Fed's Balance Sheet Edges Up in Latest Week - The Fed's asset holdings in the week ended Nov. 7 edged up to $2.832 trillion, from $2.825 trillion a week earlier, it said in a weekly report released Thursday. The Fed's holdings of U.S. Treasury securities increased to $1.651 trillion on Wednesday from $1.645 trillion. The central bank's holdings of mortgage-backed securities rose slightly to $852.06 billion from $852.04 billion a week ago. In September the Fed began buying $40 billion a month of additional mortgage-backed securities on an open-ended basis. Fed officials have said that they plan to continue buying bonds until the labor market improves significantly. Thursday's report showed total borrowing from the Fed's discount lending window was $1.17 billion Wednesday, down from $1.26 billion a week earlier. Borrowing by commercial banks fell to $6 million from $37 million a week earlier. U.S. government securities held in custody on behalf of foreign official accounts declined to $3.611 trillion, down from $3.617 trillion in the previous week. U.S. Treasurys held in custody on behalf of foreign official accounts decreased to $2.915 trillion, down from $2.921 trillion in the previous week. Holdings of agency securities edged down to $696.04 billion from the prior week's $696.25 billion.

FRB: H.4.1 Release--Factors Affecting Reserve Balances ...November 8, 2012

Fed's Williams: QE3 to likely top $600 billion - The U.S. Federal Reserve's latest round of asset purchases will probably top $600 billion, surpassing its second round of bond-buying, as the central bank continues to buy assets until the labor market improves, a top Fed official said on Monday. The effect of the Fed's asset purchases on the economy will depend on how much market participants think the central bank will ultimately buy, something the Fed itself does not know, John Williams, president of the San Francisco Federal Reserve Bank, told reporters after a lecture at the University of California, Irvine. But given the state of the labor market and the pace at which it is improving, the Fed will likely need to keep buying assets "well into next year," he said. The Fed will want to see sustained jobs gains and a consistent drop in the unemployment rate before it stops buying assets, he said.

Fed’s Bullard Sees Twist End, More QE3 on the Table - The Federal Reserve may be forced to end a program known as Operation Twist at year-end because of its depleted supply of short-term securities, and it isn’t clear what will happen to replace that leg of central-bank stimulus, a top U.S. monetary policy maker said.“My sense is that it is unlikely we’d extend Operation Twist because there is only so much balance sheet we can use” for the program, Federal Reserve Bank of St. Louis President James Bullard told reporters after a hometown speech. He was referring to a central-bank program that sells short-dated Fed-owned Treasury debt to buy a like amount of long-dated securities.Operation Twist was designed to increase the stimulative power of the Fed balance sheet without expanding its size, by changing the average maturity of central bank holdings. The program is set to end at the conclusion of the year.

Economists Expect Fed to Shift From Twist to Treasurys Purchases - When the Federal Reserve program known as “Operation Twist” ends in December, the central bank is most likely to shift to buying Treasury securities outright, according to a majority of economists surveyed by the Wall Street Journal. Since September 2011, the Fed has been selling about $45 billion in short-term Treasurys each month and using the proceeds to purchase about the same amount in long-term Treasurys. The program, which the Fed extended in June until the end of 2012, is intended to help lower long-term interest rates to spur spending, investment and hiring.

Reading Labor Markets - Atlanta Fed's macroblog - When the September employment report was released on October 5, the top-line payroll employment gain for the month, as reported in the U.S. Bureau of Labor Statistics' (BLS) establishment survey, logged in at 114,000. Under standard assumptions, a number of this magnitude would be barely enough to absorb the growth of the labor force and keep the unemployment rate constant. In contrast, in that same October 5 report we learned from the BLS household survey that the measured unemployment rate fell from 8.1 percent in August to 7.8 percent in September. According to Friday's BLS report on the employment situation for October, the top-line payroll employment gain for the month from the establishment survey was 171,000. At that pace—which is also the current average gain for the past three months—the Atlanta Fed jobs calculator suggests the unemployment rate should fall another one-half of a percentage point over the next year. At the same time, according to the BLS household survey, the unemployment rate rose from 7.8 percent in September to 7.9 percent in October. This is as good an illustration as any to explain why, on November 1, Atlanta Fed President Dennis Lockhart said the following in a speech "If the outlook for the labor market does not improve substantially, the Committee will continue its purchases of agency mortgage-backed securities, undertake additional asset purchases, and employ its other policy tools as appropriate until such improvement is achieved in a context of price stability."... For policy purposes, I think it's appropriate to be cautious about relying on a single indicator of labor market trends—for example, the unemployment rate—to determine whether the condition of "substantial improvement" has been met.

Bill Gross: QE1-3 Added No Savings or Investment - In case you missed it, bond investing legend Bill Gross has just provided the most damning evidence that various Fed easing efforts have been worse than useless. You'd think all of this helicopter dropping of cash would encourage more investment which in turn would generate more jobs, but capital expenditures Stateside are actually dropping like a rock even if real interest rates are well and truly negative: It is of course expected that Americans just keep spending their brains out since they can't help it. But, to put money aside for productive expenditures? You must be joking. We're talking about modern America here, an instant gratification society that hasn't had much to be grateful for as of late. And, where there's no investment there's no savings. Much has been made of laughably puny increases in consumer savings since the events of 2007, but if you add together government, business and consumer savings, the truth is that US net national savings are scraping all-time lows in negative territory where it's been the last three years:

Quelle Surprise! QE Zombifies Economies - Yves Smith - Nobody has wanted to heed the lesson of post bubble Japan until way too late. Early in the crisis, the Japanese took the uncharacteristic step of telling American policy makers loudly that Japan had made a big mistake in how they handled theirs. They stressed that the most important step was cleaning up the banks. Then the IMF had the bad fortune to release a study of 124 banking crises on the heel of the Lehman and AIG meltdowns, which meant its findings were ignored, since the finance officialdom was too busy trying to deal with the wreckage to process new information. But it too came squarely down on the side of making banks take their medicine: Existing empirical research has shown that providing assistance to banks and their borrowers can be counterproductive, resulting in increased losses to banks, which often abuse forbearance to take unproductive risks at government expense. The typical result of forbearance is a deeper hole in the net worth of banks, crippling tax burdens to finance bank bailouts, and even more severe credit supply contraction and economic decline than would have occurred in the absence of forbearance. Cross-country analysis to date also shows that accommodative policy measures (such as substantial liquidity support, explicit government guarantee on financial institutions’ liabilities and forbearance from prudential regulations) tend to be fiscally costly and that these particular policies do not necessarily accelerate the speed of economic recovery. Of course, the caveat to these findings is that a counterfactual to the crisis resolution cannot be observed and therefore it is difficult to speculate how a crisis would unfold in absence of such policies.

Obama Re-Election Makes Market More Confident of Fed Policy - President Barack Obama‘s re-election has made markets more confident that the Federal Reserve will continue on its current path. With Obama winning a second term, the odds are higher that any leadership change at the central bank will follow in Chairman Ben Bernanke‘s footsteps. The path of Fed policy now seems clearer to the market, as evidenced in the fed-funds futures market. November 2014 fed-funds futures now price in no chance of an interest-rate increase by then, compared with a 24% chance priced in at Tuesday settlement. The central bank has said it plans to keep rates near zero at least until mid-2015. But Bernanke’s current term ends in 2014, and some had speculated that a Romney administration would have appointed a Fed chairman who would push for higher rates sooner. Further evidence that markets expect low rates for a longer period came from the eurodollar futures market. Long-dated eurodollar futures are up today. The December 2014 contract recently priced in a rate 0.17 percentage point above the rate priced into the December 2013 contract. That is down from 0.21 percentage point Tuesday, suggesting there are expectations for short-term rates to increase at a slower pace.

Federal Reserve Liquidity Facilities Gross $22 Billion for U.S. Taxpayers - NY Fed - During the 2007-09 crisis, the Federal Reserve took many measures to mitigate disruptions in financial markets, including the introduction or expansion of liquidity facilities. Many studies have found that the Fed’s lending via the facilities helped stabilize financial markets. In addition, because the Fed’s loans were well collateralized and generally priced at a premium to the cost of funds, they had another, less widely noted benefit: they made money for U.S. taxpayers. In this post, I bring information together from various sources and time periods to show that the facilities generated $21.7 billion in interest and fee income.

