were flattening out, and GDP growth had slowed to 1.5%. Since then, the data have turned upward, much more consistent with the Fed's medium-term forecast. The July employment report was stronger, retail sales picked up, and overall growth is looking stronger, with Goldman Sachs' GDP tracking estimate rising to 2.3% for the third quarter I think the better data influenced Atlanta Federal Reserve President Dennis Lockhart to shift his language away from his dovish July comments. In short, I would argue that the data since the last FOMC meeting has in fact pointed toward an improvement in the pace of the recovery, which I think will pull the middle ground back from the brink of additional asset purchases.

Bullard Says Modest Growth Would Keep Fed on Hold -- Continued modest growth in the U.S., in the range of 2% for the balance of the year, should be enough keep Federal Reserve policymakers on hold and as data continue to show signs of improvement, St. Louis Federal Reserve Bank President James Bullard said Thursday. Mr. Bullard, in an interview on CNBC, played down a belief by some in the marketplace that minutes released Wednesday from the Fed suggest the central bank is inclined to act to stimulate the economy. Those minutes, said Mr. Bullard, are “a bit stale,” and that he doesn’t believe U.S. data now warrant a “gigantic” policy response by the Fed. The probability of further stimulus from the Fed is “not as high” as expectations seen this summer in the financial markets, he said. Still, he said he might support a more modest response if data turn soft, and that the central bank has that option on the table. In response to U.S. initial jobless claims data, released Thursday and which showed a rise of 4,000 to 372,000, Mr. Bullard said he doesn’t get concerned unless the indicator rises about 400,000. Mr. Bullard added that the Fed is intentionally vague about the timing of any possible easing. He also expressed concern that the Fed in unintentionally facilitating a build up in debt, and that more quantitative easing would make the central bank’s exit from that build up more difficult.

Fed Watch: Dueling Fed Presidents -- For those of us tracking the odds of QE3 in September, two regional Fed presidents - both non-voting participants - offered opposite views today. Neither was terribly surprising. Chicago Federal Reserve President Charles Evans reiterated his support for additional easing. Via Reuters: "The (July) employment data was a little better than expected," said Evans, one of the Fed's most dovish policymakers and who has led the most recent calls for active easing of monetary policy "It is still not nearly good enough," he added. "We need 300,000 to 400,000 (new jobs) a month to get to where we should be."... ...Evans reiterated that he thought current economic conditions already warranted action, adding that this was the third successive summer slowdown seen in the United States, and that as the Fed had acted to boost activity in the previous two downturns, there was every reason to be prepared to act this time. Of course, Evans has been pushing this story for awhile, to no avail so far. I think that had he been a voting member, he would have dissented at the last three FOMC meetings. On the other side of the coin is St. Louis Federal Reserve President James Bullard. Again, via Reuters: "I do think that the minutes are a bit stale because we have some data since then that has been somewhat stronger," Bullard, who will be a voting member of the policy-setting committee next year, said in an interview. This is similar to the concern I mentioned yesterday. To what extent have the FOMC minutes been overtaken by events, particularly better US data? Bullard further downplayed the tone of the minutes: "The tone of the discussions, for me anyway, was 'gosh things are not as good as we thought and it if continues to decelerate here, we're going to have to do something'," he said.

Bernanke letter to Issa: Scope for more easing -- In a letter to House Oversight Chairman Darrell Issa written Wednesday and released Friday, Federal Reserve Chairman Ben Bernanke said there is scope for further action by the Federal Reserve, language largely borrowed from the most recent minutes of the July 31-Aug. 1 meeting. He said the impact of Operation Twist is still working its way through the economy but said policy must be set in light of a forecast of future performance, responding to a question on whether it's premature to take further action

Bernanke Letter Defends Fed Actions - Federal Reserve Chairman Ben Bernanke, in a letter responding to questions posed by U.S. Rep. Darrell Issa (R., Calif.), chairman of the House oversight committee, defended actions the Fed has taken to support the economy and said there is room for the Fed to do more. "There is scope for further action by the Federal Reserve to ease financial conditions and strengthen the recovery," Mr. Bernanke wrote in a letter dated Aug. 22, a copy of which was obtained by The Wall Street Journal. The Fed's "Operation Twist" program—buying long-term Treasury bonds and selling short-term securities—is still "working its way through the economic system," Mr. Bernanke said. The program was first launched in September 2011 and in June 2012 was extended through the end of this year. Asked by Mr. Issa if it were premature to consider additional monetary moves, Mr. Bernanke said that "because monetary policy actions operate with a lag," the Fed must make policy "in light of a forecast of the future performance of the economy." The Fed chairman also said that the Fed's bond-buying of recent years has "helped to promote a stronger recovery than otherwise would have occurred, and to forestall the possibility of a slide into deflation…by putting downward pressure on longer-term interest rates and contributing to broader easing in financial conditions."

Video: Hilsenrath on Bernanke’s Defense of Fed Actions - Federal Reserve Chairman Ben Bernanke, in a letter responding to questions posed by Republican Rep. Darrell Issa, chairman of the House Oversight Committee, defended actions the Fed has taken to support the economy and said there is room for the Fed to do more. Jon Hilsenrath has details on The News Hub.

Further Evidence on the Fed's Superpower Status - I have made the case many times that the Federal Reserve is a monetary superpower. The Fed has this power because it manages the world's main reserve currency and many emerging markets are formally or informally pegged to dollar. As a result, its monetary policy gets exported to much of the emerging world. The ECB and Bank of Japan are also influenced by the Fed's decisions because they are careful not to let their currencies becomes too expensive relative to these dollar-pegged currencies and the dollar itself. U.S. monetary policy, consequently, gets exported to the Eurozone and Japan as well. This understanding helps explains why there was a global liquidity glut during housing boom period and suggests that some of the "global saving glut" was simply a recycling of loose U.S. monetary policy. It also implies that the Fed could now do a lot of good for both the U.S. and Eurozone economies if were to adopt something like a NGDP level target. Based on this view, the global economy sorely needs the Fed to wake up from its slumber. Fed Chairman Ben Bernanke admitted as much in one of his classroom lectures earlier this year.1 Chris Crowe and I developed this monetary superpower hypothesis in a paper that is now in my newly published book. In a new paper, Colin Gray has gone even further by formally motivating this hypothesis in a rational expectations model. He also has provided more robust empirical evidence for it.

