Fed balance sheet grows in latest week - (Reuters) - The Federal Reserve's balance sheet grew in the latest week with a jump in the holdings of agency mortgage-backed securities, Fed data released on Thursday showed. The Fed's balance sheet stood at $2.829 trillion on October 17, up from $2.794 trillion on October 10. The Fed's ownership of mortgage bonds guaranteed by Fannie Mae (FNMA.OB), Freddie Mac (FMCC.OB) and the Government National Mortgage Association (Ginnie Mae) totaled $862.30 billion, up from $835.01 billion the previous week. Under the Fed's latest stimulus program, announced last month and dubbed QE3, the central bank has pledged to buy $40 billion per month of agency mortgage-backed securities. The Fed's holdings of Treasuries totaled $1.659 trillion as of Wednesday versus $1.654 trillion the previous week. The Fed's holdings of debt issued by Fannie Mae, Freddie Mac and the Federal Home Loan Bank system totaled $82.75 billion, which was unchanged on the week. The Fed's overnight direct loans to credit-worthy banks via its discount window averaged $12 million a day during the week compared with a $17 million a day average rate the prior week.

FRB: H.4.1 Release--Factors Affecting Reserve Balances--October 17, 2012

Fed Official Says Monetary Steps Were Too Timid - The Federal Reserve’s recent expansion of its economic stimulus campaign was announced as a course correction. It wasn’t that economic circumstances had changed, officials said. They simply had concluded that they needed to do more. The implication, of course, was that the Fed had failed to do enough. William C. Dudley, president of the Federal Reserve Bank of New York, made that point explicit in a Monday speech. “Monetary policy, while highly accommodative by historic standards, may still not have been sufficiently accommodative given the economic circumstances,” Mr. Dudley said. He underscored the point later, saying, “With the benefit of hindsight, monetary policy needed to be still more aggressive.” Mr. Dudley said that the shortcomings of monetary policy were one of five reasons, in his judgment, that the recovery continues to disappoint expectations. The others he listed include the overhang of mortgage debt, economic problems in Europe and other parts of the world, the aging of the American population and the shortcomings of fiscal policy makers.

Bernanke's faith in QE on shaky ground - Since the end of the International Monetary Fund meetings in Tokyo less than a week ago, there have been a series of defensive statements from Federal Reserve officials trumpeting the success of their actions. Ben Bernanke, head of the US central bank, said Fed policy “helps strengthen the US economic recovery” and “by boosting US spending and growth it has the effect of helping support the global economy as well”. But there is little hard evidence of either a recovery in the broad economy or a connection between “quantitative easing” and any hopeful signs of improvement in the economy. The economic activity that was supposed to be sparked by the third round of quantitative easing has yet to materialise. Indeed, the impact of this latest round of unconventional monetary policy is already fading. Analysts at Morgan Stanley this week decided that returns in the high-yield market were no longer attractive in the face of deteriorating fundamentals. The stock market is struggling to make further headway, while yields on mortgage-backed securities have started to turn up after an initial drop. A drop in third-quarter capital expenditure suggests the Fed policy hasn’t been a catalyst for corporate investment at all. One major reason for the lack of effectiveness of this latest round of quantitative easing may well be a growing concern with the “fiscal cliff”, automatic US tax rises and spending cuts due to kick in on January 1. Uncertainty over “cliff risk” – and the prospects of a deal in Congress on deficit reduction – seems to be offsetting any positive impact of Fed policies. Goldman Sachs this week sent its clients its fiscal risk scenarios. What it refers to as its base case (the “not so good scenario”), in which the cliff is barely resolved by year end, results in a 1.5 percentage point deduction from real GDP growth in early 2013. Under its bad scenario, in which jobless benefits and upper income tax cuts expire, that drag rises to almost 2 percentage points. Finally, under its ugly scenario, where there is no agreement on a path to more fiscal prudence for an extended period, the GDP growth hit amounts to about 4 percentage points and plunges the economy back into recession.

Fed's Williams: Fed Actions Will Improve Growth - The "strong measures" taken by the Federal Reserve at its September meeting should spur better levels of growth in the U.S. economy, a key central bank official said Monday. John Williams, president of the Federal Reserve Bank of San Francisco, also said the open-ended buying of mortgage bonds the Fed launched last month will be adjusted as necessary. "We will continue buying mortgage-backed securities until the job market looks substantially healthier," he said, adding "we might even expand our purchases to include other assets" if that seems like an effective way to spur better activity levels. Mr. Williams, a voting member of the policy-making Federal Open Market Committee, spoke at a meeting of the Financial Women's Association of San Francisco. A vocal supporter of the Fed's efforts to get the economy back on track, he said Fed policy "cannot solve all our economic problems," but it can help speed the pace of recovery and get our economy back on track sooner." He forecast that real gross domestic product to expand at a "modest" 1.75% or so this year, but improve to 2.5% next year and 3.25% in 2014. Unemployment he sees falling by the end of 2014 to 7.25%, from the current 7.8%, with inflation staying "slightly below" 2% for the next several years, in an absence of labor-cost pressure. Even with the aggressive action taken by the Fed, which includes a conditional pledge to keep rates very low until the middle of 2015, Mr. Williams said "in no way has our commitment to price stability wavered." He added "if we find that our policies aren't doing what we want or are causing significant economic problems, we will adjust or end them as appropriate."

Fed’s Dudley: Policy Will Stay Aggressive Even When Growth Picks Up - The Federal Reserve will keep policy aggressively easy even when the pace of the recovery accelerates, a key central bank official said Monday, given that evidence now suggests past policy actions weren’t aggressive enough in responding to the financial crisis. “If we were to see some good news on growth I would not expect us to respond in a hasty manner” and begin tightening monetary policy, Federal Reserve Bank of New York President William Dudley said in a speech Monday. “Only as we became confident that the recovery was securely established, would I expect our monetary policy stance to evolve to ensure that it remained appropriate to achievement of our objective: maximum sustainable employment in the context of price stability,” the official said.

Fed’s Dudley and Plosser Spar Over Unwinding Risks - The Federal Reserve may be in the stimulus game for several years to come, but that doesn’t mean officials are done talking about how they are going to unwind all the liquidity they have provided to the economy. Over recent days, two key Fed regional bank leaders, New York’s William Dudley and Philadelphia’s Charles Plosser, have spoken in detail about the eventual policy rollback. Just as the two have very different outlooks on the need for continued monetary policy stimulus, their views on the ease of the unwind are somewhat at odds. It may seem jarring to hear the officials talk about tightening policy when the central bank’s easy stance is likely to prevail for years to come. The Fed decided only last month to launch an open-ended mortgage bond buying program that will surely push its balance sheet well beyond the current nearly $3 trillion mark, versus around $800 billion in late 2007. What’s more, the central bank has said it expects short-term rates to remain near zero until the middle of 2015.

Why Unwinding QE Won't Matter - Ashwin Parameswaran nails it once again. If you want to understand how the modern financial/monetary system actually works, run don’t walk to read this post. His key insight: Just as the East India Company could access cash on the back of their government bond holdings in the 18th century, any pension fund, insurer or bank can do the same today. Let me translate that into my words: If the CB unwinds QE by trading bonds for “money,” “sopping up” “cash” (those are all “so-called” quotes) from the private sector, the private bond-holders can just use those bonds as collateral to get (new) cash loans. Commercial and shadow banks will create (“counterfeit”) the new money under (explicit or implicit) license from the central bank, and deposit the money into the bondholders’ accounts. Result: roughly the same amount of “cash” in the system. In other words: …the private sector can monetize the deficit as effectively as the central bank can. Hence:…the reversal of QE, if and when it happens, will have no impact on economy-wide access to cash/purchasing power. This also serves to explain why QE may not have had as much effect as one might hope. The Fed gave bondholders cash in return for their bonds, so bondholders ended up with more cash but less collaterizable/monetizable/convertible-to-cash bonds. A wash?