'Managing a Liquidity Trap: Monetary and Fiscal Policy' - I like Stephen Williamson a lot better when he puts on his academic cap. I learned something from this: Managing a Liquidity Trap: Monetary and Fiscal Policy. I disagree with him about the value of forward guidance, though I wouldn't bet the recovery on this one mechanism, but it's a nice discussion of the underlying issues. I was surprised to see this reference to fiscal policy: I've come to think of the standard New Keynesian framework as a model of fiscal policy. The basic sticky price (or sticky wage) inefficiency comes from relative price distortions. Particularly given the zero lower bound on the nominal interest rate, monetary policy is the wrong vehicle for addressing the problem. Indeed, in Werning's model we can always get an efficient allocation with appropriately-set consumption taxes (see Correia et al., for example). I don't think the New Keynesians have captured what monetary policy is about. For some reason, I thought he was adamantly opposed to fiscal policy interventions. But I think I'm missing something here -- perhaps he is discussing what this particular model says, or what NK models say more generally, rather than what he believes and endorses. After all, he's not a fan of the NK framework. In any case, in addition to whatever help monetary policy can provide, as just noted in the previous post I agree that fiscal policy has an important role to play in helping the economy recover.

Nudging Inflation Expectations: An Experiment - NY Fed - Managing consumers’ inflation expectations is of critical importance to central banks in the conduct of monetary policy. But managing inflation expectations requires more than just monitoring expectations; it also requires an understanding of how these expectations are formed. In this post, we present results from a new study that investigates how individual consumers use selected information on food prices in forming their inflation expectations. While the provision of this information leads individuals to meaningfully revise expectations of their own-basket inflation rate, we find there is little impact on expectations of overall inflation.

Fed’s Williams Doesn’t See Inflation Threat - In a speech defending the Federal Reserve‘s efforts to stimulate the economy in recent years, a central-bank official said inflation isn’t a threat, and described how monetary policy easing can lower the dollar. “Inflation has been very low during this period of unconventional policies, and it remains so,” Federal Reserve Bank of San Francisco President John Williams said Monday. He added, “the public’s inflation expectations remain well anchored,” and said “we are not seeing signs of rising inflation on the horizon.” Mr. Williams is a voting member of the monetary-policy-setting Federal Open Market Committee. His comments came from the text of a speech prepared for delivery before a gathering at the University of California, Irvine. The bulk of his formal remarks were devoted to describing and quantifying the effect of a host of unconventional policies the Fed has pursued since it cut short-term interest rates essentially to 0% at the end of 2008.

Three reasons for extremely low swap spreads - US swap spreads continue to decline, as the 5y spread hovers below 10bp. A rate swaps is basically a stream of floating (3m LIBOR) vs. fixed payments. The level at which fixed payments are set (the swap rate) is therefore the market's projection of future LIBOR. This decline in spread is the market's expectation that future LIBOR to treasury spreads will be lower. Three factors are contributing to this decline:

1. With the ECB backstop to the Eurozone sovereigns in place, the perceived risks to global banks have subsided. Improved health of the global financial system means lower cost of funding for banks, which should (loosely) translate into lower LIBOR to treasury (TED) spread in the future - thus lower swap spread.

2. As LIBOR converges to CD rates (see discussion), which have generally been lower, the market is pricing in lower overall LIBOR levels in the future (reducing swap spreads).

3. The Fed has been taking duration out of the market, first via Twist (see discussion on how Twist reduced duration) and now also with MBS purchases (see discussion). With mortgage refinancing accelerating, MBS durations decline. When fixed income investors hedge against rate risk, they usually want to pay fixed and receive floating on a rate swap. But as the need to hedge fixed income portfolios declines (because portfolios have lower durations) so does the demand to pay fixed - which reduces swap rates and spreads.

Treasury Yields Update: Heading Lower? - I've updated the charts below through Thursday's close. The 10-year note closed today at 1.62, which is 26 basis points off its interim high of 1.88, also set the day after QE3 was announced. The historic closing low was 1.43 on July 25th. Many market analysts have speculated that the rise in yields from the July low was the opening move in an epic reversal of the multi-decade trend toward lower yields from stagflation era, when the 10-year peaked above 15 percent (more here).Perhaps it's too soon to make that call. If the post-election selloff in equities continues, the 10-year yield could certainly revisit the levels of late July. Japan is an example (admittedly an extreme one) of a developed nation with its own currency that has experienced a relentless demand for government bonds, as this chart illustrates. Currently Japan's 10-year yield is around 0.75, less than half that if its US counterpart.As for mortgage rates, the latest Freddie Mac weekly update, out today, shows the 30-year fixed at 3.40%, four basis points above its historic low set the first week in October. Here is a snapshot of selected yields and the 30-year fixed mortgage one week after the Fed announced its latest round of Quantitative Easing.

Q4:2012 U.S. GDP Nowcast Update | 11.5.2012 - Will the rebuilding in the Northeast in the wake of Hurricane Sandy’s destruction juice the economy’s modest growth trend? It’s too early to know, but the possibility can’t be dismissed. For now, it’s time to establish a baseline of nowcasts for Q4:2012 GDP. The official estimate is scheduled for release via the Bureau of Economic Analysis in late-February, and so there's a long road ahead in terms of economic updates. The journey starts here: The current average of our five econometric-based nowcasts anticipates real annualized Q4 growth of 1.7%, or down slightly from Q3's official 2.0% estimate. It's still early, of course, and so there's limited data for developing a robust estimate for Q4. But as the numbers roll in, we'll update the nowcasts and monitor the changes. The key issue to watch is how the nowcasts evolve—are they rising, falling, or holding steady? The trend changes will tell us quite a lot about what to expect for the government's initial estimate of Q4 GDP that's due to hit the streets next February. For now, here's where we stand in terms of The Capital Spectator's econometric nowcasts, along with two estimates from other sources for perspective:

Gauging Hurricane Sandy's impact on the US economy - Estimates of economic damage from Hurricane Sandy are now ranging between $30 - $50bn. This is clearly a large number. LA Times: - Estimates of the economic losses caused by Hurricane Sandy earlier this week reached $50 billion as experts assessed the costs of severe property damage, shut-down subways and power outages. On Thursday, Eqecat Inc. said it expects storm-related losses to fall between $30 billion and $50 billion. Of that, $10 billion to $20 billion will be insured, according to the firm, which calculates estimates for insurers. Earlier this week, Eqecat had said that damages could reach $20 billion, with up to $10 billion in insured losses. But as terrible as this event was, in terms of economic damage it is still expected to be considerably below that of Katrina, which adjusted for inflation came in at $145 bn. The question now is: what will be Sandy's impact on the US economy? Based on historical experiences, the answer is not entirely obvious. JPMorgan's recent report attempts to answer it. Their view is that "Hurricane Sandy may initially depress economic activity, then support it over time as rebuilding commences". In the near-term the hurricane-impacted high frequency data and seasonal adjustments may be off for a couple of months. Longer term however, the impact on the overall economy should be minimal. The chart below shows the monthly GDP after three major hurricane events. Although we may see some weakness within the first month or two, the economy seems to be stable six months out.

The Perfect Economic Storm - The destruction from Hurricane Sandy will negatively impact fourth quarter economic growth. Most of us have heard by now that not addressing the fiscal cliff will throw the United States back into recession. The CBO has warned and warned again. Similar to the trifecta of three separate weather events combining to create Frankenstorm, we have economic and political events colliding to do the same. Economic forecasters are tallying up the damage from Hurricane Sandy and currently estimates are coming in at $50 billion. We expect Hurricane Sandy economic impact figures to rise. By comparison, Hurricane Katrina's economic devastation was eventually estimated to be $250 billion, with property damage alone estimated at $108 billion. Katrina hit on August 29, 2005. Q3 is July through September. Below is GDP for the time around the coming of Katrina. National real GDP went from 3.2% to 2.1% from Q3 to Q4 2005. GDP does vary normally between quarters and there are many other factors which contribute to economic growth. Yet, the gulf states contribution to national GDP are minimal. Louisiana and Mississippi together are only 2.2% of national GDP. The eastern seaboard's economic contributions, on the other hand, are substantial. New York alone was 7.7% of national GDP in 2010 and New Jersey, 3.4%. Below is a graph of the state of Louisiana's GDP, annually. We see a dramatic growth rate drop after Katrina hit.