Paper: Foreign Banks Were Biggest TAF Borrowers - Foreign banks dominated a key Federal Reserve bank lending program that ran from 2007 to 2010, a paper released Monday said. At issue in the paper written by Northwestern University’s Efraim Benmelech is the Fed’s now shuttered lending tool called the Term Auction Facility. The mechanism lent directly to deposit taking banks and was created to circumvent many financial institutions’ reluctance to borrow from the central bank’s traditional source of emergency lending, the Discount Window. The research was published by the National Bureau of Economic Research. Lending via the TAF was substantial and at its peak represented the largest category on the Fed’s expanding balance sheet. It functioned by auctioning money for a fixed term, in transactions collaterized by the range of securities also available to be used at the Discount Window. Borrowing peaked at around $500 billion in early 2009 and steadily trailed off as the worst days of the financial crisis passed. Benmelech said an analysis of Fed data shows foreign banks absorbed 58% of TAF lending, at $2.2 trillion versus the $1.9 trillion borrowed by U.S. banks. Between December 2007 through the majority of 2008–the hottest period of financial distress–the “vast majority” of TAF lending went to foreign and not American banks. The biggest borrower was Barclays, and “out of the ten largest borrowers, five are foreign banks, and out of the fifty largest borrowers, more than thirty are from foreign countries.”

The Fed’s Emergency Liquidity Facilities during the Financial Crisis: The CPFF - (NY Fed) This is the first post in a series that details the steps taken by the Fed in its role as lender of last resort during the 2007-09 financial crisis. At the height of the crisis, financial intermediation activities had virtually collapsed. In response, the Federal Reserve created liquidity facilities authorized under section 13(3) of the Federal Reserve Act, citing “unusual and exigent circumstances.” These facilities provided last-resort lending options in strained markets to prevent stress in the financial sector from spilling over onto real economic activity. In this post, we review the Commercial Paper Funding Facility (CPFF), a crucial program among the special lending facilities.

The Fed’s Emergency Liquidity Facilities during the Financial Crisis: The PDCF - NY Fed - During the height of the 2007-09 financial crisis, intermediation activities across the financial sector collapsed. In response, the Federal Reserve invoked section 13(3) of the Federal Reserve Act, citing “unusual and exigent circumstances,” to authorize the creation of a series of emergency lending facilities. These liquidity facilities provided last-resort-lending options to qualified borrowers in several strained markets in order to prevent the distress on Wall Street from spilling over onto Main Street. In an earlier post, we discussed the commercial paper funding facility. In this post, we review the Primary Dealer Credit Facility (PDCF), a program that represents the Fed’s first lending facility to nondepository financial institutions since the Great Depression.

Romney Offers Lukewarm Support for Fed Audit -- Mitt Romney offered a chilly endorsement of the idea of auditing the Federal Reserve Monday. Speaking at a campaign event in New Hampshire, Mr. Romney said he was for an audit, but he added that he didn’t want to sacrifice the Fed’s independence or hand over control of the central bank to Congress in the process. The qualification puts him closer to the Fed’s own position on subjecting itself to outside scrutiny. “The Federal Reserve should be accountable and we should see what they’re doing,” Mr. Romney said when asked at an event in Goffston, N.H., whether the Fed should be audited. He said yes to the question on audits but later added, “I don’t want to have Congress run the Fed, by the way…I want to keep it independent. There are very few groups that I would not want to give the keys to, one of them is Congress.” The House voted in late July, in a 327-98 vote, to subject the Fed’s monetary policy decisions to scrutiny from the Government Accountability Office, or GAO, a congressional watchdog. The Fed’s financial statements are already reviewed by an outside audit firm before publication in its annual report. The Government Accountability Office also audits the Fed’s financials. The GAO doesn’t evaluate its monetary policy decisions or the deliberations behind those decisions. The bill introduced by longtime Fed critic Rep. Ron Paul (R., Texas) would eliminate that exemption for the Fed’s closed-door discussions of monetary policy.

Romney Reiterates He Would Replace Bernanke - Mitt Romney said Thursday that he would replace Federal Reserve Chairman Ben Bernanke, dismissing the advice of a top adviser who suggested this week that the chairman should be considered for a third term. The presumptive Republican nominee told the Fox Business Network that as president, he would want to install someone new in the Federal Reserve post. Mr. Bernanke’s term ends in January 2014. On Tuesday, Glenn Hubbard, a top economic adviser to Mr. Romney, told Reuters TV that Mr. Bernanke should “get every consideration” to stay on at the Federal Reserve, calling the chairman a “model technocrat” and saying that he deserves a pat on the back. Many of Mr. Bernanke’s acquaintances believe he wouldn’t want a third term. Mr. Romney said he appreciates the counsel of Mr. Hubbard and others but reiterated his plans to replace Mr. Bernanke. He declined to say whether Mr. Hubbard, whom he called a wonderful economic adviser, might be a candidate for the job. In the interview, Mr. Romney offered few specifics about his plans going forward to address the fiscal cliff and to implement tax reform. The president should work with Congress and “make sure we do not have a cliff,” Mr. Romney said of the automatic tax increases and spending cuts set to take effect at the end of the year. Watch the latest video at video.foxbusiness.com

Should the Fed Risk Inflation to Spur Growth? - Room for Debate - NYTimes. - The specter of runaway inflation has haunted many economists since the 1970s. Even as, by one measure, inflation was at 0 percent for the past two months, some have warned that more action by the Federal Reserve to spur growth would lead to price increases. But should the Fed overcome fears of inflation in order to help the stagnant economy?

- Put Inflation Fears Aside - Mark Thoma - The Fed is far too worried about the potential for inflation, and far too pessimistic about its ability to lower the unemployment rate.

- Inflation Should Be Feared - John Cochrane - While preventing deflation in the recession was vital, the idea that a deliberate inflation is the key out of our policy-induced doldrums makes no sense.

- There's Little the Fed Can Do - Edward Harrison - With the federal funds rate at zero, the Fed has few effective tools. It's up to Congress to help, but it won't act.

