Fed's Balance Sheet Grows in Latest Week - The Fed's asset holdings in the week ended Dec. 12 increased to $2.919 trillion, up from $2.861 trillion a week earlier, it said in a weekly report released Thursday. The Fed's holdings of U.S. Treasury securities increased to $1.661 trillion on Wednesday from $1.654 trillion a week earlier. The central bank's holdings of mortgage-backed securities rose to $928.80 billion from $883.65 billion a week ago. The Fed's portfolio has tripled since the financial crisis of 2008 and 2009 as the central bank bought government bonds and mortgage-backed securities in an effort to keep interest rates low and to stimulate the economy.Thursday's report showed total borrowing from the Fed's discount lending window was $827 million Wednesday, down from $959 million a week earlier. Commercial banks borrowed $5 million Wednesday, up from $2 million a week earlier. U.S. government securities held in custody on behalf of foreign official accounts rose to $3.221 trillion, up from $ 3.204 trillion in the previous week. U.S. Treasurys held in custody on behalf of foreign official accounts increased to $2.867 trillion, up from $2.850 trillion in the previous week. Holdings of agency securities rose to $318.29 billion, up from the prior week's $317.68 billion

FRB: H.4.1 Release--Factors Affecting Reserve Balances--December 13, 2012

After Twist, What Is the Fed’s Next Move? - TIME is running out for Operation Twist, the Federal Reserve stimulus program named for that hip-swiveling dance from the 1960s. The Fed’s twist is scheduled to end soon, mainly because the central bank is running low on the short-term securities that keep the action going. Decorum may prevent it from adopting “Gangnam Style” moves right now, but the Fed’s mesmerizing dance with the bond market isn’t over yet. “The bond market is counting on the Fed — and can keep counting on it — to hold short-term interest rates near zero for some time to come,” said Kathy A. Jones, fixed-income strategist for the Schwab Center for Financial Research. And with the weak economy vulnerable to a shock if the Congress and White House don’t reach an agreement soon on fiscal policy, the Fed is likely to introduce further innovations, perhaps as early as this week. The Fed’s hypnotizing moves have captivated the bond market for many months, said Ed Yardeni, an independent economist. “The stock market still reacts to news events these days; the bond market barely does. The Fed has put it in a nearly perpetual rally.” That can’t last forever, but ultralow yields and remarkably rich prices have persisted largely because of the Fed’s daring experiments and interventions.

Fed Balance Sheet to Reach $4 Trillion With Next Announcement = Call it QE Whatever. The Federal Reserve will “amplify record accommodation” by announcing $45 billion in monthly Treasury buying that will push its balance sheet to almost $4 trillion, according to a Bloomberg survey of economists. The news service reports that 48 of 49 economists predict that the Federal Open Market Committee on Wednesday will purchase Treasuries to bolster an existing program to buy $40 billion in mortgage bonds each month. The panel pledged in October to continue that plan until the labor market improves "substantially." "It's going to be massive and open-ended in size," Joseph LaVorgna, chief U.S. economist at Deutsche Bank Securities Inc. in New York and a former New York Fed economist, told Bloomberg. They are expanding the balance sheet beyond $2.86 trillion in a bid to spur growth and lower an unemployment rate of 7.7%.

Thresholds for the Fed -The idea here is pretty well known by now: rates stay low until unemployment falls below x per cent as long as inflation remains below y per cent. As I understand the state of play, pretty much everyone on the FOMC prefers this approach to the mid-2015 date, and discussion is well advanced. The challenge is to find a good formulation for x and y that everyone can agree on. My guess is there may be some kind of staff proposal at this FOMC meeting, but more likely one for comment by the committee, rather than one ready to act on. Choosing x and y is tricky. Here are some thoughts on how the Fed may approach it.When does the Fed want to raise rates? The first thing is to understand in what conditions the Fed expects to raise rates for the first time. A chart used by vice chair Janet Yellen in a recent speech helps. The path to look at is the blue line – optimal policy – which is influential within the Fed. It is derived by running repeated simulations to find the path of policy that best trades off unemployment and inflation. Looking at the blue line in the bottom chart, the first rise in interest rates happens in early 2016. Compare that with the top two charts, and at that time the simulation shows unemployment at 6 per cent, while inflation never rises much above 2.25 per cent. This kind of result – suggesting you can keep rates low pretty much all the way back to full employment – are common in these models (Note: an important issue with the optimal policy path is whether you can commit to staying on the blue line in 2016 and 2017 when inflation may be above target).

Fed Statement Following December Meeting - The following is the full Fed statement following the December meeting.

Parsing the Fed: How the Statement Changed - Fed watchers closely parse changes between statements to see how the Fed's views are evolving. The following tool compares the latest statement with its immediate predecessor.

FOMC Statement: Expand QE3, Sets Thresholds of 6.5% Unemployment Rate, 2 1/2 Inflation - The thresholds are huge! FOMC Statement: To support continued progress toward maximum employment and price stability, the Committee expects that a highly accommodative stance of monetary policy will remain appropriate for a considerable time after the asset purchase program ends and the economic recovery strengthens. In particular, the Committee decided to keep the target range for the federal funds rate at 0 to 1/4 percent and currently anticipates that this exceptionally low range for the federal funds rate will be appropriate at least as long as the unemployment rate remains above 6-1/2 percent, inflation between one and two years ahead is projected to be no more than a half percentage point above the Committee’s 2 percent longer-run goal, and longer-term inflation expectations continue to be well anchored. The Committee views these thresholds as consistent with its earlier date-based guidance. In determining how long to maintain a highly accommodative stance of monetary policy, the Committee will also consider other information, including additional measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial developments. When the Committee decides to begin to remove policy accommodation, it will take a balanced approach consistent with its longer-run goals of maximum employment and inflation of 2 percent.

More Bond Buying and Thresholds, by Tim Duy - The FOMC statement was released this morning. Key points are that Operation Twist will be converted one-for-one to an outright purchase program and the long-debated issue of thresholds became a reality. First thoughts: Inflation both low in near-term and longer-term inflation expectations remain anchored. Nothing too surprising here as it seems broadly consistent with the tenor of recent speeches by Fed speakers. They continue to see strains in global financial markets...although this seems odd, as it seems that financial markets have calmed considerably in recent months. The FOMC reaffirms its commitment to long-term price stability.Bond buying, key addition: The Committee also will purchase longer-term Treasury securities after its program to extend the average maturity of its holdings of Treasury securities is completed at the end of the year, initially at a pace of $45 billion per month. I am not surprised, but I was cautious that the Fed would choose to pull the trigger on a complete conversion of Operation Twist to an outright purchase program. I think the St. Louis Federal Reserve President James Bullard is right when he notes that this is a more dovish policy. The Fed has more than doubled the pace of the balance sheet expansion, a much more stimulative stance - unless, of course, we are deep into the territory of diminishing marginal returns. We all knew thresholds were coming, but in general did not expect it this meeting: the Committee decided to keep the target range for the federal funds rate at 0 to 1/4 percent and currently anticipates that this exceptionally low range for the federal funds rate will be appropriate at least as long as the unemployment rate remains above 6-1/2 percent, inflation between one and two years ahead is projected to be no more than a half percentage point above the Committee’s 2 percent longer-run goal, and longer-term inflation expectations continue to be well anchored. The Committee views these thresholds as consistent with its earlier date-based guidance. When the Committee decides to begin to remove policy accommodation, it will take a balanced approach consistent with its longer-run goals of maximum employment and inflation of 2 percent.

