FRB: H.4.1 Release--Factors Affecting Reserve Balances--July 10, 2014 - Federal Reserve Statistical Release: Factors Affecting Reserve Balances of Depository Institutions and Condition Statement of Federal Reserve Banks

FOMC Minutes: QE3 Expected to End in October - From the Fed: Minutes of the Federal Open Market Committee, June 17-18, 2014. Excerpt: Some committee members had been asked by members of the public whether, if tapering in the pace of purchases continues as expected, the final reduction would come in a single $15 billion per month reduction or in a $10 billion reduction followed by a $5 billion reduction. Most participants viewed this as a technical issue with no substantive macroeconomic consequences and no consequences for the eventual decision about the timing of the first increase in the federal funds rate--a decision that will depend on the Committee's evolving assessments of actual and expected progress toward its objectives. In light of these considerations, participants generally agreed that if incoming information continued to support its expectation of improvement in labor market conditions and a return of inflation toward its longer-run objective, it would be appropriate to complete asset purchases with a $15 billion reduction in the pace of purchases in order to avoid having the small, remaining level of purchases receive undue focus among investors. If the economy progresses about as the Committee expects, warranting reductions in the pace of purchases at each upcoming meeting, this final reduction would occur following the October meeting.

Fed Sets October End for Bond Buying - WSJ - Federal Reserve officials agreed at their June policy meeting to end the central bank's bond-buying program by October, closing a chapter on a controversial experiment in central-banking annals with results still the subject of immense debate. Officials have been winding down their purchases of Treasury bonds and mortgage-backed securities in incremental steps since January and have said they expect to end the program later this year, but until now haven't been explicit about the end date. "If the economy progresses about as the [Fed] expects, warranting reductions in the pace of purchases at each upcoming meeting, this final reduction would occur following the October meeting," the Fed said in minutes released Wednesday from its June policy meeting. The bond program aims to hold down long-term interest rates and drive investors into riskier holdings like stocks or corporate debt. That in turn is meant to stimulate borrowing, lending, spending, investing and hiring. Critics have long argued the program risks causing another financial bubble or excessive inflation, without giving an obvious boost to hiring. Fed officials and other supporters of the program argue it has helped the economy grow faster than it would otherwise grow, with limited risk.

Fed Watch: QEInfinity Not - The Federal Reserve released the minutes of the June FOMC meeting today, but the contents had little in the way of groundbreaking news. Most interesting was that Fed officials tired of being pestered about the "October or December" question regarding the end of the QE and decided to more or less commit to the earlier date:Some committee members had been asked by members of the public whether, if tapering in the pace of purchases continues as expected, the final reduction would come in a single $15 billion per month reduction or in a $10 billion reduction followed by a $5 billion reduction. Most participants viewed this as a technical issue with no substantive macroeconomic consequences and no consequences for the eventual decision about the timing of the first increase in the federal funds rate--a decision that will depend on the Committee's evolving assessments of actual and expected progress toward its objectives.In other words, who cares about that last $5 billion? The Fed's answer was to take away the mystery:In light of these considerations, participants generally agreed that if incoming information continued to support its expectation of improvement in labor market conditions and a return of inflation toward its longer-run objective, it would be appropriate to complete asset purchases with a $15 billion reduction in the pace of purchases in order to avoid having the small, remaining level of purchases receive undue focus among investors. with, of course, the usual "data dependent" caveat. Thus the predictions of QE Infinity come to an end.

The Federal Reserve is Not Ending Its Stimulus - Yesterday, the Federal Reserve confirmed that it would end new purchases of Treasury bonds and mortgage-backed securities (MBS)—what’s known as quantitative easing—in October. In response, the media are heralding the end of the Fed’s stimulus:“Fed Stimulus is Really Going to End and Nobody Cares,” says the Wall Street Journal.“Federal Reserve Plans to End Stimulus in October,” reports the BBC. This is utterly wrong.What the Fed is about to do is stop increasing the amount of stimulus it provides. For the mathematically inclined, it’s the first derivative of stimulus that is going to zero, not stimulus itself. For the analogy-inclined, it’s as though the Fed had announced (in more normal times) that it would stop cutting interest rates. New stimulus is ending, not the stimulus that’s already in place. The Federal Reserve has piled up more than $4 trillion in long-term Treasuries and MBS, thus forcing investors to move into other assets. There’s great debate about how much stimulus that provides. But whatever it is, it will persist after the Fed stops adding to its holdings.

Divide on Inflation Views Growing at the Federal Reserve, Minutes Show - Minutes from the Federal Reserve’s June meeting suggest there is a growing gap between officials who believe U.S. inflation could remain too low for the Fed’s comfort and those who believe a spike in consumer prices could be closer than forecasters think. Some policy makers “expressed concern about the persistence of below-trend inflation,” the minutes said. Indeed, a couple even suggested the central bank might have to let unemployment fall below its long-term normal rate in order to ensure inflation moves back toward the 2% target. That sentiment was far from unanimous, however. “Some others expected a faster pickup in inflation or saw upside risks to inflation expectations because they anticipated a more rapid decline in economic slack.” The divergence may help explain why Fed officials are concerned the historically low volatility seen in financial markets of late suggests investors may be underpricing risk. “Low implied volatility in equity, currency and fixed-income markets, as well as signs of increased risk-taking, were viewed as an indication that market participants were not factoring in sufficient uncertainty about the path of the economy and monetary policy,” the minutes said. That’s like the Fed telling markets: “We don’t know what we’re doing so how can you be so sure?”

Fed Has Little Uncertainty, Despite Forecasting Misses - - Federal Reserve policy makers have been consistently too optimistic about economic growth and too pessimistic about the falling unemployment rate. But ask them if they’re uncertain about their forecasts and this is their answer: no more than usual. In 2012, Fed officials said they were more uncertain than usual about their forecasts for growth, unemployment and inflation. But over the course of 2013 their uncertainty has declined, and now almost all Fed officials are confident in their forecasts, according to the Fed’s self-assessment of uncertainty which was released Wednesday as part of Fed’s June meeting minutes. Fed officials have recently been concerned that markets have grown too complacent. Yet even at the Fed, only three officials rank their uncertainty about growth as high, and only two are more certain than usual about their unemployment forecasts. (The minutes do not identify by name which Fed official makes which forecast.) For the record, most Fed officials see growth of 2.1% to 2.3% this year and unemployment at the end of 2014 between 6% and 6.1%. Those forecasts were made in advance of their June 17-18 policy meeting, and already they’re beginning to look a little suspect.

Fed, Confident in Economy, Details End of Bond-Buying Program - The Federal Reserve said on Wednesday that it planned to stop adding to its bond holdings in October, in a sign of its confidence that the economy is gaining strength even as the central bank gradually withdraws its support. The decision, described in an account of the Fed’s most recent policy-making meeting in June, signals the end of one of the central bank’s most aggressive efforts to stimulate the economy. The Fed, which started reducing its monthly purchases in January, said it planned to add a final $100 billion to its holdings of Treasuries and mortgage-backed securities over the next four months, for a total of $1.5 trillion. But the account underscored that many Fed officials remained guarded in their optimism about the economy. It also suggested that they had not yet decided when to take an even more important step in their retreat: raising short-term interest rates for the first time since December 2008. Investors generally expect the Fed to start raising interest rates next summer. The Fed said the decision to end bond purchases in October, rather than continuing purchases at a nominal level until the end of the year, should not be interpreted as evidence that rate increases were likely to begin sooner. “Most participants viewed this as a technical issue with no substantive macroeconomic consequences and no consequences for the eventual decision about the timing of the first increase in the federal funds rate,” the minutes said, referring to the benchmark interest rate that the Fed uses to influence borrowing costs for consumers and businesses.

