A Look Inside the Fed’s Balance Sheet (interactive graphic)The Federal Reserve‘s balance sheet has ballooned in the past year, and even if they start cutting back bond purchases, it’s likely to continue growing. The assets the Fed holds have jumped by over $800 billion, or about 30%, to more than $3.6 trillion since it first announced its latest bond-buying program last September. The central bank has been adding $85 billion a month in Treasurys and mortgage-backed securities since early this year. Many Fed watchers expect the Fed to cut back its purchases at this week’s meeting, but even so it will continue to add to its balance sheet — just at a slower pace. The balance sheet is up from less than $1 trillion prior to the recession. During the downturn the Fed expanded its balance sheet through several programs aimed at keeping markets functioning. As markets stabilized the Fed shifted out of emergency programs and into purchases of U.S. Treasurys, MBS and agency debt securities to drive down interest rates and encourage more borrowing and growth in three separate rounds of what is known as quantitative easing. Earlier in the recovery, MBS and agency debt holdings, which were part of the first round of quantitative easing, had steadily declined as loans were paid off or matured. But with the latest round of bond purchases, the Fed ramped up its securities purchases. The Fed holds more than $1.2 trillion in MBS and agency debt, but owns more Treasurys — over $2 trillion.

FRB: H.4.1 Release-- Factors Affecting Reserve Balances -- Thursday, September 19, 2013: Factors Affecting Reserve Balances of Depository Institutions and Condition Statement of Federal Reserve Banks

Goldman and Merrill economists on "Tapering" - From economists Jan Hatzius and Sven Jari Stehn of Goldman Sachs:

• Fed officials will review three key pieces of information next week: (1) economic activity and labor market indicators that have been modestly encouraging, (2) a stabilization in core inflation at levels well below the 2% target, and (3) a tightening of financial conditions since the last meeting, mainly because of higher long-term interest rates.From the Merrill Lynch economic team: We expect the Fed to delay tapering at its September 17-18 meeting, but a “token taper” of $10 bn is also quite possible. More important, we expect a market-friendly message from the Fed, underscoring a slow, data-dependent exit.

• We believe the news is consistent with a shift in the mix of monetary policy instruments away from asset purchases and toward forward guidance. ...

• Regarding the asset purchase program, we expect a tapering of $10bn, all in Treasuries, as well as confirmation from Chairman Bernanke that the committee still expects to end QE3 in mid-2014.

Slackers at the Fed - Paul Krugman -To taper or not to taper, that is the question. Except it’s actually two questions:

- 1. Are we getting close enough to “full employment” that it’s time to let up on the gas? How much slack is there in the economy, really?

- 2. To the extent that the economy still needs a boost, are purchases of long-term Treasuries the way to do this?

The answer to question 2 is probably no — but that’s an argument for replacing the current policy with something better, like purchases of MBS and/or stronger forward guidance, not for a taper all by itself, which serves as a sort of forward anti-guidance: it signals, whether the Fed intends this or not, a general shift toward hawkishness. But what about question 1? The measured unemployment rate is down a lot — in fact, at 7.3 percent it’s almost exactly the same as it was in November 1982 1984, when Ronald Reagan won big on claims of restored prosperity. But most of the fall in unemployment reflects lower labor force participation rather than job growth. Even if we focus on prime-age workers, so as to net out demographic effects, the employment story is highly unimpressive:

Give Jobs a Chance, by Paul Krugman - Now the Fed is talking about slowing the pace of these purchases, bringing them to a complete halt by sometime next year. Why? One answer is the belief that these purchases — especially purchases of government debt — are, in the end, not very effective. There’s a fair bit of evidence in support of that belief, and for the view that the most effective thing the Fed can do is signal that it plans to keep short-term rates, which it really does control, low for a very long time. Unfortunately, financial markets have clearly decided that the taper signals a general turn away from boosting the economy: expectations of future short-term rates have risen sharply since taper talk began, and so have crucial long-term rates, notably mortgage rates. In effect, by talking about tapering, the Fed has already tightened monetary policy quite a lot. But is that such a bad thing? That’s where the second argument comes in: the suggestions that there really isn’t that much slack in the U.S. economy, that we aren’t that far from full employment. After all, the unemployment rate, which peaked at 10 percent in late 2009, is now down to 7.3 percent, and there are economists who believe that the U.S. economy might begin to “overheat,” to show signs of accelerating inflation, at an unemployment rate as high as 6.5 percent. Time for the Fed to take its foot off the gas pedal? I’d say no, for a couple of reasons.

Fed Will Not Reduce Stimulus, Waiting for “More Evidence” of Recovery - In one of the most anticipated announcements in months, the Federal Reserve’s Federal Open Market Committee declared that it would maintain it’s policy of buying $85 billion in government debt and mortgage backed securities per month, despite expectations that it would begin to taper these purchases in response to an improving economy. According to a statement from the Fed, “the Committee decided to await more evidence that progress will be sustained before adjusting the pace of its purchases. Accordingly, the Committee decided to continue purchasing additional agency mortgage-backed securities at a pace of $40 billion per month and longer-term Treasury securities at a pace of $45 billion per month.”

Fed, in Surprise Move, Postpones Retreat From Stimulus Campaign - NYTimes.com: — The Federal Reserve postponed any retreat from its long-running stimulus campaign Wednesday, saying that it would continue to buy $85 billion a month in bonds to encourage job creation and economic growth. As Congressional Republicans and the White House hurtle toward another showdown over federal spending, the Fed said it was concerned that fiscal policy once again “is restraining economic growth,” threatening to undermine what the Fed had described just months ago as a recovery gaining strength. The Fed’s decision also may reflect the consequences of yet another premature retreat from its own policies. Mortgage rates have climbed and other financial conditions have tightened since the Fed signaled in June that it intended to reduce its asset purchases by the end of the year, the Fed noted Wednesday. “The tightening of financial conditions observed in recent months, if sustained, could slow the pace of improvement in the economy and the labor market,” it said in a statement released after a regular two-day meeting of its policy-making committee. The decision, an apparent victory for the Fed’s chairman, Ben S. Bernanke, and his allies who have argued for the benefits of asset purchases, was supported by all but one member of the Federal Open Market Committee. Esther George, president of the Federal Reserve Bank of Kansas City, dissented as she has at each previous meeting this year, citing concerns about inflation and financial stability.

Fed Watch: No Taper - Yet - The FOMC pulled yet another rabbit out of the hat by holding off on the expected taper, slamming down on analysts (including yours truly) who thought the Fed would pull the trigger today. Two significant factors that held the FOMC in check were fiscal policy and higher interest rates. From the statement:Household spending and business fixed investment advanced, and the housing sector has been strengthening, but mortgage rates have risen further and fiscal policy is restraining economic growth....Taking into account the extent of federal fiscal retrenchment, the Committee sees the improvement in economic activity and labor market conditions since it began its asset purchase program a year ago as consistent with growing underlying strength in the broader economy. The Committee sees the downside risks to the outlook for the economy and the labor market as having diminished, on net, since last fall, but the tightening of financial conditions observed in recent months, if sustained, could slow the pace of improvement in the economy and labor market.Now, why did financial conditions tighten? Oh yes, I recall - because just talking about tapering is the same as tightening. Remember, unless yields head much lower (they are down around 10bp as I write), much of the damage is already done is already done.Holding off on tapering also achieves two other objectives. The first is to make clear that policy is data dependent:The second - assuming we now have an Octaber to look forward to - is that the Fed can prove it can change policy in meetings not followed by a press conference.

Fed Statement Following September Meeting - The following is the full text of the statement following the Fed's September meeting.

Parsing the Fed: How the Statement Changed - The Federal Reserve releases a statement at the conclusion of each of its policy-setting meetings, outlining the central bank’s economic outlook and the actions it plans to take. Much of the statement remains the same from meeting to meeting. Fed watchers closely parse changes between statements to see how the Fed’s views are evolving. The following tool compares the latest statement with its immediate predecessor and highlights where policy makers have updated their language. This is the September statement compared with July.

