Fed Balance Sheet January 9, 2014: The Fed's balance sheet is a report showing factors supplying reserves into the banking system and factors absorbing (using) reserve funds. Essentially, the balance sheet shows the various Fed programs for injecting liquidity into the economy and how much the Fed has used each for adding or withdrawing reserves. For the January 8 week, the Fed balance sheet expanded by $4.6 billion, following an $8.9 billion contraction in the prior week. Holdings of Treasuries rose $4.2 billion, following a decrease of $0.1 billion while "other assets" (largely those denominated in foreign currencies) increased by $2.9 billion, following a decrease of $1.6 billion the week before. Total assets for the January 8 week were $4.028 trillion. Reserve Bank credit for the January 8 week rose $1.2 billion after falling $4.1 billion the prior week.

FRB: H.4.1 Release--Factors Affecting Reserve Balances--January 9, 2014: Federal Reserve Statistical Release - Factors Affecting Reserve Balances of Depository Institutions and Condition Statement of Federal Reserve Banks

FOMC Minutes: "Proceed cautiously" with QE3 Tapering - From the Fed: Minutes of the Federal Open Market Committee, December 17-18, 2013 . Excerpt: In their discussion of monetary policy in the period ahead, most members agreed that the cumulative improvement in labor market conditions and the likelihood that the improvement would be sustained indicated that the Committee could appropriately begin to slow the pace of its asset purchases at this meeting. However, members also weighed a number of considerations regarding such an action, including their degree of confidence in prospects for sustained above-potential economic growth, continued improvement in labor market conditions, and a return of inflation to its mandate-consistent level over time. Some also expressed concern about the potential for an unintended tightening of financial conditions if a reduction in the pace of asset purchases was misinterpreted as signaling that the Committee was likely to withdraw policy accommodation more quickly than had been anticipated. As a consequence, many members judged that the Committee should proceed cautiously in taking its first action to reduce the pace of asset purchases and should indicate that further reductions would be undertaken in measured steps. Members also stressed the need to underscore that the pace of asset purchases was not on a preset course and would remain contingent on the Committee's outlook for the labor market and inflation as well as its assessment of the efficacy and costs of purchases. Consistent with this approach, the Committee agreed that, beginning in January, it would add to its holdings of agency mortgage-backed securities at a pace of $35 billion per month rather than $40 billion per month, and add to its holdings of longer-term Treasury securities at a pace of $40 billion per month rather than $45 billion per month.

Key Passages in Fed Minutes: Consensus on QE, Focus on Bubbles - Federal Reserve officials were largely in agreement on the decision to begin winding down an $85 billion-per-month bond-buying program. As they looked to 2014, they began to focus more on the risk of bubbles and financial excess. Here is a look at key passages in the minutes of the Dec. 17-18 meeting of the Fed’s policy committee, released Wednesday: Participants generally anticipated that the improvement in labor market conditions would continue, and most had become more confident in that outlook. Against this backdrop, most participants saw a reduction in the pace of purchases as appropriate at this meeting and consistent with the Committee’s previous policy communications.Some … expressed concern about the potential for an unintended tightening of financial conditions if a reduction in the pace of asset purchases was misinterpreted as signaling that the Committee was likely to withdraw policy accommodation more quickly than had been anticipated. As a consequence, many members judged that the Committee should proceed cautiously in taking its first action to reduce the pace of asset purchases and should indicate that further reductions would be undertaken in measured steps.Several [Fed officials] commented on the rise in forward price-to-earnings ratios for some small cap stocks, the increased level of equity repurchases, or the rise in margin credit. One pointed to the increase in issuance of leveraged loans this year and the apparent decline in the average quality of such loans. A couple of participants offered views on the role of financial stability in monetary policy decision making more broadly. One proposed that the Committee analyze more explicitly the potential consequences of specific risks to the financial system for its dual-mandate objectives and take account of the possible effects of monetary policy on such risks in its assessment of appropriate policy. Another suggested that the importance of financial stability considerations in the Committee’s deliberations would likely increase over time as progress is made toward the Committee’s objectives, and that such considerations should be incorporated into forward guidance for the federal funds rate and asset purchases.

Fed Watch: FOMC Minutes - The Quick Review - Near the beginning of the minutes, the staff presents a survey on the expected costs and benefits of the asset purchase program. I feel I need to highlight this section since I have complained that the Fed is leaving us in the dark on the cost/benefit calculus. Now I know why they are leaving us in the dark - they are pretty much in the dark themselves. They sense that the math still favors ongoing purchases:Most participants judged the marginal costs of asset purchases as unlikely to be sufficient, relative to their marginal benefits, to justify ending the purchases now or relatively soon; a few participants identified some possible costs as being more substantial, indicating that the costs could justify ending purchases now or relatively soon even if the Committee's macroeconomic goals for the purchase program had not yet been achieved. Still, they are worried about financial stability:Participants were most concerned about the marginal cost of additional asset purchases arising from risks to financial stability, pointing out that a highly accommodative stance of monetary policy could provide an incentive for excessive risk-taking in the financial sector. And they really don't know what they are doing: It was noted that the risks to financial stability could be somewhat larger in the case of asset purchases than in the case of interest rate policy because purchases work in part by affecting term premiums and policymakers have less experience with term premium effects than with more conventional interest rate policy. Some continue to think of the Fed's balance sheet like that of a regular bank: Participants also expressed some concern that additional asset purchases increase the likelihood that the Federal Reserve might at some point suffer capital losses. I think it silly to complain about potential future losses without acknowledging the current profits; the asset purchase program needs to be evaluated across its entire lifespan. Moreover, it's silly to think the Federal Reserve needs to make a "profit" as if it were a regular bank. The Federal Reserve does not exist to make a profit. It exists to conduct the monetary policy of the nation. But I digress. In any event, policymakers should actually understand this, and hopefully recognize that the only reason for concern on this point is the public optics.

Fed Minutes Show Majority Believe "Marginal Efficacy of QE Likely Declining"; Economy Turned the Corner? - Inquiring minds are reading Minutes of the December 17-18 FOMC Meeting to see what the Fed is thinking. Here are a few key paragraphs: Most participants judged the marginal costs of asset purchases as unlikely to be sufficient, relative to their marginal benefits, to justify ending the purchases now or relatively soon; a few participants identified some possible costs as being more substantial, indicating that the costs could justify ending purchases now or relatively soon even if the Committee's macroeconomic goals for the purchase program had not yet been achieved. Participants were most concerned about the marginal cost of additional asset purchases arising from risks to financial stability, pointing out that a highly accommodative stance of monetary policy could provide an incentive for excessive risk-taking in the financial sector. It was noted that the risks to financial stability could be somewhat larger in the case of asset purchases than in the case of interest rate policy because purchases work in part by affecting term premiums and policymakers have less experience with term premium effects than with more conventional interest rate policy. Participants also expressed some concern that additional asset purchases increase the likelihood that the Federal Reserve might at some point suffer capital losses. A majority of participants judged that the marginal efficacy of purchases was likely declining as purchases continue, although some noted the difficulty inherent in making such an assessment. A couple of participants thought that the marginal efficacy of the program was not declining, as evidenced by the substantial effects in financial markets in recent months of news about the likely path of purchases.

FRB: Press Release--Federal Reserve issues FOMC statement from December 18, 2013

Still unclear exactly how QE eases conditions: Fed's Dudley - Extensive research into massive asset-purchase programs has not yet clarified whether such policies ease financial conditions primarily as a signal to investors or more directly through private portfolios, an influential U.S. central banker said on Saturday.The Federal Reserve is currently buying $75 billion a month in Treasuries and mortgage bonds in its third round of quantitative easing, or QE3, which is meant to ease longer-term borrowing costs in the economy."We still don't have well-developed macro-models that incorporate a realistic financial sector,' William Dudley, president of the New York Fed, told an economics conference. "We don't understand fully how large-scale asset purchase programs work to ease financial market conditions, there's still a lot of debate ..." he said. "Is it the effect of the purchases on the portfolios of private investors, or alternatively is the major channel one of signaling?"