The Cost-Benefit Challenge - Atlanta Fed's macroblog - In its latest Room for Debate feature, The New York Times poses the question "Should the Fed Risk Inflation to Spur Growth?" Befitting a balanced panel of blogging experts, Mark Thoma (Economist's View) says "yes," John Cochrane (The Grumpy Economist) says "no," and Edward Harrison (Credit Writedowns) says something like "irrelevant question, it's going to do neither." The whole discussion, naturally, is about differing assessments of the costs and benefits of additional monetary stimulus. Not surprisingly, this was also a theme disclosed in the just released minutes of the July 31–August 1 meeting of the Federal Open Market Committee:Participants also exchanged views on the likely benefits and costs of a new large-scale asset purchase program. However, others questioned the possible efficacy of such a program under present circumstances, and a couple suggested that the effects on economic activity might be transitory. In reviewing the costs that such a program might entail, some participants expressed concerns about the effects of additional asset purchases on trading conditions in markets related to Treasury securities and agency MBS, but others agreed with the staff's analysis showing substantial capacity for additional purchases without disrupting market functioning. Several worried that additional purchases might alter the process of normalizing the Federal Reserve's balance sheet when the time came to begin removing accommodation. A few participants were concerned that an extended period of accommodation or an additional large-scale asset purchase program could increase the risks to financial stability or lead to a rise in longer-term inflation expectations...

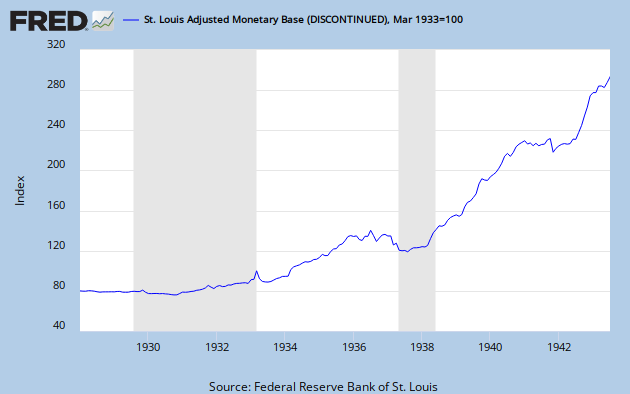

Shhhh… It’s Even Worse Than The Great Depression - In just four short years, our “enlightened” policy-makers have slowed money velocity to depths never seen in the Great Depression. Hard to believe, but the guy who made a career out of Monday-morning quarterbacking the Great Depression has already proven himself a bigger idiot than all of his predecessors (and in less than half the time!!). During the Great Depression, monetary base was expanded in response to slowing economic activity, in other words it was reactive (here’s a graph) . They waited until the forest was ablaze before breaking out the hoses, and for that they’ve been rightly criticized. Our “proactive” Fed elected to hose down a forest that wasn’t actually on fire, with gasoline, and the results speak for themselves. With the IMF recently lowering its 2012 US GDP growth forecast to 2%, while the monetary base is expanding at about a 5% clip, know that velocity of money is grinding lower every time you breathe.

The Financial System’s Death Knell? - Under widespread NIRP, pensions, annuities, insurers, banks and ultimately all savers will suffer a slow but steady decline in real wealth over time. Just as ZIRP has stuck around since the early 2000’s, NIRP may be here to stay for many years to come. Looking back at how much widespread damage ZIRP has caused since its introduction back in 2002, it’s hard not to expect that negative interest rates will cause even more harm, and at a faster clip. In our view, NIRP represents the death knell for the financial system as we know it today. There are simply too many working parts of the financial industry that are directly impacted by negative rates, and as long as NIRP persists, they will be helplessly stuck suffering from its ill-effects.

Chicago Fed: Economic Activity Increased in July - According to the Chicago Fed National Activity Index, July economic activity increased from June. The indicator, however, is still negative (meaning below-trend growth), and the data revisions of recent months worsened the 3-month moving average from last month's -0.18 to -0.21. Here are the opening paragraphs from the report: Led by improvements in production-related indicators, the Chicago Fed National Activity Index (CFNAI) increased to –0.13 in July from –0.34 in June. Three of the four broad categories of indicators that make up the index improved from June, but only the production and income category made a positive contribution in July. The index's three-month moving average, CFNAI-MA3, decreased slightly from –0.18 in June to –0.21 in July—its fifth consecutive reading below zero. July's CFNAI-MA3 suggests that growth in national economic activity was below its historical trend. The economic growth reflected in this level of the CFNAI-MA3 suggests subdued inflationary pressure from economic activity over the coming year. . [Download PDF News Release] The Chicago Fed's National Activity Index (CFNAI) is a monthly indicator designed to gauge overall economic activity and related inflationary pressure. It is a composite of 85 monthly indicators as explained in this background PDF file on the Chicago Fed's website. The first chart below shows the recent behavior of the index since 2007. The red dots show the indicator itself, which is quite noisy, together with the 3-month moving average (CFNAI-MA3), which is more useful as an indicator of the actual trend for coincident economic activity.

Chicago Fed: Growth in Economic Activity below trend in July - The Chicago Fed released the national activity index (a composite index of other indicators): Index shows economic activity increased in July Led by improvements in production-related indicators, the Chicago Fed National Activity Index (CFNAI) increased to –0.13 in July from –0.34 in June. ... The index’s three-month moving average, CFNAI-MA3, decreased slightly from –0.18 in June to –0.21 in July—its fifth consecutive reading below zero. July’s CFNAI-MA3 suggests that growth in national economic activity was below its historical trend. The economic growth reflected in this level of the CFNAI-MA3 suggests subdued inflationary pressure from economic activity over the coming year. This graph shows the Chicago Fed National Activity Index (three month moving average) since 1967. This suggests growth was below trend in July.