Four Takeaways on the Fed’s Economic and Rate Projections - The big headline in Wednesday’s Federal Reserve meeting is its decision not to pull back on an $85 billion monthly bond buying program. But important details of the Fed’s thinking also emerged in its economic and interest-rate projections: Soft growth, low inflation, modest improvement in unemployment and a very long period before short-term interest start rising again. Here is a closer look at how the Fed sees the economy and rates:

- –Ten of 17 Fed officials see short-term interest rates at or below 2% by the fourth quarter of 2016. Fourteen of 17 Fed officials don’t see the Fed starting to raise interest rates until 2015 or 2016. The message: The Fed is going to take its time before it starts raising interest rates, and once it does start raising them it intends to move slowly.

- –Once again the Fed is revising down its economic growth forecasts. The Fed now sees growth between 2% and 2.3% this year, down from 2.3% to 2.6%. It also nudged down its 2014 growth forecast to between 2.9% and 3.1%, from 3.0% to 3.5%.

- –Even though growth keeps disappointing, the Fed sees unemployment on track to keep falling to between 6.4% and 6.8% in 2014, between 5.9% and 6.2% in 2015 and between 5.4% and 5.9% in 2016. There are two important points related to these projections: 1) Fed officials are getting increasingly used to the idea that the economy doesn’t need to generate as much output as they have expected to reduce unemployment. . 2) Their 6.5% unemployment threshold looks like a very soft target. The Fed has said it won’t even start talking about raising short-term interest rates until the unemployment rate hits 6.5%.

- –The Fed sees inflation firming. The forecast for this year is between 1.2% and 1.3%, more than the forecast in June of 0.8% to 1.2%. Still, they don’t see it getting back to 2% next year. In other words, they’re little less worried about inflation getting too low, but they do see it remaining below their 2% objective. That’s likely to be floated as another reason to be patient about pulling back on bond buying or raising short-term rates.

Fed Taper End Done In By Deflation and Labor Participation Rate - The Federal Open Market Committee is not going to stop quantitative easing just yet. This is no surprise considering the weak economic conditions and as we pointed out, an inflation rate below expectations. The risk of deflation is real.The Committee decided to continue purchasing additional agency mortgage-backed securities at a pace of $40 billion per month and longer-term Treasury securities at a pace of $45 billion per month.The tightening of financial conditions observed in recent months, if sustained, could slow the pace of improvement in the economy and labor market. The Committee recognizes that inflation persistently below its 2 percent objective could pose risks to economic performance, but it anticipates that inflation will move back toward its objective over the medium term. Don't bank on the Fed stopping quantitative easing by December either as we pointed out. They are continuing to assess market conditions and are basing the decision on sustainable increases in labor market conditions and wanting to see the inflation hit the 2.0% annual target. Asset purchases are not on a preset course, and the Committee's decisions about their pace will remain contingent on the Committee's economic outlook as well as its assessment of the likely efficacy and costs of such purchases. The FOMC also released their new economic projections and notice how the PCE index is below the Federal Reserve 2.0% annual target rate. In other words, they expect inflation to be too low for the short term.

Digging a deeper hole - Looks like our assessment has been wrong. The current FOMC, who has chosen to stay the course on securities purchases, is even more dovish than many had predicted. The Fed is following a dangerous path. Nevertheless the markets love it. We've seen the damage even a hint of exiting this program did to emerging markets. The deeper the US central bank gets into this hole, the more difficult the eventual exit will become.

FOMC Projections and Press Conference - The key sentence in the announcement was: "the Committee decided to await more evidence that progress will be sustained before adjusting the pace of its purchases". With the downgrade to GDP and inflation (for 2014), it makes sense that the Fed decided to wait for more data. As far as the "Appropriate timing of policy firming", the participants moved out a little with two participants now seeing the first increase in 2016. Bernanke press conference here or watch below. On the projections, GDP was revised down for 2013 and 2014, the unemployment rate was revised down slightly, and inflation was revised down for 2014.1 Projections of change in real GDP and in inflation are from the fourth quarter of the previous year to the fourth quarter of the year indicated. The unemployment rate was at 7.3% in August.

Taper tiger - SHORTLY after the Federal Reserve hinted in May that it might start to ease up on its monetary stimulus, rich-country bond yields shot up; emerging-market currencies and stockmarkets cratered. Was it all for nothing? On September 18th, at the end of a closely-watched meeting, the Federal Open Market Committee, the Fed’s policy-setting body, chose not to “taper”. Instead, it said it would keep buying $85 billion a month of Treasury and mortgage bonds with newly-created money (the policy of “quantitative easing”, or QE). So what has now held it back? First, the pace of job growth has recently flagged, and the drop in unemployment has been flattered by the absence of people looking for work. The labour-market participation rate sank to 63.2% in August, a 35-year low. Second, fiscal policy continues to work at cross-purposes to monetary policy. Higher taxes and spending cuts have subtracted at least a full percentage point from growth this year. The prospect that spending caps may be lifted when the new fiscal year begins on October 1st has melted away. With Republicans in Congress and Barack Obama unable to agree on how to fund the government or raise the Treasury’s statutory debt ceiling, the risk of a government shutdown loomed large in the minds of Fed officials. But the third and most important restraint on the Fed was the unexpected effect on financial markets of a prospective change in monetary stance. The central bank had always emphasised that tapering did not mean tightening. Provided asset purchases remained above zero, the Fed’s balance-sheet would keep growing and monetary policy would still be loosening.

Fed Watch: Further Post-Mortem - Federal Reserve Chairman Ben Bernanke took many of us to the woodshed today with the unexpected decision to delay tapering until a later date. I am still processing the outcome of the FOMC meeting, and I suspect I will still be processing it a week from now. At the moment, I am wary of overreacting to this meeting, fearing the possibility of being slapped around again at the next meeting. So for the moment I am going to put aside the explanation that the Fed wanted "to send a message" to markets about who dictates monetary policy. Same to for the idea the Fed' s reaction curve has shift measurably. Instead, I think it best to keep it simple - the Fed decided they didn't have enough evidence to expect the current momentum, such as it is, would be sustained and consequently decided to hold pat. It depends, I think, in how you interpret this section of the FOMC statement: Taking into account the extent of federal fiscal retrenchment, the Committee sees the improvement in economic activity and labor market conditions since it began its asset purchase program a year ago as consistent with growing underlying strength in the broader economy. However, the Committee decided to await more evidence that progress will be sustained before adjusting the pace of its purchases. I think this means that, in general, the data was broadly consistent with the Fed's expectations. That is, we weren't reading the data wrong. They just decided that they could wait until longer before initiating the taper. And why might they want to do so? Two reasons: Household spending and business fixed investment advanced, and the housing sector has been strengthening, but mortgage rates have risen further and fiscal policy is restraining economic growth.

Fed’s QE surprise shows problems of forward guidance - The sense of surprise at the US Federal Reserve on Wednesday is a reminder that we are still in the PalmPilot era of forward guidance about monetary policy: the technology exists, but it is clunky, temperamental and some way off the iPad level of usability that everybody expects.Markets reacted with great enthusiasm and some bewilderment after the Fed chose not to “taper” its asset purchases from $85bn a month. It was less the decision that was a surprise – that was perfectly justifiable, given the wobbly state of the economy – but how the chairman Ben Bernanke appeared to back away from his guidance in June. The great innovation of the Fed’s third round of quantitative easing, which began a year ago, was to say it would continue until there was a “substantial improvement in the labour market”. In June, Mr Bernanke tried to clarify what substantial improvement meant, and thus provide better guidance. He said that if the jobs market kept getting better, growth started to pick up over the next few quarters and inflation began to return to target, it would make sense to start reducing purchases later this year and stop them by the middle of 2014 with an unemployment rate of around 7 per cent. But the guidance has turned out to be too specific, in a way that Mr Bernanke and the rate-setting Federal Open Market Committee clearly found intolerable. It made no allowance for the big rise in long-term interest rates triggered by the idea of tapering; it did not account for the possibility of an imminent fiscal shock from Congress; and it leaned too heavily on an unemployment rate that has fallen faster than the Fed expected, given the health of the economy.