New York Fed Chief Sees Mystery in Bond Buying - Federal Reserve Bank of New York President William Dudley said on Saturday that some key aspects of how the central bank’s bond-buying stimulus effort works remain mysterious. For more than a year, the Fed has been engaged in purchasing Treasury and mortgage bonds in a bid to drive up growth and lower unemployment. The program has been controversial. While officials like Mr. Dudley and Fed Chairman Ben Bernanke see clear benefits, others have struggled to gauge the impact of the effort. Leaders at the Kansas City and Dallas Fed banks see scant value in the buying and worry its impact is instead setting the stage for new asset-market bubbles. On the other side, some central bankers have even attempted to provide fairly clear metrics about the influence of asset buying on things like the unemployment rate. A speech last autumn by San Francisco Fed leader John Williams held that a past iteration of Fed bond-buying led to a tangible decline in the unemployment rate. Mr. Dudley acknowledged a lot is still unknown about how the bond buying works. His observation is important because he has long been a supporter of aggressive Fed actions to help the economy. Referring to the Fed’s stimulus program, Mr. Dudley said, “we don’t understand fully how large-scale asset-purchase programs work to ease financial market conditions—is it the effect of the purchases on the portfolios of private investors, or alternatively is the major channel one of signaling?”

Dudley: Unclear exactly how Fed bond buying works --Federal Reserve Bank of New York President William Dudley said Saturday some key aspects of how the central bank's bond-buying stimulus effort works remain mysterious. For over a year, the Fed has been engaged in purchasing Treasury and mortgage bonds in a bid to drive up growth and lower unemployment. Citing an improving economy, the Fed cut the pace of those purchases last month, and many market participants expect a steady reduction to happen over the course of the year. The program has been controversial. While officials like Mr. Dudley and Fed Chairman Ben Bernanke see clear benefits, others have struggled to gauge the impact of the effort. Leaders at the Kansas City and Dallas Fed banks see scant value in the buying and worry its impact is instead setting stage for new asset market bubbles. On the other side, some central bankers have even attempted to provide fairly clear metrics about the influence of asset buying on things like the unemployment rate. A speech last autumn by San Francisco Fed leader John Williams held that a past iteration of Fed bond buying lead to a tangible decline in the unemployment rate. Speaking as part of a panel in Philadelphia on the activities of the regional Fed banks, Mr. Dudley acknowledged a lot is still unknown about the impact of the bond buying. His observation is important because the official has long been a supporter of aggressive Fed actions to help the economy. The New York Fed leader has for some time expressed support for continuing the purchases, even as he also voted in favor of the Fed's decision last month to cut back on the buying.

Fed's Bill Dudley: The Fed Doesn't Fully Understand How QE Works -- Well, it took three years, but finally the Goldman Sachs-based head of the New York Fed, Bill Dudley, admitted what we all knew. From a speech just given by NY Fed's Bill Dudley at the 2014 AEA meeting in Philadelphia:"We don't understand fully how large-scale asset purchase programs work to ease financial market conditions" Or, in other words, "we still don't know how QE works." It just does (thank you Kevin Henry). And this coming from the people who want their word to become equivalent to gospel in a time when QE is being phased out and replaced with forward guidance. Luckily, at least the Fed knows all about how "forward guidance" works. The good news: it only took $4+ trillion in Fed "assets" for the central bank to understand it had no idea what it was doing.

Fed's Williams: Fed Likely to Taper More, End Bond-Buying This Year - Federal Reserve Bank of San Francisco President John Williams said Tuesday he fully supported the central bank’s recent decision to pull back on its easy-money policies last month, and added that he expects to see the Fed’s bond-buying purchases end at some point this year. The official was referring to the Fed’s decision to slow the pace of its bond-buying stimulus program in December. Then, central bankers cut the monthly pace of Treasury and mortgage purchases to $75 billion from $85 billion, amid rising confidence in the economic outlook. “Assuming the economic recovery plays out as we expect, we will likely continue to reduce the pace of those purchases, and eventually eliminate them, over this year,” Mr. Williams said. Speaking to reporters after his speech, he said he expects to see a “steady, measured” pace of cuts in the program absent some major shock in the economy. Mr. Williams told reporters that when central bankers met last month, they faced a “pretty straightforward” story of economic improvement and less uncertainty from the government. “I fully supported” the decision to slow the bond buying, he said. In his formal remarks to a bankers’ group in Phoenix, Ariz., the central banker said “with the economy having improved so much and the future looking brighter, it was time to start taking our foot off the accelerator and ease up on the monetary stimulus.”

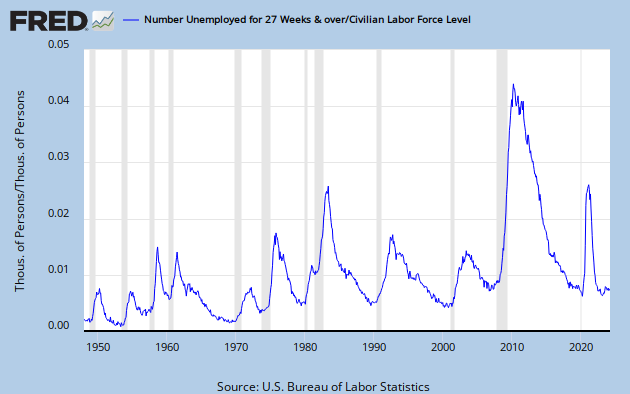

Fed’s Rosengren Says Economy Far From Where Needed - Despite clearer signs of a U.S. economic recovery, its gradual nature comes with potentially deep-rooted costs that warrant the Federal Reserve to keep its policy highly accommodative, a top central bank official said Tuesday. “There are significant costs to a slow recovery,” “It can potentially have longer-lasting and structural implications for labor markets and the economy. There may also be an impact on the Federal Reserve’s ability to reach its inflation target in a reasonable time frame.” Because the central bank is falling short on each of its two mandates–achieving full employment and maintaining stable inflation–”by fairly large margins,” Mr. Rosengren said there is “ample justification” for the Fed to keep monetary policy highly stimulative to support growth. In December, the Fed’s policy-setting board decided to reduce its $85 billion monthly bond-buying program by $10 billion starting in January. Mr. Rosengren, who no longer has a voting slot this year, was the sole dissenter at that meeting. On the employment front, the central banker isn’t fully convinced the labor market is as strong as the recent decline in the unemployment rate might suggest. Last reported at 7% for November, Mr. Rosengren said the figure is still far short of the 5.25% he estimates as full employment in the U.S. The official also pointed to a low quit rate, which suggests workers aren’t confident enough to leave their jobs for potentially better prospects even amid tepid wage growth. He also warned about employment in the prime working-age group of 25 to 54 growing only in line with its population, as well as the unusually high level of long-term joblessness.

Rapid QE withdrawal could permanently harm U.S. workers: Fed's Rosengren - A dovish U.S. central banker on Saturday again urged the Federal Reserve to be patient as it trims its support for the economy, in part because it risks permanent damage to the labor market. Boston Fed President Eric Rosengren dissented against the central bank's landmark decision last month to reduce its bond-buying program by $10 billion to $75 billion in purchases per month. In a speech here, he repeated it was a mistake because unemployment remains too high and inflation too low. "Policymakers have the opportunity to be patient in removing accommodation, speeding up the process of achieving both elements of the Fed's dual mandate" of maximum sustainable employment and inflation of around 2 percent, he said. Rosengren, who had earlier told Reuters he preferred to wait until March to cut QE, said on Saturday the risks of continuing the bond-buying at the previous $85-billion pace seem small relative to the risks of a permanent rise in the number of Americans who are out of work."The failure of monetary and fiscal policy to generate a more rapid recovery risks creating a long-term structural unemployment problem out of a severe cyclical downturn. This concern also underlies my dissent," he said at a meeting of the American Economic Association.