The Fed Adopts Numerical Thresholds for Inflation and Unemployment - The Federal Reserve's monetary policy committee announced today that it will continue its policy of maintaining exceptionally low interest rates and expand its "quantitative easing" program by purchasing bonds at the rate of $85 billion per month in a move to boost economic growth. But the big news is the central bank's adoption of numerical thresholds that, if crossed, will trigger a reassessment of its existing policies. Specifically, the Fed said it will keep the federal funds rate within the 0 to 0.25 percent range "at least as long as the unemployment rate remains above 6.5 percent, inflation between one and two years ahead is projected to be no more than a half percentage point above the committee's 2 percent longer-run goal, and longer-term inflation expectations continue to be well anchored." This signals a change from time-based Fed policies that end on a certain date to those that are contingent on the state of the economy. The latter type of policy is considered more effective and less likely to cause credibility problems if, for example, the economy does worse than expected and the Fed is forced to extend the program beyond its pre-announced end. But it's important to recognize that these are triggers, not thresholds. A 6.5 percent unemployment trigger, for example, means that if the unemployment rate falls below this level, a new policy is necessarily triggered, meaning the policy ends. But a 6.5 percent threshold brings about a discussion and a reassessment at the Fed of the appropriate policy -- but policy does not necessarily change. The Fed is instituting thresholds, not triggers, and its important to understand the difference.

More Of The Same... With "Thresholds" - Fed Chairman Ben Bernanke made it clear... again. Interest rates will remain low, even when the labor market shows stronger signs of growth. He said that if inflation doesn't exceed an annual rate of 2.5%, and unemployment stays above 6.5%, the Fed would keep its target rate near zero percent. Laying out "thresholds" is something new, but the basic message remains the same: low rates and no plans to change the status quo any time soon. As Bernanke explained at yesterday's press conference:First, as the statement notes, the committee reviews policy as likely to be appropriate at least until a specified threshold is met, reaching one of those thresholds will not automatically trigger immediate reduction in policy accommodation. If unemployment was to decline at a time inflation and expectations were subdued... the committee might judge an increase in target for the federal funds rate to be inappropriate and ultimately in deciding when and how quickly to reduce policy accommodation the committee will follow a balanced approach in seeking to mitigate deviations of inflation from the longer run 2% goal and deviations of employment from estimated maximum level. The 2.5% ceiling for pricing pressure is a "conditional inflation targeting," as Menzie Chinn labels it. As it happens, the market appears to have been anticipating that level in recent days. Yesterday's inflation forecast via the 10-year Treasury yield less its inflation-indexed counterpart was 2.51%, about where it's been all week. It's also interesting to note that the Treasury market's assumption for future inflation has been inching higher this month after bottoming out at around 2.4%.late last month.

Fed Spreads Treasury Purchases Into Shorter-Term Notes - The Federal Reserve’s commitment to buying more Treasurys next year includes a slight adjustment from its existing program, steering some of the monthly purchases away from longer-term bonds and toward shorter-dated notes. The central bank said Wednesday it will buy $45 billion in long-term Treasurys each month. This replaces the soon-to-expire Operation Twist, under which the bank buys $45 billion Treasurys monthly, but funded with sales of an equal amount of short-term notes. The new outright purchase program largely replicates the buying end of Operation Twist, but with a few tweaks on the maturities being targeted.

The Fed Turns Aggressively Dovish With ‘Evans Rule’ - Wednesday’s announcement from the Federal Reserve’s Open Market Committee marks a significant escalation (perhaps the biggest to date) in the Fed’s efforts to boost the economy. Rather than tying monetary policy decisions to far-off points in time, or signaling its intentions through vague pronouncements about whether the economy is showing moderate or modest growth, policy will now be tied directly to hard, numerical targets. Namely, the Fed will keep short-term interest rates near zero as long as unemployment remains above 6.5 percent and the inflation it expects in one to two years is no higher than 2.5 percent. That replaces the previous plan to keep rates near zero until mid-2015. Given the slow pace of job growth, the current plan could mean that rates stay super-low past mid-2015. This is essentially what Charles Evans, President of the Federal Reserve Bank of Chicago, has been arguing for over the last year. Dubbed the Evans Rule, the argument holds that monetary policy shouldn’t be tightened until the economy heals pasts a certain predetermined threshold. In a speech delivered in September 2011, Evans made the point that the Fed should be just as aggressive about fighting high unemployment as it is about high inflation.

Fed’s bond buying will continue until jobless rates drops - Offering greater clarity to financial markets and politicians, the Federal Reserve on Wednesday took the unprecedented step of saying it would continue its controversial bond buying and other steps to stimulate the economy until the unemployment rate falls to 6.5 percent or below and stays there. The Fed’s benchmark federal funds rate, the primary way it influences lending rates across the economy, has been near zero since December 2008. Unable to cut rates any more, the Fed has taken a number of unconventional steps to try and further spark a subpar recovery. Critics, especially Republicans in Congress, contended the steps may eventually spark inflation that’s hard to tame and complained about their open-ended nature. Chairman Ben Bernanke sought to quell that criticism by offering a threshold, the 6.5 percent unemployment rate, which he cautioned was nothing more than a meaningful idea of when the Fed might start pulling back on its accommodative policies and raise interest rates. “It is not a target. What it is is a guidepost of when to begin reduction of accommodation,” Bernanke said in a lengthy news conference, which included calls on Congress to avoid the fiscal cliff and projections that show the Fed slightly downgrading U.S. growth prospects for next year.

QE4 Is Here: Bernanke Delivers $85B-A-Month Until Unemployment Falls Below 6.5% - Forbes: Ben Bernanke continues to make history at the Federal Reserve. On Wednesday, the FOMC announced more quantitative easing at a rate of $85 billion a month for an extended period of time. The Bernanke Fed has also modified its guidance, noting its ultra-accommodative stance will remain in place until the unemployment rate falls below 6.5% and inflation projections remain no more than half a percentage point above 2% two years out. QE4 is here. Only a few months after announcing what had been dubbed QE3, an open-ended $40 billion a month program to buy up mortgage backed securities (MBS), the FOMC decided to extend its asset purchases in 2013 as Operation Twist expires.The Fed will therefore accelerate its rate of balance sheet expansion, easing monetary conditions further. While Operation Twist had been sterilized, which means the Fed sold assets at the same rate as it was gobbling them up, the new program will consist purely of Treasury purchases. Combined with QE3, the Fed will be taking $85 billion in bonds, both Treasuries and MBS, out of the market. The FOMC also decided to begin rolling over its maturing Treasuries as of January. Bernanke’s biggest surprise came in terms of the Fed’s forward guidance. The FOMC moved from a calendar-based guidance to one tied to economic factors, specifically, inflation and unemployment (which constitute the Federal Reserve’s dual mandate): “In particular, the Committee decided to keep the target range for the federal funds rate at 0 to 1/4 percent and currently anticipates that this exceptionally low range for the federal funds rate will be appropriate at least as long as the unemployment rate remains above 6-1/2 percent, inflation between one and two years ahead is projected to be no more than a half percentage point above the Committee’s 2 percent longer-run goal, and longer-term inflation expectations continue to be well anchored"

Fed Launches Contractionary QE4; Continues Unlimited Expansion - As expected, the Fed announced today that QE4 bond buying will start in January. We think Fed policy is contractionary. The announcement of more bond buying doesn’t improve the outlook. . Even though we disagree with the Fed’s decision to buy more bonds, we welcome the openness of the Fed’s discussion about its monetary policy vision. Under QE4, the Fed’s liabilities will quickly expand beyond $3 trillion and, given today’s announcement of an aspiration for 6.5% unemployment, probably above $4 trillion. We expect the growth impact of QE4 to follow the pattern of QE3, QE2 and Operation Twist, which saw steady declines in the Fed’s own growth expectations as the QE policies were implemented (see graph in the attachment.) During the press conference, Chairman Bernanke was asked how QE works. He drew on the portfolio rebalancing theory that he had laid out in his 2010 Jackson Hole speech. We don’t think Bernanke’s transmission theory works when private sector credit is constrained by regulatory policy. The Fed is causing a rationing process which channels capital to the government and to assets with similar characteristics at the expense of small businesses (see WSJ Near-Zero Rates Are Hurting the Economy on December 4, 2009 and WSJ How the Fed is Holding Back the Recovery on October 19, 2010.) Fed policy distorts markets, hurts savers, and favors the government at the expense of the private sector. There’s been no change in credit or regulatory policy, so there’s no increase anticipated in the M2 money supply or private sector credit. There’s been no loosening of bank regulatory policy, no increase in expectations for bank leverage and no un-freezing of the money multiplier that connects excess reserves to private sector loan growth, which remains stagnant.