Fed’s George: Decision Not to Taper Raises Risks, Clouds Credibility - The Federal Reserve‘s decision this week to keep up its bond purchases risks a spike in interest rates and clouds the credibility that is needed for future policy to be effective, a Fed official warned Friday. As the lone dissenter of the Fed’s policy decision Wednesday, Kansas City Fed President Esther George explained she is worried the Fed’s ongoing efforts to stimulate the economy fail to take into account the economic progress already made and raise future costs. Ms. George has now cast a dissenting vote at each of the Fed’s six policy meetings this year. “Waiting for more evidence at this point, in the face of economic growth, unnecessarily discounts the progress we’ve seen, unnecessarily discounts the costs of this tool,” the central banker said in a speech before the Manhattan Institute for Policy Research in New York. Such costs include potentially sharp market disruptions when the Fed does pull the tapering trigger and excessive inflation because the Fed waited too long to pull back. And those costs may not be worthwhile when the economy is seeing little added benefits from monetary stimulus. “A trillion dollars later, we have weaker GDP, we have lower inflation, we have higher interest rates. Unemployment continues to come down, but a lot of troubling things are under the cover there,” she said. “Our more powerful tool is short-term interest rates.” Furthermore, since Wednesday’s policy decision, Ms. George said the surprise reaction it caused across financial markets raises another challenge: maintaining market participants’ trust. “By delaying, I think the committee will have to think about challenges about credibility and predictability,” Ms. George said.

Goldman Pushes Back Forecast On First Taper To December, First Rate Hike To 2016: FOMC Q&A -- For what it's worth (not much lately), here is Goldman's Jan Hatzius with a Q&A on the Fed's announcement, which now sees the first tapering to start in December, QE to conclude (three months after their prior forecast), and expects the first rate hike to take place in 2016: 8 years after the start of the financial crisis.

- We now expect the QE tapering process to start at the December 2013 FOMC meeting and to conclude in September 2014, three months later than before. Our baseline is that the first step will consist of a $10bn cut in Treasury purchases. These steps remain data dependent in all respects--timing, size, and composition.

- A change in the explicit forward guidance for the federal funds rate is also likely, probably at the same time as the first tapering step. Our baseline is an indication that the 6.5% unemployment threshold is conditional on a forecast of a near-term return of inflation to 2%, and that a lower threshold would apply otherwise. But there are also other options, such as an outright inflation floor or an outright reduction in the unemployment threshold.

- Our forecast for the first hike in the funds rate remains early 2016. The reasons are the large output gap, persistent below-target inflation, and some weight on "optimal control" considerations. The market and most Fed officials see an earlier hike, although the number of FOMC participants projecting the first hike in 2016 rose from 1 to 2 and the "dots"--the projections for the appropriate funds rate at the end of 2016 by FOMC participants--came in below expectations.

Fed Gives Breathing Room to Asian Economies - The U.S. Federal Reserve’s surprise decision not to pull back on a $85 billion monthly bond-buying program provides some respite to Asian economies that have been under pressure due to concerns about an end to U.S. easy-money policies. Asian countries with large current account deficits – notably India and Indonesia – could see the most short-term benefit to their currencies, bonds and stocks from the Fed’s decision to leave its extraordinary monetary policies in place. Both these nations have faced massive selling of their currencies and have had to offer investors much higher rates to borrow money since the Fed intimated in late May it would soon begin winding down its bond buying. That’s because investors, anticipating higher U.S. rates, began to reduce their exposure to more-risky emerging markets. India and Indonesia – along with Brazil and Turkey – were especially vulnerable because they import more than they export, making them reliant on foreign capital inflows to fund the deficit. The Fed’s latest actions “may foster expectations that capital outflows from EM can stop or even reverse,” Barclays said. “This should be particularly supportive for the currencies and rates markets of countries with higher current account deficits.” Both India and Indonesia have tightened monetary policy in recent weeks in an attempt to stop the outflows. Investors may now start to think more monetary tightening – which risked further squeezing economic growth – may not be necessary. “Some of the priced-in expectations of aggressive monetary tightening may be unwound,” Barclays said.

Forget 7% Unemployment as Fed Guidepost -- So about that 7% unemployment rate Federal Reserve Chairman Ben Bernanke cited back in June? Don’t pay so much attention to that. Earlier this year he said that’s where the Fed expected the unemployment rate to be when it ended its signature bond-buying program. But it was a different message that Mr. Bernanke delivered at his press conference Wednesday after he and other Fed officials decided not to start pulling back on the $85 billion-per-month bond-buying program. Mr. Bernanke made no mention of the 7% number until asked about it by a reporter, and then he downplayed the importance of the figure. “There is not any magic number that we are shooting for. We’re looking for overall improvement in the labor market,” he said. When he offered 7% in June, it was meant to be an “indicative number” to give the public a sense of where unemployment “might” be when the bond-buying program ends, he said. He also said that the unemployment rate “is not necessarily a great measure in all circumstances of the state of the labor market overall,” referring to the fact the jobless rate has fallen in part because people are dropping out of the labor force. In June, Mr. Bernanke said the bond-buying program would likely end by mid-2014, at which point the Fed expected unemployment would be about 7%. Now it looks like the jobless rate could be quite a bit lower than that by the middle of next year. Fed officials, in their updated economic projections also released Wednesday, expect the jobless rate to be between 7.1% and 7.3% by the end of this year, and to fall to between 6.4% and 6.8% by the end of 2014.

Shorter Federal Reserve: The Economy Breathes Sort of OK if We Keep it On Life Support -- That’s what the decision to continue Quantitative Easing 3 (QE3), the purchase of 85 billion dollars of treasuries and mortgage backed securities a month, is an admission of. It is also a way of not causing Brazil and India’s currencies to crash out, which just the suggestion of a reduction of QE3 was causing. It is worth reiterating that the purpose of Quantitative Easing is to make the rich richer, and that it has done. US stock markets increased 150% from their lows, one of those bull markets traders dream of. However the employment situation has not significantly improved.Median household net worth is down, median income is down, but the rich are richer. This is not to say that QE does no good for the regular economy, it does, but it does far less good than could be done with eighty five billion dollars a month. A program to, say, retrofit every single federal building for active and passive solar would employ more people and have more of a ripple effect. Eighty five billion dollars a month (970 billion a year) is a LOT of money. Nonetheless, given its refusal to break up the large banks; the President and Congress’s refusal to actually tax rich people (thus necessitating the Fed buying treasury bonds); and a refusal to allow the housing market to settle to its actual value while supporting underwater homeowners, the Fed is in a bind. If you refuse to do anything that is primarily intended to help ordinary people, refuse to engage in sufficient measures to break the oil supply bottleneck (and no, Fracking isn’t cutting it); refuse to tax rich people (who have the money); and refuse to engage in any sort of industrial policy while funneling money to industries like banking, insurance, pharma and the military-industrial complex which are ultimately parasitical, why then, it can certainly seem like you have no choice but to continue throwing money at banks and rich people, and hoping some of it gets to the real economy.

Less Tapering Becomes Tightening Credit No Matter What Fed Says - Federal Reserve Chairman Ben S. Bernanke sent bond yields a percentage point higher just by talking about adding stimulus at a slower pace. The rout serves as a warning to monetary policy makers that their exit from record accommodation won’t be easy to control. The jump in yields has pushed up the cost of mortgages for millions of Americans, curbed demand for homes and prompted thousands of job cuts at Bank of America Corp. and Wells Fargo & Co., all at a time when the Fed’s policies are aimed at creating jobs and supporting housing. Bernanke has stressed that any reduction in the amount of money the central bank pumps into the financial system each month doesn’t mean policy is getting any more restrictive. That message hasn’t been heeded by bond investors, demonstrating how hard it will be for the Fed to control long-term interest rates as it moves toward tightening, “Getting out of ultra-low interest-rate policy was never going to be easy, and this is a perfect illustration of why,” “It is possible that this will make it even harder because the market will be even more primed to view inflection points as messy and destructive, and therefore a reason to sell early.”