Federal Reserve’s Kocherlakota: Fed May Need to Do More – Federal Reserve Bank of Minneapolis President Narayana Kocherlakota said Thursday evening weak inflation and “too high” levels of unemployment argue in favor of the central bank doing more to help the economy. But at the same time, the incoming voting member of the monetary-policy setting Federal Open Market Committee also expressed qualified support for pulling back on the Fed’s bond-buying program. Mr. Kocherlakota is one of the Fed’s most consistent supporters of aggressive action to aid the economy, and he has stood apart from many of his colleagues and called for additional forms of action to boost employment at a time where the Fed has taken concrete steps toward lowering its level of support for the economy. The Fed “could do better with respect to both of its congressionally mandated objectives by adopting a more accommodative monetary policy stance,” Mr. Kocherlakota said at a public forum held at his bank Thursday evening. He spoke in the wake of the Fed’s decision last month to cut the pace of its bond-buying stimulus program to $75 billion a month, from $85 billion. Most expect the cuts to continue through the course of the year. On Tuesday, San Francisco Fed leader John Williams said it is likely an improving economy will allow the central bank to steadily reduce the pace of buying at the year progresses. Market participants see the program ending later this year. In his remarks, Mr. Kocherlakota appeared to agree with the move to cut bond buying. “As long as the economy evolves according to our outlook…we will continue a pattern of reducing” the pace of bond buying, he said.

Fed's Plosser at odds with policy approach favored by Yellen - The Great Recession could have done permanent damage to potential U.S. output, a top Federal Reserve official said on Saturday, taking an indirect shot at more cyclical approaches to policy-making that is favored by many economists, including the next Fed chair. Philadelphia Fed President Charles Plosser said in a speech he is skeptical of so-called "optimal control" approaches to monetary policy in which mathematical models are used to predict when things like unemployment and economic growth will return to more normal levels. Fed Vice Chair Janet Yellen, who is set to take the reins at the U.S. central bank next month, has often touted this approach, including tolerating higher inflation for a short time in order to speed up the overall economic recovery. Plosser - who regains a vote on policy this year under the Fed's rotating system - is among the minority of hawks who oppose policies such as large-scale bond-buying. "Measures that arbitrarily, or by assumption, assign the bulk of fluctuation in GDP to purely temporary factors may provide poor policy guidance when shocks are more permanent in nature,"

Fed Watch: A Weekend of Fedspeak - Federal Reserve speakers were out in force this weekend at the American Economic Association's annual meeting in Philadelphia. The first rumblings from Fed speakers came from the hawkish-side of the aisle. Via MarketWatch: Philadelphia Fed President Charles Plosser warned Friday that the central bank may have to be "aggressive" in lifting interest rates and may have to chase market rates higher, if banks were to quickly release reserves. He also suggested the expectations of his colleagues by the end of 2016 that calls for Fed funds rates to be below 2% even when the job market is back to normal may be too low. This should come as no surprise - Plosser has tended to be wary of the Fed's accommodative stance. There is nothing here we don't already know. As it stands today, the Fed is comfortable with a steep yield curve. So all Plosser is telling us is that his inflation forecast differs from the FOMC as a whole, and if his forecast is realized, then policy will change accordingly. More interestingly, in a later speech Plosser challenged incoming Federal Reserve Chair Janet Yellen's preferred policy framework: What such framework would Plosser suggest? From 2010: So, if we have problems in measuring output gaps, what type of rule should we use? I believe it makes more sense to use an interest rate rule that responds aggressively to movements in inflation relative to a target and, if it responds to real economic activity, responds to a measure of the change in economic activity itself rather than some deviation from unobserved potential. But, but, but...why then is Plosser so hawkish? Inflation has been moving away from target, so it would seem that he should be taking a dovish stance. How exactly is he going to mount a challenge to a Yellen Fed's basic policy approach? By jointly arguing that policy is too loosely and suggesting a rule that, if followed, would loosen policy further? I am just not seeing it, and thus not seeing how Plosser would be effective in affecting Fed policy.

Fed Watch: How Divided is the Fed? - The minutes of the December 2013 FOMC meeting will be released Wednesday. I am looking for divisions within the FOMC on key topics, notably likely timing of the first rate hike, likely pace of rate hikes, and discussion of what follows the Evans rule. I am not so much concerned with the tapering process at this point. In my mind, that is now something of a dead issue. Barring any large shifts in the pace of economic activity, I think the Fed is largely committed to winding down that program this year. And I think that the Fed is likely committed to low interest rates through 2014. It's in the 2015 policy outlook that the real divisions start to show.As far as quantitative easing is concerned, I think the Federal Reserve is looking to end the program. Although they have not fully explained the calculus in the background, I think the cost/benefit analysis shifted against asset purchases. Moreover, the markets did not collapse after policymakers pulled the trigger on the taper, and everyone (all right, everyone but Boston Federal Reserve President Eric Rosengren) seems relatively comfortable with the pace at with asset purchases are expected draw to a close. Sure, arguably the hawks would like to see it brought to a close sooner than later, but are really just happy to see a path out, a clear indication that there is no such thing as QEInfinity.With regards to interest rates in 2014, here again I think the vast majority of FOMC members are comfortable with the idea that short term rates will most likely hold near zero for the remainder of the year. Even if the US economy receives a faster than expected burst of cyclical activity, the still large output gap and high unemployment rate suggest there is room to let the growth engine run on all cylinders for awhile This is especially the case given the inflation numbers. There is enough uncertainty about inflation, however, that I think the Fed will hesitate to lower the unemployment threshold.

This is the biggest challenge Janet Yellen will face as Fed chair - Two things are happening today in economic news. First, Janet Yellen is to be confirmed Monday evening to head the Federal Reserve. And second, Larry Summers, whom many of the president's advisers favored for the Fed post, published this buzzy op/ed in The Washington Post that sheds light on how he would be thinking about the economy, and monetary policy, if he were the one about to ascend to the big job. The timing is surely coincidence. But as it happens, the issues Summers analyzes in his piece amount to some of the most important questions that Yellen will have to wrestle with as Fed chair. Summers looks at the last 15 years or so of economic history and sees a disconcerting pattern. U.S. economic growth has been anemic -- even outside of the crisis years of 2008 and 2009, and despite years of low interest rate policies out of the Federal Reserve aimed at boosting the expansion. Summers's argument is that there are deeper problems afoot in the U.S. economy, and that so long as the Fed keeps trying to coax growth through easy money policies, without corresponding efforts by fiscal policymakers to increase demand in the economy or structural reforms to boost the country's longer-term economic potential, we are consigned to a cycle of endlessly expanding credit and asset bubbles. "If the United States were to enjoy several years of healthy growth under anything like current credit conditions, there is every reason to expect a return to the kind of problems of bubbles and excess lending seen in 2005 to 2007," Summers writes, "long before output and employment returned to normal trend growth or inflation picked up again."

White House nominates three in potential reshape of Fed - President Barack Obama may not get the chance to remake the composition of the Supreme Court but he'll get to do that at the Federal Reserve if his three eclectic nominees announced Friday are approved by Congress.Fresh on the heels of Monday's confirmation of Janet Yellen as the first woman ever to head the world's most influential central bank, Obama offered three more candidates to join the Fed's Board of Governors.In an unusual move that had been rumored for weeks, Obama nominated Stanley Fischer to join the Fed and be its vice chairman. What makes the pick different is that Fischer served as governor of the Bank of Israel from 2005 until last year, navigating that central bank during a time of global turmoil.Before that Fischer was vice chairman of Citigroup from 2002 to 2005, a time when many of the exotic financial instruments flourished that eventually caused the near collapse of the global financial system.The tenure at Citi might turn off some Democrats who decry the revolving door between the Treasury Department, Fed and Wall Street. .Obama also nominated Jerome Powell to continue serving as a Fed governor, a post he now holds. Powell was a partner in the private-equity firm The Carlyle Group from 1997 to 2005, and before that served as undersecretary of the Treasury Department during the presidency of George H.W. Bush. The only nominee without Wall Street ties was Lael Brainard, who served as Obama's Treasury undersecretary for international affairs from 2010 to 2013 and was involved in efforts to harmonize financial regulation across the globe. Prior to that she was a prominent economic researcher at the Brookings Institution and served as an adviser during the Clinton administration.