Do We Have Liftoff? -- (13 graphs) The minutes for the June 17-18 meeting of the FOMC revealed a discussion about the end of bond purchases in October but only a vague notion of when liftoff might occur. Many believe that “slack” labor market conditions are still a concern: In assessing labor market conditions, participants again offered a range of views on how far conditions in the labor market were from those associated with maximum employment. Many judged that slack remained elevated, and a number of them thought it was greater than measured by the official unemployment rate, citing, in particular, the still-high level of workers employed part time for economic reasons or the depressed labor force participation rate. The first estimate from the BLS establishment survey reports total non-farm employment increased by 288,000 in the month of June and the prior two months have been revised up by an additional 29,000. Here are our takeaways:All major BLS sectors (goods, services and government) added jobs in June. The next two charts illustrate these gains. The width of the bars represents the weight of each industry in total employment. For instance, employment in trade, transportation and utilities represents about one-fifth of all U.S. employment whereas industries like information or mining make up a much smaller fraction. In June, every industry with the exception of ‘other services’ added jobs. As you would expect from a healthy labor market, the largest job gains predominantly came from the largest sectors with trade, transportation and utilities and professional and business services adding a combined 139,000 jobs.

Analyst Expectations for Fed Rate Hikes are Shifting - Add Goldman Sachs to the list of Wall Street banks who see the Fed raising short-term interest rates sooner than previously thought. Goldman economist Jan Hatzius changed his Fed call after Friday’s jobs report, predicting the central bank would start raising short-term rates by the third quarter of 2015, not the first quarter of 2016 as previously thought. Mr. Hatzius pointed to three factors in a note to clients: 1) A faster-than-expected drop in the unemployment rate; 2) A pickup in inflation; 3) Easier financial conditions.“It marks the first time since the crisis that we have moved up our funds rate forecast,” Mr. Hatzius noted. “At least in part, we view this as an illustration of the substantial progress that the US economy has made in overcoming the fallout from the housing and credit bubble.” J.P. Morgan economists on Friday also moved forward to the third quarter of 2015 their forecast for the Fed’s first rate increase.

Fed’s Kocherlakota Sees No Urgency To Raise Short-Term Rates - Federal Reserve Bank of Minneapolis President Narayana Kocherlakota indicated Tuesday that any increase in short-term rates by the U.S. central bank likely lies well into the future. “I don’t make monetary policy according to a calendar,” Mr. Kocherlakota told reporters after a speech in Minneapolis. But he explained that a “necessary condition” for increasing short-term rates from near-zero-percent levels “should be that our one-to-two-year outlook” has inflation coming in at 2%, “or possibly above.” In his formal remarks, Mr. Kocherlakota said he sees very little risk of that scenario coming to pass anytime soon. “I currently see the probability of inflation averaging more than 2% over the next four years as being considerably lower than the probability of inflation averaging less than 2% over the next four years,” he said. Speaking to reporters, he said “I’d be willing to have inflation run above 2% for some time frame in order to bring employment back up more rapidly.” But for now, “there’s no reason for us to raise rates as long as inflation is running too low.”

Fed’s George Sees Room For Rate Hikes This Year - Kansas City Fed President Esther George said Thursday there are signs that the U.S. Federal Reserve should raise interest rates as early as this year, noting positive developments in the labor market and inflation rates closer to target. “As I look at some of the policy prescriptions that the Federal Reserve relies on, looking at formulas that help guide you on when it’s time to change, many of those are already pointing to lifting off of zero as early as even this year or next year,” . Ms. George, who isn’t currently a voting member of the monetary-policy setting Federal Open Market Committee, has been a consistent critic of the policies pursued by the central bank in the wake of the worst financial crisis since the Great Depression. In recent remarks Ms. George has argued that the Fed should start increasing short-term interest rates soon after its ends its bond-buying stimulus program later this year. Ms. George said that the economy appears to be back on track after a weak first quarter. She estimates economic growth will be somewhere between 2% to 2.5% for the full year. She said the labor market has improved to the point that surveys show the ability to attract qualified labor is a growing concern for employers, a situation that often leads to higher wages. Ms. George said that she expects the inflation rate to move closer to the Fed’s 2% target, adding that she’s concerned about the effect of higher food prices on low- and middle-income families.

Plosser Says Fed Must Consider Higher Rates as Policy Goals Edge Closer - Philadelphia Federal Reserve Bank President Charles Plosser said Friday the central bank is moving closer to its policy objectives, and therefore should begin thinking about the right time to raise interest rates. Mr. Plosser, a frequent critic of the Fed’s unconventional policies, told Bloomberg television U.S. interest rates have already been at rock-bottom lows for a very long time despite improvements in the economic outlook. “It’s important that we acknowledge that we are getting closer to our objectives and, for me, it’s important that we adjust monetary policy appropriately as we approach those objectives,” Mr. Plosser said. “We are moving closer to our goals and objectives. Inflation is drifting back up towards our 2% objective, the unemployment rate continues to move down.” Mr. Plosser said wages, which have been flat for much of the recovery, are a lagging indicator of inflation, not a leading one, suggesting the Fed could not wait for a pronounced pick-up before starting to tighten policy. “A lot of the guidelines that we look at, rules and things like that, that give us guidelines for where the stance of policy ought to be for any combination of inflation and unemployment — where that policy rate ought to be — many of these rules are indicating that we should be begin gradually raising interest rates,” he said.

Fed’s Plosser: Federal Reserve Must Prepare Markets for Rate Increases - Federal Reserve Bank of Philadelphia President Charles Plosser said Friday that the U.S. central bank needs to start preparing markets for increases in short-term interest rates that may come sooner than many currently expect. “We need to adjust the language in our statement to reflect that the economy really is better that it was, and that the necessity of having zero interest rates for a long time to come seems to me to be perhaps a risky or unnecessary step at this point,” Mr. Plosser said in an interview with The Wall Street Journal. “I don’t know if we need to tighten policy right now, but it’s pretty clear to me” the economy has improved in a way that central bankers need to get ready for the coming end to the Fed’s ultra-easy money stance, he said. Mr. Plosser, who currently holds a voting slot on the monetary policy-setting Federal Open Market Committee, long has been uncomfortable with the ultra-easy stance of monetary policy. He also has said in past that the Fed should contemplate raising interest rates sooner rather than later. In the interview, Mr. Plosser said that while he knows it is unlikely to happen, he would prefer for the Fed to lift rates this year and close out 2015 at a 1% short-term rate level, with rates at 3% by the close of next year.

Fed’s Lockhart: Still Sees First Fed Rate Boost Some Time in 2015 - Federal Reserve Bank of Atlanta President Dennis Lockhart said Friday he still believes the most likely timing for the central bank to raise interest rates lies well into next year. “I’m sticking to the view that conditions that would justify a liftoff decision will arrive in the second half of next year,” Mr. Lockhart said. “The potential and achievable benefits of sustaining very accommodative monetary stimulus, based on a policy rate in its current range of 0 to 25 basis points, beyond year-end 2014 and into next year continue to outweigh the possible costs.” Mr. Lockhart’s comments came from the text of remarks prepared for delivery before a gathering held by the Global Interdependence Center in Jackson Hole, Wyo. Speaking to reporters after his speech, Mr. Lockhart said “If the economy is much stronger than what I’m anticipating, and we get closer to our objectives sooner, than I would obviously reconsider my position.” Mr. Lockhart’s comments came as the outlook for central-bank policy is undergoing a shift. The Fed is in the process of steadily winding down its bond-buying stimulus program and will most likely end the effort at its October policy meeting.