‘It seems that the Fed now understands that tapering is tightening’ - You’ve seen those who were (ahem) surprised by the US central bank’s decision not to start tapering this month… now read the words of one who got it right: BNP Paribas’ Julia Coronado, the bank’s chief North America economist and ex-forecaster at the Fed.And interestingly, BNP think even December is in doubt:What hasn’t been clear even to seasoned Fed watchers like ourselves is how the Fed is weighing progress (or the lack thereof) on their dual mandates for employment and inflation against worries about the costs and benefits of their unconventional balance sheet policies. Wednesday’s communication made it clear that progress on dual mandates is still dominant and the Fed believes there is still some juice left in the QE orange…As we had expected, the tapering guidance was left far more open-ended and data dependent than in June. Chairman Bernanke indicated the Fed could reduce asset purchases “possibly later this year”. When asked about the 7.0% unemployment rate that he indicated in June was expected to prevail when QE came to an end, he said there is no “magic number we are shooting for. We are looking for overall improvement in the labor market”.This raises questions about our December taper call. We don’t expect as buoyant an H2 as the FOMC; our forecast is for GDP growth of 1.8% q4/q4 in 2013, whereas the Committee’s central tendency forecast is 2.15%. Chairman Bernanke suggested that tapering required three conditions: “growth that’s picking up over time, continuing gains in the labor market, and inflation moving back towards our objective”. We don’t expect these conditions to be well established until H1 2014.

The Fed Has Investors Overjoyed, And It's For All the Wrong Reasons - Mohamed A. El-Erian - If anything, the Fed under Ben Bernanke has made a point of enhancing “transparency.” Mr. Bernanke is the most communicative chairman in Fed history. He and his colleagues are releasing more data and projections than ever before. And Janet Yellen, the Fed’s vice governor and Mr. Bernanke’s likely successor, has led a comprehensive transparency initiative. Yet the Fed has ended up surprising in major ways over the last few months, leading to wild gyrations in markets. The Dow collapsed by 5% between May 21st and June 24th, before surging by 8% to a new record close on Wednesday. Commodity and bond markets have also been quite volatile, with the benchmark 10-year Treasury unusually trading in an almost 50 basis point range. Changes in underlying economic fundamentals do not warrant such volatility. While the economy continues to heal, it is has remained stuck in a multiyear, low-level growth equilibrium that frustrates job creation and worsens income distribution. It could be that the Fed is really worried about the upcoming congressional battles over funding the government and lifting the debt ceiling. As illustrated by the debacle of the summer of 2011, a slippage could undermine economic performance. And we should never underestimate the appetite of our polarized Congress for self-manufactured challenges. Having said this, the Fed usually prefers to be reactive rather than proactive in such situations. It is also hard to argue that the Fed has made a major discovery about the longer-term impact of what is after all a highly experimental policy approach. If anything, our central bankers (and, I would argue, everybody else) are essentially in the dark when it comes to the specific evolution over time of what Mr. Bernanke labeled back in 2010 the “benefits, costs and risks” of prolonged reliance on unconventional monetary policy.

Federal Reserve Program Is Socialism For The Rich - If you have followed any economic news at all you will have heard the term quantitative easing, or QE, which is technocratic shorthand for the Federal Reserve shoveling funds into Wall Street banks to produce a phenomenon known as the “wealth effect.” The wealth effect relies principally on trickery. The hope being that people will see higher asset prices, and in a self-fulfilling prophecy, invest and produce more thinking the economy is better – which will make the economy better. The reality is the Federal Reserve’s QE program has made the rich a lot richer and done little to nothing for the poor and middle class – besides screwing people living on fixed incomes. In fact, it has now devolved into a redistribution scheme to take money from poor and middle class workers and give it to the rich – or so says billionaire investor Stanley Druckenmiller. In an interview with CNBC related to Fed Chairman Bernanke’s massive cave to Wall Street earlier this week where he refused to stop QE, Druckenmiller revealed what every financially literate American knows – that QE is socialism for the rich.. First of all, as a practitioner of markets I love this stuff. OK, this is fantastic. It’s fantastic for every rich person. This is the biggest redistribution of wealth from the middle class and the poor to the rich ever. Who owns assets? The rich. The billionaires. You think Warren Buffett hates this stuff? You think I hate this stuff? I had a very good day yesterday. OK?

Fed’s Bullard: Small Taper Possible in October - St. Louis Fed President James Bullard said Friday that “a small taper is possible in October” and the decision not to move at the latest meeting was “borderline.” “This was a close decision here in September,” he said on Bloomberg TV. “It’s possible you get some data that can change the complexion for the outlook and make the committee comfortable with a small taper in October.” There’s no press conference scheduled for after the October meeting, Mr. Bullard said, but they could put one on. Mr. Bullard is one of many speakers today. He will have further comments today, and in addition there will be speeches by Kansas City Fed leader Esther George, a persistent opponent of Fed bond buying; Minneapolis Fed boss Naryana Kocherlakota, who supports aggressively easy money policy; and Fed Governor Daniel Tarullo, who will speak on regulatory issues. Mr. Bullard also said he was concerned that in its dual mandate the Fed’s focus has shifted too much toward unemployment levels and away from inflation. Mr. Bullard said that for him it would be a mistake for the Fed to remove accommodation when inflation is below its 2% target, and that to establish credibility the Fed “should defend its inflation target from below.” “If we set them in place and target 2%, we should hit that target and have credibility that we will hit that target,” he said. Adding it’s a concern to him that the Fed “is moving accommodation when inflation is below target and maybe threatening to go lower.”

What Are the Costs to Extending QE Anyway? - Brad DeLong - Toward the end of an otherwise very good think piece (i.e., a think piece that quotes my weblog favorably), the intelligent and thoughtful Cardiff Garcia mysteriously writes: But the downsides to continued QE aren’t trivial either. Which makes me ask: what are the downsides to continued QE? The Federal Reserve buys long-term Treasury debt. The private sector has no less amount of safe U.S. government liabilities to serve as collateral--in fact, the cash or that short-term Treasuries now in private hands are better collateral for cash than the long-term Treasuries. The Federal Reserve now bears some short-term risk, but not if it holds the securities to maturity--which it will. The Federal Reserve has thus promised that it will not let the money stock fall below its long-term Treasury holdings until they mature, which adds to certainty and removes deflation risk. The private sector's limited risk-bearing capacity thus has a reduced quantity of duration risk to bear, and that risk-bearing capacity can be turned to bearing the risks of investment and enterprise. Everybody wins! Or, rather, nearly everybody wins: people who were in the business of bearing duration risk find that the returns to bearing duration risk are lower, and thus that their institutional capital in the form of expertise as to how and in what manner to bear duration risk has been impaired in value by the Federal Reserve's policies. But are those who are in the business of bearing duration risk more morally virtuous than those who are in the business of starting-up risky businesses or selling their labor-power for money? Is there a reason why Federal Reserve policy should be tuned two notches toward enriching those in the business of bearing duration risk and impoverishing those in the business of starting-up risky businesses or selling their labor-power for money?

Woodford and the QE tradeoffs, revisited -- Cardiff Garcia - Matt Klein gets in touch with Michael Woodford — macro theorist of world renown, author of a timely monetarist-cheering Jackson Hole paper, intellectual-space-provider for the NGDP level targeting movement — to ask the economist just why he doesn’t mind the Fed’s plan to begin tapering. Klein first cites a passage from Woodford’s paper at Jackson Hole last year:An increase in the safety premium obtained by making “safe assets” (in the relevant sense) more scarce would in itself be welfare-reducing. If Treasuries provide a convenience yield not available from other assets (including bank reserves), then reducing the quantity of Treasuries in the hands of the public reduces the benefits obtained from this service flow. And this is from Woodford’s email response to Klein, which refers to the above: This explains, in my view, how it was possible for Fed officials to indicate that it would likely be time to begin slowing the rate of purchases later in the year, even while admitting that it was not yet time for the tapering to begin last spring. The point was not so much that they felt confident that they could already predict labor market conditions in the remainder of the year, but rather that they could already predict how large the balance sheet would have gotten by later in the year — and they knew that, barring substantial unexpected developments with regard to economic conditions, they would be concerned by then about allowing the growth of the balance sheet to continue too much further.