The Greatest Myth Propagated About The FED: Central Bank Independence (Part 1) - L. Randall Wray - It has been commonplace to speak of central bank independence—as if it were both a reality and a necessity. Discussions of the Fed invariably refer to legislated independence and often to the famous 1951 Accord that apparently settled the matter. [1] While everyone recognizes the Congressionally-imposed dual mandate, the Fed has substantial discretion in its interpretation of the vague call for high employment and low inflation. For a long time economists presumed those goals to be in conflict but in recent years Chairman Greenspan seemed to have successfully argued that pursuit of low inflation rather automatically supports sustainable growth with maximum feasible employment. In any event, nothing is more sacrosanct than the supposed independence of the central bank from the treasury, with the economics profession as well as policymakers ready to defend the prohibition of central bank “financing” of budget deficits. As in many developed nations, this prohibition was written into US law from the founding of the Fed in 1913. In practice, the prohibition is easy to evade, as we found during WWII in the US when budget deficits ran up to a quarter of GDP. It is, then, perhaps a good time to reexamine the thinking behind central bank independence. There are several related issues.First, can a central bank really be independent? In what sense? Political? Operational? Policy formation? Second, should a central bank be independent? In a democracy should monetary policy—purportedly as important as or even more important than fiscal policy—be unaccountable? Why? Finally, what are the potential problems faced if a central bank is not independent? Inflation? Insolvency? (also see The Greatest Myth Propagated About The FED: Central Bank Independence - Part 2)

The Real Scandal at the Federal Reserve - Many observers have been making the case that the zero lower bound (ZLB) on nominal interest rates is the reason for the ongoing economic slump. That is, because nominal interest rates cannot go below zero--it would pay more to hold cash so no one would lend at negative interest rates--they have not been able to fall to the level needed to clear output markets. The ZLB, therefore, is acting like a price floor that is artificially propping-up short-term interest rates and, as with any binding price floor, is creating a surplus. Implicit in this view is the belief that the short-term market-clearing nominal interest rate is negative. Many have a hard time believing this equilibrium or 'natural rate' value of the interest rate can be negative. Others might accept that it was negative in 2008-2009, but not five years later. The answer to this question would go a long ways in ending much confusion. If the answer is yes, then it would not be true that Fed has been 'artificially' suppressing interesting rates as many have claimed. Nor would it be true that the Fed has been enabling the large budget deficits with low financing costs for the treasury department. Finally, it would reveal that U.S. monetary policy has not been that loose despite the Fed's various QE programs. So why has the Federal Reserve not published real-time, monthly estimates of the short-run natural interest rate? The Fed has a huge research staff, lots of resources, and is capable of providing this important information. It should be a scandal that the Federal Reserve, an interest-rate targeting central bank, does not regularly publish the natural interest rate. One cannot intelligibly talk about the stance of monetary policy for an interest-rate targeting bank without first knowing the natural interest rate level.

A study of Financial Repression, part 3… How does it manifest? - Part 1, a basic model … Part 2, Is there evidence of financial repression in the US? When a central bank keeps its base interest rate low, financial repression can manifest. What changes do we see in the economy? And what happens when you combine low interest rates with a falling labor share? The natural real rate of interest is a balanced interest rate between saving and borrowing. Savers receive a real return on their money that matches real economic growth. and The real cost of borrowing money is balanced with real economic growth. There is “economic” balance when the current real interest rate equals the natural real interest rate. Yet, the current real interest rate does not always stay on the path of the natural real interest rate. In financial repression, the current real interest rate is below the path of the natural real interest rate, which has a positive slope with respect to the utilization of labor and capital, When the current real interest rate is below the natural real rate, savers receive less real return than what real economic growth would give, while borrowers pay less real cost than the true cost of growth. In effect there is an implicit transfer of funds from savers to borrowers. The lower return for savers subsidizes the cost of borrowing. Firms that want to borrow to increase productive capacity receive funds at lower real cost. Normal economic growth gives borrowers an instant profit over the cost of borrowing. Thus, investment in productive capacity is subsidized by savers. When interest rate policy enters the area of financial repression, productive capacity can increase faster.

When QE becomes decentralised - In a previous post we presented research by Willem Buiter, Citi chief economist and former BoE MPC member, which he conducted in the mid 2000s, into whether virtual currencies could be a useful mechanism for breaking through the zero-lower bound. The idea in many ways represents an evolved form of QE, in which differentiable units from dollars are pumped into the economy, inducing an effective negative interest rate on dollars due to the fact that there is less of the new currency in circulation than the established one. Seen from this light, the recent rise of private virtual currencies could can be seen as amounting to the market’s own endogenous version of QE. As we noted, even though Buiter was initially skeptical that such a policy could be more useful than taxing currency directly, by the time he penned this post at his FT Maverecon blog in 2009, he seemed to have warmed to the idea, advocating it as a serious option for dealing with the growing depressionary consequences of the banking crisis.Alas, Buiter’s suggestions were not taken too seriously at the time. It’s hard to imagine it now, but back in 2009 the idea of a virtual currency having any value whatsoever (whether issued by the state or by a private network) was a laughable matter — as was the very idea of alternative currency mechanisms. Five years on, however, the endogenous rise of virtual currencies seems to be providing Buiter with the last laugh. Indeed, in the context of Bitcoinmania, Buiter’s proposals look increasingly ahead of the curve.

No Recession in Sight With 98% of the Nation Expected to Expand - Breadth is perhaps my favorite analytical tool for measuring both financial market and economic health. Breadth is a great measure of underlining strength that can help identify shifts in trends before they become apparent. When the major market indexes were hitting new 52-week highs in October 2007 fewer and fewer individual stocks were hitting new highs and many were already in their own private bear markets. In the same vein, while the U.S. economy didn't officially slip into a recession until December 2007 many individual states within the nation had already slipped into recession months previous. This underscores the importance of not focusing solely on headline numbers like where the S&P 500 is trading or what the national GDP rate is. For a constant measurement of the stock market's breadth I track the data each week in my Friday's “Market's Bill of Health” report. For gauging the country's economic breadth I rely on the Philadelphia Fed's state leading and coincident indexes. This week the Philly Fed just released its State Leading Index for November which showed that 49 out of the 50 states are expected to see their coincident indexes grow over the next six months. With 98% of states expected to show growth over the next six months, the risk of a coming recession remains remote. Just look at the sea of green on the Philly Fed's State Leading Index map below, where only Alaska is expected to show contracting economic activity over the next six months. Of note, back in December of 2007 when the U.S. economy first slipped into a recession only 32 states were expected to show economic growth in the first half of 2008, as more than one third of the country was already in a recession. Clearly the present backdrop is bullish and does not offer any impending doom to the current economic expansion.