Data Notes Part 2: A Bit of Sandy Economics and Net Vs. Gross -The damage from Sandy, both to peoples’ lives and the economy, keeps mounting as each day reveals how long it’s taking to get back to normal. By definition, this increases the economic costs of the crisis, which can be thought of as having two basic parts: costs that are sunk forever and costs that will be made up. More on that in a moment, but first, here’s a chart of hurricane costs as a share of GDP covering the past few decades. The preliminary estimate of Sandy, by GS Research, is $30 billion, or about 0.2% of GDP, placing it in the top five. I think that’s low and so I added a bar of $50 billion, or 0.3% of GDP. In the case of a storm, they’re vacations that won’t be taken, nights out for dinner and a movie lost forever, conferences that were cancelled and won’t be rescheduled. Of course, other economic activities are simply postponed, and insurance typically covers about half the damage from these types of storms. So some of what you see in the economic indicators after these large storms are results that dip below recent trends for a few months and then go above recent trends, balancing out on average. And then, of course, there’s the rebuilding, and that’s where net versus gross comes in. Rebuilding stuff that was damaged or destroyed adds to GDP, because of the “G”—it’s gross domestic product, and so it doesn’t net out either standard depreciation—capital consumption, meaning the wear and tear on machinery and other goods that make up our capital stock—or the destruction from hurricanes. For that, you have to turn to net national product, which in some ways is a more revealing measure of the nation’s wealth than GDP, because it represents what’s actually available for consumption and investment.

Hurricane Sandy: Impact on "Near-Term Economic Activity" - The economic data has already shown some impact from Hurricane Sandy, and we will see more over the next couple of months. As an example, auto sales were down in the Northeast at the end of October, home listings were down in New York and New Jersey in early November, and this morning the MBA reported mortgage applications were down sharply in those states. Goldman Sachs analysts Sven Jari Stehn and Shuyan Wu tried to quantify the short term impact: The Effect of Hurricane Sandy on Near-Term Economic Activity

1. Employment dips and rebounds ... Both nonfarm payrolls and household employment typically fall one month after landfall and then rebound in the following two months. Our estimates suggest that the hit of Hurricane Sandy on November employment might be around 20,000 with a rebound in December and January. ...

2. ...as claims rise and fall slowly. Initial jobless claims typically rise over the first three weeks after landfall before gradually falling back over the subsequent two months. Our analysis suggests that Hurricane Sandy might push initial jobless claims up by around 14,000 in the week ended November 17 and that it might take until late December for the distortion to disappear entirely from the claims report.

3. Small effects on housing and manufacturing. ... we find that housing starts tend to rise only by a few thousand units in the aftermath of storms as rebuilding of damaged houses begins. Regional manufacturing surveys typically weaken following hurricanes, but the effect is small. Our results would suggest that manufacturing surveys in the affected states—the Empire and Philadelphia Fed indexes—might weaken temporarily by a point or two in December due to Hurricane Sandy, but this is likely to be hard to distinguish from statistical noise.

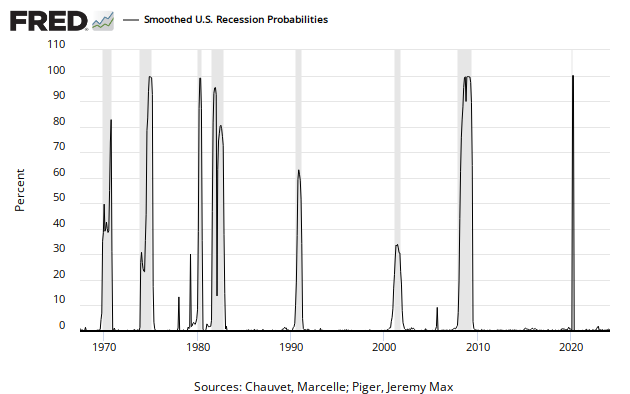

USA Recession Odds: 100%? - Here’s an interesting new data point that the St Louis Fed has put together to calculate recession probabilities:“Recession probabilities for the United States are obtained from a dynamic-factor markov-switching model applied to four monthly coincident variables: non-farm payroll employment, the index of industrial production, real personal income excluding transfer payments, and real manufacturing and trade sales. “What’s interesting about this index is the current reading. At 20%, the index is at a level that has ALWAYS been followed by a recession. As you can see below, the index has never approached 20% without a subsequent recession. All 6 recessions since 1967 have coincided with 20%+ readings in the US Recession Probabilities index. Interestingly, I still don’t see recession in my internal indicators. Those indicators have been right for a long time now (in the face of some very public recession predictions by reputable people). So I am afraid when my internal indicators point to “no recession” when an indicator like this clearly puts that opinion in the “this time is different” category….

Debunking the 100% Recession Chart - This chart is making the rounds, confirmation bias for those who are convinced that below-trend growth equals a recession. There are several leading sources pointing to the chart and suggesting that it implies a 100% chance of a recession. There are so many things wrong with this that I hardly no where to begin. Here is the commentary from non-economist talk-show guy Lance Roberts:"As stated above, each time this indicator has signaled the probability of a recession at 20%, or higher, the economy has either been in, or was about to be in, a recession. However, while the indicator is currently at a level that is indicative of a recession, along with a host of other economic indicators confirming the same (LEI Coincident to Lagging Ratio, ADS, GDI, Final Sales, STA Economic Composite, etc.), the NBER will wait to date the recession until the data revisions are in. Historically, as shown in the table below, the amount of time between the recession probability indicator hitting 20% and the NBER confirming the start of the recession has been on average about eight months. However, since the turn of the century that lag has moved to roughly 11.5 months." Try this. Look at the chart above and pretend that we were going back to the future in 2005. You could have drawn the line at 15% and said everything that Lance says now. You would have been completely wrong!

The Recession Probability Chart - One of the most frequent questions I receive via email is: "Is another recession starting?" There are quite a few people who have been calling a recession recently (ECRI has called several recessions since August 2011 or so). They still have time on their most recent calls, but their earlier calls were wrong. Part of the problem in forecasting right now is the sluggish recovery has ups and downs, and each down looks like the start of a recession to some models. There is a recession probability chart from the St Louis Fed making the rounds today. The chart shows that the odds of a recession have increased recently. Here is the chart from FRED at the St Louis Fed: "This recession probabilities series from University of Oregon economist Jeremy Piger is a monthly measure of the probability of recession in the United States obtained from a dynamic-factor Markov-switching model applied to 4 monthly coincident variables: non-farm payroll employment, the index of industrial production, real personal income excluding transfer payments, and real manufacturing and trade sales." However there are reasons this shouldn't be interpreted as indicating a new recession. Jeff Miller at a Dash of Insight does the heavy lifting: Debunking the 100% Recession Chart. Jeff actually read the underlying papers - and contacted the authors. Please read his post for more.

Beware Of Zombie Recession Forecasts - With the election behind us and the fiscal cliff approaching, recession forecasting is in full swing again, and so it's time once more to roll out the standard caveat—not all predictions are created equal. In fact, quite a lot of the opinions are of poor quality, largely because one or more of the following applies: 1) the predictions are driven by emotion; 2) the analysis relies on cherry-picking the data; 3) the analyst is generally misreading and abusing the economic signals and models; 4) the analysis is overly focused on recent data that's probably infected with short-term/seasonal distortion; 5) the analyst has another agenda to promote that conflicts with objective macro analysis. For example, some pundits claim that there's a clean, direct link between the business cycle and policy debates in Washington related to decisions that may or may not happen in the future. For example, Steve Forbes predicted yesterday that "we will have a recession." Yes, that's a reliable forecast--now and forever. There's always another recession lurking. Timing, however, is a complicating factor. That's a reminder that we must consider the source--the model--for any recession prediction. On that score, Forbes' analysis looks wobbly: "Raising taxes on capital, raising taxes on small businesses, which we will likely get now, particularly since the Republicans did so badly in the Senate races, that is going to pose a real burden." Sounds plausible, in a warm and fuzzy way. But if you spend any time analyzing the business cycle, you'll quickly discover that the link between macro fluctuations and tax rates in the short-to-medium term is clear as mud. As a tool for deciding if recession risk is high or low, rising or falling, this approach is worse than useless. If it were otherwise, your first source for predicting recessions would be listening to debates in Congress and press conferences at the White House. Good luck with that.