The paradox of over-production in a world of QE - The Fed’s taper no-show this week resulted in a plethora of commentaries and articles flagging the risks of the world’s collective addiction to QE. To name a few:

- 1) Felix Salmon noted the dangers of the growing QE multiple — the incremental sugar hit the market gets from every anticipated unit of QE.

- 2) Tyler Cowen didn’t like that very much either.

- 3) Gillian Tett, meanwhile, suggested that all that QE does in its current form is provides credit for existing infrastructure and capacity, rather for new investment.

- 4) And HSBC’s chief economist Stephen King argued that QE only exacerbates the conditions that lead to savings glut conditions, which arguably created the crisis in the first place.

Either way, the idea that the economy is now somehow dangerously addicted to QE is a pervasive theme, and QE bashing is becoming the definitive vogue in town.

What The Average American Thinks Of QE - Despite the Fed's strongest efforts at improving its 'communication', the average American is relatvely unaware of just what it is that QE does (and is). Reuters reports that a sad 73% of respondents could not define what the crucial-to-the-market's-survival program is with 12% of respondents believing QE was a computer-assisted program that the Fed uses to manipulate the dollar; and another 11% thought it was part of the Dodd-Frank Wall Street reform legislation enacted following the crisis. With the 'taper' due to be announced today and the 'tapering is not tightening' message being trumpeted loud and clear, we suspect that will not get through to the public either; but as the infamous Michael Woodford noted, it doesn't matter, "the beliefs of the general public... [aren't] the primary channel that the Fed has been relying upon." More relevant, he said, is whether bond traders understand the Fed's intent. Via Reuters, The Fed's $2.8 trillion "quantitative easing" program has, among other things, lifted stock prices to record highs, driven interest rates to record lows and put a floor under what had been a reeling housing market. Yet barely a quarter of Americans even know what it is. A poll leading up to the Fed's pivotal decision ... found just 27 percent of U.S. adults could pick the correct definition of quantitative easing from among five possible answers.

Hilsenrath Spots "The 2016 Problem" Facing The Fed - As we warned here exactly one month ago, the tapering discussion may be merely a "sideshow to a previously undiscussed main event: the Fed's first forecast of 2016 interest rates." Now, the Fed's mouthpiece-at-large has decided we can handle the truth and the WSJ's John Hilsenrath explains the dilemma - The Fed's updated economic projections could show an economy that appears back to normal by 2016, but their projections of where short-term interest rates will be could show rates still quite low by then. Their challenge: How to justify the low interest-rate plan when their own estimates suggest an economy regaining its health. Crucially, Hilsenrath adds, as the economy improves, the Fed is trying to shift its emphasis from bond buying, which has uncertain costs and benefits, to the low-rate pledge. How will the Fed square an economy near full employment with a federal funds rate that remains historically low? "There is an inconsistency there," said John Taylor - apparently confirming what Rick Santelli asked before - "What is the Fed afraid of?" As we noted in detail here a month ago,"The problem is that at the end of 2016 [the FOMC's] economic forecasts may well show an economy that is close to full employment and price stability. An end-of-2016 funds rate of 4%, which implies 300bp of tightening over the course of 2016, is well in excess of what the market is pricing in....If the Fed presents a 2016 interest rate forecast that is well above the market's expectations—and if the market takes any cue from the Fed—this could tighten financial conditions such that the forecasted acceleration in growth fails to materialize"

Fed Candidate Kohn Warns Easy Policy Leads to Imbalances - Donald Kohn, a candidate to be the next Federal Reserve chairman, Monday said easy monetary policies risk creating financial problems so big that regulators can’t handle them. “Very easy monetary policy often builds imbalances that may become so large that can’t be countered by regulation,” Mr. Kohn said at an event on financial stability at the Brookings Institution think tank. The former vice-chairman of the Fed also said it’s not yet clear whether the Financial Stability Oversight Council, a panel of top U.S. financial regulators established after the 2008 crisis to help prevent future catastrophes, has the adequate tools necessary and is the right institution to fix major potential problems in the system. The Fed is a key member of the committee. “The jury’s still out,” he said. The comments come as Mr. Kohn’s chances of becoming the next Fed chairman shot up Sunday after the White House’s top pick, former Treasury Secretary Lawrence Summers pulled out of the race. Current Fed vice-chairwoman Janet Yellen is now thought to be the front-runner for the position, but Kohn has by no means been ruled out. Mr. Kohn’s comments provide insight into the candidate’s philosophy on issues of major concern to the lawmakers who approve Fed chairman nominees and to the firms facing increased regulation: how the Fed’s current easy money policies could threaten financial stability and whether regulators have a sufficient grip on those potential threats.

Ding Dong, the Witch is Dead, Summers Withdraws Name from Fed Chair Race - Yves Smith - I was just working on a post saying that Larry Summers campaign to become Fed chairman was in serious trouble, and here he’s gone and done us all the favor of getting the message. Larry has such high regard for himself that I doubt he has the self-awareness for a day of fasting and atonement to have led to a change of heart. His withdrawal was more likely to be based on hardening media opposition and lack of enthusiasm even among his professional peers (polls of academic and Wall Street economists showed a marked preference for Janet Yellen; there was also considerable derision and a wee bond market slump when the Nikkei ran a story that the Administration was indeed going to nominate Summers).

Full Text of Summers Letter Withdrawing From Fed Consideration

Paradigm Shift - It was deeply gratifying to learn today that Lawrence Summers has withdrawn his name from consideration for Chair of the Federal Reserve Board of Governors. Summers was a key architect of the late 20th century neoliberal economic system that failed catastrophically in 2007 and 2008, and he was implicated in some of the most notorious regulatory misjudgments of that era. There is no evidence that Summers has substantially altered the economic philosophy that animated him when he was helping to design and implement that system, so if he had acceded to the job of Fed Chief he would have been well-positioned to block stronger financial regulation and extend the unreconstructed regime of too-big-to-fail banks, loose rules, hegemonic financial sector growth and systemic financial instability that he helped create. Summers’s professional behavior is also a perfect reflection of the compromised, go-go ethos of crony capitalism that has sunken deep roots in our political culture during the past three decades, with its easy back-slapping familiarity and mutually lucrative relationships between government officials and the lords of finance, and its unobstructed two-way flows of personnel between the biggest financial institutions and the government agencies concerned with regulating them. Summers has shown a very healthy appetite for financial sector cash, and had continued the hearty meal right under the public eye, even while being actively considered for the Fed position. It’s disheartening that Summers was ever the President’s top choice, and the fact that he is out by no means assures that needed reforms and progressive changes will be made. But the era of Greenspan, Rubin and Summers has now receded one giant step further back into the annals of history and the insider power structure of that era has taken a heavy political hit which has diminished its aura of invincibility and can help prevent its key remaining figures from doing further damage in the present and future.

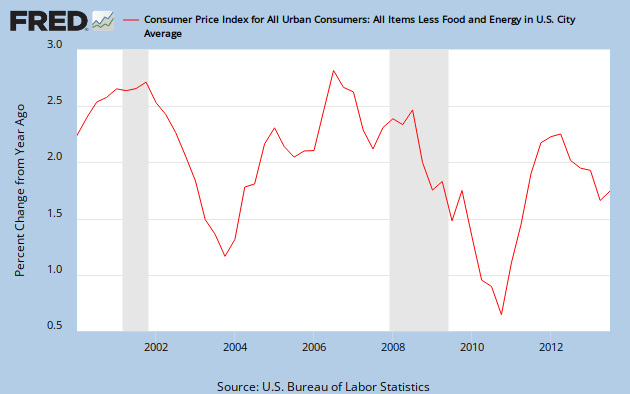

Fed Dilemma: Forecasting Inflation Is Hard - As it now stands, inflation is well under the Fed’s 2% target rate. As of the most recent reading in July, the Fed’s favored inflation gauge, the personal consumption expenditures price index, was up 1.4% from a year ago. That’s a firmer pace than what had been seen earlier in the year, but it’s still some distance from the Fed’s goal. Central bankers have argued frequently that they want inflation on target, not above, nor below. By that reckoning, it’s hard to understand how the Fed is contemplating dialing down the level of support it’s providing the economy when it’s undershooting its price target. If the Fed follows the path laid out by Chairman Ben Bernanke, the bond buying could end sometime next year. Officials who favor trimming the bond purchases cite continued economic growth, albeit at modest levels, and a steady decline in the unemployment rate. Most officials continue to believe inflation is weak because of temporary factors and will rise back to target over time. The Chicago Fed report said that over the recent years, inflation has simply not behaved as widely used forecasting models would have predicted. In fact, it’s done the opposite. Bank researchers noted that over 2009 and 2010 inflation picked up at a time when models predicted a “sharp” slowdown was in the offing.