Should Central Banks Burn All Their Government Bonds? - In June of 2008, Ron Paul made a radical proposal: the Fed should simply burn all the U.S. Treasuries it’s currently holding, reducing the government (U.S. Treasury) debt by $1.6 trillion, or about 10%. (Yes: bonds held by the Fed are counted as part of “Debt Held by the Public,” even though the government basically “owns” the Fed.) Paul called this “bankruptcy,” but it’s actually pure MMT thinking, acknowledging that 1. the Fed and the Treasury are most reasonably viewed as a single consolidated entity (“the government”), and 2. that government debt is something of a side issue in the big monetary picture (bonds are a vehicle for interest-rate management by the Fed), compared to the matter of central importance: how much newly created money the government puts into the economy by deficit spending, or takes out with a surplus (destroying more money by taxing than it creates by spending). This is pretty radical talk, for sure. (I wonder if Paul and Kucinich ever eat lunch together.) But now Gavyn Davies tells us in the Financial Times that such notions are at least floating about in some decidedly traditional circles (emphasis mine): Two separate journalists (Robert Peston of the BBC and Simon Jenkins of The Guardian) said that Lord Turner’s “private view” is that some part of the Bank’s gilts holdings might be cancelled in order to boost the economy. Lord Turner distanced himself in public from this suggestion on Saturday. However, the notion will now be widely discussed. It is easy to see how the idea could appeal to a finance minister facing the need to tighten fiscal policy during a recession in order to bring down the public debt ratio. [that's "Adair Turner, the Chairman of the UK Financial Services Agency, and reportedly a candidate to become the next Governor of the Bank of England."]

Guest Post: Should Central Banks Cancel Government Debt? - Readers may recall that Ron Paul once surprised everyone with a seemingly very elegant proposal to bring the debt ceiling wrangle to a close. If you're all so worried about the federal deficit and the debt ceiling, so Paul asked, then why doesn't the treasury simply cancel the treasury bonds held by the Fed? After all, the Fed is a government organization as well, so it could well be argued that the government literally owes the money to itself. He even introduced a bill which if adopted, would have led to the cancellation of $1.6 trillion in federal debt held by the Fed. Of course the proposal was not really meant to be taken serious: rather, it was meant to highlight the absurdities of the modern-day monetary system. In a way, we would actually not necessarily be entirely inimical to the idea, for similar reasons Ron Paul had in mind: it would no doubt speed up the inevitable demise of the fiat money system. Control can be lost, and it usually happens only after a considerable period of time during which their interventions appear to have no ill effects if looked at only superficially: “Thus we learn….to be ignorant of political economy is to allow ourselves to be dazzled by the immediate effect of a phenomenon."

Helicopter Money Drop -A helicopter money drop is a form of monetary policy in which a Central Bank prints money and distributes it directly to households / consumers. The aim of helicopter money is to boost nominal GDP, overcome deflation and help reduce unemployment. In normal circumstances printing money will be inflationary. Economists usually suggest helicopter money in a liquidity trap and period of deflation. The idea of a ‘helicopter money has been referred to by Milton Friedman and picked up by the Chairman of the Federal Reserve, Ben Bernanke. One image of ‘helicopter money is a helicopter dropping cash from the sky, which presumably would be picked up and spent pretty quick. On a more practical vein, it could involve the Central Bank sending a cheque in the post to people across the country. In a period of severe deflation, the cash sent could even have an expiry date. Meaning you have to spend it in 6 months or lose it. This expiry date will prevent people just saving it.

The Only Game in Town - What should central banks do when politicians seem incapable of acting? Thus far, central banks have been willing to step into the breach, finding new and increasingly unconventional ways to try to influence the direction of troubled economies. But how can we judge when central banks overstep their limits? When does boldness turn to foolhardiness?Central banks can play an important role in a cyclical downturn. Interest-rate cuts can boost borrowing – and thus spending on investment and consumption. Central banks can also play a role when financial markets freeze up. By offering to lend freely against collateral, they “liquify” assets and prevent banks from being forced to unload loans or securities at fire-sale prices. Anticipating such liquidity insurance, banks can make illiquid long-term loans or hold other illiquid financial assets. To the extent that unconventional monetary policy – including various forms of quantitative easing, as well as pronouncements about keeping interest rates low for a long time – serves these roles, it might be justified. Other unconventional policies, however, have been undertaken to stimulate the economy, rather than to deal with broken markets. The benefits have been commensurately smaller. QE2, in which the Fed bought long-term government bonds, did not have a discernible effect on long-term government interest rates. Indeed, with its recent decision to pursue QE3, the Fed is focusing once again on the mortgage-backed securities market; but, given that the market is much healthier now, it is unclear how much good this will do.

Housing Recovery May Validate Fed’s QE3 - Legitimate signs of life in the housing market suggest the Federal Reserve may have chosen the right lever to stimulate the economy when it launched its latest stimulus bid last month. In September, officials on the monetary policy-setting Federal Open Market Committee decided to embark on an open-ended program of mortgage bond buying, in an effort that will increase what is now a nearly $3 trillion central bank balance sheet. The purchases follow in the tracks carved out by past asset-buying efforts, which had relied more heavily on the purchase of Treasurys. Many Fed officials reckon that as the housing market’s problems have been a big reason why the recovery has been so tepid, targeting the sector with direct aid can make a big difference for the broader economy. Policymakers hope positive housing momentum will help overall activity rise, which in turn should help boost job growth and lower unemployment. An increasing amount of data suggests the Fed may indeed have targeted the right part of the economy for assistance. On Wednesday, the government reported that new home-building levels surged to a four-year high last month, amid a nearly 12% rise in new building permits. While the rise in activity is not attributable to the new Fed stimulus, it owes in part to past stimulus by the central bank. The central bank “does deserve a lot of the credit” for creating the conditions that are allowing the housing market to get itself back on track.

Fed Watch: Buyer's Remorse? - In the near-term, the upbeat news will have limited impact on monetary policy. The Fed will remain committed to the path laid out at the last FOMC meeting. That said, I have to imagine some of the moderates on the FOMC - those pulled into Federal Reserve Chairman Ben Bernanke's gravity with the softening of data this summer - will be starting to feel a little bit of buyer's remorse, thinking that maybe, just maybe, they pulled the trigger a little too soon. The doves, of course, should be ecstatic that the FOMC locked in an easier policy at beginning of an upswing. Rather than threatening to withdraw stimulus at the slightest sign of recovery, now we have a commitment to keep monetary momentum until the economy is clearly on firmer ground. This will be supportive of the upswing in activity. The death of the consumer continues to be more myth than reality. The retail sales report revealed that households have shaken off the summer doldrums: While the year over year trend is not particularly strong: the last three months have packed a bit of a punch: While industrial production was up somewhat, the trend over the past year is basically flat: The underlying story, I think, remains two-fold. First, some investment was likely pulled forward into 2011 by now-expired tax credits. Second, the global slowdown is also weighing on manufacturing growth. That said, note that the current scenario continues to look more like 1998 than 2008: To be sure, core new orders have been a little unnerving of late, and certainly something to watch. But this would not be the first time that an external shock failed to deliver a US recession. For now, I expect that to continue to be the case. And one reason to believe that the US will escape recession is the obviously improving housing market. Starts exceeded expectations in September:

Romney is shocked to learn how the Fed creates money - By William K. Black - The following passage from the transcript of Governor Romney’s secretly videotaped May 17, 2012 fundraiser has not received any attention in the media. It is a fascinating passage, however, from the perspective of Modern Monetary Theory (MMT). Here is the full context of the passage: ROMNEY: Yeah. Yeah. It’s– it’s interesting. There’s– the former head of– Goldman Sachs, John Whitehead– was also the former head of the New York Federal Reserve and– and I met with him and he said, “As soon as the Fed stops buying all the debt that we’re issuing–” which they’ve been doing. The Feds buy like 3/4 of the debt that America issues.He said, “Once– once that over– that’s over,” he said, “we’re gonna have a failed Treasury option. Interest rates are gonna have to go up. You know, we’re– we’re– we’re living in this borrowed– fantasy world where– where the government keeps on borrowing money.” You know, we– we borrow this extra trillion a year. We wonder, “Well, who’s– who’s loaning against the Treasury? The Chinese aren’t loaning to us anymore. The Russians aren’t loaning it to us anymore. So who’s giving us a trillion?” And the answer is we’re just making it up. The Federal Reserve is– is just taking it and saying, “Here, we’re– we’re giving–” it’s just made up money. And– and this– this does not augur well– for– for our economic future. No. I mean I– you know, some of these things are– are complex enough it’s not easy for people to understand, but your– your point of saying bankruptcy usually concentrates the money. Yeah, George?