Understanding the CFNAI Components - The Chicago Fed's National Activity Index, which I reported on earlier today, is based on 85 economic indicators drawn from four broad categories of data:

- Production and Income

- Employment, Unemployment, and Hours

- Personal Consumption and Housing

- Sales, Orders, and Inventories

The complete list is available here in PDF format. A chart overlay of the complete 45-year span of all four categories, even if we use the three-month moving averages, is a bit challenging for visual clarity: So here is a close-up view since 2000: But a snapshot of the 21st century contains only two recessions, so it's unclear how the individual components have behaved in during the seven recessions since the 1967 starting point for this data series. Here is a set of charts showing each of the four components since 1967. Because of the highly volatile nature of the data, the charts are based on three-month moving averages, a smoothing strategy favored by the Chicago Fed economists:

The (Unfortunately?) Consistent Record of the Recovery: Duy and Thoma Respond - Atlanta Fed's macroblog -- Mark Thoma, always generous in linking and reposting our musings here at macroblog, took a look at my last post and read a sense of helpless resignation: David Altig of the Atlanta Fed argues that "the majority of FOMC participants don't seem to think that the unemployment rate will improve that quickly, but "it is not at all obvious that the pace of the recovery is inconsistent with the FOMC's view of achieving its dual mandate." It sounds as though the Fed has given up -- we've done all that we can, there's nothing more we can do, so we won't even try -- ... Tim Duy, whose observations in fact motivated my post, had his own response to my comments: Altig's calculations make the important assumption that the labor force participation rate holds at 63.7%. This effectively assumes that none of the decline in the labor force participation is cyclical. Instead, it is all structural... There are really two separate thoughts in these comments. So let me take them in turn, but first recap what I said in the previous post (or at least what I meant to say):

- Stepping back and looking at the data, I am drawn to the conclusion that U.S. economy looks like it has settled into a pattern of something like 2 percent GDP growth with net job creation somewhere around 150,000 payroll jobs per month.

- The unemployment projections published in the FOMC participants.' June Summary of Economic Projections (SEP) would, under certain assumptions, be consistent with annual job growth averaging the 150,000 per month pace we have seen over the past year and a half.

Consumer Debt and the Economic Recovery - FRBSF -A key ingredient of an economic recovery is a pickup in household spending supported by increased consumer debt. As the current economic recovery has struggled to take hold, household debt levels have grown little. Some evidence indicates that households adjusted debt in line with house price movements in their local markets. However, the data show that consumer debt cutbacks were largest among households that defaulted on mortgages or had lower credit scores, suggesting that household borrowing also was restricted by tight aggregate credit supply.

What trash can tell us about the U.S. economy - What fascinating secrets are buried in our garbage? Perhaps an indication of how well the economy is doing. Over at Marketplace, Kai Ryssdal offers up this fascinating graph from economist Michael McDonough. It shows that U.S. GDP growth has long been tightly correlated with the change in carloads of trash that are being shipped off by rail to landfills across the country: In fact, the trash index has had an 82.4 percent statistical correlation with U.S. economic growth since 2001. Few indicators are quite so revealing. As McDonough explains to Marketplace, trash provides a broad-based indicator of economic activity: “It’s holistic because it’s not isolated to a single part of the economy. It’s people throwing things out, it’s buildings being demolished — it’s everything. … I mean, if you’re going to build a new building, there might be a building that’s already there. If you buy a couch, you might be throwing out an old couch. If you go out to McDonald’s and you buy something, you’re going to throw something out.” And that’s worrisome because, as the graph above shows, the garbage indicator (which is gleaned from statistics provided by the American Association of Railroads) appears to have plummeted for the third quarter of 2012. That could be a sign that the U.S. economy is heading for a rough patch, dragged down by the recent slumps in both Europe and China.

Is Ambercrombie & Fitch’s Difficulties in Making Sex Sell an Economic Portent? - Yves Smith - Since I can’t get worked up enough about the latest Fed minutes (short story: Mr. Market is unhappy because he wants his QE and doesn’t see evidence that it is imminent), it might instead be worth examining something quite curious: that Ambercrombie & Fitch is having trouble making sex sell. You have to understand what a total fail that is. The advertising industry is largely devoted to using sex, either overtly or covertly, to get consumers to buy stuff. This is most true for products like clothing for target customers under, say, 50, cosmetics, and accessories. Just flip through the front of a Vanity Fair or a fashion magazine. I avoid them precisely because you get an overload of messages of how cool it would be to be somebody else. For women, that’s a size two woman with pouty lips and often drugged out looking eyes whose life aspiration is to be kept by (and per the subtext of some ads, dominated by) a rich man (as in they are clearly attired in a manner they couldn’t pay for themselves). The message for men is a bit more confused. You now see men treated as sex objects too, starting with those Men’s Health covers. In my youth, hemlines were seen as a leading economic indicator. Recall the miniskirts of the 1960s, versus the dowdy below the knee length of the 1970s? That’s now broken down since women have more latitude regarding attire than they once did. Nevertheless, as Lynn Parramore pointed out in a recent Alternet article, being worried about money is an anti-aphrodisiac. So the real question is whether Ambercrombie & Fitch’s tsuris are company specific, or a sign of how the lousy economy is undermining libido to such a degree that people won’t spend as much as they used to on hopes of getting laid.

Forecasting Economic Activity... Just Slightly - Last week’s update of the Capital Spectator Recession Risk Index (CSRRI)—a simple but revealing diffusion index based on a broad spectrum of economic and financial indicators—suggested that the probability was low that July will mark the start of a new recession. A broad review of recent history can reveal quite a lot about the business cycle, but it’s only a beginning. In an effort to peek ahead by projecting CSRRI's readings for the next several months, modern econometric modeling techniques can help. In particular, by torturing the data with what’s known as an ARIMA model (short for autoregressive integrated moving average), we can develop a robust benchmark for peering forward. Yes, all the standard caveats apply—forecasting, like playing with matches at a gasoline station, can be dangerous in the wrong hands. But with a bit of adult supervision, predicting can help us to think productively about what may or may not be coming. With that in mind, let’s kick the tires on the possibilities. As a preview, crunching the numbers with a series of ARIMA estimates for each of the 17 indicators in CSRRI, and aggregating the results, implies that recession risk will remain low for August. That’s no guarantee, of course, but it’s one signal (and arguably a robust one) that the slow-growth momentum will roll on for the near term. Here’s how the latest reading on CSRRI’s indicators stack up via the published data so far:

The End Of U.S. Economic Growth - Are the good times really over for good? A provocative new paper from economist Robert Gordon, “Is U.S. Economic Growth Over? Faltering Innovation Confronts the Six Headwinds,” makes just that case, or at least questions the assumption “that economic growth is a continuous process that will persist forever. There was virtually no growth before 1750, and thus there is no guarantee that growth will continue indefinitely … the rapid progress made over the past 250 years could well turn out to be a unique episode in human history.” Indeed, as the above chart shows, growth may be headed on a trajectory back to the zero-growth (or super slow growth) era before the Industrial Revolution. Doubling the standard of living took five centuries between 1300 and 1800. Doubling accelerated to one century between 1800 and 1900. Doubling peaked at a mere 28 years between 1929 and 1957 and 31 years between 1957 and 1988. But then doubling is predicted to slow back to a century again between 2007 and 2100 Or to put it another way, per-capita real GDP growth could slow down to a rate of a mere 0.2 percent by 2100. That is roughly what it was for the 400 years before the Industrial Revolution.