Fed Watch: When The Fed Starts Raising Rates: For those that hope to use tighter monetary policy to bolster the case against equities, recall that patience may be required: For those making the bear case against long bonds, recall that initially long rates fell, and over the entire cycle rose just (roughly) 50bp: The short end of the curve suffered, and the yield curve inverted: How does this compare to now? If we consider last December's taper the beginning of this tightening cycle (the Fed does not; they prefer to think of it at reducing financial accommodation), stocks continue to power higher: The 10 year bond initially fell on the taper talk and the yield curve steepened through the 10 year. But that steepening ended when the taper began: More interesting is the flattening of the very long end after the taper began: It looks like rates are signalling that the Fed will act to contain activity such that the economy does not overheat. Which, assuming the Fed maintains its current reaction function, tends to support modest porposal's interpretation - favor the long end of the curve over the short end. I think the flattening of the yield curve should be a concern to the Fed. It suggests that while we frequently hear Janet Yellen described as a dove, the expectation is that her actual policy approach will be cautious bordering on hawkish. Not good if you think like Andy Harless: I will consider Yellen's tenure a failure if the economy does not overheat.

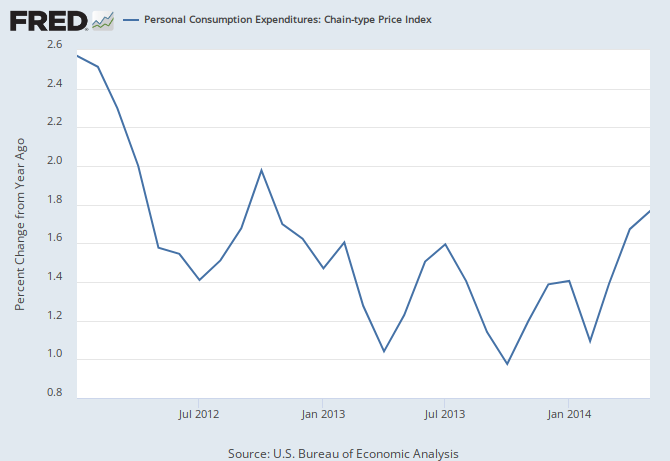

Is the Fed Behind the Curve? — Imagine Fed Governor Rip van Winkle started his nap at the beginning of 2007 and just woke up to find that inflation is close to the Fed’s objective and the unemployment rate is at its 30-year average. You could forgive him for expecting the federal funds rate to be close to its long-run norm of about 4%, and for his surprise upon learning that the funds rate is at 0.1% and Fed assets are five times where they were when his snooze began. Is the Fed already behind the curve? Why do policymakers emphasize their expectation that rates will stay low “for a considerable time” beyond October (when asset purchases are expected to halt)? What risks are they seeking to balance? The most common benchmark for monetary policy is the Taylor rule, which relates the central bank’s policy rate to a combination of deviations of inflation from its target and a measure of resource slack. The modified Taylor rule in the chart below shows that – even ignoring the Fed’s balance sheet expansion – the Fed’s interest rate policy is now unusually stimulative by the standard of the past three decades. [The blue line in the chart is based on the Fed’s preferred inflation measure, the price index of personal consumption expenditures, and the deviation of the unemployment rate from its equilibrium level as a measure of slack.] So, what might warrant such large stimulus? We can think of four possible reasons: (1) the Fed’s inflation objective isn’t really 2%, it’s higher; (2) the equilibrium real interest rate is well below the 1.75% implied by FOMC members’ current long-run projections; (3) resource slack far exceeds that implied by the 6.1% unemployment rate; and (4) the Fed is purchasing insurance against a negative economic shock that would – once again – force it to rely on unconventional balance sheet policies. Let’s analyze these one-by-one.

Fed explores overhaul of key rate: The US Federal Reserve is exploring an overhaul of the Federal funds rate – a benchmark that underlies almost every financial transaction in the world – as it prepares for an eventual rise in interest rates. ... According to people familiar with the discussions, the Fed could redefine its main target rate so that it takes into account a wider range of loans between banks, making it more stable and reliable. Concerns have grown about the reliability of the Fed funds rate since the Fed began buying trillions of dollars of assets during three rounds of quantitative easing. US banks now have huge amounts of cash and have stopped borrowing or lending Fed funds, making the market highly illiquid. With the Fed targeting rates close to zero, the reliability of Fed funds has been less important, but when the Fed starts raising rates – something markets expect it to do in the middle of next year – it needs to be sure that it is targeting a real benchmark. In particular, the Fed is looking at redefining the Fed funds rate to include eurodollar transactions – dollar loans between banks outside the US markets – as well as traditional onshore loans between US banks.

Fed vice chairman suggests including financial stability among chief goals - Federal Reserve Vice Chairman Stanley Fischer on Thursday suggested banking regulators should seriously consider broadening their goals to include financial stability as policymakers around the world debate strategies for preventing another global crisis. Fischer argued that an explicit stability mandate could give regulators more firepower to combat risks as they emerge. The issue of how central bankers should address nascent bubbles has become a flashpoint in economics, with some worrying that years of ultralow interest rates and easy monetary policy could be fueling hidden excesses. In a speech in Cambridge for the National Bureau of Economic Research -- his first as vice chairman -- Fischer warned that the U.S. structure for overseeing the financial system may not be up to its task. “It may well be that adding a financial stability mandate to the overall mandates of all financial regulatory bodies … would contribute to increasing financial and economic stability,” he said, according to prepared remarks. Fischer did not weigh in on whether central banks should use monetary policy - namely, interest rates -- to combat bubbles. But he did point out that policymakers do not have a strong understanding of how well their regulatory toolkit might work.

New Legislation Requires Fed to Adopt Policy Rule -- John Taylor --A lot of research and experience shows that more predictable rules-based monetary policy leads to better economic performance—both in terms of price stability and steadier-stronger employment and output growth. But in practice there have been big swings in Fed policy between rules and discretion, with damaging results as in the 1970s and the past decade of a financial crisis, great recession and slow recovery. This experience—especially the swing from rules to discretion in the past decade—demonstrates the need for legislation requiring the Fed to adopt rules for setting its policy instruments. So it is good news that today the ‘‘Federal Reserve Accountability and Transparency Act of 2014” was introduced into Congress. It requires that the Fed adopt a rules-based policy. In particular, Section 2, the first main section of the Act, titled “Requirements for Policy Rules for the Federal Open Market Committee,” would require that the Fed “submit to the appropriate congressional committees a Directive Policy Rule… which shall describe the strategy or rule of the Federal Open Market Committee for the systematic quantitative adjustment of the Policy Instrument Target to respond to a change in the Intermediate Policy Inputs.” Thus the rule would describe how the Fed’s policy instrument, such as the federal funds rate, would change in a systematic way in response to changes in the intermediate policy inputs, such as inflation or real GDP. The rule would also have to be consistent with the setting of the actual federal funds rate at the time of the submission.

A Legislated Taylor Rule? - John Cochrane -- John Taylor announces in his blog post, "New Legislation Requires Fed to Adopt Policy Rule'' that today .. the ‘‘Federal Reserve Accountability and Transparency Act of 2014” was introduced into Congress. It requires that the Fed adopt a rules-based policy. Basically, the Fed would have to report to Congress and explain any deviation from a "Reference policy rule," Wow. John will testify at a hearing at the House Financial Service Committee on Thursday, along with Mark Calabria, Hester Peirce and Simon Johnson. This should be very interesting. What is most interesting about a rule is what it leaves out. Notably absent here is "macroprudential" policy, "financial stability" goals, i.e. raising rates to prick perceived asset price "bubbles" and so forth. Janet Yellen's remarkable recent speech foreswore a lot of that. Of course, the Fed could always add it as a "temporary" need to deviate from the rule. Still, many people might think that should be part of the rule not part of the exception. It also leaves out housing, exchange rates, and all the other things that central banks like to pay attention to. A rule really is a list of things that the Fed shall not react to without explanation.

