Fed Prepares to Maintain Record Balance Sheet for Years - Federal Reserve officials, concerned that selling bonds from their $4.3 trillion portfolio could crush the U.S. recovery, are preparing to keep their balance sheet close to record levels for years. Central bankers are stepping back from a three-year-old strategy for an exit from the unprecedented easing they deployed to battle the worst recession since the Great Depression. Minutes of their last meeting in April made no mention of asset sales. Officials worry that such sales would spark an abrupt increase in long-term interest rates, making it more expensive for consumers to buy goods on credit and companies to invest, according to James Bullard, president of the Federal Reserve Bank of St. Louis. That “is a widespread view in parts of the Fed, I think, and in financial markets,” Bullard said in an interview last week. While he disagrees with that perspective, it “won the day.” The Fed is testing new tools that would allow it to keep a large balance sheet even after it raises short-term interest rates, a step policy makers anticipate taking next year. They would use these tools to drain excess reserves temporarily from the banking system.

FRB: H.4.1 Release--Factors Affecting Reserve Balances--June 12, 2014: Federal Reserve statistical release - Factors Affecting Reserve Balances of Depository Institutions and Condition Statement of Federal Reserve Banks

Fed’s James Bullard: Fed Is ‘Much Closer’ to Its Policy Goals - While he stopped short of calling for a change in policy, Federal Reserve Bank of St. Louis President James Bullard said Monday the time is fast approaching when the central bank may need to begin raising interest rates. “The macroeconomy is much closer to normal than it has been during the past five years,” and the Fed “is much closer to its goals” as a result, Mr. Bullard said. But at the same time, the stance of central bank monetary policy “is not close to pre-crisis levels” and remains at settings putting in place to deal with a flailing economy, the official said. Mr. Bullard did not say when he believes the central bank should commence ending the ultra-easy money policy stance that prevailed over recent years. But he noted central bankers face “a classic challenge” and added “the debate on this topic is likely to garner significant attention as the economy continues to improve during 2014.” Mr. Bullard’s comments came from a presentation prepared for a gathering held by Tennessee Bankers Association in Palm Beach, Fla. He spoke as U.S. monetary policymakers increasingly face big questions about the future. After a weak, weather-related start to the year, recent economic data have been pointing to continued growth and job gains. Inflation remains well under the central bank’s 2% target, but it has been rising back toward the level Fed officials want to see. The Fed is currently in the process of winding down its bond-buying stimulus program and officials have widely signaled that effort will be completed by the end of the year. The next issue Fed officials will likely have to deal with is what to do with the near zero percent short-term rate policy that’s been in place since the end of 2008. Most Fed officials reckon the first increase in interest rates will come some time in 2015. San Francisco Fed president John Williams, a close ally of Fed chairwoman Janet Yellen, said last month he doesn’t see rates rising until the second half of next year. New York Fed President William Dudley observed in late May rate increases lie well off in the distance, but added “no one knows” when the Fed will act. Meanwhile, Kansas City Fed leader Esther George, a persistent critic of the central bank’s easy money policies, wants to see rate increases follow shortly after the end of the bond-buying program.

Fed’s Rosengren: May Extend Taper Process To Reinvestment Buying - Federal Reserve Bank of Boston President Eric Rosengren said Monday the U.S. central bank might need to implement a second tapering of its bond-buying efforts. The central bank is steadily winding this process down and has signaled that as long as the economy plays out as officials expect, purchases that expand the size of the central bank balance sheet will be done by year’s end. Mr. Rosengren’s taper talk zeroed in on what happens after that. He speculated how the Fed could deal with its ongoing effort that takes the money from maturing Fed-owned bonds and buys new securities. The Fed does this to maintain the size of its balance sheet. The fate of the reinvestment regime becomes very important after the end of balance-sheet expanding bond buys, because its end would represent the first step in the process of raising short-term interest rates. “As the economy moved closer to the Federal Reserve’s 2% inflation target and full employment, there could be a gradual reduction in the reinvestment policy–which would allow for a predictable reduction in the size of the balance sheet,” Mr. Rosengren said in the text of a speech prepared for delivery before a gathering in Guatemala City. “A reduction in the balance sheet, when that becomes appropriate, could be implemented as a basically seamless continuation of the tapering program used for reductions in the purchase program,” he said. The Fed “could decide to reinvest all but a given percentage of securities on the balance sheet as they reach maturity, and increase that percentage at each subsequent meeting, assuming conditions allow.”

Fed’s Bullard Says Central Bank May Raise Rates Sooner Than Many Now Think - Federal Reserve Bank of St. Louis President James Bullard said Monday if the economy performs as he expects over the remainder of the year, it is likely the central bank will increase short-term rates earlier than most officials now expect. “If you get 3% growth for the rest of this year, if you get unemployment coming down below 6%, if you continue to have jobs growth at 200,000, if you continue to see inflation moving back up toward target, I think if we get to the fall of the year and all of those things are transpiring as I’m suggesting they will, that will change the conversation about monetary policy, and there will be more sentiment toward an earlier rate hike,” Mr. Bullard told reporters after a speech. The official noted that his present projection is the Fed will first increase what are near-zero percent interest rates sometime near the end of the first quarter of next year. But, he said that view is now somewhat in flux. Mr. Bullard spoke to reporters after delivering a speech on the economy to a gathering held by the Tennessee Bankers Association in Palm Beach, Fla. He weighed in as U.S. monetary policymakers increasingly face big questions about the future. After a weak, weather-related start to the year, recent economic data have been pointing to continued growth and job gains. Inflation remains well under the central bank’s 2% target, but it has been rising back toward the level Fed officials want to see.

Fed’s Tarullo Signals Short-Term Funding Market Requirement May Be Coming - —Federal Reserve Gov. Daniel Tarullo offered his strongest signal yet that a new requirement for the short-term funding markets widely used on Wall Street may soon be coming. Mr. Tarullo, who plays a central role in setting the Fed’s regulatory agenda, said, after reading accounts of the role short-term markets played in the financial crisis, a “broadly applicable” minimum margin requirement makes sense. “It’s a little hard, I think, to make a compelling case against doing something like that,” he said Monday in response to a question from the audience after a speech before the Association of American Law Schools. Mr. Tarullo has previously said the Fed is considering a margin rule. He made no explicit promises Monday that the Fed would take action, but made it clear he believes the Fed would be justified in doing so. Fed Chairwoman Janet Yellen has also said that rules targeting short-term funding could help mitigate risks to the financial system. Banks and many other financial firms, including non-banks that operate in the so-called shadow banking sector, use short-term funding transactions. Lenders holding large amounts of cash or low-risk securities use the markets to boost returns on those assets, while borrowers use those securities or cash to fund their operations, hedge or execute short sales. The transactions include repurchase agreements and securities-lending transactions and are valued in the trillions of dollars every day. Mr. Tarullo signaled he doesn’t believe such a requirement should be controversial. When banks borrow from the Fed, “we require haircuts on all the collateral presented to us,” Mr. Tarullo said. “It’s just good counterparty practice.” “Haircut” is another word for margin.

What If the Fed Has Created a Bubble? - Mohamed A. El-Erian - Macro-prudential regulation has been significantly enhanced in the aftermath of the global financial crisis. Authorities around the world have imposed higher and more intelligent capital requirements, required financial institutions to value their assets more conservatively and to hold more easy-to-sell assets, placed constraints on allowable risk-taking, insisted on more stable funding, and demanded greater provisions against bad loans. The more confident central bankers are in their macro-prudential approach, the greater their willingness to persist with stimulus policies today that could involve a bigger risk of financial instability down the road -- a trade-off that has been noted recently by Minneapolis Fed President Narayana Kocherlakota, Boston Fed President Eric Rosengren and former Fed Governor Jeremy Stein. Essentially, the Fed has been pushing stock and bond prices up to "bubblish" levels, in the expectation that they will inspire the kind of consumer spending, physical investments and hiring required to subsequently justify them. The hope is that the convergence will occur in the context of full employment and inflation near the Federal Reserve’s target of 2 percent. So far, though, the wedge between asset prices and economic reality remains large, as last week's juxtaposition of new stock-market highs and still-anemic wage-inflation data demonstrated. The danger is that the economic recovery will ultimately fail to validate artificially high asset prices, leading to significant financial instability and adverse “spillback” for the economy. The more comfortable the authorities are in their ability to counter -- and, if necessary, contain -- such potential instability, the greater their appetite for maintaining the stimulus that markets so love.