America's Future in an Enduring Recession - America's national optimism is so pervasive that not much public thought has yet been given to the possibility that the Great Recession could endure for many years. Even if GDP, the Dow Jones, and other standard economic indicators suggest that the overall economy is healthy once more, labor markets may not recover. Thus, all employment-related indicators could remain low to the end of the decade and beyond, justifying a guess about the social and political effects of an enduring recession. If the country faces a continuing labor market recession, short- and long-term unemployment are likely to rise. So will underemployment, such as involuntary part-time work and shorter work weeks for full-time workers. Discouraged workers will continue to drop out of the labor market, older ones will head for involuntary retirement, and some young people may not obtain a steady job during the entire period. The total number of labor market victims will rise well above the current official estimate of close to 15 percent of the labor force. And this estimate leaves out other victims of the recession -- people brought down by foreclosures, humongous debt, and lost pensions, as well as poor people driven into more severe poverty. If the numbers rise sufficiently, the social effects of the enduring recession, which are now still mostly hidden, will become apparent. High levels of depression and other emotional illnesses and related physical ones will multiply, as will family conflict and breakup, interpersonal and criminal violence, and other kinds of self and social destruction. Militant extremists threatening bodily destruction of immigrant and other vulnerable populations may increase in number as well. The medical community and the media are likely to be talking about post-traumatic economic stress disorder. America will be full of very unhappy people.

"Uncertainty" Is Nothing More Than Wall Street Whining - It's time to have an honest talk about "uncertainty" -- the B.S. complaint by Wall Street and corporations that they don't know what's going to happening in Washington; don't, therefore, know what to do; and are sitting on their hands and cash rather than (take your pick) expanding, hiring, investing. Look, for example, at this story by John Melloy at CNBC.com about the latest from David Kostin at Goldman Sachs. In talking about the fiscal cliff, Kostin is quoted as saying, “We believe the uncertainty is greater this year than it was 12 months ago.” Because of that, he urges investors to get out of equities before the fiscal cliff hits, could hit, might be settled, or...well...Kostin/Goldman Sachs doesn't really know, that is, they/it are "uncertain." As Kostin notes, last August's cliff-hanger fight over the debt ceiling should convince anyone who's watching what's happening now that there's no guarantee a deal will be cut, a rational agreement will be reached or the Democrats and Republicans, House and Senate, and Congress and the White House have the ability to deal with tax, spending, debt and deficit issues in a timely manner. But to bemoan the uncertainty as immobilizing and make it into its own issue is disingenuous if not completely deceitful. It's time to call it what it really is: Wall Street Whining.

Treasury Yields Reverse Directions - With the latest contraction in US equities, Treasury yields have pulled back with a flight (brief so far) to bonds. Today's Freddie Mac survey listed the 30-year fixed-rate mortgage at 3.66, up 17 basis points from its historic low four weeks earlier. As for the Fed's, Operation Twist, here is a snapshot of selected yields and the 30-year fixed mortgage since the inception of program.The 30-year fixed mortgage at current levels no doubt suits the Fed just fine, and the current low yields have certainly reduced the pain of Uncle Sam's interest payments on Treasuries. But, as for loans to small businesses, the Fed strategy is a solution to a non-problem. Here's a snippet from a recent NFIB Small Business Economic Trends report: Ninety-three (93) percent of all owners reported that all their credit needs were met or that they were not interested in borrowing. Twenty-nine percent reported all credit needs met, seven percent reported that not all of their credit needs were satisfied and 51% said they did not want. Only 3% reported that financing was their top business problem. The first chart shows the daily performance of several Treasuries and the Fed Funds Rate (FFR) since 2007. The source for the yields is the Daily Treasury Yield Curve Rates from the US Department of the Treasury and the New York Fed's website for the FFR.

On the Specialness of Long Treasuries - When Gary Schilling presented to the Baltimore CFA Society, he made the comment about how much bonds beat stocks by. His proxy for bonds was 25-year zero coupon bonds. Invest in those from 1980 to the present, rolling to the new 25-year regularly, and yeah you can beat stocks handily when interest rates fall and continue to fall. Think of what a 25-year zero coupon Treasury means. The price measures how much you are willing to discount inflation and nonexistence of the US government 25 years from now. When interest rates fall 3% for a 25-year zero, the value of the bond more than doubles. Falling almost 12% in yield since the peak, that multiplies the value of the bond more than 16 times, far more than the equity market over a similar period, including dividends.

Bankrupt! No, not the U.S. economy, just the policy discussion about it - This Week with George Stephanopolous yesterday was dominated by a panel discussing the deeply silly question of, “Is the U.S. going bankrupt?” It’s a silly question for one because it conflates issues with the federal budget deficit (which the show was entirely about) with the U.S. economy writ large. I know this is news to far too many pundits but the budget deficit and the U.S. economy are not the same thing. And if you look at the broader perspective of the U.S. economy, it’s clear that it’s not “going broke.” On average, the U.S. economy over any long period of time has been (and will be, absent some catastrophe) growing acceptably fast. Unfortunately, very few American households have actually experienced this “average” growth, since incomes at the very top have grown extraordinarily rapidly and absorbed vastly disproportionate shares of income growth in recent decades. And even in its own poorly-defined terms (i.e., the outlook for the federal budget deficit), the show was mostly a bust. For one, nobody reminded the panel or its viewers that the large increase in budget deficits in recent years have been driven entirely by the Great Recession (and its aftermath) and the explicitly temporary policy responses passed in its wake. This is important to know. In 2006 and 2007—even after the Bush tax cuts, wars fought with no dedicated funding and the passage of a deeply-inefficient Medicare drug program that also had no funding source—budget deficits averaged around 1.5 percent of total GDP, levels that no economist would argue are evidence of a crisis.