Should Congress legislate so that the Fed is forced to follow policy rules? - No. But, as John Taylor alerted us in his blog, a new bill has been introduced that would have this effect, if passed. I presume that this is one of those bills that no-one expects to pass, but is put before it to stimulate debate. Debate is always a good idea, but even a tiny chance that it might actually pass is a cause for concern. Why? Even before the financial crisis, I would have said that the ‘Science of monetary policy’, to borrow a phrase from the elegant survey of modern sticky-price-monetary policy macro by Clarida, Gali and Gertler, had not progressed to the point where anything could be gained by attempting to legislate for such a rule. Why not? Because even then there was too much disagreement encoded in the controversies about the transmission mechanism of policy to produce a consensus about what such a rule would look like. Even if such a rule were chosen by the Fed, and reported to Congress, everyone would rightly expect that the necessity to deviate from it practically every period would dominate the benefit from generating further predictability in policy. And hence little or no further predictability would result. If, by some strange quirk, the Fed found itself forced or tempted to follow such a rule, macroeconomic policy would surely suffer, and uncertainty would soon return as everyone speculated about the point at which a consensus would build to cast of the shackles of this legislation.

House Republicans Want Fed to Adopt Policy-Making Rules - Several House Republicans are embracing Stanford University economist John B. Taylor’s call for the Federal Reserve to adopt a mathematical rule for determining interest rates, stepping into a long-running debate among central bankers about how to set monetary policy. The House Financial Services Committee will hold a hearing Thursday “Legislation to Reform the Federal Reserve on Its 100-year Anniversary,” at which Mr. Taylor and other Fed critics are scheduled to testify. The hearing will focus on a bill—introduced Tuesday by Republican Reps. Scott Garrett of New Jersey and Bill Huizenga of Michigan–that would, among other things, require the Fed to provide Congress with “a clear rule to describe the course of monetary policy,” according to a committee announcement. Such a rule would be an equation showing how the Fed would adjust interest rates in response to changes in certain economic variables. One well-known example is the Taylor rule, named for Mr. Taylor. Mr. Taylor told The Wall Street Journal last month that under his rule, the Fed should be setting its benchmark short-term rate above 1%, rather than near zero. Economists have been debating for years the relative merits of basing interest rate policy on rules vs. discretion—that is, whether they should adhere to a mathematical formula or maintain some wiggle room based on circumstances and judgment. Mr. Taylor and some Fed officials are in the first camp, saying rules-based policymaking creates more predictability and transparency, leading to better economic outcomes. He praised the legislation on his blog Monday. Others, including Fed Chairwoman Janet Yellen and most top Fed officials, say they need flexibility to veer from the rules when appropriate. In 2012, Ms. Yellen, then the central bank’s vice chairwoman, said Fed officials were using a modified version of the Taylor rule intended to give greater weight to employment, which fell sharply during the recession.

House panel sets hearing to reform Federal Reserve (Reuters) – Republicans in the U.S. House of Representatives, who have proposed bills to audit the Federal Reserve and to limit its policy mandate, on Monday set a hearing to discuss measures aimed at the U.S. central bank. The title of the hearing is “Legislation to Reform the Federal Reserve on Its 100-year Anniversary,” according to a memo from the U.S. House Financial Services Committee. The notice did not cite any specific legislation to be discussed at the hearing, set for Thursday. A spokesman for the committee did not return a call from Reuters seeking more details about the hearing. Committee Chairman Jeb Hensarling has pledged to demand more transparency from the Fed. Some politicians have criticized the central bank for its aggressive actions after the financial crisis to lower unemployment and stimulate the economy using unconventional tools such as a monthly bond-buying program and building a balance sheet that now exceeds $4.5 trillion.

Lawmakers Seek Disclosure of High Earners at Federal Reserve Banks -- Two GOP lawmakers, Reps. Bill Huizenga of Michigan and Scott Garrett of New Jersey, have introduced a bill known as the Federal Reserve Accountability and Transparency Act (FRAT Act), which includes a provision that would require disclosure of Fed officials with high salaries. The main goal of the bill is to require the Fed to use a monetary policy rule in setting its policy. The Republican legislation, which will be the subject of a House hearing Thursday, would need to clear the full House and garner support in the Senate — a step that will be challenging given that chamber’s control by Democrats.One interesting provision of the bill would require the Fed’s Board of Governors to disclose, with a searchable database, the names of all employees in the Fed system who earn more than a GS-15, the top of the federal pay scale for government bureaucrats. The basic GS-15 salary begins at $100,624 a year and climbs to $130,810, according to the U.S. Office of Personnel Management. Cost-of-living adjustments push this scale higher in more expensive cities. In Washington, D.C., and New York, for example, GS-15 can climb up to $157,100. Requiring disclosure of employees earning above the GS-15 scale would require a lot of work at the Fed for one simple reason: The 12 regional Federal Reserve Banks are not subject to the GS system and many of their employees earn higher salaries. The Fed already discloses the salaries of the 12 regional presidents, ranging from $281,300 a year for St. Louis Fed President James Bullard to $410,780 a year for New York Fed President William Dudley. The reserve bank president salaries are far higher than those for the Fed’s Washington-based Board of Governors. Chairwoman Janet Yellen earns $201,700 a year and the other governors earn $181,500. The Fed declined to comment on the bill.

Central Bank Smackdown - The opening riposte came from the Bank for International Settlements, the “bank for central banks.” In their annual report, released this week, they talked about “euphoric” financial markets that have become detached from reality. They clearly – clearly in central banker-speak, that is – fingered the culprit as the ultralow monetary policies being pursued around the world. These are creating capital markets that are “extraordinarily buoyant.”The report opens with this line: “A new policy compass is needed to help the global economy step out of the shadow of the Great Financial Crisis. This will involve adjustments to the current policy mix and to policy frameworks with the aim of restoring sustainable and balanced economic growth.”The Financial Times weighed in with this summary: “Leading central banks should not fall into the trap of raising rates ‘too slowly and too late,’ the BIS said, calling for policy makers to halt the steady rise in debt burdens around the world and embark on reforms to boost productivity. In its annual report, the BIS also warned of the risks brewing in emerging markets, setting out early warning indicators of possible banking crises in a number of jurisdictions, including most notably China.” “The risk of normalizing too late and too gradually should not be underestimated,” On July 2, two days after the release of the BIS report, Janet Yellen took the stage at the IMF conference and basically said (translated into my local Texas patois), “Kiss my grits.” She was having nothing to do with risk and productivity and spent her time defending the low-rate environment she has been fostering in the US. With just a brief hat tip to the fact that monetary policy can contribute to risk-taking by going “too far, thereby contributing to fragility in the financial system,” she proceeded to maintain that monetary policy should “focus primarily on price stability in full employment because the cost to society in terms of deviations from price stability in full employment that would arise would likely be significant.” (You can read the speech here if you have nothing else to do and your recent entertainment options have been limited to watching the microwave cook.)

How Prophets Get Lonely -- Paul Krugman - At Bloomberg View, Leonid Bershinksy weeps over the cruel world that for some reason isn’t listening to Jaime Caruana of the BIS, who warns that we must raise interest rates now now now. Why is this prophet so lonely? Well, it might have something to do with the fact that three years ago Caruana and the BIS warned that interest rates must rise to avert a surge of inflation. That didn’t happen — in fact, low inflation and the threat of deflation came instead. Now, everyone gets things wrong sometimes. But when that happens, you’re supposed to think about why you were wrong, and reconsider your policy views. If the BIS did any soul-searching, nobody else noticed — and it’s still calling for higher rates, with a new justification (and where it used to warn about inflation, now it’s arguing that deflation isn’t so bad.) Why, exactly, should anyone take its views seriously at this point?But being a hard-money guy seems to mean never having to reconsider. I missed my chance to mark the anniversary, but it’s now five years plus since the WSJ warned that wildly inflationary monetary and fiscal policies were bringing on the bond vigilantes. And to read their opinion pages, you’d think they were right all along.