Fed’s Bullard Calls Out Ignoring Bubbles Developing “Under Our Noses,” So What About Now? - Yves Smith - It’s been astonishing to see members of the Fed in denial about their own handiwork, so when St. Louis Fed President James Bullard berates his fellow central bankers for their abject refusal to notice pre-crisis bubbles, it’s an all too rare departure from their usual insularity and willful blindness. Moreover, there’s one issue that Bullard mentions only obliquely that deserves more notice. Bullard specifically criticizes the way that the Fed decided to increase interest rates in the face of extreme spread compression in all credit markets in a measured, deliberate way. That well-signalled, cautious process in fact was part of a pattern of insulating investors as much as possible from losses, which of course simply encourages more recklessness. Many writers, including your humble blogger, have written at length about the Greenspan, and later Bernanke and presumed Yellen puts, that if financial markets got too upset, the Fed would ride in to their rescue. But that was not the only way the monetary authority over the years has shielded investors more and more from risk. An important article this past Sunday by John Coates in the New York Times explained how various Fed policies meant to increase the safety of the financial system were having the reverse effect. Key extracts: If we understand how a person’s body influences risk taking, we can learn how to better manage risk takers. We can also recognize that mistakes governments have made have contributed to excessive risk taking…. the Fed has pioneered a new technique of influencing Wall Street. Where before the Fed shrouded its activities in secrecy, it now informs the street in as clear terms as possible of what it intends to do with short-term interest rates, and when. Janet L. Yellen, the chairwoman of the Fed, declared this new transparency, called forward guidance, a revolution; Ben S. Bernanke, her predecessor, claimed it reduced uncertainty and calmed the markets. But does it really calm the markets? Or has eliminating uncertainty in policy spread complacency among the financial community and actually helped inflate market bubbles?…

Policy Rules When Money Still Matters - John Taylor - In an interesting recent paper and blog post “Money Still Matters,” Michael Belongia and Peter Ireland report new empirical results with relevance to monetary policy. They show that the Divisia index of the money supply (not M1 or M2) has effects on the economy over and above the effects of the short term interest rate. The results suggest that central bankers—as they look into alternative strategies for monetary policy—should consider some kind of money growth rate rule, at least as a supplement to the interest rate rules which have been the focus of research and practice for many years. I agree with this view, and have for a long time pushed back against the trend of central banks—including the Fed—to ignore money growth. In situations where the interest rate hits the lower bound or more generally in situations of deflation or hyperinflation, I have argued that central banks need to focus on a policy rule which keeps the growth rate of the money supply steady. In a 1996 paper, for example, I recommended that “Interest rate rules need to be supplemented by money supply rules in cases of either extended deflation or hyperinflation.”

Fed Fails To Stimulate Jobs, Declares Victory and Pulls Out - The seasonally finagled headline number for nonfarm payrolls for May increased 217,000. The consensus expectation of Wall Street conomists was for a gain of 220,000. This report was not too hot, not too cold but j-u-u-u-st right! The market loved it. The seasonally adjusted monthly gain equated to an annualized gain of roughly 2.6 million or 1.9%. Actual, not seasonally adjusted (NSA), nonfarm payrolls rose by 920,000 in May to a total of 139.2 million. The actual annual growth rate was +1.75%. The seasonally adjusted number slightly overstated the gain. However, the actual number was better than the 10 year average and slightly better than May 2013. On the surface it looked like a good number. However, I find the consistency of the growth pattern to be “strange”. The annual rate of change has been between 1.55% and 1.85% for more than 2 years. Excluding a brief bump in early 2012, that string has persisted since September 2011. Meanwhile, the Fed has grown its balance sheet by 38% over the past year, and stock prices have risen not quite 20%. Ben Bernanke’s theory was that stock price gains resulting from QE would stimulate jobs. After 5 years of massive Fed balance sheet expansion, it’s apparent that he was dead wrong. There’s not much trickling to the labor market, either in terms of jobs or labor income.

David Brat to Bernanke: Don’t Underestimate the Value of Protestants -- Ben Bernanke got it wrong because he forgot to account for God, or at least for the Protestant way of worshiping him. That’s the basic argument of David Brat, the Virginia Republican who toppled House Majority Leader Eric Cantor (R., Va.) Tuesday. In a 2005 paper, which he presented at an economics conference in Myrtle Beach, S.C., he took on Mr. Bernanke, the former Fed chairman, Fed governor, and former chairman of the White House Council of Economic Advisers.In the paper, titled “Is Growth Exogenous? Taking Bernanke Seriously (But How Can a Fed Guy Forget the Institutions)”, Mr. Brat waded into a debate among economists over the determinants of long-term growth with this conclusion: Mr. Bernanke’s work on economic growth overlooked the role that religious institutions–particularly Protestant ones–play in driving a country’s growth rates. In his argument against Mr. Bernanke, Mr. Brat draws on previous research titled “Economic Growth and Institutions: The Rise and Fall of the Protestant Ethic?” a 2004 paper in which he wrote that Protestantism “provides an efficient set of property rights and encourages a modern set of economic incentives” so “one might anticipate positive economic performance.” “Give me a country in 1600 that had a Protestant led contest for religious and political power and I will show you a country that is rich today,” he wrote.

Price Inflation and Wage Inflation - The figure below plots a pretty long time series of annual changes in the core PCE price index and the Employment Cost Index, a measure of nominal average compensation costs–wages plus benefits–faced by employers (and adjusted for employment shifts across industries). The core PCE has wiggled around between one and two percent for over ten years! (This has led some unenlightened souls to suggest to me that we must have been at full employment all those years…you know who you are!) But the comp measure is stuck at an all time low of around 2%, year-over-year. BTW, that’s about where overall (as opposed to core) inflation is running, implying flat real compensation growth–and this is the average. The forces of inequality tend to pull up the average relative to the median. This is not just an idle observation. There are those among us who have suggested that the Federal Reserve might be wise to factor nominal wage inflation, of lack thereof, into its thinking about wind-downs and liftoffs. Chair Yellen herself has said in the recent past: “the low rate of wage growth is, to me, another sign that the Fed’s job is not yet done” and ”low nominal wage inflation was also viewed as consistent with slack in labor markets.” The unemployment rate is biased down due to labor force exiters. Price growth is low and apparently “well-anchored.” We’re still a ways from full employment. All good reasons to considering adding wage trends (and I think the ECI is a strong candidate) to the mix of indicators guiding the Fed’s next move–or lack thereof!

There Is No Tradeoff Between Inflation And Unemployment - Anyone reading the regular Federal Open Market Committee press releases can easily envision Chairman Yellen and the Federal Reserve team at the economic controls, carefully adjusting the economy’s price level and employment numbers. The dashboard of macroeconomic data is vigilantly monitored while the monetary switches, accelerators, and other devices are constantly tweaked, all in order to “foster maximum employment and price stability." The Federal Reserve believes increasing the money supply spurs economic growth, and that such growth, if too strong, will in turn cause price inflation. But if the monetary expansion slows, economic growth may stall and unemployment will rise. So the dilemma can only be solved with a constant iterative process: monetary growth is continuously adjusted until a delicate balance exists between price inflation and unemployment. This faulty reasoning finds its empirical justification in the Phillips curve. Like many Keynesian artifacts, its legacy governs policy long after it has been rendered defunct.