U.S. 2012 budget deficit $1.1 trillion: CBO -- The U.S. government will run a budget deficit of $1.1 trillion in fiscal 2012, or 7.3% of gross domestic product, the Congressional Budget Office estimated in a new report on Wednesday. The new deficit estimate is slightly lower than the agency's March estimate of $1.2 trillion. The nonpartisan CBO predicts that the U.S. economy will grow at a 2.1% clip in 2012, but fall by 0.5% between the fourth quarter of 2012 and the fourth quarter of 2013 if scheduled tax increases and spending cuts take effect in January. Under that "fiscal cliff," the U.S. would experience a recession, with U.S. unemployment jumping to about 9% in the second half of 2013 from its current 8.3%, CBO said. Previously, the CBO said growth would be 0.5% in 2013 under the fiscal cliff.

America’s Deficit Attention Disorder - In the United States, as Republican deficit hawks tell the story, “America is broke. We must cut government spending on social programs we cannot afford. And we must lower taxes on Wall Street job creators so they can invest to get the economy growing, create new jobs, increase total tax revenues, and eliminate the deficit.” We can only borrow money from each other. The idea that we borrow money from the future is an illusion. Democrats respond, “Yes, we’re pretty broke, but the answer is to raise taxes on Wall Street looters to pay for government spending that primes the economic pump by putting people to work building critical infrastructure and performing essential public services. This puts money in people’s pockets to spend on private sector goods and services and is our best hope to grow the economy.” Democrats have the better side of the argument, but both sides have it wrong on two key points.

- First, both focus on growing GDP, ignoring the reality that under the regime of Wall Street rule, the benefits of GDP growth over the past several decades have gone almost exclusively to the 1 percent—with dire consequences for democracy and the health of the social and natural capital on which true prosperity depends.

- Second, both focus on financial deficits, which can be resolved with relative ease if we are truly serious about it; and ignore far more dangerous and difficult-to-resolve social and environmental deficits. I call it a case of deficit attention disorder.

CBO warns of significant recession if Congress doesn’t act to avoid fiscal cliff - The nation would be plunged into a significant recession during the first half of next year if Congress fails to avert nearly $500 billion in tax hikes and spending cuts set to hit in January, congressional budget analysts said Wednesday. The massive round of New Year’s belt-tightening — known as the fiscal cliff or Taxmageddon — would disrupt recent economic progress, push the unemployment rate back up to 9.1 percent by the end of 2013 and produce economic conditions “that will probably be considered a recession,” the nonpartisan Congressional Budget Office said. The outlook is considerably darker than the forecast the agency released in January, when the CBO predicted that the fiscal cliff would trigger a mild recession in the first half of 2013 followed by a quick recovery.Since that forecast was issued, Congress has steepened the cliff by extending a temporary payroll tax break and emergency unemployment benefits, which are now also set to expire in January. In addition, CBO analysts have concluded that the underlying economy is weaker than had been predicted. The shock would be felt for years to come, with the unemployment rate stuck above 8 percent through 2014, the agency said. And the effects are likely to be felt well before the fiscal cliff hits, as “businesses’ and consumers’ concern about the scheduled fiscal tightening will lead them to spend more cautiously than they otherwise would have” during the remainder of 2012.

CBO predicts deeper "fiscal cliff" recession in financial year 2013 (Reuters) - Massive spending cuts and tax hikes due next year will cause even worse economic damage than previously thought if Washington fails to come up with a solution, Congress' budget office said on Wednesday. Without Congressional action to avoid a "fiscal cliff," Americans should expect a "significant recession" and the loss of some 2 million jobs, Congressional Budget Office director Doug Elmendorf said in his gloomiest assessment yet. He said the economy is already being "held back" by the mere anticipation of the cliff and the uncertainty surrounding it. "The sooner that uncertainty is eliminated, the better," said Elmendorf. The report could intensify the pressure on Congress and the White House to resolve their differences. But the likelihood of a resolution any time soon, particularly before the November election, is seen as slim. Chances could improve after the election for action during the lame-duck session of Congress, but that's unpredictable as well. Neither Democrats nor Republicans have shown a willingness to back away from fixed positions on either budget cuts or extension of tax cuts originally enacted during the administration of George W. Bush.

CBO Sees Recession Unless Congress Acts - The Congressional Budget Office released its updated budget and economic outlook on Wednesday, likely the last official forecast to come this year ahead of the November elections. Here are some quick takeaways:

- 1) If Congress doesn’t address the looming spending cuts and tax increases set to kick in next year, the economy will quickly go into recession, averaging a reduction in gross domestic product of 2.9% on an annualized rate in the first half of 2013. If the spending cuts and tax increases are averted, the economy is only expected to grow at an anemic 1.7% next year.

- 2) If the tax increases and spending cuts aren’t averted, the unemployment rate will rise to 9.1% at end of 2013. If they are avoided, the unemployment rate will fall just slightly, to 8.0% at the end of 2013, according to CBO’s forecasts.

- 3) CBO projects the deficit in the year that ends Sept. 30, 2012, will be $1.128 trillion, or 7.3% of GDP, slightly less than the $1.211 trillion projected by the White House a few weeks ago.

- 4) For the next fiscal year, which ends Sept. 30, 2013, if the tax increases and spending cuts go into effect, the deficit will shrink to just $641 billion, the equivalent of 4.0% of GDP. If the spending cuts and tax increases are averted by Congress next year, the deficit is projected to be $1.037 trillion, or 6.5% of GDP. That’s because less tax revenue will come into the government, and higher spending levels will continue.