"This Is The Worst Of All Possible Worlds," The Fed "Is Borrowing Returns From The Future" -- Felix Zulauf, James Montier and David Iben: Three legendary investors share their views on financial markets. Everything is pricey ("we will continue to swim in a sea of liquidity; but there might be other events and developments that may not be camouflaged by liquidity which could cause a change of investor expectations.") the European periphery is a bubble ("The Euro crisis is not over...the European economies are not going to change for the better for years to come despite all the cheating and breaking of laws"), Value investors need to venture to Russia ("when you look at today’s opportunity set, you’re left with a set of assets where nothing looks attractive from a valuation point of view") or buy gold mining stocks (" The down cycle could be much bigger than anybody believes if the market realizes that all the actions taken in recent years do not work.") Summing it all up, "there is no question that [sovereigns] lack the fundamental economic base to finally service their debts,"

Yellen Is Flat-Out Wrong: Financial Bubbles Are Caused By The Fed, Not The Market - The selloff last year was a desperate warning about the lack of resilience in credit and funding. That repo markets persist in that is, again, the opposite of the picture Janet Yellen is trying to clumsily fashion. Central banks cannot create that because their intrusion axiomatically alters the state of financial affairs, and they know this. It has always been the idea (“extend and pretend” among others) to do so with the expectation that economic growth would allow enough margin for error to go back and clean up these central bank alterations. That has never happened, and the modifications persist. Resilience is the last word we would use to describe markets right now, with very recent history declaring as much

Central Bank Battles Against Bubbles - Dean Baker - In a Wonkblog post Matt O'Brien discusses central bank efforts to deal with bubbles. . A bubble that threatens the economy is a bubble that moves the economy. If there is a bubble in Uber stock or the price of hops, there is little consequence to the economy when the bubbles burst. The crashes of the stock bubble and the housing bubble led to recessions because these bubbles were driving the economy. This was easy to see in the data in both cases. In the first case, the investment share of GDP hit the highest level in more than two decades as people were able to raise billions in IPOs for utterly nonsense dot.coms. Consumption surged to then record shares of income as the stock wealth effect caused spending to surge. This boost to the economy disappeared when the bubble burst.There was a similar story with the housing bubble. Residential construction hit a record share of GDP, roughly 50 percent above its average over the prior two decades. Consumption surged to an even higher share of income, driven by the housing wealth effect. And, when this bubble burst we got the Great Recession.The other point is that central banks do have many tools other than interest rates to attack bubbles. My favorite is talk. I know it doesn't sound sophisticated and it's not terribly mathematical, but I suspect it would have a very large impact on the housing market if Janet Yellen were to say that she thought house prices were over-valued and that the Fed would be prepared to take steps to bring prices in line with fundamentals. Note that I am referring to an explicit warning backed up by Fed research, not a mumbled "irrational exuberance" subsequently qualified by incoherent gibberish. I would certainly take such a warning seriously if I was thinking of buying a house.

If All Else Fails, You Eat Your Kids - The global financial system owns our societies, banks, politicians, the whole lot. It therefore owns us too, which includes you, and it’s very counterproductive to deny that. It can do what it wants and what it pleases with impunity. It took the finance wizards surprisingly long to figure that out, but they have. This has enabled them to buy everything and everyone they wanted to buy. Yet, as with so many things in life, if and when introduced sufficiently slow and sneaky, people don’t even notice and when they do, they simply see it as a given. “You get used to anything, sooner or later it becomes your life”. This kind of slow and sneaky scheme gets far more persuasive if the perpetrators manage to convince people that it is actually to their benefit. That the scheme is meant to, for instance, lift them out of a crisis. “It’s very complicated, but lucky you, we know much more about this than you do, and you can trust us, since after all, we’re all in this together, we all want and need growth”. Or else, we have armageddon. Or seven plagues. So an insane amount of money has been spent, and pledged, on all sorts of sub-schemes – QE – that ostensibly will solve our problems, and theirs. Only, theirs have to be solved first, because if they’re not, it’s still seven plagues for everyone. There is a man in the street “consumer” base consisting of many hundreds of millions of people in the west that can be drawn on to “finance” the rescue schemes. And if that is not enough, there are hundreds of millions more of their children. Who will all be forced to put in their labor to try and survive.What the perpetrators know, and neither the people nor their children do, is that a recovery is not possible, because as things stand it would have to be built on a pile of debt so large that it makes any recovery impossible. Record stock markets, higher home prices and a tidal wave of good news stories about equal in size to the debt tidal wave, have kept the public in the dark about this painfully simple fact. Meanwhile, not only is the bankrupt financial system being kept alive, it’s made much richer.

Charting The Death Of The Saver -- Euthanasia of the rentier appears to be increasingly the modus operandi of the central planning caste of the world. As we noted previously, Bernanke's (and now Yellen's) plan to exterminate savers is wholly unsustainable, The Fed's insistence that "our savers collectively have to hold all the assets of the economy and a strong economy produces much better returns in general" must be juxtaposed with comments from a money manager that "I don't think that's a fair-trade" for money intended to be invested safely." By removing the last shred of hope for a rise in savings rates anytime soon, the Fed is once again creating the potential for major unintended consequences as the collapse in interest income for US savers from the 2008 peak forces them to extend duration (TSYs), lower quality (corporate bonds), and/or increase leverage/risk (equities).

On Losing Interest - Krugman -- No, it’s not about boredom. Instead, a further thought on the question of who might be upset about low-interest-rate policies. Low policy rates plus quantitative easing have indeed meant much lower interest earnings across the board, and this is a serious hit to the incomes of those who own interest-bearing assets. So who are we talking about? Yes, there are some middle-class retirees collecting interest on their CDs. But the big losers are people with very high incomes. Again from the Piketty-Saez data, we can track the decline in interest incomes from 2007 to 2011 (measured in 2012 dollars) and compare it with income in 2007 at different percentiles. Here’s what it looks like:Photo Credit It’s not a big deal for people in the bottom half of the top 10 percent, who might well consider themselves middle class. But among the top 0.01 percent, low interest rates have actually been a bigger income hit than Obama’s tax hikes (partial reversal of Bush cuts plus the ACA surcharge).You’re living in a fantasy world if you don’t think this has something to do with the diatribes against currency debasement and all that.

More on Class and Monetary Policy - Paul Krugman - A bit more on the question of whose interests are served by hard-money ideology: One way to identify what you might call the creditor class is to look at who derives a lot of income from interest. The Piketty-Saez tables calculate interest income as a share of total income for various percentiles of the income distribution; I looked at the numbers from 2007, when the crisis had not yet struck and returns were “normal”. It looks like this: So interest is a significant source of income only for people high in the distribution; it gets really big for people with very high incomes. These are the people who have a lot to lose if inflation erodes the values of their assets, and a lot to gain if inflation comes in below expectations or there is actual deflation. So hard-money ideology is, to an important extent, a reflection of class interests — not so much the one percent as the 0.01 percent.

Fellow Travelers of the Depression Lobby - Dean Baker -- Paul Krugman took off the gloves in his column today. He said that much of the opposition to the Fed's low interest rate policy stems from the narrow interest of very rich people who earn lots of interest on their money. Krugman argues that the reason the argument against low interest rates continually reappears in different forms is the money that the 0.01 percent have at stake in protecting their interest income. While we are on the topic of interests determining views on monetary policy, let's take a step over to a different, but arguably more important issue: dollar policy. The key point here is that the value of the dollar is the main determinant of the trade deficit. The basic point is simple. When the dollar is highly valued in terms of foreign currency (i.e. it takes a lot of euros, yen, or yuan to buy a dollar) our goods and services become more expensive relative to the goods and services produced by other countries. This means we will import lots of items from other countries, because they are cheap to us, and they will buy few of our exports, because they are expensive to them. In other words, we will have a large trade deficit. If we have a trade deficit of $500 billion (@ 3 percent of GDP), which we do, this is demand that we are generating in other countries rather than here. We have no simple mechanism for replacing this demand. We could have large budget deficits, but that route is prohibited by the bi-partisan cult of balanced budget worshiping. We can try to have the Fed boost the economy with low interest rates, quantitative easing, and other such policies, but these paths have a limited impact on growth, at least as we have seen to date. This means that we have no good route for filling the demand gap created by the trade deficit. This might lead us to believe that a lower valued dollar should be item number one, two, and three on everyone's economic agenda. Yet, it rarely appears on anyone's to-do list.