Great Moderation 2.0 Seen Lasting by JPMorgan Until Fed Shifts - The calm that has descended on financial markets has longer to run if history is any guide. Having coined the phrase Great Moderation 2.0 to describe the lull back in April, JPMorgan Chase & Co.’s John Normand is comparing this moment to periods of tranquility over the past three decades. His findings suggest the quiescence is here to stay for a while, meaning investors may be lulled into taking ever-greater risks. The bank’s head of foreign-exchange and international-rates strategy in London characterizes low volatility in the currency market as when swings in the Group of 10 major currencies slip and stay below 7 percent on a trailing three-month basis. While that happened for 45 business days as of the end of last week, the average timeframe of similar episodes since the 1980s is 150 days. They ranged in length from three months when the Federal Reserve paused its easing of monetary policy in 2002 to almost two years during the so-called Goldilocks era of the late 1990s when the U.S. economy was neither too hot nor too cold.

Easy money: Even without the Fed, we are awash in cash - The question is why. Part of the answer is that the Fed is only one aspect of a world awash in capital. We are in the midst of a cycle with no end in sight, one characterized by a supply of money that might not be endless and is surely not infinite but which is showing no signs of waning. The result has been and likely will continue to be a world where capital thrives (pace Piketty) without any countervailing force. In this Golden Age of Capital, financial assets are in a prime position to thrive and have constant new sources of fuel. And there is nothing evident on the horizon—no backlash beyond rhetoric, no movement powerful enough to curtail or channel the flow of capital to labor—that will halt this movement. Just as the Fed has slowly begun a shift from very easy money to just easy money, other spigots around the world have opened. At the end of last week, the European Central Bank, led by its president Mario Draghi, announced its own version of quantitative easing, focusing less on the Fed’s approach of asset purchases and more on incentives to get banks to lend more. The central bank of China then unveiled a program designed to boost lending to small businesses. While the exact dollar amount of these measures is unclear, they represent a new injection of liquidity into a global system that has hardly lacked for it.

Amid Upbeat Economic News, Many Reasons for Pause - WSJ - In the teeter totter between good and bad economic news, developments in the U.S. are clearly titling up. The U.S. hit a new all-time jobs peak last month. The Dow is setting new records. On Tuesday, a measure of small-business confidence sounded its most optimistic note in seven years. There’s a notable surge in job openings.But economists are of a mind that it’s a bit early to celebrate. The champagne goblet is, at best, half full. Yes, the U.S. labor market has finally nosed above where it was before the recession and the financial crisis threw millions out of work. But the country since then has grown, and the proportion of Americans in the workforce has shrunk by nearly two percentage points. By another measure, the labor force participation rate, which measures those working or actively seeking work, is near its lowest level since the late 1970s. The makeup of the job market is also far different from what it was during the relative boom years before the housing bust. The fastest growing jobs, including a surge in temp and part-time jobs, are also among the lowest paying. At the same time, jobs in manufacturing, construction and government—all among the better paying of sectors— are off by 3.6 million from their levels at the start of 2009. The Labor Department reported Tuesday that the number of job openings in April had jumped to its highest level since 2007. In all, employers reported 4.45 million job postings for the month. But for some economists, those numbers highlight a bigger challenge. With so many job openings, how can the unemployment rate remain at 6.3%? One likely culprit: A lingering shortage of workers with the right skills to fill the needed jobs. Put another way, too few of those out of work, or newly entering the workforce, have the mix of skills employers want most.

The Economic Damage of Recession News - - Real gross domestic product (G.D.P.) in the United States shrank by 1 percent in the first quarter of the year. What made this announcement seem so significant? We already knew that the economy did not perform well in the first part of the year — the Commerce Department’s Bureau of Economic Analysis initially estimated G.D.P. growth at 0.1 percent — and that early economic estimates are often revised substantially as more data become available. The key difference is the direction of change. A shrinking economy is far more scary — and newsworthy — than a slow-growing one. In this case, the G.D.P. revision prompted a wave of coverage focusing on the fact that growth was negative. Distinctions like these matter. Consumers often overweight the importance of arbitrary thresholds like zero growth. That’s why used cars with just over 100,000 miles sell for significantly less than those with just under 100,000 miles. In the case of the economy, the arbitrary distinction between slightly negative and slightly positive growth can be especially consequential because a widely used rule of thumb defines a recession as two consecutive quarters of negative growth. The political scientists Andrew Eggers and Alexander Fouirnaies examined this effect in developed economies and found that consumer confidence and private consumption declined substantially in countries that narrowly experienced two consecutive quarters of negative growth relative to countries that just missed meeting the definition. These effects appear to be driven by media reporting portraying the country as being in recession, which causes consumers to downgrade their estimates of the state of the economy and adjust their spending accordingly.

U.S. Economy’s First-Quarter Contraction Could Be Even Worse Than You Thought -- The U.S. economy may have contracted more than previously thought during the first three months of 2014, private economists said Wednesday based on new health care-sector data from the government. Some analysts said economic output may have contracted at a 2% pace in the first quarter. That would be its worst performance since the recession. The Commerce Department’s latest estimate of gross domestic product, the broadest measure of output across the economy, said GDP shrank at a seasonally adjusted annual rate of 1% in the first quarter. A revised estimate will be released June 25, and it could show an even larger contraction. That’s based on the Commerce Department’s Quarterly Estimates for Selected Service Industries report for the first quarter, released Wednesday. It showed that revenue in the U.S. health-care and social-assistance sector fell 2% in the first quarter from the fourth quarter of 2013, not adjusted for seasonal variations or price changes. Hospital revenue fell a seasonally adjusted 1.3% from the prior quarter. The Commerce Department’s last GDP report, though, said inflation-adjusted spending on health-care services surged to a seasonally adjusted annual level of $1.848 trillion in the first quarter from $1.808 trillion in the fourth quarter of 2013. That estimate for spending on health care boosted overall GDP growth by 1.01 percentage point, keeping the 1% contraction from being even worse.

It Was A Reeeeeally Bad Winter: JPM Cuts Q1 GDP From -1.1% To -1.6% -- Remember when we reported that if it wasn't for Obamacare, the US economy would have contracted not by 1% as per the revised GDP estimate but by 2%. Guess what: according to the latest spending data, the BEA massively overestimated spending on medical care services, which it had pegged at a whopping +9.7% SAAR, while according to the latest Quarterly Services Survey, the increase was actually a decrease of 5.8% SAAR! End result: one after another bank today has sprung to revise their GDP data downward, by about half a percentage point, and here is JPM, cutting its Q1 GDP from -1.1% to -1.6%, which if realized will be the worst collapse in US economic growth since the recession.

Treasury Secretary Lew Warns of Lower Potential Economic Growth - WSJ: Congressional Budget Office Projects Average Growth Rate of Just 2.1% Going Forward. The U.S. could face a permanent downturn in economic growth without increased business investment, better job training and a push to rebuild the country's aging infrastructure, Treasury Secretary Jacob Lew warned Wednesday.In a speech to the Economic Club of New York, Mr. Lew said the U.S. growth rate is now projected to run a little above 2% a year, down from a 3.4% average from the end of World War II until 2007. If America can't maintain stronger growth, the country could face deepening challenges from sluggish labor market and widening inequality, he said. "The choices we make over the years to come can alter this projection," he said. Mr. Lew called on businesses to accelerate capital investment, noting the rate of spending on items such as buildings, equipment and software during the economic recovery has been considerably slower than the pace recorded in the 50 years before the recession began in 2007. "American businesses are sitting on historically high levels of cash," he said. "What we need now is for businesses—including many of you in this room—to come off the sidelines and make investments in our future."