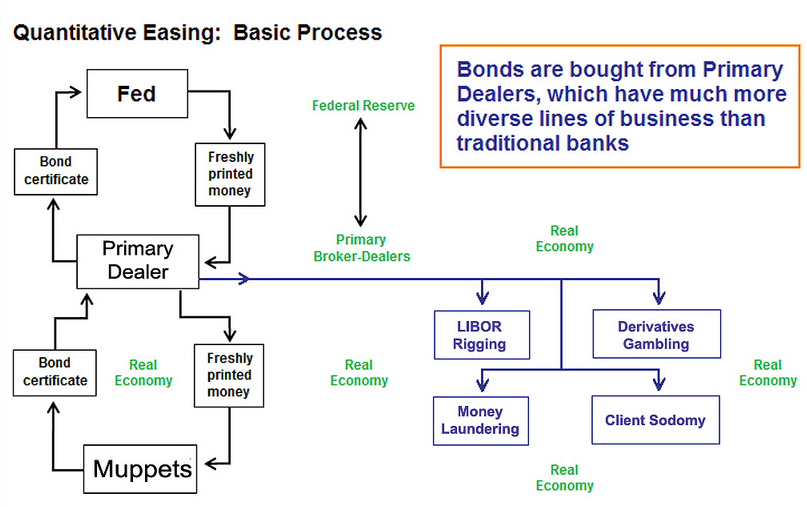

Quantitative Easing, Basic Process (graphic)

Most on Fed See Rates Low Into 2015 - Most Federal Reserve officials continue to expect the central bank to first raise interest rates in 2015, in a projection consistent with new monetary policy thresholds announced by the central bank Wednesday. Fed officials also on balance downgraded slightly their collective outlook for growth, while projecting touch-lower ranges of unemployment and inflation compared to forecasts released in September. On the monetary policy front, 14 of the 19 Federal Open Market Committee members now believe the first increase in monetary policy will come in 2015 or later. Two believe the Fed will raise rates in 2013. In September, 12 FOMC members expected a hike in 2015 and one saw it happening in 2016.

The Federal Reserve Gets Down to Business - Adopting what has come to be known as the Evans Rule, whereby rates remain low until either inflation hits 2.5 percent or unemployment reached their initial target of 6.5 percent, is a remarkable change. Beyond a needed expansion of monetary policy, this represents a major policy victory. How did this happen? The Evans Rule dates from a September 2011 speech given by Charles Evans, the president of the Federal Reserve Bank of Chicago—one of the 12 regional Federal Reserve banks informally led by the New York Federal Reserve. The speech called out the Fed for not taking both parts of its mandate—to keep both inflation and unemployment low—seriously. Evans noted that unemployment was at 9 percent while inflation was near the target, and the Fed didn’t seem that concerned. But those numbers are equivalent to a situation where inflation was higher than expected, say 5 percent, and unemployment was lower, a situation where the Federal Reserve would certainly take notice. In the speech, Evans proposed that the Federal Reserve tie its projections to unemployment while also giving a clear number on the inflation rate it would tolerate. This would prevent the Federal Reserve from keeping the economy in check by its inaction.

New From the Fed: TBG - That is, "Threshold Based Guidance." The Federal Open Market Committee's statement today included the following: To support continued progress toward maximum employment and price stability, the Committee expects that a highly accommodative stance of monetary policy will remain appropriate for a considerable time after the asset purchase program ends and the economic recovery strengthens. In particular, the Committee decided to keep the target range for the federal funds rate at 0 to 1/4 percent and currently anticipates that this exceptionally low range for the federal funds rate will be appropriate at least as long as the unemployment rate remains above 6-1/2 percent, inflation between one and two years ahead is projected to be no more than a half percentage point above the Committee’s 2 percent longer-run goal, and longer-term inflation expectations continue to be well anchored. Since the federal funds rate hit the zero lower bound - four years ago - other monetary policy tools have taken on a more prominent role. One of them is the Fed's ability to influence expectations, which it tries to do by making promises about future policy ("forward guidance"). Because long-term interest rates depend on expected future short term rates, convincing people that short-term rates will be low for longer can bring down long-term rates, and thereby reduce the cost of investment and credit purchases. One of the difficulties that the Fed has to get around, though, is that people believe it places a high priority on keeping inflation low and would tighten policy at any hint of the economy heating up.

Analysis: Why Is the Fed Being So Specific? - The Federal Reserve says it expects to keep rates exceptionally low at least as long as unemployment is above 6.5% and inflation set to stay below 2.5%. PNC Financial Services Senior Economist Gus Faucher discusses the report with The Wall Street Journal Online’s Dan Loney.

The mandate is willing but the tools are weak - Low inflation and full employment have been statutory goals of the Federal Reserve since 1977, but its officials always felt more comfortable with the first than the second. After all, in theory monetary policy can’t alter unemployment in the long run. But the stubbornly weak economy of recent years prompted some at the Fed to question their historical neglect of the second half of their mandate. “The Fed’s dual mandate … has the force of law behind it,” Charlie Evans, president of the Federal Reserve Bank of Chicago, said in September, 2011. “So, if 5% inflation would have our hair on fire, so should 9% unemployment.” Mr Evans argued the Fed should make it clear that unemployment and inflation both carried weight in its decisions by setting thresholds for both that would trigger a policy response. This meant the Fed would explicitly tolerate inflation higher than its target if it wasn’t satisfied with the state of unemployment. Mr Evans' argument was so powerful because it called on the Fed to do nothing more than apply orthodox economic policy reasoning to Section 2A of the Federal Reserve Act. It was also a little bit subversive: Mr Evans' rule was a sort of watered-down nominal GDP targeting. But the Evans rule was much easier for the Fed to swallow than NGDP targeting because it required no radical remake of its operating framework.

Monetary Policy Innovations - It is always interesting to compare the Fed, ECB and Bank of England. For both the Fed and ECB it has been quite a year for innovation. At the Fed the most recent announcements in terms of forward guidance can be seen as just a development of how it began the year, by publishing its own forecasts for interest rates. Once you tell others how you expect policy to develop given one (central) projection of how the economy will go, it is natural to say how it might develop in other circumstances. Just as it seemed to me the first development was eminently sensible (but others disagreed), so I think recent moves are as well. Do they mark a substantial shift in policy? Brad DeLong thinks so, but Paul Krugman is more downbeat. I think the answer depends on the timespan you are looking at. In terms of the very recent developments, they are perhaps not a huge shift, although I agree with Mark Thoma that raising the inflation target from an ‘apparent 2%’ to a ‘definitely at least 2.5%’ is significant. Seen over the year as a whole, and including the idea of continuing QE, I think it is an important change.

Too Little, Too Late? -The FOMC, after over four years of overly tight monetary policy, seems to be feeling its way toward an easier policy stance. But will it do any good? Unfortunately, there is reason to doubt that it will. The FOMC statement pledges to continue purchasing $85 billion a month of Treasuries and mortgage-backed securities and to keep interest rates at current low levels until the unemployment rate falls below 6.5% or the inflation rate rises above 2.5%. In other words, the Fed is saying that it will tolerate an inflation rate only marginally higher than the current target for inflation before it begins applying the brakes to the expansion. Here is how the New York Times reported on the Fed announcement. The Federal Reserve said Wednesday it planned to hold short-term interest rates near zero so long as the unemployment rate remains above 6.5 percent, reinforcing its commitment to improve labor market conditions. The Fed also said that it would continue in the new year its monthly purchases of $85 billion in Treasury bonds and mortgage-backed securities, the second prong of its effort to accelerate economic growth by reducing borrowing costs.But Fed officials still do not expect the unemployment rate to fall below the new target for at least three more years, according to forecasts also published Wednesday, and they chose not to expand the Fed’s stimulus campaign.