Vital Signs: ‘Oil’s Well’ for Fourth-Quarter GDP Growth -- Tuesday’s November trade deficit report shows the stark turnaround in the U.S.’s dependence on foreign oil. In dollar terms, imports of petroleum have fallen sharply over the past two years, while exports have surged. As a result, the U.S. trade deficit in oil has narrowed rapidly. The trade balance on other goods hasn’t shown the same improvement. In both nominal and price-adjusted terms, non-oil goods imports have grown faster than similar U.S. exports have over the past two years. That’s a reflection of faster economic growth in the U.S. which tends to pull in more imports while sluggish global growth has slowed the growth in demand for U.S.-made goods. Oil, however, matters greatly when it comes to trade flows. A steep drop in oil imports helped the total November U.S. trade deficit to narrow sharply to $34.3 billion, the smallest gap since 2009. Even after adjusting for price changes, the trade deficit so far in the fourth quarter is significantly less than its third-quarter average. After seeing the improving trade picture, economists have revised up their tracking of fourth-quarter real gross domestic product growth. Stephen Stanley, chief economist at Pierpont Securities, increased his estimate to a 2.3% annualized rate from 1.5% previous. Ian Shepherdson of Pantheon Macroeconomics now sees growth at 3% from 2.5%. And Goldman Sachs economists increased their GDP rate to 2.8% from 2.3%. The smaller trade gap is also a plus for the Federal Reserve. “The narrowing trade deficit should help power the final quarter to better growth than had been feared and that should give new Fed Chair Janet Yellen some wiggle room as she starts the tapering process,”

Deep Freeze May Have Cost Economy About $5 billion — Hunkering down at home rather than going to work, canceling thousands of flights and repairing burst pipes from the Midwest to the Southeast has its price. By one estimate, about $5 billion. The country may be warming up from the polar vortex, but the bone-chilling cold, snow and ice that gripped much of the country — affecting about 200 million people — brought about the biggest economic disruption delivered by the weather since Superstorm Sandy in 2012, said Evan Gold, senior vice president at Planalytics, a business weather intelligence company in suburban Philadelphia. While the impact came nowhere close to Sandy, which caused an estimated $65 billion in property damage alone, the deep freeze’s impact came from its breadth. “There’s a lot of economic activity that didn’t happen,” Gold said. “Some of that will be made up but some of it just gets lost.” Still, Gold noted his $5 billion estimate pales in comparison with an annual gross domestic product of about $15 trillion — working out to maybe one-seventh to one-eighth of one day’s production for the entire country. “It’s a small fraction of a percent, but it’s still an impact,” Gold said.

Of brains and balls: Nassim Taleb's macro bets - Nassim Taleb is a vulgar bombastic windbag, and I like him a lot. His books do a good job of explaining some deep, important finance ideas for a general audience. He has helped popularize the notion of "skin in the game". His trolling of economists is also good for some lulz (I particularly enjoyed his coinage of the term "macrobullshitters"). However, Taleb has a tendency to indulge in a little macrobullshitting of his own. In February of 2010, he advised everyone in the world to short Treasuries: As for Treasuries, “It’s a no brainer, every single human should short U.S. Treasury bonds,” said the hedge fund adviser and financial author. “So long as you see the picture of Larry Summers going to Davos, you have to stay short U.S. Treasuries for another year. It means they (the Obama administration) don’t know what’s going on,” Taleb said. “Every time you see the picture of what’s his name, (Federal Reserve Chairman Ben) Bernanke, and he still has that job, you have to run to make sure your position is active. So long as these two guys are in office, that’s the trade.” Taleb also recommends betting on hyperinflation using options to buy gold and silver and sell Treasuries. This could be regarded as sound trading advice. But the macroeconomics here is just atrocious (and not just because Taleb feigns not to know Ben Bernanke's name). In 2/2010 Taleb was predicting that the world had underestimated the danger of hyperinflation, and that the world would come to realize that the danger was bigger than it had thought, thus causing Treasury yields to spike and making a huge profit for anyone who shorted them. But history ruled against the inflationistas; even as more and more Quantitative Easing was announced, inflation stayed low and stable. In other words, people who think that "money-printing" and deficits lead to inflation were forced to rethink their entire worldview. But probably not before they did damage to the world economy, as John Aziz points out.

US inflation expectations hit eight-month high - FT.com: US inflation expectations have jumped to their highest since May, with central banks and investors seeking insurance against the prospect that a recovering American economy will stoke price pressures. Inflation expectations, as measured by the difference between yields on 10-year nominal Treasury notes and Treasury inflation protected securities (Tips), have risen to 2.28 per cent from a low of around 2.10 a month ago. Tips help insulate holders from the threat of rising prices, as their value increases when the seasonally adjusted consumer price index rises. In contrast, holders of fixed-rate bonds suffer as inflation erodes their value. Higher market expectations for US inflation comes after a tough year for the sector, with big investor outflows and a rare negative annual return characterising the asset class for 2013. US inflation fell last year, wrongfooting buyers of Tips who had expected accelerating consumer prices because of the Federal Reserve’s infusion of money into the financial system under its quantitative easing policy. As the new year has begun, modest exchange traded fund outflows are being outweighed by demand from foreign central banks and other long-term investors focused on seeking inflation protection as it is seen as being a buying opportunity in the wake of the asset classes’ underperformance in 2013.

Fed Likely Sent About $76 Billion to Treasury in 2013, Less Than 2012 - It’s well known that the Federal Reserve’s unconventional programs have been quite the boon to U.S. Treasury’s coffers. By the end of the month, we should know exactly how much the central bank deposited last year. But there’s no need to wait for the official announcement to get a pretty good idea of the profits the Fed sent to Treasury last year: about $76.3 billion, according to a Wall Street Journal analysis of daily Treasury statements. (The final tally the Fed releases later this month won’t exactly match, but it will be close.) That would be somewhat less than in 2012, when the central bank sent a record $88.9 billion to Treasury. The Fed is required to use its income to cover its operating expenses and send much of the rest to the Treasury’s general fund, where it is used to pay government bills and benefits. Much of the Fed’s income in recent years has come from the U.S. Treasury paying interest on government bonds purchased by the central bank. Fed Chairman Ben Bernanke has said that since 2009, the Fed has sent more than $350 billion to Treasury, about equivalent to the amount it had sent during the entire 18-year period before the crisis. Why has the Fed become such a money maker? Since the financial crisis and ensuing recession, the Fed has launched numerous bond-buying programs and other efforts aimed at stabilizing the financial system and later pushing down long-term interest rates to encourage growth. These programs have swelled the Fed’s portfolio of securities to more than $4 trillion by the end of 2013 from less than $900 billion before the crisis. The Fed is collecting a lot of interest on those assets.

In 2013, the Fed Showed Why Fiscal Policy is Still Important - Last April I had a piece in Wonkblog saying we’d get to see whether or not the expansion of monetary policy in fall 2012 would offset 2013 fiscal austerity. I concluded that it wasn’t looking too good at the start, that QE3 was a smart idea anyway (and should go further), and, most importantly, that a fiscal multiplier would be in effect, and we should run a larger deficit and cancel out things like the payroll tax cut while the economy is still fragile. It received a lot of responses at the time (see the endnotes here for a list). Recently, there’s been a wave of posts by Scott Sumner and David Beckworth calling me and others out, saying that the votes are in and it's a victory for the market monetarists, the team that said monetary policy would offset austerity in 2013 and fiscal policy wouldn't matter. (There have also been responses from Brad DeLong and Noah Smith.) I don’t see it. I’m willing to be convinced, but the two clearest tests I saw the market monetarists put forward in early 2013 have resulted in failure. Let’s go through them:

Economists Spar Over U.S. Recovery —Economists John Taylor and Larry Summers exchanged pointed words Saturday about the best approach to spurring the economic recovery. Mr. Taylor, of Stanford University, suggested that the slow recovery—and the economy’s downward trajectory during the 2007-2009 recession—was in part due to the movement of regulatory, monetary and fiscal policy toward “more discretion, more intervention and less predictability.” As examples of unusual policy steps surrounding the crisis, Mr. Taylor cited the government’s bailouts of financial institutions as well as the Federal Reserve’s bond-buying stimulus, known as quantitative easing. Monetary, fiscal and regulatory policy should “get back to regular order,” Mr. Taylor said, to permit growth to pick up. “Get rid of this QE stuff,” he advised, and return to “rules-based monetary policy.” Mr. Summers, of Harvard, said that extraordinary times call for extraordinary measures and not a blind perseverance on a given course that may have worked in the past. Mr. Summers was an adviser to President Barack Obama early in his first term, when a sweeping stimulus act was passed. Do I want my doctor to be “consistently predictable or responsive to” a particular health emergency, Mr. Summers asked. Better, he answered, to have a doctor “evaluating my condition and responding appropriately.” Mr. Taylor acknowledged that, “It’s great to have the all-knowing doctor,” but added that history bears out that the economy does better when policy is “predictable…and rules-based.”