How Romney could end quantitative easing - To belabour the obvious, the Federal Reserve and monetary policy are critical to any president’s success; presidential elections are usually determined by the state of the economy and the Fed has a great deal to do with that, arguably never more so than today. Many observers believe that President Obama hurt himself by taking a somewhat lackadaisical attitude toward the Fed – leaving positions on the Fed board vacant for long periods, not moving quickly to appoint replacements and failing to back away from appointees that ran into Senate confirmation difficulties. Were he elected it is unlikely that Mitt Romney will make the same mistakes. I expect that he will move quickly to put his stamp on the Fed. So what can we expect? Republicans in Congress have been highly critical of Fed policy, especially the episodes of “quantitative easing” that took place in 2009, 2010 and again this year. Despite the continuing lack of inflation in the price data, Republicans believe that quantitative easing is highly inflationary and should be reversed as soon as possible. Mr Romney will have an immediate opportunity to encourage a move in that direction. Among the many responsibilities of the president is making appointments to the seven member Federal Reserve Board, which must also be confirmed by the US Senate. Members seldom complete their entire 14-year terms creating opportunities for additional appointments to fill unexpired terms. The critical position of chairman of the Fed is one to which an existing member must be separately appointed and confirmed to a 4-year term.

Monetary Policy under Obama and Romney – Macroadvisers - The outcome of this election will almost certainly affect the conduct of monetary policy.

- We assume that, if President Obama is re-elected and Ben Bernanke does not seek or is not offered another term, Janet Yellen will be nominated to be Chair of the Federal Reserve Board (and thus also of the FOMC).

- If Governor Romney is elected, he will most likely nominate one of his two principal economic advisers: Glenn Hubbard or Greg Mankiw. John Taylor, another adviser, would surely also be on the short list.

- We have previously distinguished between dovish and hawkish rules.

- Dovish rules portray recent and current policy as restrictive, notwithstanding the prevailing near-zero funds rate. Hawkish rules portray policy today as too stimulative.

- Dovish rules embed a much more aggressive response to departures from full employment than do hawkish rules.

- Dovish rules prescribe a later first rate hike than do hawkish rules.

- Taylor is unquestionably the most hawkish. His rule embeds a modest response to departures from full employment. The FOMC would already have raised rates under his rule.

- Yellen is the most dovish. Based on her rule, policy should respond aggressively to departures from full employment, and the first rate hike would still be two years away.

- Mankiw is somewhere in between. While his rule, like Taylor's, allows for only a modest response to departures from full employment, it nevertheless prescribes a later first rate hike that is still one year away.

- While Glenn Hubbard has not written down a rule, his recent comments reveal that he is not as hawkish as Taylor, not as dovish as Yellen, but likely somewhat more hawkish than Mankiw.

Why US Monetary Policy is Too Tight -- An excellent op-ed by Doug Irwin on why US monetary policy is too tight: The Divisia M3 and M4 figures for the US money supply, calculated by the Center for Financial Stability, show that the money supply is no higher today than in early 2008. For all the fretting about the Fed’s accommodative policy, the money supply has barely increased and is way off its previous trend. This represents a very tight policy compared to Friedman’s rule that growth in the money supply should be limited to a constant percentage. The lack of growth in the money supply is an important reason why US inflation and inflationary expectations remain under control. The Federal Reserve Bank of Cleveland’s latest market-based estimate of the 10-year expected inflation rate is 1.32 per cent.

Key Measures show low inflation in September - The Cleveland Fed released the median CPI and the trimmed-mean CPI this morning: According to the Federal Reserve Bank of Cleveland, the median Consumer Price Index rose 0.2% (2.6% annualized rate) in September. The 16% trimmed-mean Consumer Price Index increased 0.2% (2.6% annualized rate) during the month. The median CPI and 16% trimmed-mean CPI are measures of core inflation calculated by the Federal Reserve Bank of Cleveland based on data released in the Bureau of Labor Statistics' (BLS) monthly CPI report. Earlier today, the BLS reported that the seasonally adjusted CPI for all urban consumers rose 0.6% (7.1% annualized rate) in September. The CPI less food and energy increased 0.1% (1.8% annualized rate) on a seasonally adjusted basis.Note: The Cleveland Fed has the median CPI details for September here.This graph shows the year-over-year change for these four key measures of inflation. On a year-over-year basis, the median CPI rose 2.3%, the trimmed-mean CPI rose 1.9%, and core CPI rose 2.0%. Core PCE is for August and increased 1.6% year-over-year. On a monthly basis, two of these measure were above the Fed's target; trimmed-mean CPI was at 2.6% annualized, median CPI was at 2.6% annualized. However core CPI increased 1.8% annualized, and core PCE for August increased 1.3% annualized. These measures suggest inflation is close to the Fed's target of 2% on a year-over-year basis.

Two Measures of Inflation: New Update - The BLS's Consumer Price Index for September, released today, shows core inflation fractionally at teh Federal Reserve's 2% target at 1.98%. Core PCE, at the end of last month, is further below the target at 1.58%. The Fed is on record as preferring Core PCE as its inflation gauge: This close-up comparison gives us a clue as to why the Federal Reserve prefers Core PCE over Core CPI as an indicator of its success in managing inflation: Core PCE is lower than Core CPI and less volatile. Given the Fed's twin mandates of price stability and maximizing employment, it's not surprising that the less volatile Core PCE is their metric of choice.The Bureau of Labor Statistic's Consumer Price Index and The Bureau of Economic Analysis's monthly Personal Income and Outlays report are the main indicators for price trends in the U.S. The chart below is an overlay of core CPI and core PCE since 2000. For some technical data explaining the differences between the calculation of PCE and CPI, see this comparison article from the BEA. In the real world we can't exclude food and energy from our monthly expenses. But the extreme volatility of these two expense categories, especially energy, often obscures the underlying trend, which is the focus of the chart above. For evidence of the volatility, see this overlay of headline and core CPI and this one of headline and core PCE.

High Unemployment Points to Below-Target (But Still Stable) Inflation - Dallas Fed: The Federal Reserve has a mandate to promote price stability and full employment. Generally, “price stability” is given a forward-looking interpretation. Policy should be conducted so that expected medium-term (two- to five-year) inflation is low and stable or, less strictly, so that expected inflation beyond the next few years is low and stable.[1] Households and businesses, too, are generally more interested in where prices are headed than in where they have been. How best to forecast inflation is controversial. Many analysts have assumed that changes in inflation depend on the amount of labor market slack: Inflation tends to rise when the unemployment rate is low and to fall when it is high. It follows that you cannot reduce inflation without going through a period of higher-than-normal unemployment. Others, however, believe that slack—at least as we usually measure it—doesn’t matter: The best predictor of future inflation is current inflation. It appears that both of these views oversimplify. Neither is a good approximation over the past 15 years—a period that has been characterized by remarkable stability in long-term inflation expectations. Our research carries the implication that should this stability be maintained, the current high unemployment rate means that inflation is likely to run somewhat below 2 percent in the coming year. It does not mean, however, that we can expect ongoing declines in inflation.