How risky is the Fed's major move? - Muhammed El-Erian - A bold and necessary move? Yes, but the Fed's growing activism has limits and is ultimately inconsistent with the proper efficient functioning of a market economy. Wow! That is what I suspect many investors said when they heard Wednesday's policy announcement…. Yesterday's Fed announcement will go down in the history books…. The Fed took two major steps on Wednesday, one expected and one less so. First, it added to its expected purchases of market securities, doubling the dollar amount to $1 trillion for 2013…. Second, the Fed shifted to quantitative (unemployment and inflation) targets for forward policy guidance…. This further leap into the policy unknown was motivated by continued disappointment with the economy's sluggish growth, persistently high unemployment and increasing concern about joblessness becoming more structurally embedded into the economy…. The bad news is that the institution, with its imperfect tools for the challenge at hand and with other federal government entities essentially MIA, may be taking on an unsustainable burden…. [T]he outcome of the Fed's unusual activism is neither predictable nor costless… an increasing risk of collateral damage and unintended consequences… ultimately inconsistent with the proper efficient functioning of a market economy. With a market share that will end 2013 between 30% and 45% depending on the securities, the Fed is heavily involved in markets as both a referee and player. As such, it distorts their functioning, the price discovery process and the allocation of capital.

Why QE4 Will Fail - The Fed turbo-charged the printing press yesterday, turning QE3 into QE4. Yet the stock market closed flat on the day -in fact it sold off after an initial sugar rush rally. Why no party? Perhaps because despite being more open ended (no calendar end date), it is a more constrained edition of QE than previous versions. Operation Twist has been running since September 2011 and has managed to convert $667 billion of short term Treasury Notes into intermediate term Treasury Notes on the Fed's balance sheet. You may recall Operation Twist was the Fed stimulus program wherein it sold $45B/month in short term Treasury Notes to fund buying of intermediate term Treasury Notes, thus avoiding new money printing and balance sheet expansion. However, since the Fed's inventory of short term bonds (3 years and less) is now gone, it won't be able to continue Operation Twist. Instead, it will use $45B per month in freshly printed dollars to fund its purchases of intermediate and longer term Treasury Notes. The Fed is also going to continue buying $40B per month in agency-backed mortgage bonds (what was QE3). So in total, this new action (QE4) will see the Fed buying $85B per month in U.S. Tbonds and Fanny/Freddie bonds with newly printed dollars -essentially debasing the dollar by 1 $trillion per year. The Fed will continue doing this until:

- The unemployment rate drops to 6.5%;

- The inflation rate tops 2.5%;

- The cows come home and the fat lady sings.

QE 4: Folks, This Ain't Normal - Okay, the Fed's recent decision to boost its monetary stimulus (a.k.a. "money printing," "quantitative easing," or simply "QE") by another $45 billion a month to a combined $85 billion per month demonstrates an almost complete departure from what a normal person might consider sensible. To borrow a phrase from Joel Salatin: Folks, this ain't normal. To this I will add ...and it will end badly. If you had stopped me on the street a few years ago and asked me what I thought would have happened in the stock, bond, foreign currency, and commodity markets on the day the Fed announced an $85 billion per month thin-air money printing program directed at government bonds, I would have predicted soaring stock prices on the expectation that all this money would have to end up in the stock market eventually. I would have predicted the dollar to fall because who in their right mind would want to hold the currency of a country that is borrowing 46 cents (!) out of every dollar that it is spending while its central bank monetizes 100% of that craziness? Further, I would have expected additional strength in the government bond market, because $85 billion pretty much covers all of the expected new issuance going forward, plus many entities still need to buy U.S. bonds for a variety of fiduciary reasons. With little product for sale and lots of bids by various players, one of which – the Fed – has a magic printing press and is not just price insensitive but actually seeking to drive prices higher (and yields lower), that's a recipe for rising prices. Then I would have called for sharply rising commodity markets because nothing correlates quite so well with thin-air money printing as commodities. That's what should have happened. But it's not what we're seeing.

Fed’s Fisher Worries About ‘Hotel California’ Monetary Policy - Dallas Fed President Richard Fisher said Friday on CNBC he opposed the Federal Open Market Committee‘s recent decision on employment thresholds and that he was extremely concerned that it would become increasingly difficult to exit the Fed’s accomodative monetary policy. “We are at risk of what I call a ‘Hotel California’ monetary policy, referring to the Eagles’ song, where we can check out any time we want from this program, but we can never leave” due to an engorged balance sheet, he said. Mr. Fisher said he argued that the markets would become overly fixated on the “unemployment target that the Fed put in there, and not on the thresholds,” but he lost his argument. He said there is flexibility in the approach to the 6.5% thresholds as we approach them, as Chairman Ben Bernanke made clear, and if we need to alter monetary policy.

Dallas Fed Richard Fisher: Fed Risks 'Hotel California' Monetary Policy - At least one Fed governor understands the Bernanke Fed's hyper-accommodative monetary policy has no exit. Today on CNBC "Squawk Box", Dallas Fed governor Richar Fisher complained Fed Risks 'Hotel California' Monetary Policy. Dallas Fed President Richard Fisher told CNBC that he's worried the U.S. central bank is in a "Hotel California" type of monetary policy because of its "engorged balance sheet." Evoking lyrics from the famous song by The Eagles, he said he feared the Fed would be able to "check out anytime you like, but never leave." Fisher said on "Squawk Box" that he argued against revealing the new inflation and unemployment targets set by the Fed this week, saying he's worried that the markets will become "overly concerned" with the thresholds. Fisher would not comment on any contingency plans at the Fed should Republicans and President Barack Obama fail to strike a deal to prevent the automatic tax increases and spending cuts from taking effect in the new year. "What you see is what you get here," Fisher said. "We have a hyper-accommodative monetary policy here ... cheap and abundant money that the Fed has made widely available."

Two Fed officials speak out against the latest FOMC policy decision - We are seeing some dissent among the Fed officials with respect to this week's decision.

1. Richmond Federal Reserve President Jeffrey Lacker, who voted against the FOMC's last policy decision, remains uneasy: Reuters: - "I do not believe that tying the federal funds rate to a specific numerical threshold for unemployment is an appropriate and balanced approach to the FOMC's price stability and maximum employment mandates," he said in a statement, referring to the Federal Open Market Committee. Focusing on MBS purchases pushes capital into the housing sector - and according to Lacker should be left to the federal government, not the central bank. Reuters: - "Deliberately tilting the flow of credit to one particular economic sector is an inappropriate role for the Federal Reserve," he said, adding that trying to influence credit allocation within the economy was a function of fiscal policy.

2. Dallas Fed President Richard Fisher calls the latest FOMC action a "Hotel California" policy (with respect to the expansion program, you can "check out anytime you like, but never leave").

The Fed Focuses on the Unemployed - The FOMC just did a great thing. The Federal Reserve tied interest rates and quantitative easing to U.S. labor. The messaging alone is powerful. The Federal Reserve is saying, very clearly, U.S. workers matter. Businesses need to start hiring and increasing wages if they want to actually improve the overall economy. About 5 million people—more than 40 percent of the unemployed—have been without a job for six months or more, and millions more who say they would like full-time work have been able to find only part-time employment or have stopped looking entirely. The conditions now prevailing in the job market represent an enormous waste of human and economic potential. The FOMC set out specific parameters to the ongoing QE3. To support continued progress toward maximum employment and price stability, the Committee expects that a highly accommodative stance of monetary policy will remain appropriate for a considerable time after the asset purchase program ends and the economic recovery strengthens. In particular, the Committee decided to keep the target range for the federal funds rate at 0 to 1/4 percent and currently anticipates that this exceptionally low range for the federal funds rate will be appropriate at least as long as the unemployment rate remains above 6-1/2 percent, inflation between one and two years ahead is projected to be no more than a half percentage point above the Committee’s 2 percent longer-run goal,

Digital threat to Fed’s jobless target - -Functions driven by technology are displacing many human workers. In recent months, something striking has quietly occurred at Exim Bank, the US export credit guarantee agency. For the fourth year in a row, the agency is watching an export boom. So far this year, Exim has provided $35.8bn of export financing to support $50bn of export sales, 25 per cent up on last year. But while that might seem good news for the American economy, there is a crucial catch: so far in 2012, the number of jobs backing those Exim-supported exports has fallen by 12 per cent. Yes, you read that right. In 2012 Exim-supported companies have been selling more widgets (such as planes) and services (such as engineering advice), helping them to post profits, and the economy to grow. But fewer workers were needed to produce these sales, even – or especially – in sectors which are booming (such as engineering design). It is a telling saga for investors, particularly in a week that Ben Bernanke, Fed chairman, has declared that the Fed will not tighten monetary policy until the US jobless rate drops below 6.5 per cent. In some senses, the Exim data may be extreme as they only reflect a tiny slice of corporate America. But they are not an aberration. After all, this year the economy is on track to post growth above 2.5 per cent. However, the unemployment rate has barely fallen, running at 7.7 per cent. Just like those Exim-backed companies, the American economy as a whole now seems to be doing more with the same, or fewer, people. This is jobless growth.