Blame Polarization for Tepid Economic Growth? --There has been a running argument among economists on the extent to which uncertainty over U.S. government policy –taxes, spending and regulation – is a big reason the economy has been so distressingly sluggish.In a skirmish over the weekend at the annual meeting of the American Economic Association, Harvard’s Larry Summers challenged the case that uncertainty is a big problem: Do I want my doctor to be “consistently predictable or responsive to” a particular health emergency, he asked. Better, he answered, to have a doctor “evaluating my condition and responding appropriately.”Stanford’s John Taylor responded: “It’s great to have the all-knowing doctor,” but history bears out that the economy does better when policy is “predictable…and rules-based.”Now the leading advocates of the case that uncertainty over policy is hurting the economy — a band of academics from Stanford, and the University of Chicago – have come up with a new hypothesis: Political polarization is adding to the uncertainty that is hurting the economy.The partisan divide, they argue in a paper presented at the AEA meetings, leads consumers, businesses and investors to expect “more extreme policies, less policy stability and less capacity of policy makers to address pressing problems.” An index of policy uncertainty that these economists created from surveys of newspaper articles shows an increase in uncertainty over economic policy in recent decades that parallels the increase in various measures of political polarization, both in Congress and among voters. While the American system of checks and balances has long been seen as a way to produce stability because it tends to preserve the status quo, that isn’t always true – especially when something like a looming debt ceiling or an unsustainable budget deficit requires a change in the status quo.

Strategies for sustainable growth, by Lawrence Summers - Last month I argued that the U.S. and global economies may be in a period of secular stagnation in which sluggish growth and output, and employment levels well below potential, might coincide for some time to come with problematically low real interest rates. ...More troubling, there are signs of eroding credit standards and inflated asset values. If the United States were to enjoy several years of healthy growth under anything like current credit conditions, there is every reason to expect a return to the kind of problems of bubbles and excess lending seen in 2005 to 2007...The challenge of secular stagnation, then, is not just to achieve reasonable growth but to do so in a financially sustainable way. There are, essentially, three approaches. The first would emphasize ... deep supply-side fundamentals: the skills of the workforce, companies’ capacity for innovation, structural tax reform and ensuring the sustainability of entitlement programs. ...The second strategy, which has dominated U.S. policy in recent years, is lowering relevant interest rates and capital costs as much as possible and relying on regulatory policies to ensure financial stability. ...The third approach — and the one that holds the most promise — is a commitment to raising the level of demand...Secular stagnation is not inevitable. With the right policy choices, the United States can have both reasonable growth and financial stability. But without a clear diagnosis of our problem and a commitment to structural increases in demand, we will be condemned to oscillating between inadequate growth and unsustainable finance. We can do better.

Will the Real “Secular Stagnation Thesis” Please Stand Up - John Taylor - Last Thursday I published an oped in the Wall Street Journal criticizing the new “secular stagnation” view as put forth by Larry Summers in a talk at an IMF conference in November. The topic was also the focus of debate at a session in which Larry and I appeared over the weekend at the AEA meetings with Marty Feldstein, Dale Jorgenson, and Ed Prescott. At the heart of Larry’s thesis is the view that there has been a secular decline in the past decade in the “real interest rate that was consistent with full employment,” and that decline is what I addressed in the oped. (I also gave a paper at the meetings with my views on the subject.) In the meantime, Jared Bernstein decided that my oped was “worth a brief response” because it goes “after an argument that has resonated with many in recent weeks: secular stagnation.” A number of people have asked me about Jared’s response. But to my surprise, I see that he does not even mention the decline in the equilibrium interest rate which is at the heart of the view that Larry put forth. So Jared’s response has missed the main point of the argument between Larry and me, and I’m disappointed that there’s not much to respond to in that regard. Rather Jared seemed to be defending another secular stagnation thesis. I did not address this thesis in my oped. But in trying to defend it, Jared throws out several incorrect and misleading statements about my policy evaluation research.

Summers Calls for U.S. Fiscal Stimulus - An unusually weak and intractable U.S. economic recovery requires another dose of fiscal stimulus to have a fighting chance of being sustained, Harvard economist Lawrence Summers said Saturday. Mr. Summers, speaking at the American Economic Association meeting in Philadelphia, expanded on his notion that the economy is undergoing a period of “secular stagnation” where there are not enough good investment opportunities to enable full employment. “We may be doomed to oscillation between inadequate and slow growth and bubbly, unsustainable and problem-creating growth,” he said. “Fiscal consolidation in such circumstances is a step importantly in the wrong direction.” The situation requires “direct fiscal policy action,” Mr. Summers added. He suggested the Federal Reserve’s loose monetary policy risked creating asset bubbles and therefore could not be pushed much further to support the expansion. “If growth is rapid but associated with financial conditions that are on their way to becoming unsustainable, that in many ways is a corroboration of the line of argument I am presenting,” Mr. Summers said. “Given current conditions, and given current savings and investment propensities, growth wit

Is Larry Summers Right About 'Secular Stagnation'? - Larry Summers argument that the United States economy may be suffering from “secular stagnation,” first made at an I.M.F. conference in November, has focussed attention on just how disappointing America’s economic performance has been over the past decade, and has raised important policy questions that deserve to be widely discussed. Writing in the Washington Post earlier this week, Summers warned that relying on low interest rates to boost the economy for long periods “virtually ensures the emergence of substantial financial bubbles,” and he called for more public and private investment. Having written two books about bubbles, I’m sympathetic to the point that Summers is making, which is essentially a reiteration of the argument that Alvin Hansen and other American Keynesians put forward in the late nineteen-thirties and early forties. However, the way Summers framed the argument, in terms of interest rates, and, particularly, the “natural interest rate”—a concept borrowed from Knut Wicksell, a Swedish economist who lived around the turn of the twentieth century—has caused some unnecessary confusion. To try and clarify Summers’s thesis and illuminate its strengths and weaknesses, I’ll recast it in a way that should be more familiar: in terms of supply and demand.

Summers believes we can reduce bubbles with big budget deficits. - Here's Larry Summers: Last month I argued that the U.S. and global economies may be in a period of secular stagnation; in which sluggish growth and output, and employment levels well below potential, might coincide for some time to come with problematically low real interest rates. Since the start of this century, annual growth in U.S. gross domestic product has averaged less than 1.8 percent. The economy is now operating nearly 10 percent, or more than $1.6 trillion, below what the Congressional Budget Office judged to be its potential path as recently as 2007. And all this is in the face of negative real interest rates for more than five years and extraordinarily easy monetary policies. Lots of problems here. Monetary policy since 2008 has actually been the tightest since Herbert Hoover was President, if we use the criteria recommended by Ben Bernanke in 2003. Summers seems to believe that low interest rates mean easy money, but by that measure money must have been really tight during the German hyperinflation. If the United States were to enjoy several years of healthy growth under anything like current credit conditions, there is every reason to expect a return to the kind of problems of bubbles and excess lending seen in 2005 to 2007 long before output and employment returned to normal trend growth or inflation picked up again. I don't believe in bubbles, but excess lending is certainly possible given all the moral hazard built into our financial system.

More on Summers, Taylor, and Secular Stagnation - I appreciate the fact that John Taylor responded to my recent critique of his WSJ oped debunking the Summers’ thesis of secular stagnation. It’s also timely in that Larry has another piece on the issue that’s worth reading in today’s WaPo. With respect to John–we often disagree but I think we do so without being disagreeable–I didn’t think his response to me was…um…responsive. His main argument is that since I didn’t address the decline in the equilibrium interest rate, we’re talking past each other. …to my surprise, I see that [Jared] does not even mention the decline in the equilibrium interest rate which is at the heart of the view that Larry put forth. So Jared’s response has missed the main point of the argument between Larry and me, and I’m disappointed that there’s not much to respond to in that regard. I’m confuzzled. Both John and Larry (and myself and everyone else who talks about this) frame the issue in terms of weak output, high unemployment, low investment and the decline in potential GDP, even in the face of very low interest rates. John refers readers to a recent piece he wrote on the issue, in which the abstract begins: In recent years the American economy has been growing very slowly averaging only 2 percent per year during the current recovery. The result has been stagnant real incomes and persistently high unemployment. Summers’ oped today begins the same way, pointing to weak output and unemployment even in the face of very low rates. The interest rate point is diagnostic: a near-zero Fed funds rate since 2009 amidst this continued weakness leads Larry to worry about secular stagnation and John to worry about the ACA, Dodd-Frank, et al. No one, John included, denies the fact of the near-zero FFR and the weak recovery.