Fed Watch: Inflation Hysteria Redux -- I am in general agreement with Calculated Risk on this point:I also think the economy is picking up, and I agree that as slack diminishes, we will probably see real wage growth and an uptick in inflation. Moreover, note that this is largely consistent with the Federal Reserve's outlook as well. Recall St. Louis Federal Reserve President John Williams from April, via Bloomberg: Williams, who forecast the Fed will start raising interest rates in the second half of next year, said inflation has “bottomed out” and will gradually accelerate to the central bank’s 2 percent target. He said prices have been held down by temporary forces such as a slowdown in health care costs. The Federal Reserve has consistently predicted higher inflation, and consistently been surprised that that inflation has not yet arrived despite rapidly falling unemployment rates. It would appear, however, that their forecasts are finally coming true. Hence, I also agree with Calculated Risk when he says: I'm sympathetic to people like Joe Weisenthal at Business Insider who is looking for signs of inflation increasing; I'm starting to look for signs of real wage increases and inflation too. I just think inflation isn't a concern right now. It is enough to simply say that inflation is coming. That in and of itself is insufficient. Any inflation call needs to be placed in the context of magnitude and expected monetary policy response. Regarding both, follow Calculated Risk's warning: Monetary policy can't halt the violence in Iraq or make it rain in California - and this is why it is important to track various core measures of inflation. The Fed doesn't target core inflation. They target headline inflation. But they also believe that headline inflation will revert to core, and as such tend to be more concerned with core inflation in excess of 2%. Consider the history of core inflation since 1985:

Fed's Kocherlakota downplays recent inflation rise One of the Federal Reserve's leading doves downplayed recent higher readings on inflation on Tuesday, saying he expects the price level to stay below the central bank's target for several more years, possibly even until 2018.While inflation has climbed over the past three months and is now up 1.8% over the past year, "many large fluctuations in [the personal consumption expenditure index] inflation end up being purely transitory," said Narayana Kocherlakota, the president of the Minneapolis Fed, in a speech to the Minnesota Business Partnership . "I currently see the probability of inflation's averaging more than 2% over the next four years as being considerably lower than the probability of inflation's averaging less than 2% over the next four years," he said. Low inflation means that resources are being wasted, Kocherlakota added, notably in the form of unemployed workers. "There is still significant underutilization of our country's most important resource - its people," he said. The unemployment rate, which fell to 6.1% in June "could well overstate the degree of improvement in the U.S. labor market," he added. As a result, the Fed is undershooting its price stability objective and underperforming its maximum employment objective, he said. Kocherlakota is a voting member of the Fed policy committee this year.

Fed’s Lockhart Isn’t Convinced of Firmer Inflation Trend - A top Federal Reserve official said on Friday that policy makers needed more time to determine whether a recent pickup in inflation from levels regarded as undesirably low is likely to persist. Dennis Lockhart, president of the Atlanta Fed, repeated his view that the central bank should keep interest rates near zero at least until the middle of next year. Other officials have been hinting that firmer economic growth may warrant a move sooner than that. Mr. Lockhart told Bloomberg Television some of the factors pushing up inflation, such as energy prices, could be transitory. “I welcome the firming of [inflation] rates that we’ve seen in the last very few months. Whether those numbers make a trend—and it’s a trend that we want, the sustainability of inflation around 2%—remains to be seen,” he said. “I’m not sure yet, I want to watch the numbers for a while to determine whether it is going to hold. It’s a little early to make such a call.” Mr. Lockhart emphasized inflation had been running well below the Fed’s target for several years. “I am still in the camp of wanting to see a test of time to prove that we, in fact, are going to see rates near or at our target of 2%,” he said.

Fed’s Kocherlakota: It Could Take 4 Years to Get Back to 2% Inflation -- Federal Reserve Bank of Minneapolis President Narayana Kocherlakota said Tuesday it could take nearly half a decade for inflation to get back to levels central bankers deem appropriate. The Fed is “undershooting its price stability goal” of 2% inflation and will likely continue to do so for some time to come. Mr. Kocherlakota says that he sees the probability of inflation averaging more than 2% over the next four years as being “considerably lower” than the probability of inflation coming in less than 2% over the same time period. “We need to do better,” the official said. Mr. Kocherlakota’s remarks largely the same as an address he gave in late May. The official did not make any forward-looking comments about the monetary-policy outlook in his formal remarks, but he was due to take questions from the audience and reporters. Mr. Kocherlakota has been among the Fed’s strongest supporters of using monetary policy aggressively to help drive up growth and lower unemployment. In the spring, he offered a formal dissent against the monetary-policy setting Federal Open Market Committee’s decision to move toward vaguer guidance regarding the factors that will eventually cause it to raise interest rates. Mr. Kocherlakota reiterated that he is skeptical that improvements in the job market are strong as they seem.

Fed’s Evans: Inflation Over 2% Not Necessarily a Catastrophe - Federal Reserve Bank of Chicago President Charles Evans said Friday it’s pretty unlikely the economy will suddenly grow fast enough to drive him to move forward his expected timing of the central bank’s first interest rate increase. Speaking to reporters, Mr. Evans said he could envisions a scenario where economic growth accelerated very sharply relative to expectations, inflation moved back toward the Fed’s target and wage gains returned to their historic levels. “I could see that happen, but it’s not my highest likelihood,” and as a result, it’s possible, but pretty unlikely, that the Fed would move forward the time in which it would raise short-term interest rates off their current near zero percent levels, he said. Mr. Evans comments came from an appearance before an event held by the Global Interdependence Center in Jackson Hole, Wyo. Mr. Evans is one of the Fed’s strongest defenders of taking aggressive action to spur growth. In his formal speech, he said the central bank faces little pressure to raise rates given that the job market is still showing weakness and inflation is under the Fed’s official 2% target.

Waiting for inflation - The Economist - OVER the last six months, America's labour market seems to have strengthened meaningfully, if not exactly dramatically. At the same time, the long trend toward steady disinflation seems to have come to a halt, or at least paused. Inflation as measured by both the consumer price index and the price index for personal consumption expenditures (the Fed's preferred gauge) has ticked back up toward the Fed's 2% target. Some economic writers, like Business Insider's Joe Weisenthal, reckon there might be even more ahead. So, what are the odds of a bout of above-target inflation? Most of the time, the Fed's overriding concern is stabilisation of the inflation rate at a level a bit below 2%. What that means in practice is that headline inflation will move around a bit, thanks to swings in commodity prices or other supply-side influences that are not expected to feed through in any significant way to underlying, or core, inflation. Core PCE inflation will be much less volatile, and will, over the medium run, hover basically where the Fed wants it. As Tim Duy writes in an excellent post on the subject: If you are making a short-term bet on higher headline inflation, primarily you are making a bet on energy and food. That bet is about the Middle East and weather, not monetary policy. I don't have an opinion on that bet. If you are betting on inflation over the medium-term, primarily you are making a bet on higher core inflation. More to the point, you are betting against the Fed. Betting against the Fed? In 1981, core PCE inflation was nearly 10%. The Fed then induced a major recession, and over the next 12 years core inflation declined steadily. Since 1994, year-on-year core PCE inflation has never been as high as 2.5%. Indeed, David Beckworth argues pretty compellingly that since 2008, the Fed has essentially been targeting a corridor for core PCE inflation of between 1% and 2%.