SF Fed declares the ‘end of exceptional growth’ for America -- An unsettling forecast from America’s technology hub: “Productivity and Potential Output Before, During, and After the Great Recession” by John Fernald of the Federal Reserve Bank of San Francisco… Alan Greenspan in 2000 suggested that the economy was in the midst of a “once-in-a-century acceleration of innovation.” That hope has fallen short. For three of the past four decades, productivity growth has proceeded relatively slowly, suggesting this slower pace is the benchmark. … For now, the IT revolution is a level effect on measured productivity that showed up for a time as exceptional growth. Going forward, productivity growth similar to its 1973-95 pace is a reasonable expectation. The end of exceptional growth implies slower growth in potential output. But this fact does not mean that all the economy’s problems in recent years are structural or supply-related. After all, output gaps by any measure have closed very slowly despite substantial monetary accommodation. In other words, growth in aggregate demand has also been weak.Slower productivity and population growth also point towards a lower neutral real interest rate, which increases the challenges of providing sufficient monetary stimulus to close gaps. Uncertainty about any such forecast is inherently high. Jones (2002) argues that 20th century U.S. growth depended on rising education and research intensity. That is, maintaining growth required us to pedal ever harder and harder. That isn’t sustainable in steady state, so his model implies slower long-run growth.

U.S. Economic Recovery Looks Distant as Growth Lingers - Recessions are always painful, but the Great Recession that ran from late 2007 to the middle of 2009 may have inflicted a new kind of pain: an era of slower growth.It has been five years since the official end of that severe economic downturn. The nation’s total annual output has moved substantially above the prerecession peak, but economic growth has averaged only about 2 percent a year, well below its historical average. Household incomes continue to stagnate, and millions of Americans still can’t find jobs. And a growing number of experts see evidence that the economy will never rebound completely. For more than a century, the pace of growth was reliably resilient, bouncing back after recessions like a car returning to its cruising speed after a roadblock. Even after the prolonged Great Depression of the 1930s, growth eventually returned to an average pace of more than 3 percent a year. But Treasury Secretary Jacob J. Lew, citing the Congressional Budget Office, said on Wednesday that the government now expected annual growth to average just 2.1 percent, about two-thirds of the previous pace. “There are questions about whether America can maintain strong rates of growth and doubts about whether the benefits of technology, innovation and prosperity will be shared broadly.” The most recent recession and the slow recovery have “left lasting scars on the economy,” the Labor Department concluded late last year in a report that declared slower growth “the new normal” for the American economy. The Federal Reserve, persistently optimistic in its previous forecasts, said in March that it no longer expected a full recovery in the foreseeable future.

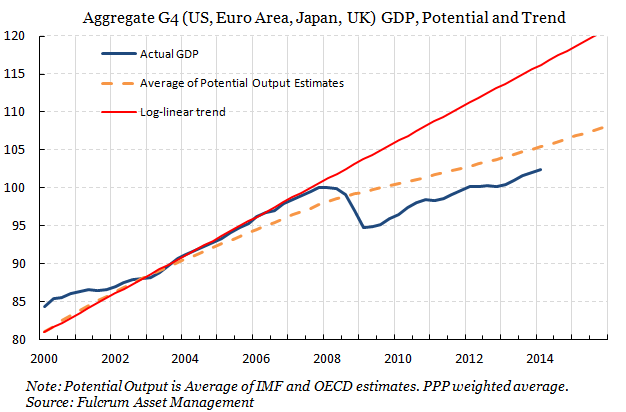

Still extrapolating the bubble - Economists and pundits continue to draw a line through the US GDP chart to show how the current growth is so far below trend (blue line below). Look, we are operating so much below capacity because of ... whatever it is that they want to complain about. Nonsense. The real trend is the red line. Extrapolating the “bubble era” trend is suggesting that the credit/housing bubble was the norm.

Last Time this happened, The Financial Crisis Broke Out - The Fed has a measure for it: the Financial Stress Index, issued by the St. Louis Fed. And according to the index, all this craziness, created by the Fed’s policies, is simply a sign of low “financial stress.” The data series goes back to 1993. The index is intended to be at zero, on average. Higher financial stress would show up with a positive number, lower financial stress with a negative number. And in the latest reporting week, ended May 30, the index fell to -1.281, the lowest in its history. The previous record low occurred in February 2007 at -1.268. A very unpropitious moment. The housing bubble was already imploding, but at the time, “the froth” was just coming off; it was “plateauing” before the next surge. Stocks were still going up on a relentless escalator. Merger Mondays were thrilling CNBC talking heads. Mega-LBOs were greeted with media hoopla even as leverage in the system skyrocketed. And malodorous fumes were already emanating from cracks that had appeared in the foundations of banks and other financial institutions. Bit by bit, these inconvenient issues were worming their way into the Financial Stress Index, and by August 2007, the index rose into positive territory, and even then it edged up only gradually, and it made it past the Bear Stearns collapse in early 2008 without much of a squiggle, but by August 2008, it was at +1.17 and by September 5, it was at +1.47, and then the Lehman moment happened, and suddenly, after having essentially ignored all the issues along the way, the index spiked every week until it peaked on October 17, at a phenomenal 6.27:

The Lack of Major Wars May Be Hurting Economic Growth - Tyler Cowen -- The continuing slowness of economic growth in high-income economies has prompted soul-searching among economists. They have looked to weak demand, rising inequality, Chinese competition, over-regulation, inadequate infrastructure and an exhaustion of new technological ideas as possible culprits.An additional explanation of slow growth is now receiving attention, however. It is the persistence and expectation of peace. The world just hasn’t had that much warfare lately, at least not by historical standards. ... Counterintuitive though it may sound, the greater peacefulness of the world may make the attainment of higher rates of economic growth less urgent and thus less likely. This view does not claim that fighting wars improves economies, as of course the actual conflict brings death and destruction. The claim is also distinct from the Keynesian argument that preparing for war lifts government spending and puts people to work. Rather, the very possibility of war focuses the attention of governments on getting some basic decisions right — whether investing in science or simply liberalizing the economy. Such focus ends up improving a nation’s longer-run prospects. ...

Is the lack of war hurting economic growth? - I have a new piece for The Upshot on that topic, here is one excerpt: Counterintuitive though it may sound, the greater peacefulness of the world may make the attainment of higher rates of economic growth less urgent and thus less likely. This view does not claim that fighting wars improves economies, as of course the actual conflict brings death and destruction. The claim is also distinct from the Keynesian argument that preparing for war lifts government spending and puts people to work. Rather, the very possibility of war focuses the attention of governments on getting some basic decisions right — whether investing in science or simply liberalizing the economy. Such focus ends up improving a nation’s longer-run prospects. It may seem repugnant to find a positive side to war in this regard, but a look at American history suggests we cannot dismiss the idea so easily. Fundamental innovations such as nuclear power, the computer and the modern aircraft were all pushed along by an American government eager to defeat the Axis powers or, later, to win the Cold War. The Internet was initially designed to help this country withstand a nuclear exchange, and Silicon Valley had its origins with military contracting, not today’s entrepreneurial social media start-ups. The Soviet launch of the Sputnik satellite spurred American interest in science and technology, to the benefit of later economic growth.

War is the Health of the GDP - The headline of Tyler Cowen's Upshot piece, "The Lack of Major Wars May Be Hurting Economic Growth" is calculated to provoke controversy. Cowen's point, though, isn't that we need a war to boost the economy. As he concludes: "Living in a largely peaceful world with 2 percent G.D.P. growth has some big advantages that you don't get with 4 percent growth and many more war deaths." But there is an underlying logic to Cowen's reductio ad absurdum that I'm not sure he grasps completely. The national income accounts were designed with the idea of paying for war in mind. That actually might make sense during a time of war when you're trying to figure out how to pay for it. But it embeds a social accounting protocol that is incompatible with the absence of war. The predictable results are policies such as the Cold War rearmament based on the premise that arms spending will pay for itself by siphoning off revenues from the additional growth that the spending will stimulate. The Latin term for it is inflatio. Time to recycle a piece from three years ago:

Treasury: Budget Deficit declined in May 2014 compared to May 2013 -- The Treasury released the May Monthly Treasury Statement today. The Treasury reported a $130 billion deficit in May 2014, down from $138 billion in May 2013. For fiscal year 2014 through May, the deficit was $436 billion compared to $626 billion for the same period in fiscal 2013. In April, the Congressional Budget Office (CBO) released their new Updated Budget Projections: 2014 to 2024. The projected budget deficits were reduced for each of the next ten years, and the projected deficit for 2014 was revised down from 3.0% to 2.8%. Based on the Treasury release today, I expect the deficit for fiscal 2014 to be lower than the current CBO projection. This graph shows the actual (purple) budget deficit each year as a percent of GDP, and an estimate for the next ten years based on estimates from the CBO.The deficit should decline further next year. The decline in the deficit, as a percent of GDP, from almost 10% to under 3% in 2014 is the fastest decline in the deficit since the demobilization following WWII (not shown on graph).