Secular Stagnation, Green Shoots or What? - Servaas Storm - The Obama administration and the mainstream media are now talking up an imminent recovery, perhaps even a modest boom. We’ve of course heard this many times before during the past five years — and there is no reason why we should be optimistic now. For one, Obama’s optimism stands in sharp contrast to the gloomy spectre raised by former Treasury secretary and key White House adviser Lawrence Summers in speeches made at a Brookings-Hoover conference in October, and then again at an International Monetary Fund conference in November 2013. Mr Summers fears the U.S. has entered a period of “secular stagnation” — a notion proposed by Keynesian economist Alvin Hansen back in the 1930s to explain America’s dismal economic performance—in which sluggish growth and output, and employment levels well below potential, coincide with a problematically low (even negative) equilibrium real interest rates even in the face of extraordinarily easy monetary policy. Summers believes that the negative equilibrium interest rate is caused by the so-called Global Savings Glut—U.S. banks are said to be flooded by the inflow of Asian capital which supposedly depresses the equilibrium interest rate. Initially Summers left the impression that not much could be done to get the economy out of this conundrum, even — somewhat guardedly — hinting at the need for another asset price bubble to restore growth. But in a Financial Times article of January 5, he has clarified his position, arguing that secular stagnation is not inevitable and can be undone by the right policies, essentially fiscal stimulus (in the form of public investment in “green” energy and infrastructure). It is no surprise that Mr Summers’ analysis has stirred up strong responses on the political right. It is easy to predict that these reactions will become even more antagonistic after his recent “coming out” on fiscal stimulus. The tenor of these responses is quite predictable: the pitiful recovery must be blamed on government failure.

The Austerity Flip-Flop -- On April 28, 2013 Paul Krugman clearly said that 2013 was a test of market monetarism: But as Mike Konczal points out, we are in effect getting a test of the market monetarist view right now, with the Fed having adopted more expansionary policies even as fiscal policy tightens. Yesterday (Jan 4, 2014) however, Paul Krugman, said:…I don’t take seriously the claims of market monetarists that the failure of growth to collapse in 2013 somehow showed that fiscal policy doesn’t matter.There are two obfuscations here. First, it wasn’t the market monetarists who established the test it was Konczal and Krugman who laid down the glove so Krugman is saying he doesn’t take his own (April) claims seriously. Second, in April Krugman did appear to take his claims seriously, perhaps because:…the results aren’t looking good for the monetarists: despite the Fed’s fairly dramatic changes in both policy and policy announcements, austerity seems to be taking its toll. Now that the results are in, however, Paul claims that compared to southern Europe American austerity wasn’t so bad or it was really bad but small enough to be offset by “other stuff”: But the ticker tape (April 27, 2013) suggests a much different emphasis (note also that here Paul names “other stuff’ and it is adding to the problem not subtracting): Even more amusingly, arch-Keynesian Paul Krugman now says we are approaching the long run! In a post titled What A Good Year Won’t Prove he says: If 2014 is a year of relatively good growth, you know that many people will take that as somehow refuting Keynesianism — hey, didn’t you guys predict that the economy would never recover without fiscal stimulus? No, we didn’t [the linked post, is from 2009]

How to Tell if Fiscal Policy Works - There is a raging debate in the econo-blogosphere concerning the effectiveness of fiscal policy when the economy is in a deep recession. This question is important because monetary policy loses much of its effectiveness in severe downturns. Why does monetary policy lose its effectiveness in deep recessions? As the economy enters a recession, the Fed responds by lowering the interest rate to stimulate the economy. For mild recessions, that is generally enough to turn the economy around. But in severe recessions even if the Fed lowers its target interest rate to zero – the zero lower bound as it is known – it is generally not enough to bring about a robust recovery. More stimulus is needed. The Fed can turn from traditional interest rate policy to non-traditional policies such as quantitative easing, but those polices do not have anywhere near the effectiveness of traditional interest rate policy and – as we’ve seen in the Great Recession – it is not enough to avoid a highly sluggish recovery. When monetary policy alone is not enough, can fiscal policy be used to provide the extra stimulus that is needed to propel the economy back toward full employment? In theory, the answer is yes. Modern macroeconomic models tell us that while fiscal policy is not a very effective policy tool during normal times, it is very effective at the zero lower bound. However, many observers have argued that the evidence suggests otherwise. Standard Keynesian analysis implies the sequester should have been a drag on the economy, they argue, but the economy did relatively well after the sequester was put into place. But this type of analysis cannot settle questions about the effectiveness of fiscal policy. To understand why, consider an example from economic history.

How Fiat Money Works - Warren Mosler tells a good story that shows how our economy works at its most basic level. Imagine parents create coupons they use to pay their kids for doing chores around the house. They “tax” the kids 10 coupons per week. If the kids don’t have 10 coupons, the parents punish them. “This closely replicates taxation in the real economy, where we have to pay our taxes or face penalties,” Mosler writes.So now our household has its own currency. This is much like the U.S. government, which issues dollars, a fiat currency. (Meaning Uncle Sam doesn’t have to give you something else for it. Say, like a certain weight in gold.) If you think through this simple analogy, all kinds of interesting insights emerge. For example, do the parents have to get coupons from their kids before they can pay them to do any chores? Obviously not. In fact, the parents have to spend their coupons first by paying their children to do chores before they can collect the tax. “How else can the children get the coupons they owe to the parents?” Mosler writes. “Likewise,” he continues, “in the real economy, the federal government, just like this household with its own coupons, doesn’t have to get the dollars it spends from taxing or borrowing or anywhere else to be able to spend them.” The government creates dollars. It doesn’t even have to print them. The vast majority of spending is simply done by adding electronic dollars to bank accounts. Therefore, the U.S. government can’t go bankrupt. It pays all its bills in U.S. dollars, of which it is the sole issuer. This sounds really obvious, but it is amazing how many people — even very smart people — forget this simple fact. They get hysterical about the fiscal deficit or the national debt. (This is not to say there aren’t bad consequences from issuing too many coupons, or from government spending in general.) The only way the U.S. government can default is if it chooses to do so.

Where is the Arithmetic in Rubin’s Financial Times Piece? - Brad Delong -- Right now the U.S. government can issue a 30-year inflation-protected maturity with a yield of 1.5% per year. Right now if the U.S. spends an extra $100 billion next year it gets $200 billion of increased real GDP and $67 billion of additional tax revenue next year, for $33 billion of additional debt and $500 million of additional annual debt interest in the further future. If $200 billion of additional GDP next year has a long-term boost to GDP of even 1/100 as large–either as extra workers set to work brush-up on their skills, as organizations and capital learn more about how to produce, or as greater corporate cash flow leads to productive private or as government purchases are diverted to productive public investment, the extra annual debt service is more than covered by extra taxes produced by higher potential output. Rubin says that stimulus is “no substitute for fiscal discipline”. But as long as interest rates and economic slack are at their current levels, stimulus is fiscal discipline. It is the failure to undertake fiscal stimulus right now that is long-run fiscal profligacy. Why doesn’t this arithmetic show up anywhere in Rubin’s piece?