Fitch Sees Risk of U.S. Recession on Fiscal Cliff Concern - The U.S. risks entering a recession that will hurt economic growth worldwide should policy makers fail to avoid the so-called fiscal cliff of automatic tax increases and spending cuts next year, Fitch Ratings said. “We think that will tip the U.S. back into recession,” Fitch Managing Director Ed Parker said in an interview in Istanbul yesterday. “This should be a wholly avoidable, unnecessary recession.” U.S. stocks have tumbled, sending the Standard & Poor’s 500 Index to its biggest two-day drop in a year, after U.S. President Barack Obama’s re-election, as concern deepened that lawmakers will be unable to reach a budget compromise to avoid more than $600 billion in spending cuts and tax increases. The Congressional Budget Office reiterated that a failure to strike a deal would lead to a recession in the first half of 2013. Fitch, which rates the U.S. AAA, its highest investment grade status, on Nov. 7 warned that the U.S. may be downgraded next year unless lawmakers avoid automatic tax boosts and budget cuts and raise the debt ceiling, while Moody’s Investors Service said it will wait to see the economic impact should the nation experience a fiscal shock. S&P stripped the U.S. of its AAA credit rating on Aug. 5, 2011, after months of political wrangling over the debt ceiling.

Trade Makes Third Quarter Look Better - A better than expected trade report is causing economists to bolster their view of third quarter economic growth. The U.S. trade deficit in September unexpectedly contracted 5.1% to $41.55 billion — the lowest level since the end of 2010, the Commerce Department said Thursday. The August deficit was revised down to $43.79 billion from $44.22 billion. The data suggests that the deficit acted as less of a drag on the economy than initially reported last month. The trade gap subtracted about 0.2 percentage point from the government’s first reading of 2.0% third quarter growth.

Third Quarter GDP Looking Better, but May Be at Expense of Fourth Quarter - Initially viewed as another lackluster period, the third quarter could turn out to be among the most robust economic advances of the current recovery. After surprisingly positive reports on wholesalers’ inventories and the trade deficit this week, some economists are now forecasting that the gross domestic product increased at better than a 3.0% rate during the third quarter. The government initially pegged it as a 2.0% gain, but will use the latest data to revise the figure later this month. Economic growth has only twice topped a 3.0% rate since the recovery began thirteen quarters ago. The economy hasn’t grown at better than a 3.0% clip for a full year since 2005. J.P. Morgan Chase raised its estimate of third quarter growth to 3.2% from 2.8% Friday after a Commerce Department report showed that wholesale inventories increased 1.1% in September — far exceeding expectations — and August inventory growth was revised up. “We are raising our tracking estimate…because wholesale inventories were stronger than what had been assumed” by the government in its advance report, said economist Daniel Silver. Initially, the government saw the change in inventories was a 0.1 percentage point drag on overall growth, but data released since indicates that the change should now contribute 0.6 of a percentage point to the GDP gain, he said.

Treasury Yields/Mortgage Rate Update - I've updated the charts below through Friday's close. The S&P 500 is 3.52% off its interim high set on September 14th, the day after QE3 was announced. The 10-year note closed the week at 1.75, which is 13 basis points off its interim high of 1.88, also set the day after QE3 was announced. The historic closing low was 1.43 on July 25th. The latest Freddie Mac weekly update shows the 30-year fixed at 3.39%, three basis points above its historic low set the first week in October. Here is a snapshot of selected yields and the 30-year fixed mortgage one week after the Fed announced its latest round of Quantitative Easing. The first chart shows the daily performance of several Treasuries and the Fed Funds Rate (FFR) since 2007. The source for the yields is the Daily Treasury Yield Curve Rates from the US Department of the Treasury and the New York Fed's website for the FFR. Now let's see the 10-year against the S&P 500 with some notes on Fed intervention. For a long-term view of weekly Treasury yields, also focusing on the 10-year, see my Treasury Yields in Perspective.

TAGP expiration will put downward pressure on short-term yields - In 2008 many businesses in the US became concerned that the various transaction accounts they use to conduct business could be at risk due to banks failing. In order to reassure frightened corporate America, the FDIC implemented the Transaction Account Guarantee Program (TAGP), which provided unlimited government guarantees for non-interest-bearing transaction accounts such as deposits earmarked for payroll. This was all part of the Temporary Liquidity Guarantee Program (TLGP) meant to restore confidence in the shaky financial system. At the end of 2012 however, this unlimited FDIC guarantee program is set to expire, affecting some $1.4 trillion of deposits. According to a recent survey (see attached paper from Western Asset Management), two out of five depositors in these accounts will reallocate cash elsewhere once the accounts are no longer guaranteed. The money will go into either interest bearing accounts, short term securities such as CP or short-term treasuries, or money market funds (and money market funds will be forced to buy short term securities). Given an already significant shortage of money market products out there - a problem that has been worsening since the financial crisis (see this post from 2009) - this will put downward pressure on rates (including short-term IG corporate paper). Even in a normal year demand for short-term securities increases at year-end (see discussion), but with TAGP expiration we may see more negative yields in short-term treasuries and incredibly tight CP spreads.

An MMT Fiscal Responsibility Narrative: Some Truths - Many MMT posts and other writings on fiscal responsibility, including my own, focus on the myths of neoliberalism, pointing out why they are myths and developing an alternative MMT perspective in some detail. Off hand, and I may have forgotten something, I couldn’t think of a brief positive MMT narrative containing primarily the truths, rather than the myths. So, here’s my version.

- – The US Government can’t involuntarily run out of fiat money because it has the constitutional authority to create it without limit. Congress constrains and regulates this ability; but its existence is still a stubborn fact!

- – In addition to taxing and borrowing money and, most importantly, the Government has an unlimited capacity to create it. When it taxes and borrows, it removes it from the private sector. When it creates it, over and above what it taxes or borrows, it adds it to the private sector.

- –The Treasury can keep borrowing money if we want it to. There’s no limit on the Government credit card except the one imposed arbitrarily by Congress.

- – Bond markets don’t control US interest rates; the Federal Reserve Bank does by exercising its authority to meet its target interest rates. Bond vigilantes have no power against the Fed. If they fight against its interest rate targets; then they “die.”

- – The bond markets will most probably buy US debt for the foreseeable future; but if they don’t, then the US won’t be forced into insolvency; because the Government can always create the money needed to meet US obligations.

- – We’re obligated to pay all US debts as they come due. Nevertheless, our national debt cannot be a burden for our grandchildren; since we have an unlimited credit card to incur new debt at interest rates of our choosing, or, alternatively can create all the money we need to pay off debt subject to the limit, without incurring any more debt; unless they wish to make it so by stupidly taxing more than they spend.

- – Since the US Government has no limits on its authority to create/spend money other than self-imposed ones, neither the level of the national debt, nor the debt-to-GDP ratio can affect the Government’s capacity to spend Congressional Appropriations at all.

- – The Federal Government is not like a household! Households can’t make their own currency and require that people use that currency to pay taxes! So, their supply of dollars is always limited; while the Government’s supply is a matter of its decisions alone.