Will Congress "Pay the Bills" in 2015? -- I wrote several posts about the "debt ceiling" debate in 2011 and again in 2013. Unfortunately "debt ceiling" sounds virtuous, but it isn't - it is actually a question of "paying the bills". And I've always argued that Congress would "pay the bills". So even though the debate in 2011 clearly scared many Americans and impacted the economy, I was confident that Congress would eventually do its job. These political stunts always happen in off election years with the hope that most voters will forget about the nonsense by the next election. So there is a risk in 2015 - and right now I'm a little more concerned than in previous years. Most of the commentary concerning the upset of Congressman Eric Cantor has focused on immigration reform, but his opponent has also argued that the government should not pay the bills (default on payments to the American companies and people). This is an economic risk for next year (and a political risk for the GOP). As Republican Senator Mitch McConnell noted in 2011, if the debt ceiling isn't raised the "Republican brand" would become toxic and synonymous with fiscal irresponsibility.

What Eric Cantor’s Exit Means for Economic Policy - The surprising defeat of House Majority Leader Eric Cantor (R., Va.) this week in a primary election will have myriad political consequences in the coming weeks, but what will it mean for Congress’s approach to the economy? Mr. Cantor was often caught in the middle of the battle for the soul of the House GOP, leading conservatives in some fights and falling in line with leadership on others. These are some issues where his vacancy will be felt:

- 1.) The debt ceiling. Mr. Cantor was one of fewer than 30 House Republicans who voted in February to suspend the debt ceiling until 2015. The suspension was a calculated move by House Speaker John Boehner (R., Ohio) not to risk another fiscal standoff with the White House, following the government shutdown last year. The measure passed largely because of the support from Democrats, and it opened Mr. Cantor (and others in the GOP) up to criticism that they didn’t hold the line and demand budget changes to restrain the growth of the deficit.

- 2.) Reform Conservatism. A Mr. Cantor is essentially the GOP leadership’s spokesman when it comes to “reform conservatism,” which is an effort to frame conservative principles in a way that hits home with middle class voters. A number of Republicans, both centrists and conservatives, believe the party needs to do a better job reaching out to mainstream voters, and Mr. Cantor was trying to help shape the party’s image.

- 3.) Wall Street. China almost always emerges as a bipartisan punching bag during presidential elections, but Wall Street’s strawman reputation is growing. When House Ways and Means Committee Chairman Dave Camp (R., Mich.) proposed a new way of taxing financial companies a few months ago, the banking industry went bananas, enlisting many friendly Republicans to ensure the proposal never saw the light of day (it didn’t). But how much longer will they hold such sway? The professor who defeated Mr. Cantor in Tuesday’s primary, David Brat, seems to hold Wall Street banks in the same regard as Sen. Elizabeth Warren, the Massachusetts Democrat who dreamt up the idea of a consumer financial regulator. Will Mr. Brat’s disdain for Wall Street become contagious?

Companies Keeping Billions in Tax Havens - Apple: $36.4 billion; Microsoft: $24.4 billion; Citigroup: $11.7 billion. That's how much each company would owe in corporate taxes if they repatriated the more than $230 billion of profits they hold offshore, according to a report released Thursday from the Citizens for Tax Justice and U.S. PIRG. The report finds that 72 percent of Fortune 500 companies have subsidiaries in tax haven jurisdictions. The majority of those companies—307 out of 362—do not disclose the average tax rate they pay on offshore profits. But for the 55 that do, they pay an average rate of just 6.7 percent and would owe nearly $150 billion in corporate taxes if they repatriated the profits.That’s a massive amount of money and speaks to both the complexity of the U.S. corporate tax code and the extreme lengths companies will go to lower their tax bill. Apple, for instance, uses a subsidiary known as Apple Operations International (AOI) to hold most of its offshore profits, as a report from the Senate Permanent Subcommittee on Investigations explained last year. AOI is incorporated in Ireland, where the corporate tax rate is just 2 percent. Because of that, AOI avoids paying the U.S. corporate tax rate of 35 percent. But the Irish corporate tax code only applies to companies whose management and control reside in Ireland. It has nothing to do with where the entity is incorporated. Therefore, AOI’s management and control is not located in Ireland, so it avoids the Irish corporate tax as well.The Citizens for Tax Justice report shows that Ireland is the seventh most popular tax haven for Fortune 500 companies. You’ll see some other familiar names on the list: the Netherlands, the Cayman Islands, Bermuda and Switzerland.

The Fantasy that Tax Repatriation Can Pay for Highways (or anything else…) Like a bad penny, this tax repatriation idea just keeps coming back. You know, the one where you offer a bribe to multinational corporations in the form of a big tax cut to “repatriate” their foreign earnings. In this case, members on both sides of the aisle are conspiring to use this gimmick to replenish the nearly exhausted highway trust fund.My CBPP colleagues have pointed out many times over why this doesn’t work, but simply put: repatriation can’t pay for anything because it’s a big, fat revenue loser. The figure below shows the score of such a plan by the bi-partisan Joint Tax Committee. The first two bars show something like $20 billion initially flowing into the Treasury as foreign earnings are brought home at an 85% discount on the 35% corporate tax rate (that’s a tax rate around 5%: (1-.85)*.35). But after that, the temporary tax cut starts losing revenue, and for an interesting reason: multinationals ramp up their deferrals of foreign earnings (holding them overseas) in advance of the next tax holiday. The “holiday” terminology is interesting, btw, because a bunch of these alleged revenues have already been on holiday, sunning themselves in Caribbean tax havens.

New NBER Paper Analyzes Sales Tax on Services: A Wonkish Review --A recent National Bureau of Economic Research working paper assessing optimal sales tax policies has found that exempting some services (like health and education) from a hypothetical national sales tax would amount to only a 3 percent revenue loss. They also find that charging different rates on different categories of goods rather than a flat sales tax rate can improve society-wide “utility” (how well off people feel) by 30 percent for any given level of revenues.These findings are provocative. Sales tax base expansion to services is widely regarded as being a major revenue boost for states, and charging different rates on different goods is also widely regarded as ill-advised policy except in perhaps a few special circumstances. However, a look at the paper itself reveals that its claims, while totally reasonable within the paper’s context, need some bracketing.

OECD Urges Broad Tax Reform In U.S. - The U.S. should reform its tax code with “a degree of urgency” to overcome challenges to long-term economic growth, including an aging population and rising household inequality, the Organization for Economic Cooperation and Development said in a report Friday. The OECD said the U.S. recovery is solidly on track, if historically sluggish, and that the short-term outlook is favorable with a resurgent manufacturing sector and new energy development. But the country is facing long-term challenges—due largely to the retirement of baby boomers—that require sweeping policy reforms, according to the Paris-based think tank, which is backed by the 30 leading industrialized countries. Among a series of recommendations, the OECD said the U.S. should lower its corporate tax rate, eliminate tax loopholes that benefit businesses, and make the tax code more redistributive. The U.S. corporate tax rate of 39.1% is the highest of OECD countries, far above the average 25.5%. But loopholes in the code mean that the actual taxes businesses pay vary widely and enable some firms to avoid paying an share necessary for a stronger economy.