CBO Expects 2013 "Fiscal Cliff" Recession Because of Automatic Spending Cuts and Tax Hikes - Automatic tax hikes and spending cuts will go into effect in 2013 causing a "fiscal cliff" recession according to the CBO. Massive spending cuts and tax hikes due next year will cause even worse economic damage than previously thought if Washington fails to come up with a solution, Congress' budget referee said on Wednesday. The Congressional Budget Office said failure to avoid the so-called "fiscal cliff" of expiring tax cuts and automatic spending reductions would cause U.S. gross domestic product to shrink 0.5 percent in 2013. Previously, the non-partisan CBO forecast full-year GDP growth of 0.5 percent. The first half of 2013 will be particularly difficult, the CBO said in its mid-year forecast update. Tax hikes and spending cuts will cause GDP to shrink 2.9 percent in the first half, compared with a prediction in May for a 1.9 percent contraction. There will still be a slight bounceback in the second half of 2013, but it will be weaker, with growth of only 1.9 percent, compared with a previous forecast of 2.3 percent growth.

CBO: If nothing changes, we’re in for another recession - Usually the release of Congressional Budget Office economic and budget projections is as dull as that phrase makes it sound. But not these economic and budget projections, released today by the CBO. The main takeaway is that if we go over the fiscal cliff — that is, if we let the Bush tax cuts and payroll tax holiday expire while allowing the automatic budget cuts under last summer’s debt ceiling deal to take effect — we’re going to fall into another recession, with real GDP declining by 0.5 percent in 2013. That’s nowhere near the 3.1 percent decline we saw in 2009, but it’s a far cry from the already anemic 2.4 percent and 1.8 percent growth rates of 2010 and 2011 respectively, and the 1.75 percent average we’re at for 2012 so far. Doing nothing also leads unemployment to rocket up to 9.1 percent, as the graph below shows. The “projected baseline” is what happens if we do nothing, and the “alternative fiscal scenario” is what happens if current policies are extended. Note that in 2015, in both scenarios, unemployment is still way above its pre-recession level. We’re just not growing fast enough to get back to normal:

The CBO Outlines How The Fiscal Cliff Would Send The US Into A Recession (Infographic) - Investors are wary of the fiscal cliff – the over $600 billion in tax and spending provisions that are set to change unless Congress acts – that would be a major drag on the U.S. economy. Now, the Congressional Budget Office is out with a new infographic on their baseline scenario which projects a recession for the U.S. economy in 2013. And an alternative fiscal scenario in which lawmakers extend tax cuts and prevent spending reductions. The infographic also looks at the impact this would have on the federal deficit, economic growth, and the implications this would have on future policy decisions.

‘Fiscal Cliff’ Has Many Perils - The U.S. economy likely would slide into a “significant recession” next year if Congress doesn’t avert tax increases and spending cuts set to begin in January, the Congressional Budget Office said Wednesday. But if they are postponed for at least a year, the federal government faces the prospect of a fifth straight year with a budget deficit greater than $1 trillion, the CBO said…The CBO painted two starkly different scenarios for next year, depending on which path lawmakers take. Under current law, the Bush-era tax cuts are scheduled to expire at year-end, raising tax rates on more than 100 million Americans. These tax increases, combined with roughly $100 billion in required spending cuts on military and other government programs, would shrink projected deficits from $1.13 trillion in the fiscal year ending Sept. 30 to $641 billion for the year that ends Sept. 30, 2013. That would reduce the deficit from roughly 7.3% of the nation’s gross domestic product to roughly 4% of GDP, the CBO said, the largest one-year reduction since 1969. But as a consequence, the economy would contract at a projected annualized rate of 2.9% in the first half of 2013, and by 0.5% over the entire year. The unemployment rate would rise to 9.1% at the end of the year from just above 8% now, the CBO estimated. If Congress were to postpone the tax increases and spending cuts, the deficit would shrink just slightly in the next fiscal year, to $1.037 trillion, or 6.5% of GDP. The unemployment rate at the end of 2013 would be 8%, a difference of roughly two million jobs from the other scenario, CBO said. The economy would grow by 1.7% over the year

Gloom or Doom from CBO -- The Congressional Budget Office’s summer budget update charts two undesirable paths for the nation’s economic and fiscal health next year. Call them Gloom and Doom. Gloom is what happens if the tax increases and government spending cuts scheduled to arrive in January actually occur. CBO says that would drive the economy back into recession in 2013 and push unemployment above 9 percent. But there’s some sunshine too: the federal deficit would drop sharply—by nearly half in 2013 alone—and would be under 1 percent of GDP by 2016 (dark blue bars in graph). The federal debt would decline from 73 percent of GDP this year to 59 percent in 2022. And the economy would resume growing in a year or so. Long-term gain for short term pain. Doom occurs if Congress and the president agree to extend all of the expiring tax cuts and postpone the scheduled spending cuts for the next ten years. Short-term extension would prevent renewed economic collapse—the economy would maintain its slow growth and unemployment would continue its slow downward trend. But deficits would fall much less (the sum of the bars in the graph) and government debt would climb to nearly 90 percent of GDP in 2022.

Fiscal Cliff Risk In Perspective - The Congressional Budget Office warned yesterday that there's a recession coming next year if Congress doesn't act to soften the blow from the scheduled expiration of tax cuts and automatic budget cuts. The so-called fiscal cliff, in short, is moving closer. What can you do with this information? Nothing. Unless, of course, you're prone to making decisions today based on forecasts six months or more into the future. But history suggests you should think twice before jumping off the forecasting cliff, regardless of who's dispensing the prediction. Don't misunderstand: the scheduled expiration of tax cuts and automatic budget cuts represent real, albeit potential, threats to the economy. But so is the economic blowback via higher oil prices if Israel attacks Iran in a pre-emptive strike; or if Syria's civil war worsens and turns into a regional war. In fact, anyone can come up with a laundry list of plausible scenarios, both here and abroad, that would probably push the economy into recession. The fiscal cliff scenario is one of them, and it's a risk that we should take seriously, but not too seriously... at least not yet. The problem is that there are always risks lurking that could derail economic growth. But it's also true that recessions rarely arrive as bolts out of the blue with no advance warning in the numbers. The idea that you could go to sleep on Monday, when all is fine, and wake up on Tuesday and find the economy contracting is the macro equivalent of worrying about hobgoblins under your bed.

The ‘Fiscal Cliff’ in Charts - The Congressional Budget Office released its latest budgetary outlook, noting that the U.S. economy could slip into recession if Congress fails to act on the “fiscal cliff.” The report also included the following charts: Charts from CBO's August 2012 Budget and Economic Outlook from Congressional Budget Office Among the highlights:

- Slide 3: Shows deficit forecasts under several different scenarios.