Explain the disease to help US citizens - Today, the US private sector is saving a staggering 8 per cent of gross domestic product – at zero interest rates, when households and businesses would ordinarily be borrowing and spending money. But the US is not alone: in Ireland and Japan, the private sector is saving 9 per cent of GDP; in Spain it is saving 7 per cent of GDP; and in the UK, 5 per cent. Interest rates are at record lows in all these countries. This is the result of the bursting of debt-financed housing bubbles, which left the private sector with huge debt overhangs – notably the underwater mortgages – giving it no choice but to pay down debt or increase savings, even at zero interest rates. However, if someone is saving money or paying down debt, someone else must be borrowing and spending that money to keep the economy going. In a normal world, it is the role of interest rates to ensure all saved funds are borrowed and spent, with interest rates rising when there are too many borrowers and falling when there are too few. But when the private sector as a whole is saving money or paying down debt at zero interest rates, the banks cannot lend the repaid debt or newly deposited savings because interest rates cannot go any lower. This means that, if left unattended, the economy will continuously lose aggregate demand equivalent to the unborrowed savings. In other words, even though repairing balance sheets is the right and responsible thing to do, if everyone tries to do it at the same time a deflationary spiral will result. It was such a deflationary spiral that cost the US 46 per cent of its GDP from 1929 to 1933. Those with a debt overhang will not increase their borrowing at any interest rate; nor will there be many lenders, when the lenders themselves have financial problems. This shift from maximising profit to minimising debt explains why near-zero interest rates in the US and EU since 2008 and in Japan since 1995 have failed to produce the expected recoveries in these economies. With monetary policy largely ineffective and the private sector forced to repair its balance sheet, the only way to avoid a deflationary spiral is for the government to borrow and spend the unborrowed savings in the private sector.

The coming debt battle - James Galbraith - In the tense run-up to Hurricane Sandy, I clicked on one of those headlines that appears on the right side of the screen: “Civilization May Not Survive This, Economist Says.”Once there, I knew I’d been had. It was about … the public debt. It cited one Lawrence Kotlikoff of Boston University, one of America’s most talented artificers, who “estimates the true fiscal gap is $211 trillion when unfunded entitlements like Social Security and Medicare are included.” Compared to that, what’s a thousand mile-wide hurricane? That the looming debt and deficit crisis is fake is something that, by now, even the most dim member of Congress must know. The combination of hysterical rhetoric, small armies of lobbyists and pundits, and the proliferation of billionaire-backed front groups with names like the “Committee for a Responsible Federal Budget” is not a novelty in Washington. It happens whenever Big Money wants something badly enough. Big Money has been gunning for Social Security, Medicare and Medicaid for decades – since the beginning of Social Security in 1935. The motives are partly financial: As one scholar once put it to me, the payroll tax is the “Mississippi of cash flows.” Anything that diverts part of it into private funds and insurance premiums is a meal ticket for the elite of the predator state. And the campaign is also partly political. The fact is, Social Security, Medicare and Medicaid are the main way ordinary Americans connect to their federal government, except in wars and disasters. They have made a vast change in family life, unburdening the young of their parents and ensuring that every working person contributes whether they have parents, dependents, survivors or disabled of their own to look after. These programs do this work seamlessly, for next to nothing; their managers earn civil service salaries and the checks arrive on time. For the private competition, this is intolerable; the model is a threat to free markets and must be destroyed.

US austerity? US 'fiscal cliff' would trigger cuts of up to 5.1% GDP - As US public debt is about to rise over the limit of $16.39 trillion, analysts warn of the drastic damage it could create. Should the debt limit remain unchanged, the US economy will have to suffer austerity measures worth around $804.5 billion. The debt held by the public skyrocketed to about 102% of the US GDP in 3Q 2012. The ratio was higher only once in the US economic history – in 1945 when it reached 113% of GDP.Meanwhile, a new so-called “debt ceiling”, that was last raised by Congress in January 2012 to $16.394trln, seems to be not high enough, as the figures show that the room for further borrowing is becoming increasingly narrower. Earlier this week the US Treasury said the country was set to hit the debt limit by the end of the year. Meanwhile the Treasury has continued to unveil borrowing plans that include massive bond issues, which will inevitably drive the US economy deeper into debt. If the US Congress does not raise the debt ceiling in the next few months, it would result in an “onset of austerity measures worth 5.1% of American GDP,” or $804.5bn, Margaret Bogenrief from ACM Partners told Business RT.

Going over the fiscal cliff -- The "fiscal cliff" refers to a broad set of tax increases and spending cuts that under current U.S. law will take effect in January. A recent assessment by Bank of America Merrill Lynch estimates the tax increases in 2012 could come to $470 B and spending cuts another $250 B, for a combined fiscal shock of $720 B, or 4.6% of GDP. A fiscal contraction of this size in an economy as weak as the United States would likely be enough to send the country back into a recession. Since that's not an outcome either party wants to see, my assumption has been that somehow Congress and the President will find a way to avoid it. Some respected analysts have suggested to me that there is one political reason that our leaders might prefer to go over the cliff and then try to back our way up. The advantage is one of framing-- once we've gone over the cliff, their position can be described relative to the new status quo, namely, every politician can claim to be in favor of tax cuts, but with the Democrats opposing "new tax cuts for the wealthy." If we were to drive over the cliff before trying to back up, one of the logistically cumbersome changes to undo involves the alternative minimum tax, since the changes here concern taxes owed on income earned in calendar year 2012. Business Week explains: the number of households facing the alternative tax would increase to 32.9 million from 4.4 million, according to the Internal Revenue Service. That's an average unanticipated tax increase of about $2,800. The effect from the AMT, as the parallel tax is known, would be immediate in early 2013 because Congress hasn't addressed the change for tax year 2012, and taxpayers start filing returns in January. A retroactive AMT change is much more cumbersome than retroactive changes in the 2013 income tax rates, which can be handled through paycheck-withholding adjustments

Fiscal cliff looms over campaign climax - Some of the largest US asset managers and pension funds issued an urgent warning over America's looming budget crisis, underlining concern in the markets of a damaging political stand-off in the event of a narrow election victory for Barack Obama. Even as Mr Obama and Mitt Romney made their last pitches to voters, the investors called on Congress to do a deal to avert the "fiscal cliff", $600bn in spending cuts and tax rises set to take effect on January 1 if changes to the law are not agreed. Such fiscal austerity could push the economy into a recession next year, the Congressional Budget Office and the Federal Reserve have warned. "America is facing an urgent crisis, barely discussed during the fall's election campaign," said the group of investors led by BlackRock and joined by pension systems from Florida, Utah, Texas and Illinois, in full-page advertisements placed in leading US newspapers on Monday. "Every day we go without a resolution to the fiscal cliff will erode confidence," said Larry Fink, head of BlackRock which oversees $3.6tn for investors. He said US companies held $1.7tn in cash, "a huge reservoir of money standing by to be put back into the economy" if confidence improves, if there was a fix that is seen as "tangible and credible".

U.S. Vows to Avoid Falling Over Fiscal Cliff Amid G-20 Warning -- The U.S. gave an election-eve commitment to “carefully calibrate” its budget retrenchment amid global warnings that a rush of austerity would harm the weak world economy. As Americans prepared to choose a president, Group of 20 finance chiefs said after talks yesterday in Mexico City that the U.S. pledged to avoid a “sharp fiscal contraction” in 2013. That’s when $607 billion of automatic tax increases and spending cuts are set to take effect unless lawmakers act. “Time is of the essence and significant policy uncertainty in Washington must be addressed,” International Monetary Fund Managing Director Christine Lagarde told reporters. “It will be important for the U.S. to address quickly the so-called fiscal cliff.” The push for U.S. action took center stage at the G-20 meeting during which finance ministers also agreed to dilute their two-year-old budget-cutting goals. Their new vow, to ensure the “pace of fiscal consolidation is appropriate to support recovery,” highlights increased concern that government belt-tightening would threaten an expansion the G-20 labeled modest. The statement “reflects how the consensus has become less austere,” said Torsten Slok, chief international economist at Deutsche Bank AG in New York. “Previously, austerity was thought best, but markets don’t seem to believe that now and politicians are recognizing they have to be realistic over what can be achieved.”