FOMC Projections and Bernanke Press Conference - Here are the updated projections from the FOMC meeting. Here is the video stream. The FOMC is no longer presenting a "date-based guidance" for policy, and instead changed to announcing thresholds for raising the Fed Funds rate based on the unemployment rate and inflation. How this will work will be a key topic of the press conference today. Currently the thresholds are holding rates low "at least" until the unemployment rate is above 6 1/2%, and the inflation outlook "between one and two years ahead" is no more than 2 1/2%, as long as inflation expectations remain "well anchored" - this means inflation could increase to 3% or 4% without an increase in rates, as long as expectations remain anchored and the outlook one to two years ahead is at or below 2 1/2%. This is a significant change in policy guidance. Another key question is: Which will come first, a rate hike or stopping or slowing QE3 (the FOMC will expand QE3 to $85 billion per month in January)? The four tables below show the FOMC December meeting projections, and the September projections to show the change.

A Fed That Is Focused on the Value of Clarity - The Federal Reserve’s decision on Wednesday to announce specific economic objectives for its policies would have stunned and dismayed earlier generations of central bankers, who regarded secrecy as a virtue and obfuscation as a prized technique for manipulating financial markets. “Since I’ve become a central banker, I’ve learned to mumble with great coherence,” Alan Greenspan, a former Fed chairman, told reporters in 1987. “If I seem unduly clear to you, you must have misunderstood what I said.” Until recently, the Fed under Mr. Greenspan and his successor, Ben S. Bernanke, were tentative participants in this revolution. Over the last two years, Mr. Bernanke and his colleagues have announced a series of changes intended to increase the transparency of the Fed’s decision-making. Some of those moves have also transformed the way those decisions are made and, the Fed hopes, increased the power of its efforts to revive the economy. Several of those changes were tied together by Wednesday’s announcement that the Fed would hold short-term interest rates near zero as long as the unemployment rate remained above 6.5 percent and inflation remained under control.

More Monetary Policy Uncertainty - The Fed’s announcements yesterday increase monetary policy uncertainty in two fundamental ways. First, the new quantitative easing announcement implies a gigantic increase in the size of the Fed’s balance sheet and thus effectively an amplification of the policy risks and uncertainty which I have discussed, for example, in this oped with George Shultz and other colleagues in September. The Fed now plans to purchase $85 billion a month of longer-term Treasury and mortgage backed securities until there is substantial improvement in the labor market, which requires a completely unprecedented increase in reserve balances as illustrated in this chart. The chart shows reserve balances held by banks at the Fed. These are used to finance the large scale asset purchases. The chart assumes that substantial labor market improvement is defined by the 6.5% unemployment rate the Fed is using to assess when to raise interest rates. Thus, assuming the central tendency forecast of the FOMC, the announced buying spree will bring reserve balances to about $4 trillion in mid-2005. The risk is two-sided. If the Fed does not draw down reserves fast enough during a future exit, then it will cause inflation. If it draws them down too fast, then it will cause another recession.

Bernanke's Non-Stupidity Pact - Krugman - So, how big a deal was yesterday’s Fed announcement? Philosophically, it was pretty major; in terms of substantive policy implications, not so much. What the Fed did was pledge not to raise rates until unemployment is considerably lower than it is now, or inflation is running significantly above the 2 percent target. One fairly important wrinkle I haven’t seem emphasized: the inflation criterion was couched in terms of the inflation projection, rather than past inflation. This would let the Fed hold rates low even in the face of a blip caused by, say, a sharp rise in commodity prices. It’s fairly clear — although not explicitly stated — that the goal of this pronouncement is to boost the economy right now through expectations of higher inflation and stronger employment than one might otherwise have expected. So philosophically, this represents a conversion to the Evans criterion for rates and the Woodford/Krugman doctrine about monetary policy in a liquidity trap. Substantively, however, there isn’t that much going on here. Basically, Bernanke is promising that the Fed won’t do anything stupid — specifically, that it won’t pull an ECB, and raise rates even though the economy is still depressed and underlying inflation is still low. As it was, however, few people expected the Fed to pull an ECB in any case. That’s reflected in the market reaction: rates actually rose, and expected inflation, as measured by the spread between nominal and real rates, went up only slightly.

Fed presidents discuss economic recovery at Becker Friedman Institute - The presidents of three regional Federal Reserve Banks discussed the Fed’s role in America's recovery from the economic recession at a Dec. 1 panel arranged by and for University of Chicago undergraduates and sponsored by the Becker Friedman Institute. Fed presidents Charles Evans of the Chicago bank; Narayana Kocherlakota, PhD '87, of the Minneapolis bank; and Charles Plosser, PhD'76, of the Philadelphia bank, shared their views on target rates for inflation, interest rates, and unemployment, and other aspects of monetary policy with a student audience of more than 200. In January 2012, the Federal Open Market Committee announced that 2 percent inflation is a desirable limit, with a target of 5.25 to 6 percent unemployment. Evans said that for more than two years, he has been making the case for greater accommodation from the Fed to improve economic outcomes. He favors keeping interest rates low until unemployment declines to 6.5 percent, as long as inflation stays below 2.5 percent. He shared his reasoning: “I’m led to think this way because I’ve considered economic theory and the best stochastic models, and they all seem to indicate a need to continue” greater accommodation. His approach builds in a safeguard at 3 percent inflation, in case inflation takes off more than expected.

How Charles Evans Saved the Recovery - Some revolutionaries wear Guy Fawkes masks and talk about the 1 percent, and some revolutionaries wear suits and talk about policy thresholds. Chicago Fed president Charles Evans is one of the latter. A year ago Evans was the rare dovish dissenter at the Fed. He didn't think it was taking the unemployment half of its dual mandate seriously enough, so he proposed a new, eponymous rule for it to do better. He certainly wasn't the first Fed president to have his own ideas about monetary policy, but a funny thing happened on his way to heterodoxy -- his ideas quickly became the consensus. Now, just a year later, the Fed has fully embraced the so-called Evans rule by linking interest rates to the unemployment rate. Ain't no revolution like a monetary policy revolution.

Central bankers give voice to a revolution - FT.com: Ben Bernanke seemed unusually buoyant at his press conference this week. He smiled – more than once; there was a folksy story about his roots in South Carolina, and a joke about his facility with a southern accent. The chairman of the US Federal Reserve had reason for cheer and for a little pride: his committee had just said it would keep interest rates close to zero until the US unemployment rate falls below 6.5 per cent (it is 7.7 per cent today). For a central bank, let alone the Fed, to tie rates to the economy in this way was without precedent.The move speaks of a quiet revolution that is sweeping over central banks. A day earlier, Mark Carney, currently governor of the Bank of Canada, soon-to-be governor of the Bank of England, became the most senior central banker to praise an even more radical policy: targeting the level of nominal gross domestic product. Instead of having apoplexy, Britain’s chancellor said he wanted a debate. Like most revolutions, it seems to come from nowhere but has deep roots. Like most revolutions, it holds the promise of great good but has the potential for harm. It is crucial that politicians and the public understand what this revolution in central bank thinking is and is not about.