Poll: Economists Foresee Weak but Improving Growth — Economists foresee only tepid growth for the coming year, with unemployment back above 8 percent for the first half of 2013. The good news: The housing market is recovering faster than expected and the economy likely won’t fall off a “fiscal cliff.” The quarterly survey by the National Association for Business Economists released Monday predicts growth will be weak overall but should slowly accelerate through 2013. The 44 economists surveyed now see gross domestic product – the value of all goods and services produced in the United States – rising just 1.9 percent in 2012 before reaching a 3 percent pace by the fourth quarter of next year. Employment growth is forecast to weaken. The panel predicts that the unemployment rate will rise to 8.1 percent by the end of the year. The economy should add an average of 125,000 jobs per month during the fourth quarter, down from the economists’ May forecast of 190,000 jobs.

Economists Polled on the Pre-Election Economy - A survey of economists is published in the November 2012 issue of Foreign Policy. One question was whether we thought that the US unemployment rate would dip below 8.0% before the election. When the FP conducted the poll at the end of the summer, unemployment was 8.1-8.2%. Now it’s 7.8%. Only 8% of the respondents said “yes.” (I was one. I basically just extrapolated the trend of the last two years.) My fellow economists choose defense and agricultural subsidies as the two categories of US federal spending that they think the best to cut. They rate the euro crisis as the greatest threat to the world economy now and are particularly worried about Spain. For a slideshow presentation of the results, see “The FP Survey: The Economy.” Or in a magazine format: “If we’re ever going to get out of this slump, what will it take? We asked more than 60 leading economists to tell us.” Also, here is a recent poll from The Economist, asking similar questions of NBER and NABE economists: “Asking the Experts,” Oct. 6.

Recession Trends – Stanford -The sixteen selected domains cover the most important economic and social institutions in the U.S. In choosing them, our goal was simply to cover the major institutions of interest, not necessarily to single out those especially affected by the downturn. We rehearse below some of the core questions underlying the Recession Briefs within each domain.

- Income, Wealth, and Debt

- Consumption and Savings

- Labor Markets

- Housing

- Poverty

- Social Safety Net

- State Budgets

- Family and the Lifecourse

- Health and Mental Health

- Education

- Crime

- Immigration

- Political and Public Opinion

- Charitable Giving

- Retirement

- Communities

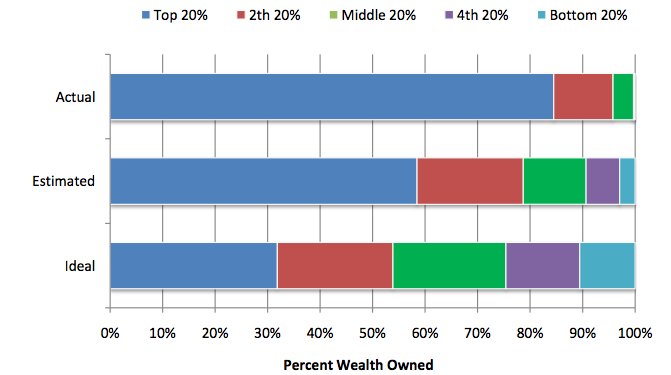

GDP, Prosperity, The Wealth Effect, and Marginal Propensity to Consume - It comes to mind as I ponder the rather grudging and tepid suggestions that you hear here and there these days — that excessive inequality might actually be a drag on economic growth and prosperity. There are some full-throated assertions of this belief out there, but in the mainstream economics community they are rare and in general quite decidedly mealy-mouthed. The general failure to question the “more inequality is good for growth” mantra has deep roots, even among progressive economists. Viz, this from Paul Krugman back in December, 2008, when the highest inequality since The Great Depression was was in the process of delivering the first (at least potential) depression since…The Great Depression (bold mine):There’s no obvious reason why consumer demand can’t be sustained by the spending of the upper class — $200 dinners and luxury hotels create jobs, the same way that fast food dinners and Motel 6s do. In fact, the prosperity of New York City in the last decade — largely supported off of super-salaried Wall Street types — is a demonstration that you can have an economy sustained by the big spending of the few rather than the modest spending of large numbers of people. This seems to completely ignore marginal propensity to consume (MPC) — that poorer people spend a larger percentage of their income than rich people, so a more equal income distribution would result in higher money velocity, hence higher GDP. But I’d like to suggest that the problem runs deeper. Almost all the thinking about MPC seems to obsess about income, and greatly downplay the role of wealth, or net worth. This failure to consider wealth is important because wealth inequality in this country (and worldwide) utterly dwarfs income inequality.

Conference Board LEI: ''Fluctuating Around a Slow-Growth Trend'' - The Conference Board Leading Economic Index (LEI) for August was released this morning. The index increased 0.6 percent in September to 95.9 (2004 = 100), following a 0.4 percent decline in August, and a 0.4 percent increase in July. The Briefing.com consensus had been for 0.2 percent. "Fluctuating around a slow-growth trend" is the summary phrase from today's press release, an upgrade from last month's "fluctuating around a flat trend." Here is the overview of today's release from the LEI technical notes: The Conference Board LEI for the U.S. increased in September after declining in the previous month. Large positive contributions from building permits and the financial components offset the negative contributions from ISM® new orders index, consumer expectations for business conditions and weekly initial claims for unemployment insurance (inverted). In the six-month period ending September 2012, the leading economic index increased 0.3 percent (about a 0.6 percent annual rate), much slower than the growth of 2.6 percent (about a 5.2 percent annual rate) during the previous six months. In addition, the strengths and weaknesses among the leading indicators have become balanced in recent months. [Full notes in PDF format] Here is a chart of the LEI series with documented recessions as identified by the NBER. And here is a closer look at this indicator since 2000. We can more readily see that the recovery from the 2000 trough has been more or less flatlining in recent months.

Downside Risks - Occasionally, over the last several years, I've posted a list of downside risks to economic growth - and here is another one. Currently my forecast is still for sluggish and choppy growth, but I think there are reasons to expect US economic growth to pickup in the next year or two, perhaps to trend growth. As I noted last month in Two Reasons to expect Economic Growth to Increase, residential investment is now a tailwind for the economy, and the drag from state and local government cutbacks is mostly behind us. There are always many downside risks (meteor strikes, major terrorist attack, war somewhere - possibly with Iran), but I think these are the most probable downside risks:

• The European financial crisis. The European crisis has been threatening to spill over into the US for several years. Looking back, I was writing about Greece, Ireland and Spain sovereign debt issues in 2009. This year the recession in Europe is hitting US exports, but so far there is little financial contagion..

• The economic slowdown in China. The recession in Europe has spilled over into China, and has led to fears of a sharp slowdown. From the WSJ: China's Growth Continues to Slow Growth in China's gross domestic product fell to 7.4% in the third quarter compared with a year earlier, China's National Bureau of Statistics said Thursday, down from 7.6% in the second quarter and the weakest since the beginning of 2009.

• The Fiscal Slope. This is commonly called the "fiscal cliff", but it is more of a slope. This refers to several federal tax increases and spending cuts that are scheduled to happen at the beginning of 2013. This includes ending the Bush-era tax cuts, ending the temporary payroll tax reduction, ending extended unemployment benefits, and some large budget cuts mostly for defense spending. No one expect this to be resolved before the election, but after the election this could become a significant issue.

Debate Rages Over Recoveries From Financial Crises - While the presidential candidates battle over the Obama administration’s handling of the U.S. economy, some prominent economists are going to war over a related subject. At issue: Should the economy be expected to bounce back quickly or slowly after a financial crisis? Economists Carmen Reinhart and Kenneth Rogoff of Harvard University have been saying for several years that the answer is ‘Slowly.’ The Obama administration has leaned on their book, “This Time Is Different,” to argue that it isn’t to blame for the dismal economic recovery. The book was in the works before Mr. Obama took office. In it, the economists studied 224 banking crises spread out over several centuries and across different countries and found that recoveries after a financial shock tend to be tepid, with financial institutions and government budget emerging from the crisis strained. Rutgers University economic historian Michael Bordo and Cleveland Fed economist Joseph Haubrich studied just U.S. recessions going back to 1882 and found that U.S. recoveries following financial shocks tend to be rapid. Top economic advisers to Republican Mitt Romney have leaned on this research to argue that the culprit in the current slow recovery is Mr. Obama himself, not the financial crisis that preceded him. This line of research has taken issue with the Reinhart and Rogoff studies, arguing, among other things, that U.S. crises can’t be likened to financial crises that have happened elsewhere in the world — such as small developing markets – because their economic institutions are so different.