The Strange Fruit of the House’s Bonus Depreciation Bill - When the Ways & Means Committee sent the House a measure to make permanent extra-generous tax subsidies for firms that purchase capital equipment, I noted in passing that the bill included a provision extending “bonus depreciation” rules to fruit and nut trees. If I had read the bill more carefully, I would have noticed that while it applied to fruit that grows on trees and vines, it inexplicably excluded fruit that grows on bushes. As a blueberry lover, I am shocked and outraged. This job-killing exclusion also extends to raspberries—both black and red. Cranberries are more complicated. They usually grow on a bush, but sometimes a vine. So eligibility for the special tax break may depend on the variety of cranberry we are talking about. I suspect the bill has tax lawyers scrambling to find the broadest possible definition of tree. After all, there must be some bright-eyed legal associate out there who can make the case that a bush is nothing more than a short tree. Or a fat vine. Kudos to Bloomberg BNA’s Marc Heller for describing this foolishness. Marc reports that the fruit and nut amendment was added by Rep. Devin Nunes (R-CA), whose district includes growers of apricots, grapes, and almonds. But not, apparently, blueberries. Marc also noted that Michigan, the home state of Ways & Means chair Dave Camp, is a major producer of those blown-off blueberries. This may prove that Camp, whose tax reform plan would scrap bonus depreciation entirely in return for lower tax rates, is no hypocrite. Alternatively, after announcing his retirement, he may simply have lost interest in adding home-state goodies to the tax law.

Full Show: How Tax Reform Can Save the Middle Class | Moyers & Company - A report out this week finds that over 70 percent of Fortune 500 companies use offshore tax havens to avoid paying US taxes. In the second part of his interview with Bill, the Nobel Prize-winning economist Joseph E. Stiglitz says that such lucrative loopholes are contributing to America’s inequality problem and persistent unemployment rate. In fact, corporate greed, combined with a tax code too biased toward the very rich, is hurting our economy and reducing public investment at a time when we really need it. Stiglitz says it doesn’t have to be this way. He has a new plan for overhauling America’s current tax system, which he believes contributes to making America the most unequal society of the advanced countries. “We can have a tax system that can help create a fairer society,” Stiglitz tells Bill in the second part of their conversation. “Only ask the people at the top to pay their fair share. It’s not asking a lot. It’s just saying the top 1% shouldn’t be paying a lower tax rate than somebody much further down the scale – [they] shouldn’t have the opportunity to move money offshore and keep it in an unlimited IRA account.” Stiglitz believes that taxes should incentivize corporations to act in ways that benefit our country. “If your taxes say we want to encourage real investments in America, then you get real investment in America… But I also believe that you have to shape incentives and that markets on their own don’t necessarily shape them the right way.”

Rich got 14.6% richer in 2013 - Global private financial wealth grew by 14.6 per cent in 2013 to reach a total of $152 trillion, with the spike in stock prices helping to power the expansion, according to a study from Boston Consulting Group. Wealth is growing most quickly in the Asia-Pacific area, excluding Japan, where it expanded by 30.5 per cent in the year. The Asia-Pacific region is expected to overtake Western Europe in 2014 to become the second-wealthiest region and to beat out North America to become the wealthiest part of the world by 2018, the report said. The Boston Consulting Group has done an annual study of private wealth for the past 14 years, estimating the cumulative amount of cash and deposits, money market funds, and listed securities around the world. The study is meant to help pinpoint trends for the wealth management industry, including the increasing amount of wealth (28 per cent) invested in stock markets and the fact that the growth of private wealth was driven primarily by returns on existing assets.

The rich have advantages that money cannot buy - FT.com: Larry Summers - With the popularity of Thomas Piketty’s book, Capital in the 21st Century, inequality has become central to the public debate over economic policy. Piketty, and much of this discussion, focuses on the sharp increases in the share of income and wealth going to the top 1 per cent, 0.1 per cent and 0.01 per cent of the population. This is indeed a critical issue. Whatever the resolution of arguments over particular numbers, it is almost certain that the share of personal income going to the top 1 per cent of the population has risen by 10 percentage points over the past generation, and that the share of the bottom 90 per cent has fallen by a comparable amount. The only groups that have seen faster income growth than the top 1 per cent are the top 0.1 per cent and top 0.01 per cent. This discussion helps push policy in constructive directions. There is every reason to believe that taxes can be reformed to eliminate loopholes for the wealthy and become more progressive, while also promoting a more efficient allocation of investment. In areas ranging from local zoning laws to intellectual property protection, from financial regulation to energy subsidies, public policy now bestows great fortunes on those whose primary skill is working the political system rather than producing great products and services. There is a compelling case for policy measures to reduce profits from such rent-seeking activities as a number of economists, notably Dean Baker and the late Mancur Olsen, have emphasised. At the same time, unless one regards envy as a virtue, the primary reason for concern about inequality is that lower- and middle-income workers have too little – not that the rich have too much. So in judging policies relating to inequality, the criterion should be what their impact will be on the middle class and the poor. On any reasonable reading of the evidence starting where the US is today, more could be done to increase tax progressivity without doing any noticeable damage to the prospects for economic growth.

CEO Pay Continues to Rise - Economic Policy Institute - The 1980s, 1990s, and 2000s were prosperous times for top U.S. executives, especially relative to other wage earners and even relative to other very high wage earners (those earning more than 99.9 percent of all wage earners). Executives constitute a larger group of workers than is commonly recognized, and the extraordinary pay increases received by chief executive officers of large firms had spillover effects in pulling up the pay of other executives and managers.1 Consequently, the growth of CEO and executive compensation overall was a major factor driving the doubling of the income shares of the top 1.0 percent and top 0.1 percent of U.S. households from 1979 to 2007 (Bivens and Mishel 2013). Income growth since 2007 has also been very unbalanced as profits have reached record highs and, correspondingly, the stock market has boomed while the wages of most workers (and their families’ incomes) have declined over the recovery (Mishel et al. 2012; Mishel 2013). It is useful to track CEO compensation to assess how well this group is doing in the recovery, especially since this is an early indication of how well other top earners and high-income households are faring through 2013. This paper presents CEO compensation trends through 2013 and finds:

- Average CEO compensation was $15.2 million in 2013, using a comprehensive measure of CEO pay that covers CEOs of the top 350 U.S. firms and includes the value of stock options exercised in a given year, up 2.8 percent since 2012 and 21.7 percent since 2010.

- From 1978 to 2013, CEO compensation, inflation-adjusted, increased 937 percent, a rise more than double stock market growth and substantially greater than the painfully slow 10.2 percent growth in a typical worker’s compensation over the same period.

- The CEO-to-worker compensation ratio was 20-to-1 in 1965 and 29.9-to-1 in 1978, grew to 122.6-to-1 in 1995, peaked at 383.4-to-1 in 2000, and was 295.9-to-1 in 2013, far higher than it was in the 1960s, 1970s, 1980s, or 1990s.

Who Does Wall Street Own In Washington? - Last night we saw one of Wall Street's favorite politicians of the decade, Eric Cantor, destroyed by a random teabagger who railed against him endlessly for pushing through Bush's TARP bailout of the big banks. Just this cycle, the financial sector had contributed $1,396,450 to Cantor's mammoth campaign coffers. But grotesque bribery from Wall Street isn't just about Republicans. This is a list of the dozen most corrupted designated point persons for Wall Street in the House (since 1990):