Another Debt Ceiling Fight Is Coming Up - Wells Fargo economists John E. Silvia and Michael A. Brown sent out a note today titled, "Another Debt Ceiling Deadline." Yes, the debt ceiling is back and we're quickly approaching it. Congress has a few things to take care of in the next few weeks, including the omnibus spending bill, the farm bill and possibly an extension of emergency unemployment benefits. Soon after that, it will face its toughest challenge of the year when Democrats and Republicans will have to find a way to prevent us from defaulting. The deal to end the government shutdown in October raised the debt ceiling until February 7. After that, Treasury can employ extraordinary measures to extend the deadline even further. How long is still up in the air - it could come as soon as late February or as late as June depending on the amount Treasury collects in tax receipts. Either way, the debt ceiling is coming and Republicans have been making it very clear recently that they are gearing up for another fight. President Obama and Democrats are expected to employ the same strategy as they used last fall in refusing to negotiate whatsoever. They (rightly) don't believe that Republicans should be able to demand a ransom for raising the debt ceiling.

Republicans to lower the cost of raising the debt ceiling - In all likelihood the US debt ceiling will need to be raised no later than this coming March. The question now is whether we are going to see a repeat of last October's game of chicken. According to Deutsche Bank, the US sovereign CDS spread has stabilized, with market participants not anticipating a major disruption (note that US CDS is fairly illiquid with "lumpy" trading activity).The showdown in October, followed by the ugly rollout of the ACA Health Insurance Marketplace, has changed the political landscape. As a result, the Republicans' debt limit demands may have shifted away from the original "dollar-for-dollar" spending cuts requirement (the so-called “Boehner Rule” ). And the new ask may be considerably smaller. The Hill: - Mark McKinnon of Hill and Knowlton Strategies said the “equation is pretty clear." “When Republicans screw with the debt ceiling and threaten a government shutdown, their unfavorable ratings go up. When they talk about Obamacare, Democrats’ unfavorables go up,” he said. The GOP demands are likely to be small, a former top GOP aide now on K Street said. That’s because conservative lawmakers and Republicans feeling primary heat will be unlikely to back any debt-limit boost,meaning House Republicans will probably need some Democrats to come to their side. “Most Republicans see that the shutdown was a mistake, and that there is more pragmatism in dealing with the debt ceiling,” said strategist Ron Bonjean.

House GOP Introduces Stopgap Spending Bill - Conceding that negotiations on a broad government spending bill are unlikely to finish in time to meet a Wednesday deadline, House Republican leaders introduced a stopgap funding bill Friday to keep the government funded through Saturday Jan. 18, and allow more time for talks to wrap up. House Appropriations Chairman Hal Rogers (R., Ky.) said he expected negotiations on the broader funding bill to wrap up Sunday or Monday. Congress faces a Wednesday Jan. 15 deadline, when government funding runs out under the terms of the budget deal passed late last year. Mr. Rogers is negotiating agency-by-agency spending levels with his Senate counterparts to fund the government through Sept. 30, the end of the current fiscal year. Mr. Rogers expressed confidence that the deal will not be derailed by remaining differences–which other officials said were related to health-care funding, environmental policy riders and other issues.

Diagrams and Dollars: Modern Money Illustrated (Part 1) - The reason our current Congressional leaders are having such a difficult time with our National Budgeting process is because they’re trying to design a “building” based on an incorrect diagram. No matter how they add up the numbers, they seem incapable of devising a budget that builds America forward in a positive way. In fact, their budgetary efforts more closely resemble the actions of a wrecking crew than a construction team!Here is my best effort to construct the diagram it appears the Congressional leaders are presently trying to use. I’m putting it together, as best I can, from the story they tell us, every day, about the fiscal dilemmas they are struggling to resolve. This diagram is also powerfully reinforced by a news media spinning and reporting daily on the politician’s seemingly futile efforts: The main features of the diagram are two “pots” containing Dollars. One pot is labeled the Private Sector (PS). This is basically the national economy—businesses and corporations, families and foundations, state and local governments, etc. All the transactions that occur in the Private Sector (PS) pot add up to what is called the GDP (gross domestic product). The second “pot” is the Federal Government (FG), and the Dollars contained in this pot are SPENT to pay for public goods –weather forecasting, bridge repairs, Medicare services, etc.—and to make the “transfer” payments like social security, unemployment aid and food stamps that many Americans depend on to one degree or another. The diagram shows that the Dollars in the Federal Government (FG) pot are obtained via two spigots in the Private Sector (PS) pot: one spigot is TAXES, the other is the “BORROWING” spigot through which the Federal Government (FG) obtains Dollars by “selling” Treasury Bonds to the Private Sector.

Pay to Extend Unemployment Benefits? Why Not Pay to Extend Temporary Tax Breaks Too? -- In the battle over whether to extend long-term unemployment benefits, one of the Republican talking points is: Sure, we’ll consider an extension, but it must be paid for. That’s a fine idea. Here’s another: In exactly the same way, Congress should offset the cost of restoring dozens of temporary tax breaks that expired on Dec. 31 by raising other taxes. Here’s how Senate GOP Leader Mitch McConnell (R-KY) put it the other day: “There is no excuse to pass unemployment insurance legislation… without also trying to find the money to pay for it so we’re not adding to a completely unsustainable debt.” Now, simply substitute the phrase…expiring tax provisions…for… unemployment insurance. Why should the rule be different? Tax breaks are not the same, say some. But for the most part, these highly targeted subsidies are precisely the same. Most are nothing more than spending in drag. Just as the unemployment program transfers cash to a specific group, so do the scores of tax credits and other subsidies that some are hot to renew. Only the beneficiaries are different. Instead of the long-term unemployed, they are Manhattan real estate developers, auto racetrack owners, movie studios, distillers of Puerto Rican rum, multinational corporations, makers of alternative fuel vehicles, etc., etc., etc. Every year Congress mindlessly extends them. And simply adds to the deficit.

For the first time ever, half of the members of Congress are millionaires -- For the first time ever, half of US Congressmen, both Democrats and Republicans, are millionaires, according to figures from a group that examines the influence of money on politics. At least 268 of 534 lawmakers currently elected to the House of Representatives and the Senate had a net worth of $1.0 million or more in 2012, according to disclosures filed by all members of Congress. For a few, that figure went into the hundreds of millions — and the median net worth was just over a million, at $1,008,767, according to analysis by the Center for Responsive Politics at OpenSecrets.org. Median figures for Republicans and Democrats in the “millionaires club” are nearly equal, with Democrats edging just a bit ahead with $1.04 million compared to $1.0 million for Republicans.Charting the Decline in Service at the I.R.S. -- The national taxpayer advocate, the ombudswoman for the Internal Revenue Service, has released her annual report about the biggest issues facing the agency. One major concern that the advocate, Nina E. Olson, emphasized was declining customer service at the agency, driven by budget cuts. How much has the service declined? Here’s a chart showing the share of taxpayers who called wanting to speak with a customer representative and actually spoke to one (blue line), and the wait before reaching a representative (green bars):In fiscal year 2013, the I.R.S. answered only 61 percent of such calls, and the average wait was 17.6 minutes.

Time to abolish the corporate tax? - Yesterday we posted a blog looking at a New York Times editorial entitled Abolish the Corporate Income Tax, exposing many of the numerous fallacies and misunderstandings at the base of it. Forgive us for going on about this, but it is important. Now Citizens for Tax Justice in the U.S. has produced an article of their own, which complements ours and adds several more important points. It starts like this: Another year, another campaign to give even bigger breaks to corporations and claim that this will create jobs. In 2014, the campaign opened with a January 5 op-ed by Laurence Kotlikoff in the New York Times titled, “Abolish the Corporate Income Tax.” And it is a campaign: in the United States, the United Kingdom - everywhere, really. It's based on ideology, not practical realities. A U.S.-based correspondent to TJN, with many connections in U.S. tax circles, added in an e-mail yesterday: "Larry is a leading right-wing Boston U economist who is otherwise best known as a former Reagan Council of Econ advisor and a deficit hawk. He means well, but he is generally clueless when it comes to the Real World. Unfortunately his piece is only the latest in a crescendo of right wing voices calling for abolition in the US. And the idea is gaining traction in business circles." Our arguments yesterday - and CTJ's arguments to follow - illustrate that if you support the abolition of the corporate income tax you either have no idea what you are talking about, or you are a shill. We can't think of another explanation (apart from where you are a mix of both.)