Sorry, U.S. Recoveries Really Aren’t Different - Carmen M. Reinhart and Kenneth S. Rogoff - Five years after the onset of the 2007 subprime financial crisis, U.S. gross domestic product per capita remains below its initial level. Unemployment, though down from its peak, is still about 8 percent. Rather than the V- shaped recovery that is typical of most postwar recessions, this one has exhibited slow and halting growth. This disappointing performance shouldn’t be surprising. We have presented evidence that recessions associated with systemic banking crises tend to be deep and protracted and that this pattern is evident across both history and countries. Subsequent academic research using different approaches and samples has found similar results. Recently, however, a few op-ed writers have argued that, in fact, the U.S. is “different” and that international comparisons aren’t relevant because of profound institutional differences from one country to another. Some of these authors, including Kevin Hassett, Glenn Hubbard and John Taylor -- who are advisers to the Republican presidential nominee, Mitt Romney, have stressed that the U.S. is also “different” in that its recoveries from recessions associated with financial crises have been rapid and strong. We have not publicly supported or privately advised either campaign. We well appreciate that during elections, academic economists sometimes become advocates. It is entirely reasonable for a scholar, in that role, to try to argue that a candidate has a better economic program that will benefit the country in the future. But when it comes to assessing U.S. financial history, the license for advocacy becomes more limited, and we have to take issue with gross misinterpretations of the facts.

Bubble, Bubble, Conceptual Trouble -- Krugman - We’re living in the aftermath of a major financial crisis. Reinhart-Rogoff warned in advance that recovery was likely to be slow; so, with less historical detail, did I. And so it has proved. But based on the discussion I’ve heard, both on the blogs and in forums like that House of Commons debate Monday, there’s a lot of confusion even among economists about what the pattern of slow recovery from financial crisis is really telling us. Basically, there seems to be a confusion between saying that something is usual and saying that it is necessary. Those aren’t the same thing. Here’s how I interpret what we see in the historical data: financial crises leave an overhang of private-sector problems, principally excessive debt on the part of some subset of economic agents — households, in the case of the United States. Because these agents are either forced or strongly induced to slash spending, the “natural” rate of interest, the interest rate consistent with full employment, falls sharply — and in the case of a severe crisis, falls well below zero. What this means in turn is that conventional monetary policy, which normally bears most of the burden of economic stabilization, is no longer up to the job.

Is overregulation contributing to slow recovery in the US? - John Taylor makes an interesting point on his blog (here) with respect to the bloated government regulation in the US. Here are two charts that compare the recovery from the recession in the early 80s (during the Reagan administration) with the current economic recovery. One trend that really stands out is the number of federal workers employed in regulatory activities (excluding transportation security). The two trends are drastically different. It shows how the US regulatory framework is becoming in many ways similar to the European governments' tactics. Regulate it all, ask questions later. Below is a comparison of the quarterly GDP during the two recoveries. Of course this could simply be a coincidence, but is it?

Weak Recovery Denial - Paul Krugman disagrees with my recent post that the recovery is weak compared to recoveries from past serious U.S. recessions including those associated with financial crises. In making his critique, Krugman appeals to a recent oped in Bloomberg View by Carmen Reinhart and Ken Rogoff who criticize the research of economic historian Michael Bordo and his coauthor Joseph Haubrich of the Cleveland Fed, which I have referred to. Bordo and Haubrich demonstrate that the recovery from the recent recession and financial crisis has been unusually weak compared to recoveries from past recessions with financial crises in the United States. In separate research, Jerry Dwyer and Jim Lothian report the same finding. Neither Reinhart-Rogoff nor Krugman disprove this finding. First, they argue for a narrower definition of a financial crisis. Reinhart and Rogoff say that one should “distinguish systemic financial crises from more minor ones and from regular business cycles.” Thus they exclude some cases studied by Bordo and Haubrich. But narrowing the focus to systemic crises in this way does not change the Bordo-Haubrich findings because the recovery from the recent recession is weaker than the average of past recessions cum financial crises even with these exclusions. Second, Reinhart and Rogoff argue that one should look at recessions together with recoveries when looking at severity. In fact, in their work they explicitly “don’t delineate between the ‘recession’ period and the ‘recovery’ period.”

Income Inequality May Take Toll on Growth - Income inequality has soared to the highest levels since the Great Depression, and the recession has done little to reverse the trend, with the top 1 percent of earners taking 93 percent of the income gains in the first full year of the recovery. The yawning gap between the haves and the have-nots — and the political questions that gap has raised about the plight of the middle class — has given rise to anti-Wall Street sentiment and animated the presidential campaign. Now, a growing body of economic research suggests that it might mean lower levels of economic growth and slower job creation in the years ahead, as well. “Growth becomes more fragile” in countries with high levels of inequality like the United States, said Jonathan D. Ostry of the International Monetary Fund, whose research suggests that the widening disparity since the 1980s might shorten the nation’s economic expansions by as much as a third. Reducing inequality and bolstering growth, in the long run, might be “two sides of the same coin,” research published last year by the I.M.F. concluded. Since the 1980s, rich households in the United States have earned a larger and larger share of overall income. The 1 percent earns about one-sixth of all income and the top 10 percent about half, according to statistics compiled by the respected economists Emmanuel Saez and Thomas Piketty.

Shrink Inequality to Grow the Economy? - Room for Debate - The International Monetary Fund and others say that income inequality represses economic growth, and is not simply a byproduct of growth. To expand the economy, should the United States enact policies to address inequality? And if so, what initiatives would promote growth and reduce the income gap?

- Political Causes, Political Solutions Joseph E. Stiglitz, Nobel laureate

- A Big Gap Means There Is Room to Move Up - Diana Furchtgott-Roth, Manhattan Institute

- Working Harder, and Earning Less Michael C. Dawson, author, "Not In Our Lifetimes: The Future of Black Politics"

- All Will Benefit If More Are Secure Jacob S. Hacker, Yale University political science professor and Nathaniel Loewentheil, Yale Law School

- Inequality Is Not What We Imagine - Scott Winship, Brookings Institution

- We Need Latin American Style Affirmative Action Tanya Katerí Hernández, Fordham Law School

- Revive Labor’s Power Timothy Noah, Author, "The Great Divergence''

- Train Americans to Make Their Own Safety Nets Douglas Holtz-Eakin, American Action Forum

- When Too Many People Are in Prison Tehama Lopez Bunyasi, political scientist, Ohio University

US runs a 4th straight $1 trillion-plus budget gap - The United States has now spent $1 trillion more than it's taken in for four straight years. The Treasury Department confirmed Friday what was widely expected: The deficit for the just-ended 2012 budget year — the gap between the government's tax revenue and its spending — totaled $1.1 trillion. Put simply, that's how much the government had to borrow. It wasn't quite as ugly as last year. Tax revenue rose 6.4 percent from 2011 to $2.45 trillion. And spending fell 1.7 percent to $3.5 trillion. As a result, the deficit shrank 16 percent, or $207 billion. Debt piles up, year after year. It's reached $11.3 trillion — $16.2 trillion if you include money the government has borrowed from itself, mostly revenue from Social Security. Unless something changes, the Congressional Budget Office warns, the federal debt would reach a level that is "unsustainable from both a budgetary and an economic perspective." Over time, big government debts can damage the economy. The economists Kenneth Rogoff of Harvard University and Carmen Reinhart of the Peterson Institute for International Economics have found that growth tends to slow sharply once national government debt reaches 90 percent of GDP.