A Sober Wake-Up Call The Morning After - President Obama was re-elected yesterday, and we wish him well. But the news is already ancient, given the pressing demands of defusing the fiscal cliff threat--a deep round of tax hikes and spending cuts slated to start in January if politicians don't intervene. Failure isn't an option here, given the dire effects these cuts and tax hikes could inflict on the still-struggling economy. Unfortunately, that's the likely scenario if politics as usual prevails in the weeks ahead. It's hard to imagine anything else at the moment, given the rancorous, hyper-partisan atmosphere that's defined the Beltway bunch for the past year. Maybe the sour mood will evaporate now that Obama has won a fairly decisive victory in the Electoral College—303 votes for Obama vs. Romney's 206, with 270 needed to clinch the deal. Maybe, but don't count on it. There are several factors that will impede a quick solution to the fiscal troubles that loom, starting with the fact that the U.S. government remains divided: A Democrat in the White House and a Democrat-controlled Senate paired with a Republican-dominated House of Representatives. In other words, nothing much changed yesterday in terms of the balance of power in Washington, and so the potential for political dysfunction is as strong as ever. It's an open question if a lame duck Congress will work with the President to resolve the fiscal cliff risk that threatens to push the economy into recession. The same question can and should be posed from the perspective of 1600 Pennsylvania Avenue: Can the President work with a lame duck Congress? We're about to find out, and the stakes couldn't be higher.

Re-elected Obama would push quickly for fiscal deal -party aides - If President Barack Obama wins re-election, he's expected to move quickly, perhaps within a day, to renew his bid for a bipartisan deal to avert a "fiscal cliff" that threatens to push the United States into recession, top Senate Democratic aides said on Monday. A victorious Obama could reach out to Republicans as early as Wednesday and pledge that, with the election decided, it's time to find common ground to deal with the year-end expiration of Bush-era tax cuts and the launch of automatic spending cuts that would suck $600 billion out of the economy in 2013. "He wants to get the process started immediately," one aide said. "We could move quickly," another aide said, explaining that the basic ingredients of any deal - increased tax revenues coupled with cuts in entitlement programs - have been debated thoroughly for the past two years. "Everyone knows what needs to be done," he said. Two Democratic aides said White House officials have discussed the matter with top Senate Democrats, though it remains unclear exactly how a re-elected Obama would proceed.

Fitch: U.S. must fix fiscal cliff to keep AAA - President Barack Obama won't enjoy a fiscal honeymoon after winning re-election, with pressure on U.S. officials to resolve the so-called fiscal cliff and other issues in order to maintain the country's AAA credit rating, Fitch Ratings said Wednesday. "The economic policy challenge facing the president is to put in place a credible deficit-reduction plan necessary to underpin economic recovery and confidence in the full faith and credit of the [United States]. Resolution of these fiscal policy choices would likely result in the U.S. retaining its AAA status from Fitch," the firm said. Failure to avoid the fiscal cliff -- a combination of tax hikes and spending cuts that will come into effect on Jan. 1 unless politicians reach a budget deal -- and raise the country's debt ceiling in a timely manner would likely result in a downgrade in 2013, said Fitch, which has a negative outlook on the U.S. credit rating. Rival firm Standard & Poor's last year stripped the U.S. of its AAA rating on debt worries

Election Results: Budget Debate Got More Difficult - There's no doubt in my mind that the election results mean that the budget debate just got much, much more difficult. If you were wondering/hoping/praying that a deal would be more likely after the election than it was before, you will be very disappointed.

‘Fiscal cliff’ clock starts in earnest as election fades to background - President Obama returns to Washington from the campaign trail Wednesday to face an epic year-end battle over taxes and spending that could ultimately tame the national debt and advance his ambitions for a second term. The president, who won reelection late Tuesday, must now confront the “fiscal cliff,” nearly $500 billion in automatic tax hikes and spending cuts set to take effect in January that could throw the nation back into recession.If Obama can engineer a compromise to avert the cliff with the freshly reelected Republican House, he could set the stage for progress on other second-term priorities, including immigration reform, climate change and investments in education and manufacturing. Such a compromise could also infuse fresh energy into an economic recovery that has suffered from uncertainty over the future of federal budget policies. “Getting a deal on long-term fiscal soundness is paramount to move forward and to see the economy really keep improving,” said Bill Daley, Obama’s former chief of staff. It will also “give confidence that the political system can address a major issue.”

Back to Work, Obama Is Greeted by Looming Crisis : Newly re-elected, President Obama moved quickly on Wednesday to open negotiations with Congressional Republican leaders over the main unfinished business of his term — a major deficit-reduction deal to avert a looming fiscal crisis — as he began preparing for a second term that will include significant cabinet changes. Mr. Obama, while still at home in Chicago at midday, called Speaker John A. Boehner in what was described as a brief and cordial exchange on the need to reach some budget compromise in the lame-duck session of Congress starting next week. Later at the Capitol, Mr. Boehner publicly responded before assembled reporters with his most explicit and conciliatory offer to date on Republicans’ willingness to raise tax revenues, but not top rates, together with a spending cut package. “Mr. President, this is your moment,” said Mr. Boehner, a day after Congressional Republicans suffered election losses but kept their House majority. “We’re ready to be led — not as Democrats or Republicans, but as Americans. We want you to lead, not as a liberal or a conservative, but as president of the United States of America.” His statement came a few hours after Senator Harry Reid, leader of a Democratic Senate majority that made unexpected gains, extended his own olive branch to the opposition. While saying that Democrats would not be pushed around, Mr. Reid, a former boxer, added, “It’s better to dance than to fight.”

What does President Obama’s re-election mean for the ‘fiscal cliff?’ - With the end of the 2012 election, policymakers’ focus will pivot to the so-called “fiscal cliff” of legislated spending reductions and expiring tax cuts scheduled for 2013, which are projected to induce a recession if they materialize. So what does President Barack Obama’s re-election imply for navigating the “fiscal cliff,” both in terms of his budgetary proposals’ economic impacts and their political viability? The “fiscal cliff” exposes that the pace of deficit reduction must be moderated to sustain economic recovery. “Cliff,” however, is a terrible metaphor because it implies a false dichotomy; we prefer “obstacle course” as the numerous separable policies should be weighed on their merits. A recent paper I coauthored with my colleague Josh Bivens concluded that the upper-income Bush-era tax cuts and recent estate tax cuts fail any reasonable cost-benefit analysis and should expire; these policies are the least supportive of jobs of all fiscal obstacle course components. Expiration of remaining stimulus measures—notably the payroll tax cut and emergency unemployment benefits—and looming spending cuts from last summer’s debt ceiling deal actually pose the gravest economic drags. And temporary stimulus could easily offset small economic headwinds from raising taxes. The president’s most recent budget request actually adheres closely to this framework. On net, the president’s budget would increase the budget deficit for 2013 relative to the “current policy” baseline in which most expiring provisions are assumed to continue, which is important because this baseline includes sizable fiscal contraction that should be moderated (notably, the payroll tax cut and emergency unemployment benefits are assumed to expire). Increased government investment and spending would boost employment by about 1.1 million jobs in 2013, as we estimated in another recent paper. This amounts to substantially moderating the pace of deficit reduction for 2013.

Obama's Next Economy: Why He Must Take This Opportunity to Reframe the Economic Debate - Robert Reich - When the applause among Democrats and recriminations among Republicans begin to quiet down — probably within the next few days — the President will have to make some big decisions. The biggest is on the economy. His victory and the pending “fiscal cliff” give him an opportunity to recast the economic debate. Our central challenge, he should say, is not to reduce the budget deficit. It’s to create more good jobs, grow the economy, and widen the circle of prosperity. The deficit is a problem only in proportion to the overall size of the economy. If the economy grows faster than its current 2 percent annualized rate, the deficit shrinks in proportion. Tax receipts grow, and the deficit becomes more manageable. But if economic growth slows – as it will, if taxes are raised on the middle class and if government spending is reduced when unemployment is still high – the deficit becomes larger in proportion. That’s the austerity trap Europe finds itself in. We don’t want to go there. This is why January’s so-called “fiscal cliff” — $600 billion in automatic spending cuts and tax increases – is so dangerous. It’s too much deficit reduction, too soon. Tax increases on the middle class would reduce their spending just when the economy needs that spending in order to keep growing, and cuts in government’s own spending would make the problem worse. If we go over the fiscal cliff, we’re in another recession. Don’t just take my word for it. That’s also the view of the Congressional Budget Office and most private economic forecasters. The way to ensure continued growth is to continue the President’s payroll tax cut and extend the Bush tax cuts for income under $250,000, and continue government spending.