Key Measures Show Low Inflation in August --The Cleveland Fed released the median CPI and the trimmed-mean CPI this morning: According to the Federal Reserve Bank of Cleveland, the median Consumer Price Index rose 0.2% (2.0% annualized rate) in August. The 16% trimmed-mean Consumer Price Index increased 0.1% (1.5% annualized rate) during the month. The median CPI and 16% trimmed-mean CPI are measures of core inflation calculated by the Federal Reserve Bank of Cleveland based on data released in the Bureau of Labor Statistics' (BLS) monthly CPI report. Earlier today, the BLS reported that the seasonally adjusted CPI for all urban consumers rose 0.1% (1.1% annualized rate) in August. The CPI less food and energy increased 0.1% (1.5% annualized rate) on a seasonally adjusted basis. Note: The Cleveland Fed has the median CPI details for August here.This graph shows the year-over-year change for these four key measures of inflation. On a year-over-year basis, the median CPI rose 2.1%, the trimmed-mean CPI rose 1.7%, the CPI rose 1.5%, and the CPI less food and energy rose 1.8%. Core PCE is for July and increased just 1.2% year-over-year. On a monthly basis, median CPI was at 2.1% annualized, trimmed-mean CPI was at 1.5% annualized, and core CPI increased 1.5% annualized. Also core PCE for July increased 0.9% annualized. These measures indicate inflation is below the Fed's target

Canadian Billionaire Predicts The End Of The Dollar As Reserve Currency; Warns "It's Likely To Get Ugly" - Grab your pre-FOMC popcorn and watch for a brief few minutes as sense is spoken on everything from the reality of the USD reserve currency's dwindling support, the stupidity of Obama's Syrian debacle, China and Russia's deals, the inevitable inflation when "the United States losing the privilege of being able to print at its will."

Fed Cuts Economic Growth Forecast - Confused why the Fed stunned everyone, and is willing to anger the TBAC by soaking up to a whoping 0.4% in 10 Year equivalents from the bond market each week thus crushing bond market liquidity even more? The reason is simple: even further trimming in the Fed's economic forecasts, which now sees 2014 GDP growth of 2.9%-3.1%, well below the 3.0%-3.5% seen in June, driven by yet another reduction in its PCE inflation forecast from 1.4%-2.0% to 1.3-1.8%. For those curious what the first forecast of 2016 data shows, here it is: the FF is seen anywhere between 0.5% to just over 4%, with the "longer run" eventually hitting 4%.

The Fed Marks Down Their Growth Forecast…Again -I’ve already given Ben&Co. a shout out for holding off on the taper, i.e., continuing their monetary stimulus at the same pace instead of beginning to dial back the asset-buying program. Clearly and appropriately, they were motivated by continued weakness in the macro-economy and the job market. The recovery remains fragile, and higher interest rates associated with even hints of Fed tightening right now aren’t helping. Another motivator for today’s surprise move is yet another mark-down of their GDP forecast. The figure below shows the average Fed forecast for this year’s real GDP growth (Q4/Q4) starting in January 2011 when they thought we’d be cruising at a smart clip by now, all the way through to today’s forecast where they think we’ll be puttering along at-or-slightly-above trend by the end of the year.The figure suggests a couple of points:

- –Like most forecasters, the Fed underestimated the depth and persistence of the downturn; though they’ve applied both conventional and creative monetary policy to push back hard,

–Surely the markdowns are partly a function of austere fiscal policy. That is, in their earlier forecasts for 2013, they could not have foreseen sequestration, the premature ending of the payroll tax break, and other measures that created the fiscal headwinds currently extracting 1-1.5 percentage points off of GPD growth this year. - –As I note here, the next Fed chairperson, whoever she may be, needs to consider recalibrating the Fed’s forecasting model, including a bigger role for financial markets, bubbles, and leverage.

Guess What The Fed's Original 2013 GDP Forecast Was - For some reason, today pundits are appalled by the loss of Fed credibility only because Bernanke "surprisingly" U-turned on the taper announcement, catching virtually everyone offguard. Perhaps instead of that, the sophisticated financial community should focus on the core of the problem: the Fed's chronic inability to look even more than a couple of years into the future without being dead wrong about what transpires, even in the absence of a great financial crisis (which the Fed never could predict in the first place of course). Case in point, yesterday's most recently downward 2013 GDP projection. The chart below tracks how the latest and greatest prediction of the 2.15% 2013 GDP (2.0%-2.3%) moved over the past two years.From Guggenheim's Scott Minerd:"Since the U.S. Federal Reserve first began to release economic projections three years ago, it has consistently downgraded its outlook. In the latest Federal Open Market Committee meeting, the Fed further lowered its projections for GDP growth in 2013 to an average of 2.15 percent, compared with an average of 4.15 percent from its initial projections in January 2011."In other words, the Fed started at 4.2%... and ended with half that number. Oh, and that includes the recent GDP-boosting revision, without which GDP growth for the year would have been even lower.

Weak Economic Recoveries Are A Feature, Not A Bug -- Business Insider’s Steven Perlberg passing along this chart from a new paper on American employment by economists Olivier Coibion, et al who analyzed recessions and recoveries going back more than 20 years and found that “weak” recoveries have increasingly become the rule rather than the exception: Summary: The trend is reminiscent of 1980s Western European recessions dubbed “Eurosclerosis,” leading the authors to ask if the United States is fighting its own bout of “Amerisclerosis.” In lay terms, we might call Amerisclerosis the “jobless recovery.” New normal indeed.

Tapering threatens a stormy outlook for America - FT.com: Sheila Bair -The storm season will soon be upon the US, both meteorologically and metaphorically. Continued – though slowing – economic growth suggests the Federal Reserve’s anticipated “tapering” of its aggressive bond-buying programme may not be far off, and gale-force winds are possible. We saw a bolt of lightning in June when the stock market dropped 659 points at the mere suggestion by Ben Bernanke, Fed chairman, that the central bank could slow its bond purchases in autumn. Well, what do you expect? When the buyer of an estimated 90 per cent of net new bond issuance announces it is likely to call a halt, markets react. It is already raining in emerging economies. Weekly outflows from emerging bond and equity funds are escalating, reaching a total of $6bn at the end of August. Capital can now chase juicier returns in the US, particularly in the bond market, where 10-year Treasury rates hover around 3 per cent, nearly double the 1.6 per cent the securities were yielding in May. An eventual return to normalised interest rates will be a welcome development for savers, as well as markets, which have been distorted by the Fed’s intrusions. However, the path to normalisation could be challenging, particularly for US megabanks. It is hard to predict the impact. When was the last time the Fed bought $3.4tn of bonds to keep long-term rates low? Right. Never. Megabanks will reap benefits from a return to normality. Increased trading activity in volatile markets will help their investment banking revenues. Rising rates on their loans will benefit their commercial side (and ideally motivate them to lend more). But the downsides are real. All those low-yielding bonds sitting on their balance sheets will lose market value as rates climb, which under new capital rules will eat into their capital base. At the four biggest banks, the value of Treasury and mortgage-backed securities holdings fell by $13bn in the second quarter because of rising rates, with Bank of America taking the biggest hit. At some point, increased rates will put upward pressure on the rates they must pay depositors.