Treasury Yields/Mortgage Update: Yields Rise, 30-Year Mortgage Falls - I've updated the charts through today's close. Here is a snapshot of selected yields and the 30-year fixed mortgage one week after the Fed announced its latest round of Quantitative Easing. The 30-year fixed mortgage at the current level no doubt suits the Fed just fine, and the low yields have certainly reduced the pain of Uncle Sam's interest payments on Treasuries (although the yields are up from their recent historic lows). But, as for loans to small businesses, the Fed strategy continues to be a solution to a non-problem. The first chart shows the daily performance of several Treasuries and the Fed Funds Rate (FFR) since 2007. The source for the yields is the Daily Treasury Yield Curve Rates from the US Department of the Treasury and the New York Fed's website for the FFR.

Foreign holdings of US debt hit record $5.43T — Foreign demand for U.S. Treasury securities rose to a record level in August, further evidence that most nations see U.S. debt as a safe investment. The Treasury Department says total foreign holdings rose to a record $5.43 trillion in August. That's up 1.5 percent from the July level. China, the largest foreign holder of U.S. debt, increased its holdings 0.4 percent to $1.15 trillion. And Japan increased its holdings 0.5 percent to $1.12 billion. Japan now trails China's holdings by just $32.1 billion. Demand for U.S. debt has remained high even though the United States has run budget deficits in excess of $1 trillion for the past four years. Many foreign investors see U.S. debt as a safe investment with Europe in crisis and global growth slowing.

China Continues To Boycott Treasurys As Japan Prepares To Become Largest Foreign Holder Of US Paper - Where there were notable developments in today's TIC report, was in the composition of buyers of US paper, which showed that for yet another month, there has been virtually no buying interest in US paper by the biggest non-Fed holder: China, whose total TSY holdings were $1,154 billion, down $12 billion since the beginning of the year, and down a whopping $125 billion from a year ago. Ironically that other massively indebted country, Japan, which has Y1 quadrillion in its own public debt to deal with, for a debt/GDP ratio will above 200%, continues to load up on US paper, as the biggest paper ponzi scheme continues going ever higher and nothing possibly can get in the way. In fact, as the chart below shows, the difference between total Chinese and Japanese holdings has declined to a record low $32 billion, and will likely see Japan surpass China as the biggest holder of US paper very soon.

Debt and the burden on future generations - I don't want to bore people, but once again this question has come up (see here, here, here, here, here, here, and here for the whole battle royale) , and I thought I'd blog about it, because hey, every econ blog should occasionally do some little "thought experiment" type stuff, even if it doesn't quite as much traffic as does making fun of commenters. The question, once again, is: "Does government debt impose a burden on future generations?" I took a crack at this question back in January, and my answer is still the same, but I'd like to phrase it more concretely. Here's how I like to think about this question. In my mind, to "impose a burden on future generations" means "to decrease the consumption possibilities of future generations". So the question is really whether or not the size of today's stock of government debt reduces the total consumption possibilities of people not currently born. In other words, if government debt is $1,000,000,000 today, does that mean that the consumption of future people must be lower than if government debt were $1 today?

Final Thoughts on the Baker-Rowe-DeLong-Krugman Deficit Debate - Dean Baker - After having provoked a debate that subsequently involved Nick Rowe, Brad DeLong and Paul Krugman, I will assert blogowners’ privilege and throw out some summary thoughts. First, we all seem to agree that in a situation where the economy is clearly operating well below its potential, governments can run deficits to boost employment and output. I believe we all agree that in principle the government can also use these deficits to increase future output through productive investment in either physical or human capital. This would make future generations better off on net as a result of deficits today, since the economy will be larger than it would be without the deficits. I would also add, without necessarily implicating anyone else, that simply by increasing output and employment the government is likely to make society better off in the future for two reasons. First, by keeping people employed we will keep them attached to the labor force and reduce the number of hard core unemployed who would be difficult to re-employ in subsequent years, possibly leaving us with a higher rate of unemployment (and lower output) long into the future. The other reason that short-term increases in employment can have long-term effects is that by keeping families intact, children are likely to have better upbringings and do better in school. This means that the next generation will on average will have happier more productive lives because we used deficits to keep their parents employed today.

Foreigners and the Burden of Debt - Paul Krugman - A number of comments on my non-burden of the debt post were along the lines of “But what if the debt is owed to foreigners?” OK, this takes a bit more thinking. Another thought experiment: suppose that for some reason the Chinese and a bunch of domestic investors do an asset swap: the Chinese sell off $500 billion of Treasuries and buy an equal amount of, say, corporate bonds, while the domestic investors do the reverse. Has America become any richer (or any poorer)? Obviously not — as a nation we still owe the same amount to the rest of the world. What this tells us is that when we’re trying to assess the burden or lack thereof of debt, foreign ownership of government debt doesn’t really matter. What does matter is our net international investment position, the value of the overseas assets owned by all domestic residents minus the value of all domestic assets owned by foreign residents.. Now, this ties right in with what Brad said about the burden of the debt: we’d all agree that deficits make us poorer if they crowd out investment spending — which they would if the economy were near full employment, but won’t if we’re deeply depressed. All we have to do is realize that net foreign investment — purchases minus sales of assets from and to foreigners — is also a form of investment. Or to put it a bit more simply, sure, budget deficits can make us poorer as a nation if they lead to bigger trade deficits. So far, nothing like this has happened. Here’s the U.S. budget deficit (all levels of government) and the current account deficit, both as a percentage of GDP:

The Burden of Government Debt - The recent ‘exchange’ on this topic (see Nick Rowe here, here, here and here, and apparently on the other side Dean Baker, Brad DeLong, Paul Krugman and Noah Smith) may just have confused many, so here is my attempt to unconfuse. I’m doing this because (a) the issue is tricky (as I know from my own experience) (b) I’ve written about this before (c) I happen to be teaching this stuff right now (d) Nick Rowe needs some support (although no help). Bottom line: government debt can be a burden on future generations (the current generation can use it to take resources from future generations) even if there is no impact on future output, but it is also likely to reduce future output, so we really should worry about the size of government debt in the longer term. But none of these worries applies when the economy is demand constrained, as it is right now

Government Debt and Intergenerational Distribution - After reading Nick Rowe, Brad DeLong, and Paul Krugman, I now understand who bears the burden of the government debt. Any member of the younger generation who reads the stuff that these old guys have written on government debt will be hopelessly confused. And that will be a burden on us all. The idea that a larger government debt is a burden for future generations is so strongly intuitive as to be part of the standard narrative for anyone who wants to tell you that more government debt is a bad idea. But is that correct? When I teach undergraduates about government finance, I find it instructive to start with the Ricardian equivalence theorem. In a frictionless world, government debt is irrelevant. A tax cut that increases the government debt today has no effect because everyone understands that government debt is just deferred taxation. Lifetime wealth does not change, and everyone saves their tax cut today so as to pay the higher future taxes that are required to pay off the government debt in the future. Ricardian equivalence is a useful starting point, as it makes clear what frictions might cause Ricardian equivalence to break down - and that's a route for thinking about how policy might work to improve matters. Distorting taxes, intragenerational distribution effects from tax policy, and credit market frictions all potentially make a difference. But that doesn't make Ricardian equivalence "wrong" or useless. Indeed, it is an important organizing principle, and needs to be taken seriously.

Dean Baker: The National Debt and Our Children: How Dumb Does Washington Think We Are?: While much of the country is focused on the presidential race, the Wall Street gang is waging a different battle; they are preparing an assault on Social Security and Medicare. This attack is not exactly secret. There have been a number of pieces on this corporate-backed campaign in the media over the last few months, but the drive is nonetheless taking place behind closed doors. The corporate honchos are not expecting to convince the public that we should support cuts to Social Security and Medicare. They know this is a hopeless task. Huge majorities of people across the political spectrum strongly support these programs. Instead they hope that they can use their power of persuasion, coupled with the power of campaign contributions and the power of high-paying jobs for defeated members of Congress, to get Congress to approve large cuts in Social Security, Medicare, Medicaid and other key programs. This is the plan for a grand bargain that the corporate chieftains hope can be struck in the lame duck Congress. Most of the media have been happy to cooperate with the corporate chieftains in this plan. There are two main ways in which they have abandoned objectivity to support the plan for cutting Social Security and Medicare.