Trendline on the unemployment rate projects the Fed ending zero rate policy by late 2014 - The Fed's new approach to targeting a specific unemployment rate (called the "Evans’ Rule") may shed some light on how long the monetary easing may continue. Credit Suisse did a simple linear extrapolation from the peak unemployment rate in 09. Such approach sets the end of the program for late 2014. That of course assumes the unemployment rate will continue declining in a linear fashion (which may be unrealistic given the structural shift in employment). It also assumes that labor participation (something the Fed is tracking closely, though it's not part of the official target) will improve with falling unemployment - another "leap of faith".This extrapolation gets to the "target" considerably faster than the FOMC's "middle of 2015" projection or even the Fed Funds futures curve market expectation (Feb-2015 contract now implies full 25bp).The new unemployment targeting program (combined with inflation tolerance level) is expected to make for a more flexible policy tool because the FOMC would be less reluctant in adjusting its rate expectations. CS researchers think both the FOMC and the futures markets will adjust to an earlier date as the unemployment rate continues to decline (some comments in brackets [ ] ).

The Fed targets $45 billion in treasury purchases a month; why then did treasuries sell off? - The Fed has announced that in addition to the $40 billion of monthly MBS purchases, it will also commence $45 billion in treasury purchases. This unprecedented open-ended program will swell bank reserves and ratchet up the monetary base. The announcement of this new asset purchase program should be a big positive for treasuries, right? Turns out that it wasn't. Longer dated treasuries rallied immediately after the announcement, but sold off shortly after, now trading at the lows for the week. With the FOMC doves running the show, the Fed announced it would target a specific combination of unemployment and short-term inflation expectations. The two-year inflation expectation (the so-called breakeven rate) however now stands at about 1.3% - which means the Fed has given itself quite a bit of room to get to 2.5%. And that was the reason for the selloff - such an open-ended policy clearly runs inflation risks. Bloomberg: - “The Fed is losing some of its credibility as an inflation fighter,” . “They will allow inflation to go above the long-term target. That’s disappointing for the market.”

Bank reserves still down on the year; should ramp up shortly - Some MBS settlements have now been reflected on the Fed's balance sheet, as agency paper holdings increase. Bank reserves are also gradually moving up, though still down for the year. So far the growth in reserves has been underwhelming.With the newly announced treasury purchases, this should pick up steam. And the settlement schedule will be much less "lumpy" than agency MBS. One thing worth mentioning here is that the US treasury will be borrowing $45bn a month effectively interest free. That's because the Fed passes interest income back to the Treasury (less its own expenses) via earnings distribution once a year. This certainly helps reduce pressure on Washington to cut spending quickly - the can will be kicked down the road once more.

Exit Strategy? What Exit Strategy? - Today the Federal Reserve issued this Policy Statement Regarding Purchases of Treasury Securities and Agency Mortgage-Backed Securities. On December 12, 2012, the Federal Open Market Committee (FOMC) directed the Open Market Trading Desk (the Desk) at the Federal Reserve Bank of New York to purchase longer-term Treasury securities after the maturity extension program is completed at the end of December 2012, initially at a pace of about $45 billion per month. The FOMC also directed the Desk to continue purchasing additional agency mortgage-backed securities (MBS) at a pace of about $40 billion per month. These actions should maintain downward pressure on longer-term interest rates, support mortgage markets, and help to make broader financial conditions more accommodative. The FOMC also directed the Desk to maintain its existing policy of reinvesting principal payments from the Federal Reserve’s holdings of agency debt and agency MBS in agency MBS, and, in January, to resume rolling over maturing Treasury securities into new issues at auction.Recall when the Fed pretended it was working on an exit strategy to reduce its balance sheet at the appropriate time? It was a lie then and it's an even bigger, more apparent lie now (which is why you no longer hear Bernanke mentioning it) . The simple fact of the matter is that every Fed asset purchase makes it more difficult to exit.

"Regime Change": The Critical Message In Today's FOMC Announcement - It will take the market some time to figure it out, but there were two main parts to the Fed's announcement: the actual breakdown of the $85 billion/month QE4EVA which were priced in as far back as the day QE3 was announced and were not a surprise at all; and the employment and inflation hard-targeting part, the so-called Evans Rule, which is, or at least should be, a shock to the market, only it hasn't quite realized it yet. Why shock? Because starting today, every incremental economic data point that is materially better, brings us closer to an explicit end of Fed intervention. Because at least before the Fed's calendar target was as soft as it gets; now the Fed will have no choice but to terminate its monetization once the unemployment rate plunges (be it entirely due to part-time jobs or 68 year old workers, as has been the case lately). It also means that as the economy continues along an "improving" glideslope, whether real, manufactured or doctored, the market will start pricing in its own "flow"-based demise. Because once the Fed's $85 billion/month in new Flows ends, it's game over.

Conditional Inflation Targeting in Effect - Nearly a year ago, Jeffry Frieden and I called for Conditional Inflation Targeting. Today, policy seems to have turned toward that direction. From today's statement from the FOMC:...the Committee decided to keep the target range for the federal funds rate at 0 to 1/4 percent and currently anticipates that this exceptionally low range for the federal funds rate will be appropriate at least as long as the unemployment rate remains above 6-1/2 percent, inflation between one and two years ahead is projected to be no more than a half percentage point above the Committee’s 2 percent longer-run goal, and longer-term inflation expectations continue to be well anchored. ... The Fed had earlier conditioned its asset purchases on the state of the economy, and continues to do so (although replacing Operation Twist with outright purchases). But today, the Fed provided explicit numerical reference points to condition the policy regarding the setting of the Fed funds rate. From our Foreign Policy article: [We need] inflation -- just enough to reduce the debt burden to more manageable levels, which probably means in the 4 to 6 percent range for several years. The Fed could accomplish this by adopting a flexible inflation target, one pegged to the rate of unemployment. Chicago Fed President Charles Evans has proposed something very similar, a policy that would keep the Fed funds rate near zero and supplemented with other quantitative measures as long as unemployment remained above 7 percent or inflation stayed below 3 percent.

Key Measures show low inflation in November - The Cleveland Fed released the median CPI and the trimmed-mean CPI this morning: According to the Federal Reserve Bank of Cleveland, the median Consumer Price Index rose 0.2% (2.3% annualized rate) in November. The 16% trimmed-mean Consumer Price Index increased 0.1% (1.6% annualized rate) during the month. The median CPI and 16% trimmed-mean CPI are measures of core inflation calculated by the Federal Reserve Bank of Cleveland based on data released in the Bureau of Labor Statistics' (BLS) monthly CPI report. Earlier today, the BLS reported that the seasonally adjusted CPI for all urban consumers fell 0.3% (-3.7% annualized rate) in November. The CPI less food and energy increased 0.1% (1.4% annualized rate) on a seasonally adjusted basis. Note: The Cleveland Fed has the median CPI details for November here.This graph shows the year-over-year change for these four key measures of inflation. On a year-over-year basis, the median CPI rose 2.2%, the trimmed-mean CPI rose 1.9%, the CPI rose 1.8%, and the CPI less food and energy rose 1.9%. Core PCE is for October and increased 1.7% year-over-year. On a monthly basis, median CPI was above the Fed's target at 2.3% annualized. However trimmed-mean CPI was at 1.6% annualized, and core CPI increased 1.4% annualized. Also core PCE for October increased 1.6% annualized. These measures suggest inflation is mostly below the Fed's target of 2% on a year-over-year basis. The Fed's focus will probably be on core PCE and core CPI, and both are at or below the Fed's target on year-over-year basis. Also, the FOMC statement this week indicated the Fed will tolerate an inflation outlook "between one and two years ahead" of 2 1/2 percent.

Elliott's Paul Singer Reveals The Thing That Scares Him Most - "They say this is not massive money printing, but first they are wrong; and second, monetary authorities in the United States did not see the crash coming and the unsoundness of the financial system. In fact, right up until the crash they were saying that nothing like what happened could ever happen... This monetary policy, $3 trillion of bond buying in the United States, $3 trillion in Europe and another $2.5 trillion to $3 trillion in Japan, is unprecedented. ... If and when people lose confidence in paper money because of repeated bouts of quantitative easing and zero-percent interest rates—it could happen suddenly and in a ferocious manner in the commodity markets, in gold, possibly in real estate—interest rates could go up at the long end by hundreds of basis points in a very short time. I’m quite concerned as a money manager that we have to manage money, not just for the boundaries of what’s in front of our faces—maybe we’ll have a little tax increase or not, the fiscal cliff, or the stock market might go up or down 10% or 15%—but for a basic shift. The thing that scares me most is significant inflation, which could destroy our society."