• John Boehner (R-OH)- $9,797,914

• Eric Cantor (R-VA)- $8,492,465

• Spencer Bachus (R-AL)- $6,257,494

• Jeb Hensarling (R-TX)- $5,540,181

• Charlie Rangel (D-NY)- $5,376,743

• Ed Royce (R-CA)- $5,006,718

• Pat Tiberi (R-OH)- $4,702,881

• Steny Hoyer (D-MD)- $4,612,825

• Carolyn Maloney (D-NY)- $4,574,624

• Joe Crowley (D-NY)- $4,526,330

• Pete Sessions (R-TX)- $4,505,220

• Paul Ryan (R-WI)- $4,056,918

How ordinary Americans can influence policy – Recently, Benjamin Page and Gilens disturbed many Americans with their finding that “average citizens’ preferences have little or no independent impact on policy.” Their data suggest that the wealthy have 15 times the influence of the middle class. As remarkable as this conclusion is, many of the reporters discussing the study failed to read it carefully and missed other important findings. For example, Page and Gilens found that the preferences of elites actually correlate fairly well to the preferences of the average citizen (with a coefficient of 0.78, with 1.0 indicating exact alignment and –1.0 reflecting inverse correlation), whereas business groups have preferences that are far more divergent (–0.10). Public interest groups, such as unions and the American Association of Retired Persons, correlate slightly better with the interests of the average voter (0.12). However, pro-business groups, whose interests largely conflict with the average voter’s, have about nine times the influence as typical voters. In an e-mail, Page noted that the U.S. might get some “democracy by coincidence” — meaning that the preferences of the affluent for the most part align with those of the middle class — but such luck rarely occurs with the preferences of business groups. He also said that while his work with Gilens focuses on the top 10 percent of income earners, the top 1 percent and the top 0.1 percent may have even more influence and more divergent preferences as well. To fix these oligopolistic trends, we must turn to the states for ideas. Patrick Flavin may have some answers on this score. He has been using methods similar (although not entirely comparable) to those used by Gilens, Bartels and Page to test which states are most responsive to the interests of citizens. What he finds should give reformers hope: There are policies to strengthen the voice of middle class voters.

Why the Worst Get on Top – in Economics and as CEOs - William K. Black Libertarians are profoundly anti-democratic. The folks at Cato that I debate make no bones about their disdain for and fear of democracy. Friedrich von Hayek is so popular among libertarians because of his denial of the legitimacy of democratic government and his claims that it is inherently monstrous and murderous to its own citizens. Here’s an example from a libertarian professor based in Maryland.“[W]hen government uses its legal monopoly on coercion to confiscate one person’s property and give it to another, it is engaging in what would normally be called theft. Calling this immoral act “democracy,” “majority rule” or “progressive taxation” does not make it moral. Under democracy, rulers confiscate the income of productive members of society and redistribute it to various supporters in order to keep themselves in power. In order to finance a campaign, a politician must promise to steal (i.e., tax) money from those who earned it and give it to others who have no legal or moral right to it. There are (very) few exceptions, but politicians must also make promises that they know they can never keep (i.e., lie). This is why so few moral people are elected to political office. The most successful politicians are those who are the least hindered by strong moral principles. They have the least qualms about confiscating other peoples’ property in order to maintain their own power, perks, and income.

SEC commissioner calls on US regulators to end turf wars - FT.com: US regulators must end their turf wars, SEC commissioner Kara Stein said on Thursday, in a sweeping speech that criticised colleagues for falling behind on financial reforms. At the same time the Securities and Exchange Commission had to broaden its role in addressing systemic risks in the financial system, she said. In particular, Ms Stein said, regulators needed to rein in the financial industry’s reliance on short-term funding through securities lending and repurchase agreements, a sentiment that has been echoed by Federal Reserve governor Dan Tarullo, the Fed’s top policy maker on regulation. In the speech at the Peterson Institute for International Economics, Ms Stein also expressed her disappointment at the lack of progress in implementing parts of Dodd-Frank, as she continued to push regulators to be tougher on Wall Street when it comes to financial reform regulation. She has extra influence at the SEC as the most left-leaning member of the agency, counting Democrats on the Senate banking committee as her allies. Congress sets the SEC’s budget and can hold hearings on the agency. Ms Stein joined the SEC last year and was in Congress when the Dodd-Frank bill was passed in 2010. Since joining the commission, she has at times been critical of the agency now headed by former federal prosecutor Mary Jo White, including on whether banks admitting wrongdoing should be given access to capital markets without regulatory scrutiny. “Far too many of the substantive reforms mandated by the Dodd-Frank Act are not yet implemented,” Ms Stein said. “Many of the most important systemic risk reforms of Dodd-Frank just aren’t done.”

SEC Commissioner Kara Stein Declares War on SEC Chair Mary Jo White -- Yves Smith - A relatively new SEC Commissioner, Kara Stein, has decided to depart from the usual polite behavior regulatory overseers and is making noise about SEC decisions and policies that she finds to be dubious. The word most commonly used in the media about her remarks is “blistering”. But the press, while giving Stein’s unusually forthright speeches the attention they warrant, has either failed to notice or is pretending to miss what is really going on: Stein is taking on SEC chairman Mary Jo White on her finance-firm-friendly regulatory stance in a remarkably frontal manner.The reason that Stein’s outspokenness is so unusual is that it is almost unheard of for a regulatory supervisor to cross swords openly with an agency head who hails from the same party.And don’t think that Stein is merely making noise. Even though she’s only been in her post for roughly a year, she’s already having an impact. The final Volcker rule came out much tougher than the financial services industry expected, and insiders report that Stein played a significant role in those eleventh-hour improvements. Similarly, having a strong pro-regulation, pro-enforcement voice on the commission emboldens staffers in the SEC to be more vigorous in pursuing violations (contrary to popular opinion, many career staff members are keen to stamp out bad conduct. Too often, they are curbed by the more craven politicized division heads. One has to wonder, for instance, if the SEC’s Drew Bowden would have been as direct and specific as he was in calling out widespread abuses in the private equity industry in early May if Stein hadn’t paved the way for more blunt SEC public remarks.

The South Rises Up to Take on Wall Street and High Frequency Trading - Southern states are mad as hell and aren’t going to take it any more. After more than five years of watching their cities and towns suffer foreclosure and mortgage abuse from the biggest firms on Wall Street, rigged Libor swaps impoverishing local governments, and massive stock losses to municipal workers’ pensions, the South is rising up and suing Wall Street over its latest fleecing scheme – high frequency trading. And before anyone starts to chuckle about the chances of Southern lawyers outfoxing the mega Wall Street law firms in their own stomping ground in the U.S. District Court for the Southern District of New York, you should know this one salient detail: one of the key Southern lawyers involved is Michael Lewis. That’s not bestselling author Michael Lewis; that’s Big Tobacco Cartel suing and winning lawyer Michael Lewis who mightily assisted in bringing the tobacco cartel out of the shadows and changed the health of a Nation forever. Even more problematic for Wall Street and its hideously shrewd lawyers is that one of the smartest programming brains in U.S. markets, Eric Hunsader, is cooperating with the Southern lawyers. (Wall Street On Parade has previously written about Hunsader here and here.)

US Chamber of Commerce voices concern over potential BNP fine - FT.com: The US Chamber of Commerce, the powerful American business lobby, has voiced concern about the potential scale of a fine on French bank BNP Paribas by US regulators, echoing anxious demands by the French government for moderation. Speaking in Paris, Myron Brilliant, head of international affairs for the USCC, said the Chamber might “weigh in” on the issue if BNP was hit by “excessive” penalties for breaking US sanctions on doing business with Iran, Sudan and Cuba. “We worry about actions by government and other entities that could undermine the business environment and create uncertainty,” Mr Brilliant told the Financial Times. “We do not want to see a chilling impact on investment into the US.” His comments reflect the USCC’s longstanding concerns about the effects of regulation and litigation on business. Yet they also hint at concern that the BNP case could damage the prospects of a new transatlantic trade deal for which the USCC has been one of the most devoted advocates. BNP is currently negotiating the terms of a settlement in the case, with US regulators reported to be considering a fine of up to $10bn against France’s biggest bank by market capitalisation, along with a possible temporary bar on dollar clearing. President François Hollande raised the issue with Barack Obama at a meeting in Paris last week. But his appeal was brushed aside in public by the US president, who said he could not intervene in judicial cases.