Semantics and the Debt Burden - Does government debt impose a burden on future generations? A relevant question given the high current government debt levels to which most people will answer with a clear "yes": we are spending today and passing the bill to the next generation. But this answer is incorrect (or to be more precise it might be incorrect). The link between debt and burden on future generations is much more complex than what many think. Recently, a debate has populated the economics blogosphere as some argue that that debt only imposes a burden when it is held externally, others coming up with counterexamples where this is not true (borrowing from Noah Smith a list of links to the debate: here, here, here, here, here or here.) The debate becomes even more complex as the issue of desirability of another round of fiscal stimulus is mixed with the notion of intergeneration transfers associated to increasing government debt. Unfortunately, economists tend to go in circles and debate the same subjects over and over again without reaching consensus, so when I went back a few months (January this year) I found a very similar debate with practically identical arguments being put forward by both sides. The lack of consensus in this particular debate is much more about semantics that about disagreements on how the economy works. My reading of the debate is summarized well by Noah Smith long list of updates to his blog entry. In particular the following question: is government debt an indicator of the (fiscal) burden we are imposing on the next generations? And the answer is a clear no. Debt does not matter. Debt is not a burden per se but it can be the outcome of tax and spending decisions that lead to redistribution of resources.

One More Rumination on the Burden of Fiscal Deficits - You would think that everything that needs to be said about this topic has been put on the table in the past few weeks. And you might be right, but I’ll offer a different take anyway. The debate has been cast in an aggregative framework in which the set of welfare-relevant individuals includes both those who pay taxes tomorrow to repay today’s deficits and those who hold the bonds and receive payments. Fine, but let’s consider a narrower question, one that most economists apparently think is beneath discussion: what it is the purely fiscal burden of public debt? Well it’s obvious, isn’t it? Either you pay off the debt in the future or you roll it over and pay more interest. Either way you bear a fiscal burden, and they are the same in present value terms. Well, try this. In thinking about the fiscal burden, it may help to imagine a country with two types of citizens. One type pays taxes but owns no financial assets; the other owns financial assets but pays no taxes. (We’re getting there....) The government runs a fiscal deficit in period 1. In subsequent periods will there have to be offsetting transfers from the taxpayers to the bondholders?

Myth Drives the Budget Fuss - Nearly everyone believes that Uncle Sam is like a family that must get money before it can spend. But that is not true. A basic function of any sovereign government is to create and run the country’s money system. Unlike a family, the US government is sovereign. It creates money and can never run out. All the words about America’s financial limits mean nothing. Years ago, our money was based on silver and gold. But that did become a limitation when economies around the world needed money to grow faster than metal was dug out of the ground. The US went off the gold standard in 1971, but we still act as if its limitations remain. The economy is often shown as a circular flow of goods and services moving in one direction from producers to consumers, and money to pay for them flowing in the opposite direction. Like a juggling act, the flow keeps running until something interferes. Families that save interfere by removing some of the money. They also remove money when they buy more things from other countries than the US exports. The flow of goods and services slows down when money is removed unless some other party replaces it. The sovereign federal government is the other party. It creates new dollars by spending more into the flow than it removes with taxes. The big bad deficits that haunt so many people are just new dollars that the government crates to replace dollars that savers and importers remove. Moreover, the federal debt that causes so much heartburn is just the sum of all new dollars created since the country began. Truth in labeling would have deficits called something like “new dollars created” or “new savings” and the debt would become “total dollars created” or “total savings”. This is shown every week when savers bid to buy Treasury securities as safe places to put their dollars. The debt is not a liability that will burden future generations, it is an asset that present and future generations of savers will depend on.

Modern Money and Public Purpose 2: Governments Are Not Households - Presentation by Warren Mosler and Stephanie Kelton. Presented at Columbia Law School on September 25, 2012 as part of the Modern Money and Public Purpose series.

Bond Market Vigilantes Are The U.S. Economy's Big Foot - I first used the phrase “deficit cheerleaders” in a column more than two years ago to describe what Wall Street bond traders were really telling Washington, D.C., about the budget. It was August 2010, and contrary to what some in Washington were saying, the supposedly all-knowing and all-seeing traders formerly known as “bond market vigilantes” absolutely were not insisting that the federal government reduce its red ink and we had to stop saying that they were. I also wrote that those who were using the bond market as an excuse for spending cuts and tax increases were misreading or — far more likely — misrepresenting the messages actually being sent by the bond traders. Based on both the low interest rates of the time and the direct statements they were making, it was clear two years ago that the vigilantes had turned into an increase-the-deficit cheering section. They were letting it be known that they not only wouldn’t criticize those who helped produce deficits but would be rooting for those who helped make them happen. In other words, no matter what they might have been saying to the Clinton administration and Congress in the 1990s, the bond market of 2010 actually wanted higher deficits, and the vigilantes had become deficit cheerleaders.

‘Crowding Out’ is Coming to Get You - The principle of 'crowding out' is ubiquitous in economics. It is a standard statement in many basic economics textbooks. A couple of definitions of crowding out are found at Wikipedia: public debt crowds out private investment and increases in government spending crowds out investment spending. The definition from Investopedia is public spending reduces private spending. These arguments are logically based on theories that private spending will be reduced by anticipation of higher future tax rates and higher interest rates resulting from eventual shortages of capital because the government is "hogging the money resource" so to speak. I have engaged in a number of informal discussions about the crowding out concept in which I have questioned it and have been questioned (critically by some) in return. My bottom line from these exchanges is that the topic needs more thorough analysis than many have given it. This is not the start of my attempt to contribute to that analysis (in which I hope to be engaged in the coming weeks), but is simply to throw some cards on the table to explain why the subject so intrigues me.

Six (maybe) good arguments for deficits (and one bad). - Are deficits good or bad? That depends. Sometimes they are good, and sometimes they are bad. But even when deficits are good, don't use bad arguments to defend them. It really annoys me. Here's a list of arguments for deficits:

- 0. "There is no burden on future generations because the extra taxes to service the debt will be paid to those same future generations that inherit (sic) the bonds." That is a really bad argument. It's just plain wrong

- 1. "Yes, future taxes will be a burden on future generations, but monetary policy won't work at the zero lower bound, and we need fiscal deficits to increase demand now, and the benefits exceed the costs." I happen to disagree with the assumption that monetary policy can't work at the ZLB. But I might be wrong.

- 2. "Yes, future taxes will be a burden on future generations, but the roads and schools etc. we are borrowing to build will be an even bigger benefit to those future generations". Good argument.

- 3. "Yes, future taxes would be a burden to future generations, but all we are doing is building the same roads and schools a couple of years earlier than we would have done, and doing it when roads and schools are cheap to build, and real interest rates are very low or even negative, so there's a chance that future taxes might even go down if we run a deficit today and pay it all back by building fewer roads and schools in a couple of years." Another good argument.

- 4. "Yes, future taxes would be a burden to future generations, but the rate of interest on government bonds will on average remain below the growth rate of the economy forever, so we can increase the debt, rollover the debt plus interest forever, without ever having to increase taxes on future generations, who will actually be better off because they will get a higher rate of return on their savings." This argument is valid. But I admit it does scare me, because we don't know for sure what future interest rates and growth rates will be.

- 5. "Yes, future taxes will be a burden on future generations, but future generations will be richer than we are, and it's OK to transfer wealth from richer to poorer". OK. Maybe.

- 6. "Running deficits in bad times and surpluses in good times but balanced budgets on average doesn't mean higher taxes on future generations, and it's better than having government spending procylical and tax rates countercyclical".