Greenspan: U.S. Must Embrace Fiscal Responsibility - Former U.S. Federal Reserve Chairman Alan Greenspan said Wednesday the U.S. needs to return to fiscal responsibility, and that “all the easy answers have already been tried.” Speaking with Guillermo Ortiz, formerly Mexico’s central bank president but now a chairman of Mexican bankGrupo Financiero Banorte, Mr. Greenspan said the U.S. needs to increase taxes, but more importantly it needs to cut spending. In a discussion held before Banorte board members and clients, Mr. Greenspan described the current situation in the U.S. as “scary,” saying members of Congress are reluctant to “reach across the aisle” to clinch bipartisan deals. The large amount of cash that corporations and banks appear to be hoarding reflects a lack of confidence and uncertainty about the future, he said. In the case of banks, they will continue to hold onto large amounts of cash until they see better opportunities in the market to lend it out, the former Fed Chairman said. Greenspan had kind words for his successor, Ben Bernanke, calling him a “capable economist.”

Waiting for the bond vigilantes - Nick Rowe --- Paul Krugman is right if he is talking about a small attack by the bond vigilantes. It's a good thing, because it increases Aggregate Demand, which is what the US economy needs. But too much of a good thing will be a bad thing.A large attack by the bond vigilantes would be a bad thing, because it would increase Aggregate Demand too much. That would force the Fed to increase interest rates a lot, and that would force the US government to raise taxes and/or cut spending to cover the increased costs of servicing the debt. If the bond vigilantes suspected that the US government could not or would not raise taxes and/or cut spending to cover the increased cost of servicing the debt, the bond vigilantes would all attack en masse. If the debt were small, the amount by which taxes would need to be raised and/or spending cut to cover the increased debt service costs would be small too, and it could easily be done. But if the debt were large, the amount by which taxes would need to be raised and/or spending cut to cover the increased debt service costs would be large too, and it could not easily be done.

Economists Worry About Fiscal Cliff Resolution - Economists at Wall Street’s biggest banks are warning that a resolution of the year-end “fiscal cliff” situation remains elusive despite the outcome of elections Tuesday. Forecasters are worried that since the levers of government are in essentially the same hands as before the election, lawmakers may be hardening themselves against any form of compromise to deal with a threat many economist say could bring a new recession.The clock is ticking: At year end, broad-based Bush-era tax cuts are set to expire at the same time a series of drastic government spending cuts are set to kick in automatically. Lawmakers generally acknowledge something does, in fact, need to be done, but that hasn’t made a solution any easier.The central problem is the lack of change. President Barack Obama was reelected. Democrats retained control of the Senate, while Republicans held on to the House of Representatives. The fiscal cliff can only be resolved if lawmakers work together.“Returning to status quo likely means all sides see the voters as supporting their views, which means reaching compromise is not likely to get any easier,”

Business Groups: President Must Use Mandate to Face Down Fiscal Cliff - Business organizations said Wednesday Barack Obama‘s re-election gives him a mandate to quickly address the pending fiscal cliff and work for deficit reduction and tax reform. The groups, however, stressed the two goals shouldn’t both be tackled in the next few months. “There isn’t much time,” said John Engler, president of the Business Roundtable, referring to the lame-duck session of Congress. “At minimum you have to get the fiscal cliff under control” by extending existing tax rules through 2013 and avoiding steep cuts to military spending and other government budgets. Mr. Engler said any type of “grand bargain” should be put off until next year to avoid the risk that Congress ends up gridlocked in an attempt to enact wider reforms before mid-January. “The history of these sessions is pretty dismal,” he said on a conference call with reporters. “If you want big dramatic changes to tax policy, you do that as part of the grand bargain.” For example, if Democrats insist of raising taxes on the wealthiest Americans as part of a fiscal-cliff deal, a compromise could fall apart. “A tax increase on that group is not going to solve fiscal-cliff or long-term deficit issues,” said Greg Casey, president of the Business Industry Political Action Committee. “It’d be nice if there was a cease fire until we understand what the larger proposals will be.”

What Is the Fiscal Cliff? - Unless the law is changed, or Congress and the president find another way to trim the deficit, on Jan. 1 the following spending cuts and tax changes will automatically kick in. Click the image for full-size graphic.

IMF Tells G-20: ‘Temporary’ U.S. Fiscal Cliff a ‘Medium-Probability Event’ -- International Monetary Fund officials warned global financial leaders this week they believe there is a “medium probability” the U.S. government will fail to reach a deal preventing large spending cuts and tax increases from taking effect in the new year, a package of measures known as the “fiscal cliff.” The IMF has previously warned that failure to reach an agreement on the $700 billion package–roughly 4.5% of gross domestic product–would push the country into recession. But the warning in a report given to financial leaders from the Group of 20 industrial and developing nations meeting this week is the first time fund officials have estimated the odds of the feared event materializing. Fund staff said the severity of the economic effects partly depends on the duration of the cliff.

IMF urges permanent fix to U.S. 'fiscal cliff' - The International Monetary Fund on Thursday urged the United States to quickly reach an agreement on a permanent fix to avoid automatic tax hikes and spending cuts early next year, saying a stop-gap solution could be harmful to the global economy. In a report prepared for the Group of 20 finance ministers' meeting in Mexico on November 4-5 and published on Thursday, the IMF warned that the euro zone crisis and the threat of a political impasse in Washington over the looming fiscal cliff posed the biggest risks to the world economy. The IMF has estimated that the tax increases and spending cuts amount to $700 billion in 2013. Unless avoided, this could contract U.S. gross domestic product by around 4.5 percent. "A last-minute deal that relies on suboptimal fixes or largely 'kicks the can down the road' may ultimately prove harmful," the IMF said in the report.

The Fiscal Cliff: International Implications - Most of the discussion has focused on the domestic repercussions of going off the fiscal cliff (or as my former colleague Chad Stone calls it, the “fiscal slope”). I think it important to remember that, as the single largest economy, policy in the US has profound implications for economic developments overseas. This is particularly true with the eurozone still in a fragile state, and China growing (relatively) slowly. Jim’s post yesterday tabulated the numerical components of the fiscal cliff. Goldman Sachs has used its own tabulation to estimate the impact on GDP growth over 2013 (SAAR), shown in Figure 1. Note that one difference between the BofA and GS calculations involves the size of the Bush tax cuts. BofA indicates $180 bn, while GS indicates $192. The consequential piece of information is that $56 billion of the $192 bn is associated with high income tax cuts. Retaining the lower tax cuts for incomes less the $250K means the fiscal cliff would be reduced by $136 bn. Nonetheless, with interest rates at zero, contractionary fiscal policy is likely to have large (negative) effects.

Tail risks lurk in the shadows. Fiscal cliff is out in the open. - Merrill conducts a periodic survey of US institutional money managers. One area the survey focuses on is a set of questions on the so-called "tail risks", the less probable but potentially devastating events that negatively impact financial asset valuations. Here are the survey results from September and October of this year. The US fiscal cliff is clearly on people's minds and is quickly becoming the dominant concern in the financial community. If this survey were conducted today, the percentage of participants who would view the upcoming budget cuts and tax increases as the main risk to their portfolios would increase sharply. In fact, based on Google Trends, the public's concerns about the US fiscal cliff have spiked recently.But once certain risks become this widely "respected", they can no longer be called "tail risks". In fact as we saw in today's equity markets, these risks are already being priced into the markets. Tail risks are usually those events that are not fully priced, risks that are ignored, sometimes leading to formations of asset bubbles. What would be an example of such a risk these days? One potential candidate may be some of the US bond markets, for example credit (see discussion on corporate credit). Below is the famous CS Risk Appetite Index shown together with its US Credit Risk Appetite sub-index. US credit risk appetite is approaching what CS refers to as the "euphoria" level.