Exclusive - U.S. using JPMorgan penalty to speed cases against other banks (Reuters) - The U.S. Justice Department is spending some of the $13 billion (7.74 billion pounds) JPMorgan Chase & Co agreed to pay to settle claims stemming from mortgage misdeeds to speed up similar punishments against other lenders, possibly including Bank of America Corp and Citigroup, according to people familiar with the matter. U.S. Attorney's offices that have been among the most active in probing banks over the toxic loans they bundled into mortgage securities and sold to investors have received funds to hire new civil prosecutors, the people said. U.S. Attorneys in New Jersey, Colorado and the Eastern District of California, based in Sacramento, are among those most experienced in pursuing the probes, the people said. The increased activity is a sign that President Barack Obama is trying to follow through on his 2012 pledge to hold more banks accountable for their role in the housing crisis, after prosecutors faced criticism for little high-profile action. Attorney General Eric Holder has also expressed a desire to wrap up more of mortgage securities-related cases this year. "There is a widespread recognition that the banks have not yet been held fully accountable for their origination practices and the harm that did to borrowers, investors and the American economy in general," said Don Hawthorne, a partner with Axinn, Veltrop & Harkrider in New York who has represented clients in mortgage-backed securities litigation.

Citigroup Said to Face $10 Billion Request in U.S. Talks - The U.S. Justice Department has asked Citigroup Inc. (C) for more than $10 billion to settle a probe into the lender’s sale of mortgage-backed bonds before the 2008 financial crisis, a person familiar with the negotiations said. Prosecutors broke off talks with Citigroup on June 9 and are preparing to sue the New York-based bank after it offered less than $4 billion to resolve the matter, said the person, who asked not to be named because the discussions are confidential. The Justice Department could file a lawsuit as early as next week, according to the person, who also said the bank’s offer included about $1 billion in cash and the rest in consumer relief.

Bank of America Shocker: New Commercial Loan Plunge Is Largest Since Lehman - A shocker from Bank of America: "The number of new commercial loans made by BAC has declined notably over the first half of the year. Measured as an indexed level to cycle peak (which was December 2005), the data show that the recent drop was the largest since the recovery began." Oops. If this is accurate then not only is the Fed fabricating loan data outright, it is massively misrepresenting the general direction of loan creation altogether. In fact, if loans are contracting, when one adds the decline in reserve "asset" creation, then banks are set for a world of pain come October when QE is set to end!

Why fix banks? - Do we need banks? Frances raises this question. She says: Lack of spending in an economy (shortage of aggregate demand) is caused by distributional scarcity of money, not by lack of loans. It is not necessary to restore lending in order to encourage spending. It is necessary to replace the money that is not being created by banks. She's right. The famous "helicopter drop" - more realistically, a money-financed fiscal expansion - might well* do more to boost aggregate demand than measures to boost credit supply such as the Funding for Lending Scheme or "targeted" LTROs. But this poses the question. If governments can bypass banks by simply printing money, why bother to fix the banking system at all? Why not just let it be a dysfunctional casino? The question gains force from the likelihood that, in practice, measures to improve bank lending are in effect subsidies to bankers. I suspect that the reason bank shares did so well after the ECB's announcement last week isn't so much that investors are looking forward to a brighter economic future, but simply that LTROs are yet more hand-outs. There is, though, an answer here. It's not that helicopter money would be inflationary; in the euro area, higher inflation is something to be desired. Nor is it much of a problem that such a policy would create a merely "artificial" boom; I've always been irritated by Austrians' tendency to dismiss some economic actions as less genuine than others in violation of Hayek's justified warnings about the boundedness of individual knowledge.

Economist: U.S. Banks Preparing to Charge Customers For Deposits -- In the week that the European Central Bank cut its deposit rate for banks from zero to -0.1%, economist Martin Armstrong warns that negative interest rates are coming to the United States, meaning that Americans will be forced to pay just to keep their money in the bank.Armstrong, who is noted for calling the 1987 economic crash to the very day, warns that U.S. banks are preparing a raft of new account fees that will serve as a de facto negative interest rate. “In the USA, we are more-likely-than-not going to get the negative rates directly passed to consumers by the banks who will claim it is the Fed who will do so at the requests of the banks. Larry Summers has set the stage. This is just how it works. He flew the balloon to get everyone ready. This is likely to be bullish for the stock market,” writes Armstrong, noting that, “The talk behind the curtain is to impose negative interest rates on the consumer.”

Bank Failure, Relationship Lending, and Local Performance - Whether bank failures have adverse effects on local economies is an important question for which there is conflicting and relatively scarce evidence. In this study, I use county-level data to examine the effect of bank failures and resolutions on local economies. Using quasi-experimental techniques as well as cross-sectional variation in bank failures, I show that recent bank failures lead to lower income and compensation growth, higher poverty rates, and lower employment. Additionally, I find that the structure of bank resolution appears to be important. Resolutions that include loss-sharing agreements tend to be less deleterious to local economies, supporting the notion that the importance of bank failure to local economies stems from banking and credit relationships. Finally, I show that markets with more inter-bank competition are more strongly affected by bank failure.

Unofficial Problem Bank list declines to 495 Institutions - This is an unofficial list of Problem Banks compiled only from public sources. Here is the unofficial problem bank list for June 6, 2014. It was a very quiet week for the Unofficial Problem Bank List with only one removal. The list holds 495 institutions with assets of $153.9 billion. A year ago, the list had 923 institutions with assets of $355.7 billion. The OCC terminated the action against Independence National Bank, Greenville, SC ($97 million Ticker: IEBS). Next week, we anticipate for the OCC to provide an update on its enforcement action activity through mid-May 2014. Note: The first unofficial problem bank list was published in August 2009 with 389 institutions. The list peaked at 1,002 institutions on June 10, 2011, and is now down to 495.

The Biggest Policy Mistake of the Great Recession - The popular conception of the Great Recession explains that it stemmed from a financial shock. Housing prices stopped going up, and then Lehman Brothers fell, triggering paralysis in the credit markets. This spilled onto Main Street, and the effects still linger in terms of elevated unemployment and sluggish economic growth. But this history of the recession can’t be right, say two economics professors who have studied the data. In their new book House of Debt, Amir Sufi of the University of Chicago and Atif Mian of Princeton point out that consumer purchases dropped sharply well before the September 2008 Lehman bankruptcy, and most deeply in places where home prices fell the most. They found that steeper declines in net worth — many homeowners were completely wiped out by falling home prices — led to far sharper reductions in consumer spending, and bigger job losses. But even those with no debt suffer when fire-sale foreclosures drop home prices, and lower overall demand spreads out across the country. By reviewing other economic downturns, Mian and Sufi discover two recurring features: a buildup of household debt before the crash, and an extreme decline in consumer spending afterward, as households cut back, hoarding money to pay off those scaled-up debts. The normal channels of fiscal and monetary policy have difficulty dealing with highly leveraged household balance sheets. House of Debt correlates these features of recessions, and really targets debt as the core problem, arguing that it needs to be restructured during crises and prevented during better times.

Larry Summers' Attempt to Rewrite Cramdown History - Larry Summers has a very interesting book review of Atif Mian and Amir Sufi's book House of Debt in the Financial Times. What's particularly interesting about the book review is not so much what Summers has to say about Mian and Sufi, as his attempt to rewrite history. Summers is trying to cast himself as having been on the right (but losing) side of the cramdown debate. His prooftext is a February 2008 op-ed he wrote in the Financial Times in his role as a private citizen. The FT op-ed was, admittedly, supportive of cramdown. But that's not the whole story. If anything, the FT op-ed was the outlier, because whatever Larry Summers was writing in the FT, it wasn't what he was doing in DC once he was in the Obama Administration. Let's make no bones about it. Larry Summers was not a proponent of cramdown. At best, he was not an active opponent, but cramdown was not something Summers pushed for. Maybe we can say that "Larry Summers was for cramdown before he was against it." Here's a telling paragraph from a National Journal article by Stacy Kaper called, The 'Cramdown' Fix Was Out, from Mar. 22, 2012. (in Lexis): William Longbrake, a former vice chairman with Washington Mutual who joined the Obama transition team in early 2009, recalls an administration divided over cramdown. "My sense is that Larry Summers probably ultimately brokered the solution," said Longbrake, now an executive in residence at the University of Maryland. "It was decided, but never publicly announced, sort of like, ‘Well, we are not going to oppose it, but we are just not going to support it.' … and then, ultimately, it died."