FOMC Projections - The FOMC projections, central tendency: The GDP growth projections were only marginally softer. Most notable was the decrease in the high end of the 2014 forecast. The unemployment rate projection fell in the near term, necessitated by the decline this year. But the 2014 projection was roughly the same. Inflation expectations were marginally softer, and notice that, within the central tendency, there are no projections above 2%. You need to move to the overall range to get an upper-bound projection of 2.2%, still within the Fed's now explicit margin of error of 50bp. Another point: There is no indication here of a fundamental change regarding the rate of potential output growth or the natural rate of unemployment in the longer-run. For now, the speed-limits remain the same. The expected date of first tightening is still reported:Most participants (13, instead of 12 like in September) expect the first tightening in 2015. Notice that this is consistent with unemployment falling below 6.5% that year. The Fed thinks that the unemployment rate will hit its threshold first.

Fed Downgrades Economic Outlook: With the most recent meeting of the Federal Reserve came the quarterly release of the Fed's economic projections we can update our tables and charts. When it comes to the economy the Fed has consistently overstated economic strength. Take a look at the chart and table. In January of 2011 the Fed was predicting GDP growth for 2011 at 3.7%. Actual real GDP (inflation adjusted) was 1.6% or a negative 56% difference. The estimate at that time for 2012 was almost 4% versus 1.8% currently. We have been stating repeatedly over the last 2 years that we are in for a low growth economy due to the debt deleveraging, deficits and continued fiscal and monetary policies that are retardants for economic prosperity. The simple fact is that when an economy requires nearly $5 of debt to provide $1 of economic growth the engine of prosperity is broken. As of the latest Fed meeting the forecast for 2013 and 2014 economic growth has been revised down as the realization of a slow-growth economy has been recognized. However, the current annualized trend of GDP suggests growth rates in the next two years that will roughly be half of the Fed's current estimates of 2.6% and 3.4%. As we have stated over the past year - a recession in 2013 remains a strong likelihood given the current annualized trend of economic growth since 2000. A recession followed by a rebound in 2014 would leave economic growth running at annual rate close to 1%-1.5% versus the current estimate of 3.35%. What is very important is the long run outlook of 2.6% economic growth. That rate of growth is not strong enough to achieve the "escape velocity" required to substantially improve the level of incomes and employment that were enjoyed in previous decades. With the Fed's new goal of targeting a specific unemployment level to monetary policy could potentially put the Fed into a box. Currently, the Fed sees 2014 unemployment falling to 6.75% and ultimately returning to a 5.5% "full employment" rate in the long run. The issue with this full employment prediction really becomes what the definition of reality is.

Lost Decade Watch - Paul Krugman - Along with its new policy pronouncement, the Fed released its economic projections (pdf). What struck me is that the Fed expects the unemployment rate to be well above its long-run level even in the fourth quarter of 2015, which is as far as its projections go. This means that the Fed is projecting elevated unemployment nine full years after the Great Recession started. And, of course, the Fed has been consistently over-optimistic. This is an awesome failure of policy — not solely at the Fed, of course. When I wax caustic about Very Serious People, bear this in mind. Faced with an economic crisis where textbook macroeconomics told us exactly how to respond, people of influence chose instead to obsess over budget deficits and generally punt on employment; and the result has been a huge economic and human disaster.

Bernanke: Fiscal Cliff Is Already Harming The Economy -The Chairman of the Federal Reserve Board spoke again today about the dangers of the fiscal cliff: The U.S. economy is already being hurt by the “fiscal cliff” standoff in Washington, Federal Reserve Chairman Ben Bernanke said Wednesday. But Bernanke said the Fed believes the crisis will be resolved without significant long-term damage. The steep tax increases and spending cuts can be avoided with a successful budget deal, Bernanke said during a news conference after the Fed’s final meeting of the year. The Fed’s latest forecasts for stronger economic growth next year and slightly lower unemployment assume that happens. Still, Bernanke said the uncertainty surrounding the resolution is already affecting consumer and business confidence. And it has led businesses to cut back on investment. “Clearly the fiscal cliff is having effects on the economy,” Bernanke said. Bernanke said the most helpful thing that Congress and the Obama administration can do is resolve the issue quickly.

Latest Article in the Atlantic - Ramesh Ponnuru and I have a new article in the Atlantic where we argue concerns about the fiscal cliff are exaggerated if the Fed continues to stabilize nominal spending. We note two experiences that support this notion: The Bank of England vividly demonstrated the power of central banks to offset fiscal policy at the dawn of the Thatcher era. In 1981 her government introduced a budget that would sharply reduce the deficit in the midst of a recession. Most economists opposed it on Keynesian grounds, with 364 of them signing a now-famous letter arguing there was "no basis in economic theory or supporting evidence" for it. Yet the Thatcher government implemented its plan and by late 1981 the economy was recovering. The Bank of England at the same time had begun a cycle of monetary policy easing, and the economists had underestimated its effects. Something similar happened in Canada in the mid-1990s. After running several decades of budget deficits that had led to a debt-to-GDP ratio of 70 percent in 1995, then-Finance Minister Paul Martin introduced a budget plan that began a half decade of reducing the federal budget, largely through cuts in spending. This fiscal tightening led to budget surpluses by the early 2000s. As in the British case, the Bank of Canada eased monetary policy over the same time, offsetting any fiscal drag. The economy performed nicely. The same outcome is possible for the U.S. fiscal cliff, but would require the Fed to adopt a NGDP level target. Reihan Salam provides a smart follow-up discussion here.

Is The US Already in Recession?, by Tim Duy: Via a recent media blitz, ECRI Co-Founder Lakshman Achuthan insists that the US is already in recession, apparently as of July. I would be very skeptical that this was in fact the case. I think the preponderance of evidence weighs in favor of ongoing expansion, disappointing as the pace of that expansion may be. Actually, Achuthan loses credibility quite quickly by claiming there is a strict definition of recession based upon peaks of production, income, jobs, and sales. In contrast, according to the NBER business cycle dating committee: The Committee does not have a fixed definition of economic activity. It examines and compares the behavior of various measures of broad activity: real GDP measured on the product and income sides, economy-wide employment, and real income. The Committee also may consider indicators that do not cover the entire economy, such as real sales and the Federal Reserve's index of industrial production (IP). The Committee's use of these indicators in conjunction with the broad measures recognizes the issue of double-counting of sectors included in both those indicators and the broad measures. Still, a well-defined peak or trough in real sales or IP might help to determine the overall peak or trough dates, particularly if the economy-wide indicators are in conflict or do not have well-defined peaks or troughs. Dating a recession, it would seem, is something of an art. And note that Achuthan appears to ignore the role of GDP and GDI in the determination of a recession. Taking a quick look at those two series:

Weisenthal interview with Goldman's Jan Hatzius - From Joe Weisenthal at Business Insider: Goldman's Top Economist Explains The World's Most Important Chart, And His Big Call For The US Economy - Hatzius is bullish on the U.S. economy starting in the second half of 2013, because finally he expects private releveraging to occur at a nice clip, and to not be counteracted by a fiscal drag. Says Hatzius: "If the business sector is basically trying to reduce its financial surplus at a more rapid pace than the government is trying to reduce its deficit then you’re getting a net positive impulse to spending which then translates into stronger, higher, more income, and ultimately feeds back into spending." He has a specific explanation and numbers in mind, to explain the private sector's inclination to reduce its savings, and spend more. "Since mid-2009, that surplus has gradually come down as businesses and households have gotten closer to where they need to be from a long-term balance sheet perspective. They’ve paid down debt, they’ve eliminated the excess supply of housing, and that’s basically allowed them to reduce the financial surpluses that they run. They’re still running large surpluses – still 5.5 to 7 percent of GDP, but they’re no longer as large. We expect those figures to come down as the balance sheet adjustment process makes further strides and that’s an underlying source of boost to the economy that’s happening on the one side."