It's All But Official: There is No 2% Inflation Target - Rather, there is a 2% upper bound to the Fed's inflation target. This is an argument that Ryan Avent, Matt Yglesias, Paul Krugman, and others have been making for some time. I am sympathetic to this view and have made the case that the Fed has been effectively targeting a core PCE inflation corridor of 1% to 2% over the past five years. The evidence continues to mount in favor of this view. First, consider the timing of the Fed's QE programs and changes in the core PCE inflation rate as seen below. The figure suggests that the FOMC iniatiates QE programs when core inflation is under 2% and has been falling for at least six months. It also indicates the FOMC tends to end QE programs when core inflation is above 1% and has been rising for at least six months. That ending of QE3 in October later this year follows this pattern. Reinforcing this point, the Fed's purchases of treasuries since the crisis started is correlated with changes in core PCE inflation. Specifically, changes in the Fed's holdings of treasuries as percent of all treasuries can explain almost half of the variation in core PCE inflation since 2007 as seen below: Second, consider the central tendency ranges of inflation forecasts provided by members of the FOMC. This information can be found in the 'projection' material. These forecasts are consistent with the observed core PCE inflation data highlighted above. They consistently show 2% as an upper bound.

Inflation Targeting: A Monetary Policy Regime Whose Time Has Come and Gone - Inflation targeting emerged in the early 1990s and soon became the dominant monetary-policy regime. It provided a much-needed nominal anchor that had been missing since the collapse of the Bretton Woods system. Its arrival coincided with a rise in macroeconomic stability for numerous countries, and this led many observers to conclude that it is the best way to do monetary policy. Some studies show, however, that inflation targeting got lucky. It is a monetary regime that has a hard time dealing with large supply shocks, and its arrival occurred during a period when they were small. Since this time, supply shocks have become larger, and inflation targeting has struggled to cope with them. Moreover, the recent crisis suggests it has also has a tough time dealing with large demand shocks, and it may even contribute to financial instability. Inflation targeting, therefore, is not a robust monetary-policy regime, and it needs to be replaced.

The Unemployment Cost of Below-Target Inflation: Recently, inflation in the United States has been consistently below its 2% target. The situation in Sweden is similar, but has lasted much longer. The Swedish Riksbank announced a 2% CPI inflation target in 1993, to apply beginning in 1995. By 1997, the target was credible in the sense that inflation expectations were consistently in line with the target. From 1997 to 2011, however, CPI inflation only averaged 1.4%. In a forthcoming paper in the AEJ: Macroeconomics, Lars Svensson uses the Swedish case to estimate the possible unemployment cost of inflation below a credible target... The unemployment rate would be about 0.8% lower if inflation averaged 2% (and presumable lower still if inflation averaged slightly above 2%). ... Svensson concludes with policy implications:"I believe the main policy conclusion to be that if one wants to avoid the average unemployment cost, it is important to keep average inflation over a longer period in line with the target, a kind of average inflation targeting (Nessén and Vestin 2005). This could also be seen as an additional argument in favor of price-level targeting...On the other hand, in Australia, Canada, and the U.K., and more recently in the euro area and the U.S., the central banks have managed to keep average inflation on or close to the target (the implicit target when it is not explicit) without an explicit price-level targeting framework.

Knutty Asset Prices - Paul Krugman - Neil Irwin has a nice piece about high asset prices that actually ties into my Wicksell discussion from earlier today. What Irwin points out is that the price of just about every asset category is now high by historical standards. Bond prices in “safe” countries are very high, which is the same thing as saying that interest rates are very low. But so are prices of risky sovereign debt — Paul De Grauwe points out that Spain’s borrowing costs are now the same as Britain’s. Corporate bond rates are low; stock prices are high; all across the board, assets are up. The proximate cause is obvious: policy interest rates are very low, and expected to remain low, so money is pouring into alternative assets, driving their yields down too. The question is what you think about this situation.Quite a few people — including a lot of people on Wall Street, at the BIS, and so on — look at this and say that it’s terrible: the Fed is keeping interest rates “artificially low” and thereby distorting asset prices across the board, and it will all end in grief. But although I hear the phrase “artificially low” all the time, I don’t think many people who use it have thought through what they mean. What would a non-artificial interest rate be?

Class and Monetary Policy - Paul Krugman - I’ve been writing a lot lately about the continuing influence of inflation hysterics despite their awesome wrongness over the past five-plus years. One question that naturally arises is whose interests are served by this unjustified influence. You don’t want to be too crude about it. I don’t think there are a lot of clear-headed hard-money types who secretly admit to themselves that their models have failed and that the policies they advocate could mire the economy in a permanent slump, but nonetheless say what will support their class interests. Instead, interests feed ideology, and the ideologues may then be sorta-kinda sincere in their beliefs. Still, it is worth asking who benefits from low inflation or deflation, and from higher interest rates. And the answer, basically, is rich old men. On the rich part: Using SIPP data, we can look at the comparison between financial assets and debt by household net worth: Only the top end have more financial assets (as opposed to real assets like housing) than they have nominal debt; so they’re much more likely to be hurt by mild inflation and be helped by deflation than the rest.

Who Wants a Depression?, by Paul Krugman -- One unhappy lesson we’ve learned in recent years is that economics is a far more political subject than we liked to imagine. ... I’ve written a number of times about the phenomenon of “sadomonetarism,” the constant demand that the Federal Reserve and other central banks stop trying to boost employment and raise interest rates instead, regardless of circumstances. I’ve suggested that the persistence of this phenomenon has a lot to do with ideology, which, in turn, has a lot to do with class interests. And I still think that’s true. But I now think that class interests also operate through a cruder, more direct channel. Quite simply, easy-money policies, while they may help the economy as a whole, are directly detrimental to people who get a lot of their income from bonds and other interest-paying assets — and this mainly means the very wealthy, in particular the top 0.01 percent. ... Complaints about low interest rates are usually framed in terms of the harm being done to retired Americans living on the interest from their CDs. But the interest receipts of older Americans go mainly to a small and relatively affluent minority..., and it surely explains a lot of the hysteria over Fed policy. The rich ensure that there are always plenty of supposed experts eager to find justifications for this attitude. Hence sadomonetarism.

High Asset Prices, the Savings Glut, Secular Stagnation, and Unemployment -- Dean Baker - Neil Irwin has an interesting piece in the NYT noting how high prices for a wide variety of assets have driven returns down to historical low levels. He notes that this is a predictable outcome, and in fact an intended result, of the low interest rate policy being pursued by the Fed and other central banks. The idea is that high asset prices make it cheap for firms to borrow to finance new investment. They also make it easier to buy a home and allow many people who had higher interest rate mortgages to refinance into lower cost ones, thereby freeing up money for other types of consumption. There is also a wealth effect whereby higher stock and house prices will translate into increased consumption. Through these channels central banks hope to provide some boost to growth. However the flip side of this policy is that investors can anticipate lower returns on their savings, unless they want to hold exceptionally risky assets. This is the idea of there being a savings glut, or as Irwin suggests today, a shortage of adequate investment opportunities. A savings glut implies an economy that is not producing at its capacity. To cut through the nonsense, savings in an economic sense means not spending. From the standpoint of the economy, it is just as much savings if you put $1,000 in the stock market, a checking account in your bank, stuff it under your mattress, or burn it in your fireplace. Anything that does not involve the purchase of a newly produced good or service means saving. Saying that we have a saving glut means we have an economy that does not generate enough demand to keep the economy at full employment. This is of course the story of secular stagnation that folks like Larry Summers have recently discovered and the problem that some of us pre-mature secular stagnationists have raised for years. The idea that the economy could be subject to an ongoing problem of inadequate demand used to be grounds for eviction from the realm of serious economists. But anyone who is willing to look at the evidence with a straight face really can't escape this conclusion.