A near debt experience: New crisis approaching? - Central bankers are widely held to be boring. True, central bank bosses can attract vast media speculation and, as Larry Summers just learnt, it’s a harrowing process trying to gain approval. New Central Bankers can be treated like financial rock stars, as newly-appointed Governors in Britain and India have just discovered. Well, at least for the first week... Nevertheless, central bankers are broadly perceived as rather dull, plodding individuals and their excitement at the minutiae of Repo transactions can cure insomnia in many for whom sleep is a difficult state to achieve. The Bank for International Settlements, “the central bankers’ bank” is situated in Basel, a lovely Swiss city but nonetheless not regarded as a hotspot of excitement even amongst the Helvetic Cantons [Switzerland]. However, when somebody at the BIS breaks their silence and leads what amounts to the banking equivalent of the monastic life, then the world ought to be listening. This week William White the BIS Chief Economist has made a chilling pronouncement to freeze the autumnal Swiss air: “This looks to me like 2007 all over again, but even worse.” Given his office, such a brutal prognostication would be worrying enough. However, bear in mind Mr White’s pedigree - he foresaw the last financial crisis (and was widely ignored at the time). Should we be terrified?

Unpleasant After-Effects of Prolonged Low Interest Rates Starting to Show: There's a notion among central banks of the global economy that goes like this: if you lower interest rates, you will get economic growth. On the surface, it makes sense; easy monetary policies by central banks are supposed to bring confidence to an economy -- they're supposed to encourage consumers and businesses to borrow, which should translate to more jobs created and an improvement in the standard of living. This phenomenon of lowering interest rates to spur the economy has spread through the global economy like wild fire. Interest rates at the central bank of Australia have been trending lower since the financial crisis. In December of 2007, the cash rate (the benchmark interest rate) there was 6.75%. Fast-forwarding to today, this rate is 2.5%. Brazil's central bank has lowered its benchmark interest rate since the end of 2008. The interest rate dictated by the country's central bank stood at 13.75% near the end of 2008; now it stands at nine percent. The benchmark interest rate in South Africa is down almost 50%. While we've been watching this happen, no one is really asking the question how are interest rates being kept low? The answer: to keep the interest rates low central banks print more paper money and stay involved in their bond markets. Since central banks in the global economy started to lower their interest rates, their money supply has gone up significantly. For example, since the last quarter of 2007 to the second quarter of 2013, Brazil's M1 money stock (the amount of notes and coins in circulation plus timed deposits, such as checking accounts) has increased over 52%. ( But in spite of all the money printing and other games being played by central banks in their effort to keep interest rates down, the global economy isn't seeing robust growth. The International Monetary Fund (IMF) has lowered its expectation on growth in the global economy repeatedly.

The Great Recession isn't over yet - A majority of Americans say that the country still hasn't recovered from the financial crisis and many think that another crisis may be on its way. Five years ago this month, the bankruptcy of Lehman Brothers signaled the start of an economic crisis and the beginning of the Great Recession of 2008. For most Americans, the nation is still struggling with that recession, one that many Americans say had a serious impact on them personally. The latest Economist/YouGov Poll finds just 8% saying the country has recovered from the recession. There is a long way yet to go. The recession affected many Americans. More than half say they know someone who lost their job in the financial crisis – and 7% claim they personally lost a job. And when Americans are asked how serious the recession was, 41% describe the impact on them personally as serious, only a few percentage points less than the result in early February 2009.

Drivers of financial boom and bust may be all in the mind - The research offers the first insight into the processes in the brain that underpin financial decisions and behaviour leading to the formation of market bubbles. Publication of the study coincides with the five year anniversary of the infamous collapse of the Lehman Brothers investment bank in 2008. A 'bubble' happens when active trading of a commodity or asset reaches prices that are considerably higher than its intrinsic value, usually followed by a market crash. The boom and bust of the US 'dot com' sector and the crash in the UK housing market are recent examples that resulted in billions of pounds in financial losses. Although bubbles have been intensely investigated in economics, the reasons why they arise and crash are not well understood and we know little about the biology of financial decision behaviour. Researchers at the California Institute of Technology investigated the problem by bringing together expertise in experimental finance and neuroscience to look at the brain activity and behaviour of student volunteers as they traded shares within a staged financial market. The researchers used functional Magnetic Resonance Imaging (fMRI), a technique to measure the flow of blood in the brain as an indication of activity, to map participants' brain activity as they traded within the experimental market. They found that the formation of bubbles was linked to increased activity in an area of the brain that processes value judgements. People who had greater brain activity in this area were more likely to ride the bubble and lose money by paying more for an asset than its fundamental worth.

U.S. debt now about 73% of GDP, CBO says -- The U.S. national debt is now about 73% of gross domestic product, the Congressional Budget Office said Tuesday. The percentage of debt is higher than any point since around World War II, and twice the percentage it was at the end of 2007, the nonpartisan agency said in its long-term budget outlook. If current laws stay in place, debt will decline "slightly" relative to GDP over the next few years, the agency said. But it warned that growing future deficits will push the debt to 100% of GDP 25 years from now

The new CBO debt study is way worse than the media is telling you - Almost all media reports about the Congressional Budget Office’s new long-term budget analysis will highlight its forecast that the federal public debt, now about 73% of GDP, is on track to reach 100% of GDP in 2038. Now that’s scary enough. As Maya MacGuineas of the Committee for a Responsible Federal Budget puts it: “Today’s report confirms exactly what we have been warning — that the debt is on an unsustainable long-term trajectory.” So over the next 25 years, Americans will be taxed more to pay for a federal government that will more purely become a redistribution, wealth-transfer mechanism. Taxes and spending at record highs. America as a nuclear-armed insurance company. But here’s the thing: that forecast, as the CBO notes, does not factor in “the harm that growing debt would cause to the economy.” Hey, that would be a good thing to know, right? Well, you have to dig deeper into the CBO study to find those numbers. And when you take into account stuff like how deficits might “crowd out” investment in factories and computers and how people might respond to changes in after-tax wages, you find the debt is much, much larger, closer to 200% of GDP.

Interest, Social Security to Eat Up Increasing Share of U.S. Budget - The government likely faces rising costs to fund the national debt that will likely “crowd out” a lot of its ability to spend on military and social programs in coming years, a new report from the Committee for a Responsible Federal Budget warns. The group, which bills itself as a nonpartisan budget watchdog, weighed in just ahead of a Federal Reserve policy meeting at which officials could take the first in a series of steps that will likely lead to higher borrowing costs in the future. At the heart of the report is the notion that after a long stretch of rock-bottom borrowing costs, rates will almost certainly rise over time. Annual deficits and the total national debt, which are cheap to finance now, will become more challenging to pay for in the years to come. Moreover, interest rates will be rising at the same time as government spending related to the retirement of the baby boom generation. Given the projected path of interest rates and the level of government debt over coming years, federal spending to finance government borrowing will rise from 1.3% of GDP today, to 6.4% in 2050, the report said. This projection is based on interest rates moving back toward “historic levels,” the group said in its report.

This Is Not A Crisis - Paul Krugman - It’s not even a picture of a crisis. The new CBO long-term budget projections are out, and while they’re not good, they don’t show crisis levels of debt even looking out a quarter-century. Unless, that is, you believe that debt of 100 percent of GDP is the end of the world even though Britain exceeded that level for a large part of its history: The point is not that we should completely ignore issues of fiscal responsibility. It is that we are nowhere near fiscal crisis; we aren’t even looking at anything like a fiscal crisis 15 or 20 years from now. So budget deficits, entitlement reform, and all that simply don’t deserve to be policy priorities, let alone dominate the national discussion the way they did for the past few years.