Should we be grateful for the Bush deficits? - IN THE recent debate between America's vice-presidential candidates, current Vice President Joe Biden criticised opponent Paul Ryan for "voting to put two wars on a credit card". Matt Yglesias chides Mr Biden for this, noting that borrowing at the time was quite sensible: [D]uring the Bush years, we had low inflation, low interest rates, and plenty of private investment. What would higher taxes have accomplished? There are lots of valid criticisms to be made of Bush-era fiscal policy. Low taxes could have gone to bolstering working class incomes, for example, rather than those at the high end. We could have made potentially useful domestic public investments rather than spending all that money in Iraq...But the idea that we should have relied more on taxes and less on borrowing doesn't hold much water. That's an interesting take. Orthodoxy would suggest that during a typical economic expansion a normal economy shouldn't be running large government deficits (unless the public sector is borrowing to fund positive return public investments that are likely to pay for themselves). Government borrowing competes with private borrowing, crowding out potential private investment (perhaps there was "plenty" but there might otherwise have been more). Sustainable budgeting should aim for balance over the cycle: with surpluses in good times to offset deficits in bad times. Alternatively: if the ratio of net public debt to GDP had been 35% in early 2009 (as it was in 2000) rather than 66%, then America's government might have worried less about the possible fiscal costs of a truly massive fiscal stimulus.

Ryan and Romney’s Secret Plan to Cut the Deficit – and why Romney opposes it - Bill Black - At Thursday’s VP debate, Representative Ryan renewed his claim that he has a secret plan to cut the deficit while cutting all tax rates by 20 percent and not eliminating any tax deductions for which the middle class are large recipients. Oh, and Romney has also promised to increase military spending. Romney is reprising the three contradictory budgetary promises that President Reagan made during the 1980 campaign. Reagan’s OMB Director David Stockman admitted no plan could produce the three promises. Stockman’s job was to lie in order to cover up the fact that the administration had no plan that could simultaneously (1) cut taxes, (2) end the budget deficit, and (3) increase military spending. Stockman invented the “magic asterisk” to hide the truth from the public.There is, of course, no Ryan plan. There cannot be a Ryan plan because mathematicians are not like historians. The cruel joke about historians is that while God himself cannot change history; historians can. It is perhaps because they can be useful to God in this regard that he tolerates their continued existence and frequent errors. Mathematicians are useless to God, at least in the non-exotic realms of mathematics relevant to budgets, because they are so good at exposing errors and when they do so the error is beyond dispute. (Econometricians are God’s favorites among the quants.) No budget plan could meet all (or even most) of the policy constraints Ryan and Romney have promised they would obey. It is mathematically impossible. Romney and Ryan’s primary lie is that they have a secret plan to cut taxes, cut the deficit, and increase military spending.

Moody’s Zandi Warns of Need to Deal With Fiscal Woes - Mark Zandi, the chief economist of Moody’s Corp.’s research arm, believes the U.S.’s fiscal woes will take a turn for the better — but not just yet. “I am meaningfully optimistic about the economy in the second half of the decade,” said Mr. Zandi, of Moody’s Analytics, at the Association for Corporate Growth’s M&A East conference in Philadelphia. “[But] we need to solve a number of fiscal issues pretty quickly after the election.” Mr. Zandi pointed to the fact that the U.S. government needs to tackle the so-called fiscal cliff looming on Jan. 1. Besides that, Congress will be faced with whether to raise the debt ceiling again by the end of February or early March.

A Reminder Of Why A Fiscal-Cliff Compromise Is Not Coming Any Time Soon - CEOs suggest a major reason they are not spending is 'policy uncertainty', politicians blame the other side for stifling growth because of 'policy uncertainty', and brokers, bankers, & economists whine that the only reason the Dow is not at Bernanke's goal-seek'd 36,000 is the 'policy uncertainty'. If only the 'fiscal cliff' issue would go away - we'd all have a pony and life could go on. Sorry to burst that bubble; as we noted here, the market is priced for a total compromise and earnings expectations appear to imply a full fiscal cliff resolution in Q4. The hope remains that 'even if we were to go off the fiscal cliff, the political reaction will be swift and vengeful and we will see a 'V'-shaped recovery - so do not worry'. There are two small (ok, very large) problems with that thesis: 1) the self-reinforcing shadow-banking collateral squeeze that would occur as asset values dump again and liabilities remain; and 2) the record-high polarization among our political class. Something to ponder as earnings outlooks continue to drop...

Chances of Going Over Fiscal Cliff May Be Higher Than Experts Think- What are the odds of the U.S. running off the so-called fiscal cliff — the mix of spending cuts and tax increases that would likely tip the U.S. into recession? On average, economists in the latest Wall Street Journal economic forecasting survey put the probability at just 17%, but some economists and analysts say that may be too low. “Our view remains that the debate in D.C. following the election will be contentious beyond precedent and that this difficulty in finding common ground suggests the odds of going over the cliff are higher than people seem to appreciate,” RBC Capital Markets chief U.S. economist Tom Porcelli said Tuesday in a note to clients. Unless the White House reaches a deal with Congress, the Bush-era tax cuts are scheduled to expire at year-end, raising tax rates on more than 100 million Americans. Another $100 billion in spending cuts on military and other government programs are set to kick in. Other smaller tax policy changes also are looming.

Officials: Obama ready to veto a bill blocking 'fiscal cliff' without tax hike for rich - President Obama is prepared to veto legislation to block year-end tax hikes and spending cuts, collectively known as the “fiscal cliff,” unless Republicans bow to his demand to raise tax rates for the wealthy, administration officials said. Freed from the political and economic constraints that have tied his hands in the past, Obama is ready to play hardball with Republicans, who have so far successfully resisted a deal to tame the debt that includes higher taxes, Obama’s allies say. In the days after the November election, the tables will be turned: Taxes are scheduled to rise dramatically in January for people at all income levels, and Republicans will be unable to stop those automatic increases alone. If he wins reelection, Obama may finally be able to dictate the terms of a bipartisan debt-reduction deal. And if he loses to Republican Mitt Romney, Obama could make sure that tax rates rise before he hands over the keys to the White House on Inauguration Day in late January. Administration officials declined to say whether the veto threat will stand if Obama loses the election.

Obama's plan: Push Republicans off the fiscal cliff -- I’ve criticized the Obama campaign for failing to detail much of a vision for a second term. But that’s not to say they don’t have one. They do. It’s just a hard one to campaign on. After promising in 2008 to bring about a new era of cooperation in Washington, they’re campaigning in 2012 knowing that, if reelected, they will start their second term with a brutal, economy-shaking showdown with Republicans over spending and taxes. If the Obama administration were to really lay out their plans, they would go something like this. In November, President Obama will reiterate, clearly and firmly, that he will veto any attempts to extend the high-income tax cuts or lift the big, dumb spending cuts without finding equivalent savings elsewhere. In fact, as my colleague Lori Montgomery reports, they’re already reiterating that promise. That veto threat is the center of the Obama administration’s second-term strategizing. The Obama administration believes – and, just as importantly, they believe Republicans believe — that they’ve got the leverage here. The Republican position on taxes is less popular than the Democratic position. The outcome of gridlock is much higher taxes, which is more anathema to Republicans and arguably cheering to Democrats. The big, dumb spending cuts, despite being poorly timed and inanely constructed, are very progressive in their effect, falling heavily on military spending while exempting Medicaid, Social Security, and Medicare beneficiaries.

Brookings Institute On Looming Fiscal Cliff: Little Room for Optimism - Brookings Institute Senior Fellow Ron Haskins discusses the Looming Fiscal Cliff in the following video. About 30 seconds in, Haskins' stated "the fiscal cliff is kind of the opposite of Keynesian economics". I was thinking here we go again, another person thinks we cannot do anything about this "now". Having played it entirely, it is clear Haskins is not supportive of the Keynesian view, rather, he is disgusted as to why we are where we are, blaming Congress, the president, an partisan politics. He failed to address the role of the Fed or fractional reserve lending, but he is against can-kicking exercises.

Fiscal Cliff Could Play Scrooge This Holiday Season - If workers start paying attention, the fiscal cliff could play Scrooge this holiday season. Economists have been warning for a while about the overall drag coming from the fiscal cliff–the coming combination of government spending cuts and tax increases. Company executives already are reacting to the situation. Business surveys suggest policy uncertainty is holding back hiring and capital spending in the second half of 2012. Consumers, however, aren’t bothered by the potential impact on their wallets. Polls show a jump in economic optimism even as the U.S. approaches the cliff.