New CBO report on "Fiscal Cliff" -Note: My baseline forecast assumes a compromise on the fiscal slope (more of a "slope" than a "cliff", and January 1st is not a drop dead date). My current guess is an agreement will be reached AFTER January 1st - so that the Bush tax cuts can expire and certain politicians can claim they didn't vote to raise taxes. I expect the relief from the Alternative Minimum Tax (AMT) will be extended, the tax cuts for low to middle income families will be reenacted, and that most, but not all, of the defense spending cuts will be reversed (aka "sequestration"). However I think the payroll tax cut will probably not be extended, and tax rates on high income earners will increase a few percentage points to the Clinton era levels. It wasn't worth spending much time on this before the election, but now the details will be important. As the CBO notes, a policy mistake could lead to economic contraction (a new recession), but I think some reasonable agreement is likely. From the Congressional Budget Office: CBO Releases a Report on the Economic Effects of Policies Contributing to Fiscal Tightening in 2013 Significant tax increases and spending cuts are slated to take effect in January 2013, sharply reducing the federal budget deficit and causing, by CBO’s estimates, a decline in the nation’s economic output and an increase in unemployment. What would be the economic effects of eliminating various components of that fiscal tightening—or what some term the fiscal cliff?

CBO blog | CBO Releases a Report on the Economic Effects of Policies Contributing to Fiscal Tightening in 2013 - Significant tax increases and spending cuts are slated to take effect in January 2013, sharply reducing the federal budget deficit and causing, by CBO’s estimates, a decline in the nation’s economic output and an increase in unemployment. What would be the economic effects of eliminating various components of that fiscal tightening—or what some term the fiscal cliff? To answer that question, today CBO released a report—Economic Effects of Policies Contributing to Fiscal Tightening in 2013. This report provides additional details about the agency’s estimates—originally released in its August report An Update to the Budget and Economic Outlook: Fiscal Years 2012–2022—of the economic effects of reducing fiscal tightening. As CBO projected in August, the sharp reduction in the deficit will cause the economy to contract but will also put federal debt on a path more likely to be sustainable over time. If certain scheduled tax increases and spending cuts would not take effect and current tax and spending policies were instead continued, the economy would grow in the short term, but the government’s debt would continue to increase.

Economic Effects of Policies Contributing to Fiscal Tightening in 2013 - CBO - Substantial changes to tax and spending policies are scheduled to take effect in January 2013, significantly reducing the federal budget deficit. According to CBO’s projections, if all of that fiscal tightening occurs, real (inflation-adjusted) gross domestic product (GDP) will drop by 0.5 percent in 2013 (as measured by the change from the fourth quarter of 2012 to the fourth quarter of 2013)—reflecting a decline in the first half of the year and renewed growth at a modest pace later in the year. That contraction of the economy will cause employment to decline and the unemployment rate to rise to 9.1 percent in the fourth quarter of 2013. After next year, by the agency’s estimates, economic growth will pick up, and the labor market will strengthen, returning output to its potential level (reflecting a high rate of use of labor and capital) and shrinking the unemployment rate to 5.5 percent by 2018. Output would be greater and unemployment lower in the next few years if some or all of the fiscal tightening scheduled under current law—sometimes called the fiscal cliff—was removed. However, CBO expects that even if all of the fiscal tightening was eliminated, the economy would remain below its potential and the unemployment rate would remain higher than usual for some time. Moreover, if the fiscal tightening was removed and the policies that are currently in effect were kept in place indefinitely, a continued surge in federal debt during the rest of this decade and beyond would raise the risk of a fiscal crisis (in which the government would lose the ability to borrow money at affordable interest rates) and would eventually reduce the nation’s output and income below what would occur if the fiscal tightening was allowed to take place as currently set by law.

Counterparties: Cliff Notes - The fiscal cliff (née taxmageddon) has been looming for months — yet, as Binyamin Appelbaum says, it never got any real traction during the campaign. But now that the campaign is over, the issue is everywhere. After all, if Congress doesn’t act, we’re headed straight for another recession, thanks to a mix of automatic spending cuts and expiring tax cuts. (For background, see our previous posts. The WSJ has a simple visualization of what’s in the fiscal cliff; Tracy Alloway flags a handy calendar, which includes when the debt limit will likely be reached). It’s an old topic, but there are brand-new trial balloons! In a statement the NYT called ”conciliatory”, Speaker of the House John Boehner said his party would now be open to “new revenues” in exchange for entitlement cuts and/or tax reform. This may mean that Obama may be finally making progress in what Joshua Green calls the president’s long “battle for revenue”. In the suddenly more pleasant world of post-election politicking there may even be something like common ground: Grep Ip and Peter Orszag both say that there might be short-term solutions which eases the economic pain of the fiscal cliff while giving Congress time to wrangle over the really hard budget decisions. (This is also known, in some circles, as “kicking the can down the road”.) The CBO today released a broad guide to three basic debt-reduction scenarios, while the Center on Budget and Policy Priorities has another approach: aim a bit lower. Instead of obsessing over coming up with the “almost mythical” $4 trillion in cuts suggested by proposals like the Simpson-Bowles plan, why not cut half that and call it a day? A deficit reduction package that size, the CBPP’s Richard Kogan writes, would stabilize our debt over the next decade and buy crucial time to evaluate how to properly cut health care costs — a question we’re only beginning to answer.

CBO on "Ultimate Can Kicking" -The Congressional Budget Office is out with a very well timed report on what the hell should be done with debt, deficits, taxes and the economy. There is a lot of information in the reports.. (link), (link) I doubt that too many of the folks in Congress will bother to read it. I looked through it; I think the following chart is the one the deciders in D.C. will focus on: Lots of policy options are measured in the chart. Think like a politician, and go to the bottom line. What set of proposals has the biggest bang? My summary from the CBO chart:

- -Totally junk the scheduled spending cuts for the military.

- -Do away with all of the mandatory non-defense cuts (sequestration).

- -Don’t do anything with taxes. Roll over everything for a couple of more years.

- -Extend the 2% payroll tax break for two years.

If we kick the can down the road for a few more years, what do we get? The deep thinkers have come up with numbers that look pretty attractive. The CBO thinks that significant benefits could be realized as soon as September 30, 2013.

Kick the Can, Please - As Dimitri Papadimitriou recently observed, the overwhelming push for austerity in the United States is partly driven by the sense that deficit reduction simply cannot wait: Many in Washington and the media are convinced that the recovery is well underway, and if spending cuts and tax increases are delayed for even a year it will be too late to tame inflation and tighten fiscal policy on a soaring economy. The urgency rests on unfounded optimism. We still have a very long way to go before the economy is anywhere near healthy enough to heat up. The GDP is now, and has long been, far below trend. Here’s how Papadimitriou and Greg Hannsgen illustrate the point in a recent policy brief: It is rather odd to be concerned about deficit reduction coming “too late” (i.e. that the black line will rise above the pink line), given how far we are from the historical growth trend. As Papadimitriou and Hannsgen put it: “Based on the present state of the economy, any notion that implementing better policy would be mostly a matter of precise timing is patently absurd. The gap between recent real GDP growth and the historical trend is so large that the danger of overshooting the trend is hard to imagine.”*

Debt Ceiling Complicates a Tax Shift - — Come January, should Congress fail to act, the United States will face more than immense tax increases and spending cuts. It will also run out of room to finance its large running deficits. The Treasury Department expects the country to hit its debt ceiling, a legal limit on the amount the government is allowed to borrow, close to the end of the year. That would give Congress only a matter of weeks to raise the ceiling, now about $16.4 trillion, before sending financial markets into a panic. Congressional leaders have made clear that the debt ceiling will be part of the intense negotiations over the so-called fiscal cliff, with many members unwilling to raise the ceiling without a broader deal. That has raised financial analysts’ worries of a financial market panic over the ceiling in addition to the slow bleed of the tax increases and spending cuts. Congressional action is required to raise the debt limit. The Treasury can jostle payments for a few months. But expenses will eventually overwhelm revenue, putting the administration in the position of choosing which bills to pay. It might stop paying soldiers, for instance, or sending Social Security payments.