The US Federal Deficit Continues to Shrink - The federal budget deficit has been plummeting in size over the last few years; however, judging from polls, most Americans do not know that – indeed, their concern over the deficit has grown even as the annual deficit has shrunk significantly. And it continues to do so: the Congressional Budget Office (CBO) estimated yesterday that the deficit for the first eleven months of this fiscal year fell $400 billion from the comparable period last year.The 35 percent decrease was driven by a combination of decreases in government spending and increases in revenues. Federal outlays fell by $127 billion, and tax receipts increased by $284 billion. This is part of a longer trend. As highlighted by Nobel Prize-winning economist Paul Krugman in August, the budget deficit (as a percent of GDP and in absolute terms) has been falling since it peaked in 2009. But you would not know that from reading the polls alone. Despite the decreasing size of the deficit, 72 percent of Americans surveyed in January 2013 said they felt reducing the budget deficit should be a “top priority” for the president and Congress this year. In January 2009, only 53 percent of Americans said reducing the budget deficit should be a top priority. But back in 2009, the deficit was higher than it is now. It was about to increase because tax revenues fell due to the recession and the mostly one-year increase in government spending – known as the “stimulus” – to arrest the free fall of the economy and to stem job losses. A YouGov.com poll also found that far more people erroneously believed the deficit was larger in 2012 compared to 2011.

Bernanke Warns That Lawmakers’ Budget Battles Could Tank Economy - Federal Reserve Chairman Ben Bernanke on Wednesday warned that a government shutdown or failure to raise the federal debt ceiling could have “very serious consequences” for the economy and urged the White House and Congress to reach a budget deal. “Our ability to offset these shocks is very limited, particularly a debt limit shock, and I think it’s extraordinarily important that Congress and the [Obama] administration work together to find a way to make sure the government is funded, public services are provided, that the government pays its bills and that we avoid any kind of event like 2011 which had at least for a time a noticeable adverse effect on confidence and on the economy,” Mr. Bernanke said at a press conference. The U.S. Treasury Department has told Congress that the federal government will exhaust its ability to continue borrowing money in mid-October. At that point, the government would only have cash on hand available to finance its operations, including making interest payments on the national debt and paying Social Security, Medicare and veterans’ benefits. The last major showdown in 2011 rattled markets. Before that, the White House and Congress need to strike a spending deal for the new fiscal year, which starts Oct. 1. Barring that, the government would shut down. Mr. Bernanke said that Fed officials discussed the ongoing fiscal debates at a policy meeting Wednesday. The chance of a government shutdown as well as the possibility that Congress won’t raise the debt limit are a concern, he said. “If these actions led the economy to slow, then we would have to take that into account,” Mr. Bernanke said.

Treasury warns Congress not to wait til last minute on debt ceiling (Reuters) - Treasury Secretary Jack Lew on Tuesday warned Congress against waiting until the last minute to raise the nation's limit on borrowing, saying a misstep could irrevocably damage the economy. "We cannot afford for Congress to gamble with the full faith and credit of the United States," Lew told the Economic Club of Washington, a business forum. The government has been scraping up against its $16.7 trillion debt limit since May but has avoided defaulting on any bills by employing emergency measures to manage its cash, such as suspending investments in pension funds for federal workers. Lew repeated a warning he made last month that Treasury would run out of borrowing options around mid-October, when he said that Treasury would be left with only around $50 billion in cash on hand. Default could come soon after that. As America runs lows on cash there is a risk investors could lose confidence in Washington and stop reinvesting in U.S. government debt. Every Thursday, the Treasury pays investors back about $100 billion that investors immediately lend back to the government, a process known as rolling over the debt. "If U.S. bond holders decided that they wanted to be repaid rather than continuing to roll over their investments, we could unexpectedly dissipate our entire cash balance," Lew said.

Obama to face fresh test of resolve over budget talks - FT.com: Jack Lew, the US Treasury secretary, said on Tuesday that the administration would not negotiate over congressional approval to lift US borrowings, drawing a line in the sand ahead of high-stakes budget talks with Republicans in coming weeks. But after a fortnight in which President Barack Obama has zigzagged between diplomacy and military action on Syria, and backed away from nominating Lawrence Summers to head the Federal Reserve, Republicans plan to test the president’s resolve. Washington faces two fiscal crises in the next month pitting the White House against Republicans in Congress, both of which are littered with partisan mines to make passage difficult in such a short period of time. Congress must approve a new budget by the end of the month or face a government shutdown, and also lift the country’s borrowing limits by around mid-October to fund public spending at the threat of triggering a sovereign default. The stand-off coincided with the release from the non-partisan Congressional Budget Office of its latest dire warning about the long-term fiscal outlook in the US. According to the CBO, federal debt held by the public – now at 73 per cent of gross domestic product – will reach 100 per cent of the economy in 2038, a trajectory it dubbed unsustainable.

This Year's Budget Fight Isn't About The Budget = There are many reasons why the budget fight that will take pace over the next few weeks and months will be more difficult than any of the close-to-debacles that have occurred in recent years.The reasons include John Boehner (R-OH), who was already the weakest and least effective House speaker in modern times, being even weaker; a president with what at best is tepid support from his own party in Congress; an increasingly frustrated tea party wing of the GOP that no longer sees procedural compromises as satisfying; increasingly defiant House Democrats, who see less and less value in supplying votes to enact must-pass legislation when the Republican majority is unable to do it; and a seemingly hopeless split in the House GOP that makes further spending reductions, standing pat at current levels or spending increases impossible. Add to this "crisis fatigue." So many actual or man-made economic and financial disasters have occurred in recent years that the kinds of things that used to scare Congress and the White House into compromising -- like possible federal defaults and government shutdowns -- no longer motivate them to act. But none of these admittedly depressing factors are what makes this year's budget cliffhanger so difficult. This year the biggest complication is that the budget fight isn't really about the budget: It's about ObamaCare, and that makes it hard to see what kind of arrangement will garner enough votes to avoid the kind of shutdown and debt ceiling disasters that have been only narrowly averted the past few years.

Shutdown moves closer to reality - The threat of a government shutdown intensified Tuesday as House Republican leaders moved toward stripping funding from President Obama’s landmark health-care initiative and setting up a stalemate with the Democratic Senate.House Speaker John A. Boehner (R-Ohio) had hoped to keep the government open past Sept. 30 with relatively little fuss. But roughly 40 conservatives revolted. After a strategy session Tuesday, Boehner and his leadership team were being pushed into a more confrontational strategy that would fund the government into the new fiscal year only if Democrats agreed to undermine Obama’s signature legislative achievement.Obama and Senate Majority Leader Harry M. Reid (D-Nev.) have ruled that out, leaving the parties hurtling toward an apparent impasse. In less than two weeks — with the nation at war and authorities investigating a mass shooting at the Washington Navy Yard — every federal agency from the Pentagon to the FBI is due to shut down unless Congress can reach an agreement. A shutdown would not only disrupt critical government services but also whip up a panic just as lawmakers confront the next major deadline on their fall calendar: the need to raise the $16.7 trillion federal debt limit.Congressional Budget Office Director Douglas Elmendorf said Tuesday that the Treasury Department is likely to run out of cash to pay its bills “sometime between late October and mid-November,” confirming independent estimates. Treasury Secretary Jack Lew has so far been vague about that deadline, telling Congress only that he would exhaust his ability to juggle the books by mid-October.

#cliffgate Update: Is A Shutdown Boehner's Only Way Out? - I'm quickly coming to the conclusion that a government shutdown may be the only way to deal with the coming budget bedlam and #cliffgate.Let's start by reviewing the situation.

- As of today there are less than two weeks before fiscal 2014 begins.

- None of the FY14 appropriations have been enacted; none have any chance of being enacted.

- There are no formal negotiations going on between Congress and the White House, between the House and Senate or between Democrats and Republicans.

- The only discussions that seem to be taking place are between the two main factions in the House GOP...and the best thing that can be said about them is that they appear to be going nowhere.

- The original plan suggested by the House Republican leadership was flatly rejected by the tea partiers in the House GOP caucus. The tea partiers were energized by their success.

- House Speaker John Boehner (R-OH) and Majority Leader Eric Cantor (R-VA) haven't put a new plan on the table since their last plan was rejected by members of their own party a week ago. Boehner has even indicated publicly that he's not sure whether there is a plan than is acceptable to his caucus.

- Meanwhile, in keeping with the tradition that the House goes first on CRs, Senate Majority Leader Harry Reid (D-NV) has said he is going to wait for the House to act before moving forward.