The recovery: In search of "natural" velocity - The Economist - I HAD high hopes for the American economy after the Federal Reserve's policy shake-up in September. It looked to me like a shift in framework that signalled increased tolerance for inflation, one that could potentially allow for a shift up in the trajectory of the recovery. Revisions may vindicate this view, but Friday's jobs numbers, for the month of November, show an expansion stuck on course. The economy added 146,000 jobs last month. The Bureau of Labour Statistics helpfully noted, "Since the beginning of this year, employment growth has averaged 151,000 per month, about the same as the average monthly job gain of 153,000 in 2011." Since late 2010, growth in employment and nominal output has been strikingly, impressively, and disappointingly stable. Will the economy ever manage to do any better? Goldman Sachs economist Jan Hatzius reckons there's a chance it will turn a corner late next year, provided that Congress doesn't drive the country back into recession. In an interview with Business Insider's Joe Weisenthal, he describes his sectoral balances approach to business cycles: [E]very dollar of government deficits has to be offset with private sector surpluses purely from an accounting standpoint, because one sector’s income is another sector’s spending, so it all has to add up to zero. That’s the starting point. It’s a truism, basically. Where it goes from being a truism and an accounting identity to an economic relationship is once you recognize that cyclical impulses to the economy depend on desired changes in these sector's financial balances...

Goldman Q4 GDP Forecast At 1.0% Following Trade Data - So just what is below "stall-speed" growth in the New Normal? And with 48 out of 49 economists now predicting what we said would happen back in September, namely that the Fed will go all in with QEternity+1 and take its balance sheet to $4 trillion (and then $5 trillion in 2014) yet firmly holding their 2013 year end GDP forecast at 2.0%, lower than Q3 2011's 2.7%, does it mean that even $1 trillion in additional flow and stock from the Fed can barely keep the economy above the Old Normal stall speed definition? What exactly would happen if the Fed were to not monetize hundreds of billions in debt? We shiver to even think.

The Big Four Economic Indicators: Industrial Product and Retail Sales Brighten the Picture - Official recession calls are the responsibility of the NBER Business Cycle Dating Committee, which is understandably vague about the specific indicators on which they base their decisions. This committee statement is about as close as they get to identifying their method. There is, however, a general belief that there are four big indicators that the committee weighs heavily in their cycle identification process. They are:

- Industrial Production

- Real Personal Income

(excluding transfer payments)- Employment

- Real Retail Sales

The weight of these four in the decision process is sufficient rationale for the St. Louis FRED repository to feature a chart four-pack of these indicators along with the statement that "the charts plot four main economic indicators tracked by the NBER dating committee." Here are the four as identified in the Federal Reserve Economic Data repository. See the data specifics in the linked PDF file with details on the calculation of two of the indicators. This morning I've added two more of the Big Four for November: Industrial Production from the Federal Reserve, the purple line in the chart below and Real Retail Sales, the green line.

Economic Outlook: Where are we? - Once again we are nearing a political event horizon that could significantly impact the economy - and we can't see beyond the horizon. My baseline assumption is an agreement will be reached, probably during the first few weeks of January, and the agreement will mean Federal fiscal drag next year at about the level of the CBO's alternative fiscal scenario. This would suggest modest GDP and employment growth next year, although probably better than in 2012. Note: There is no clear drop dead date for the "fiscal cliff". Nothing horrible happens on January 1st, but the longer it takes to reach an agreement next year, the larger the negative impact on the economy. With that assumption, there are two key drivers for additional growth next year. The first is residential investment (construction employment lags investment with a lag, so construction employment should pick up in 2013), and the second is the end of the state and local drag. I've discussed both of these before - see: Two Reasons to expect Economic Growth to Increase - but I think this is worth repeating. This graph shows the contribution to percent change in GDP for residential investment and state and local governments since 2005.

The Slow Growth in Investment - One of the puzzles of the post-crisis period is why investment has been so slow. Some would want to resort to stories of uncertainty. Is there something to this idea? Figure 1 depicts the gross investment to net capital stock. Goldman Sachs (David Mericle, “The Drivers of Capital Spending, December 5, 2012, not online) notes: Our econometric analysis [of data over the 1991-2012 period] leads us to draw the following conclusions about each class of model: First, the accelerator model generally fits well. ... The model also substantially overpredicts investment during the last couple of years because it implies that the lagged effect of the sharpest downturn phase of the recession should have passed by now.Second, Tobin’s Q model ... is considerably noisier and overpredicts investment during the recovery from the Great Recession much more severely than the other models. Finally, combining the accelerator model with a measure of credit availability captures investment dynamics reasonably well. ... Our analysis suggests that an improved version of the standard accelerator model that accounts for the availability of credit goes a long way toward explaining recent investment patterns. GS provides this graph:

Delusions of Wisdom - Paul Krugman - Both Jonathan Chait and Charles Pierce have a field day with a Politico piece titled, without a hint of irony, Crafting a boom economy. In said piece they talk to various Very Serious People, and divine the insider consensus on What Must Be Done — which mainly seems to involve, naturally, cutting Social Security and Medicare while reducing corporate tax rates.What I find remarkable about this piece is that after everything that has happened these past five years or so, Jim VandeHei and Mike Allen still take it for granted that these people actually know what they’re talking about; the whole premise of the article is that the insiders really do have the key, not just to good policy, but to achieving a dramatic rise in the growth rate.Now, they don’t tell us everyone they talked to; but I think we can safely assume that, with few exceptions, the insiders in question:

- Believed that financial deregulation was a great idea, because bankers had really learned to manage risk

- Did not believe that there was a housing bubble

- Insisted that budget deficits, even in a depressed economy, would send interest rates soaring any day now

- Insisted that austerity measures would promote recovery, not hurt it, because of the confidence fairy

And on and on.

The Trade-Off Between Economic Growth and Deficit Reduction -- Laura Tyson - The economy is continuing to recover from its deepest recession since the Great Depression, but the pace of recovery is frustratingly slow. The question is why, and the answer has profound implications for fiscal policy and for the debate over deficit reduction and economic growth that has transfixed Washington. Since 2010, annual growth of gross domestic product has averaged about 2.1 percent. This is less than half the average pace of recoveries from previous recessions in the United States since the end of World War II, according to a recent study by the Congressional Budget Office. Both potential G.D.P., a measure of the economy’s underlying capacity, and actual G.D.P. have grown unusually slowly compared with previous recovery periods. Slow G.D.P. growth has meant slow growth in employment. Payroll employment has been expanding at a rate of about 150,000 jobs per month during the last two years, only slightly above the growth of the labor force. Employment growth has been largely consistent with overall G.D.P. growth and with the “jobless” pattern of the 1990-91 and 2001 recoveries. In both this recovery and the previous two, the rebound in employment growth has been weaker and later than the rebound in G.D.P. growth. But G.D.P. growth in the current, jobless recovery has been slower. Another salient difference is that the loss of jobs in the most recent recession was more than twice as large as in previous recessions, so a slow recovery has also meant a much higher unemployment rate.

An Alternative Meme for Money, Part 5: A Spending Meme --- L. Randall Wray - Let me repeat and clarify my purpose in this series. I am attempting to initiate a discussion among progressives on how to frame discussions about money and related issues. My perspective is MMT. To be sure, on one level MMT is a description. It provides a correct description of the operation of a sovereign currency system. Some commentators have objected to my progressive framing; they assert that one can accept MMT without the progressive bias. Sure they can. One can understand how money “works” but prefer NOT to use money in the public interest. Science is necessarily a progressive endeavor. Or, as Stephen Colbert puts it, reality has a well-known liberal bias. Of course it does. From global warming to the problems of unemployment, the liberal perspective is based in reality, while the conservative view necessarily denies science.But one can accept the MMT description and still pursue a reactionary policy agenda. The conservative is willing to take the “technology” of a modern money system to use it against the public purpose. Technology can be used in highly anti-progressive ways. Tear gas to put down civil rights demonstrators. Nuclear weapons to vaporize humans. Concentration camps and gas chambers. Science, however, is progressive.