Is The Fed Going To Attempt A Controlled Collapse? -- As most Fed watchers know, last week was interesting because Janet Yellen, speaking at IMF came out and said something quite surprising. In a nutshell, she said “It’s not the Fed’s job to pop bubbles”. While many market participants immediately took this to mean, “To the moon, Alice!” and started buying equities hand over fist, there’s another possible explanation for Mrs. Yellen’s proclamation of unwillingness: The Fed could be preparing to do exactly what it said it wouldn’t. Bringing forward the next leg of the cycle, may well be on the Fed’s agenda.

5 Years After the Great Recession, Our Economy Still Far from Recovered - This June marks the five-year anniversary of the end of the Great Recession, but champagne toasts would be distastefully premature, as the U.S. economy remains far from fully recovered. Perhaps unsurprisingly, a March NBC News/Wall Street Journal poll showed 57 percent of surveyed American adults believed the United States was still in a recession (although that is the lowest share of respondents under that impression since early 2008). The Great Recession officially began in December 2007 and ended in June 2009, according to the National Bureau of Economic Research, which determines the start and end dates of U.S. recessions based on a range of economic indicators. Now, five years after emerging from recession, the best metrics of economic health suggest the economy is only between one-third and half of the way to fully recovered. What are the key features of this continued sluggishness in the economy? Early into the recovery, roughly 11 million jobs were needed to restore the unemployment rate to pre-recession levels. Today, that number stands at an improved, but still staggering 7 million jobs needed, according to estimates by both the Economic Policy Institute and the Brookings Institution. Less than 40 percent of the employment shortfall caused by the Great Recession has been closed.

"Don't Worry, Be Happy" Fed Financial Stress Index At Record Low For 3rd Week -- Feeling stressed? Worried about the financial markets? Don't be - the Fed has an index for that. The St. Louis Fed 'financial stress index', constructed from 18 weekly data series (6 interest rates, 6 yield spreads, and 5 others) fell to a record low for the 3rd week in a row signaling all-clear... right? Just one thing, in a world entirely disintermediated by central banking largesse, just how relevant are these 'market' indications of financial stress? As Bloomberg warns, the financial stress index has now been below zero for 130 consecutive weeks, the longest period since 2008.

Current economic conditions -- I am a little slow responding to the stunning revision to the first-quarter GDP estimates that came out two weeks ago, but here are my thoughts about the new estimates. The Bureau of Economic Analysis announced on June 25 that U.S. real GDP fell at a 2.9% annual rate during the first quarter, compared with an initial estimate of 0.1% growth for the quarter that the BEA had initially put out in April. The revision sets a couple of records. For one, it makes 2014:Q1 the worst quarter for GDP since World War II that was not part of an economic recession. The next closest contenders were a drop of almost 2.9% in the second quarter of 1981 and a 2.2% drop in the third quarter of 1973. Each of those was followed by a single quarter of solid GDP growth after which the economy fell into a full-blown recession, constituting some of the evidence behind Jeremy Nalewaik’s claim that the economy often reaches a stall speed just before falling into a recession. A second record was noted by Jason Furman: the estimates of GDP growth for 2014:Q1 represent the largest revision from an advance estimate to a third estimate, as well as the largest revision from a second estimate to a third estimate, in the roughly thirty years the Bureau of Economic Analysis has done these estimates. The biggest single source of discrepancy from the earlier estimates came in health care services, which account for 1/6 of total personal consumption expenditures. Last month the BEA had claimed that health care added 1 percentage point to the Q1 GDP growth rate, whereas the new estimate is that it instead subtracted 0.2 percentage points. Jason Furman explains that the main survey that the BEA uses to track health care spending was not available until this month, and hence there was considerable guesswork in the original estimate. The second most important factor in the revision is that the Q1 deterioration of exports is now seen as even worse than originally reported, with lower exports subtracting 1.2 percentage points from the GDP growth rate. Part of this may be payback for unusually strong export numbers for 2013:Q4. But if it signals a weakening in China or other key trading partners it could be more worrisome.

In U.S. Data, a Baffling Contradiction - The first quarter of this year was the worst for the United States economy since the depths of the Great Recession in early 2009. During the same period, employers hired more people than in any quarter over the last six years, signaling gathering strength in the economy. It is hard to imagine how both of those statements could be true, but they are what government statistics indicate. While the employment numbers have been strong, the government sharply cut its estimate of first-quartergross domestic product late last month. It had previously said the economy declined at an annual rate of 1 percent during the quarter — a small dip that could be explained by severe weather in much of the country. The new figures showed a 2.9 percent rate of decline, the worst since a 5.4 percent drop in the first three months of 2009. What happened? Put simply, a single government survey produced highly dubious numbers. Those who conduct the survey say it was done normally and that nothing suspicious surfaced in the responses. The result was suspiciously low revenue estimates for companies in both health services and food retailing. In May, the Bureau of Economic Analysis of the Commerce Department, which produces the G.D.P. figures, estimated that in the first quarter such spending rose at an annual rate of 9.7 percent before adjusting for inflation. That would have been the largest quarterly increase in 13 years. But the revised estimate released in June said that spending on health care services fell at an annual rate of 0.9 percent. Instead of the largest increase in more than a decade, it was the first decline in nearly half a century, since the third quarter of 1965. That one change accounted for most of the decline in the estimate for overall first-quarter G.D.P.Behind that reversal were the results of a quarterly survey of service providers. The survey, conducted by the Census Bureau, asks 18,000 companies in 11 service industries about their revenue and expenses. Health care providers, including physicians and hospitals, reported a decline in revenue from the previous quarter. Because that survey is supposed to cover all sources of revenue, including money from patients, insurance companies and the government, it is taken as definitive in calculating spending on health care services.

Gross domestic problem - On June 25, the U.S. Bureau of Economic Analysis released its highly anticipated gross domestic product numbers and revised the negative first quarter estimates downward. Increasingly, the fate of presidents and governors as well as macroeconomic policy is tied to these numbers. But as we consider the economic challenges of the 21st century, it is increasingly clear that conventional metrics of growth are inadequate. GDP measures the economic output of a coal plant, but it doesn’t tell us how many children get asthma or tally deaths from coal-related air pollution. As Robert F. Kennedy said in 1968, “Our gross national product now is over $800 billion dollars a year, but … that gross national product counts air pollution and cigarette advertising and ambulances to clear our highways of carnage.” Economists have long known the difficulties in using production as a proxy for progress, but that arcane debate has rarely leaked into the broader public discussion. More than four decades later, the threat of climate changes forces us to confront the question of what we are sacrificing for growth. GDP is a fine measure of the goods and services produced within a country’s borders. However, it does not tell us how sustainable that growth is or at what cost it comes. As a group of social scientists argued in a January issue of Nature, “If a business used GDP-style accounting, it would aim to maximize gross revenue — even at the expense of profitability, efficiency, sustainability or flexibility.” It’s time for the United States to adopt new economic measures that better account for the environmental and social costs of growth.

GDP and the Public Sector - Lew Daly has an interesting, but unfortunately misdirected, critique of the measurement of the public sector's contribution to GDP. He notes several areas, such as infrastructure and education spending, where the government contributes to our well-being, but which are not directly picked up in GDP as contributions from the government. While the point is true, the piece fundamentally mistakes what GDP is and also grossly understates the government's role in the economy. First, GDP is a measure of economic activity. It is not a comprehensive measure of societal well-being and anyone who tries to use it as such is showing off their ignorance. GDP can be thought as being comparable to weight. It is difficult to imagine a doctor doing a medical exam and not wanting to know the patient's weight. It is useful and important information. If a person is 50 percent above or below their ideal weight, it likely means they have a serious health issue. On the other hand, someone could be right at the ideal weight for their body type and still be dying of cancer. Any doctor who ended their check-up with writing down what the scale shows has done some serious malpractice. Similarly, GDP is telling us the value of goods and services the economy produced. It is not telling us whether the pollution that results is killing us, whether it all went to produce weapons and prisons, or whether Bill Gates and his kids pocket it all. We need other measures to evaluate such things, and we have them, but they are not GDP.