- Slide 9: Shows actual and projected growth for the U.S. and its leading trading partners.

- Slide 12: Shows projected unemployment rates under both a scenario where the fiscal cliff is avoided (8% at end 2013) and if the spending cuts and tax rates are allowed to occur (9.1% at end 2013).

- Slide 13: Shows actual and projected GDP compared to potential. According to the chart the U.S. still has a long way to go to get back to potential.

Latest CBO Budget Projections Underline Need for Goldilocks Budget Deal - The latest analysis from the Congressional Budget Office (CBO) shows a sharp divergence between a baseline projection and an alternative fiscal scenario for the U.S. economy. To put it in language a child could understand, the baseline projection is too cold while the alternative scenario is too hot. It is clear from the report that we need a Goldilocks budget deal to get things just right. The CBO’s baseline assumes no changes in current law. Paradoxically, no change in the law would mean big changes in policy. That is because we are facing the so-called fiscal cliff–a set of measures that include allowing the Bush tax cuts to expire as scheduled, making sharp cuts in Medicare payments to doctors, ending extended unemployment benefits, and allowing mandatory cuts to defense and nondefense spending to come into force. The CBO projects that those changes would shrink the budget deficit to about 4.0 percent of GDP, compared with a projected 7.3 percent for 2012. The deficit would decline to 1 percent of GDP by 2016. The alternative fiscal scenario assumes that Congress will make the kinds of changes to current law that it has regularly made in the past. Tax cuts will not be allowed to expire (except for the temporary reduction in payroll taxes); Medicare cuts will be postponed (the so-called “docfix”); and mandatory spending cuts will be cancelled or postponed. Under those projections, the deficit for 2013 would be 6.5 percent of GDP, never falling below 4.2 percent of GDP. The alternative fiscal scenario—business as usual—is “too hot” in the sense that it keeps the deficit and debt on unsustainable paths.

As the Fiscal Cliff Nears, Will Anyone Swerve? - While Congress is on recess and both major political parties are gearing up for their conventions, the Congressional Budget Office on Wednesday issued a stark reminder of the danger posed to the U.S. economy by the set of budget cuts and tax increases set to go into effect after the new year. These budget measures, popularly known as the “fiscal cliff,” will cut more than $500 billion from the deficit, money that would come directly from a convalescent economy, most likely forcing the U.S. back into recession, according to CBO forecasts. As it stands, on January 1 the following cuts and increases will go into effect:

- The expiration of the Bush tax cuts for every tax bracket;

- The expiration of a 2% cut in payroll taxes enacted by President Obama and Congress in 2010 and extended again earlier this year; and

- Spending cuts to Medicare, defense and other discretionary spending as part of Congress’s and the Obama Administration’s deal to raise the debt ceiling last summer.

With federal debt held by the public reaching 73 percent of GDP, and yearly deficits recently topping $1 trillion, it’s almost unanimously agreed upon that the U.S. has a long-term debt problem. But most economists and policy analysts believe that the debt situation isn’t bad enough that it can’t be addressed in a more gradual and careful manner than current law allows.

The Fiscal Cliff Is Not as Steep As It Seems - Dean Baker - The Congressional Budget Office came out with its mid-year budget update. The update included a warning that if the Bush tax cut and the payroll tax cut are both allowed to expire and the cuts from last year's budget agreement take effect, the economy will sink into recession in 2013 and the unemployment rate will rise to 9.0 percent. The NYT immediately picked up on this warning in a news article on the new projections. It is important to realize that this projection for a shrinking economy and rising unemployment rate is based on the higher taxes and lower spending remaining in place for a whole year. The failure of Congress and the president to agree to a package by January 1, 2013, by itself, would not lead to this sort of contraction. If Congress and the president were to work an agreement somewhere in the month of January or even February, it would mean that people would be paying higher taxes for a short period of time. This reduction in disposable income, coupled with the cuts in spending scheduled to take place, would dampen growth. However, if an agreement reached early in the year restored part of the tax cuts and reversed some of the spending cuts, then the impact on the economy would be very limited. The point is that January 1, 2013 is not a drop dead date. While it would be desirable to have an agreement on tax and spending issues before this date, and in fact as soon as possible, there will be little harm if negotiations continue into next year, as long as a deal is reached before we get too far into the new year.

Hitchcock Could Teach Congress About Dangers of ‘Fiscal Cliff’ - The CBO report projected that current fiscal laws would cause gross domestic product to contract at a severe annual rate of 2.9% in the first half of 2013 and the jobless rate would rise back above 9%. Despite the dire warnings, politicians in Washington have made little effort to avoid the cliff. Dithering policy makers seem to think their decisions can be made in isolation. They could use some lessons from director Alfred Hitchcock on human reaction to suspense. In Hitchcock’s view, if a movie audience watches an innocent-looking scene and a bomb under a chair goes off, the reaction is immediate surprise. But if the audience knows the bomb is under the chair and timed to go off in five minutes, they will watch the scene holding their breath, fingernails digging into their armrests. For economic players, the bomb under the chair is the billions in coming tax increases and spending cuts. The economic equivalent of holding their breath is to table buying and hiring decisions. As the CBO report says about the second half of 2012, “businesses’ and consumers’ concern about the scheduled fiscal tightening will lead them to spend more cautiously than they would otherwise.”

Nobody Cares About the Deficit - Paul Krugman -- Dave Weigel makes a good point: there’s a huge inconsistency between the way Republicans are responding to the new CBO report on the fiscal cliff and everything they’ve been saying for the past two years. What the CBO says is that allowing the Bush tax cuts to expire and the sequester to kick in would hit the economy hard next year — because it would lead to a sharp fall in the deficit while the economy is still depressed. It’s pure Keynesianism, the same point that all of us anti-austerians have been making for years. If the right was at all consistent, it would be denouncing the CBO report for failing to take into account the impact of a lower deficit in deterring the invisible bond vigilantes and encouraging the confidence fairy. But whaddya know: suddenly the deficit is not an issue. Of course, it has been obvious all along that the whole deficit-hawk pose was insincere, that it was all about using the deficit as a club with which to smash the social safety net. But now we have a graphic demonstration.