QE Has (Nearly) Ended. But How Will The Fed Unwind It? - The Fed’s large-scale asset purchases (LSAPs, popularly known as QE) have been tapering off for some time now and are expected to end this month. But even though the Fed won’t be making any new purchases, it will still have the largest balance sheet in history. All the securities it has purchased in three rounds of QE and Operation Twist are sitting on its balance sheet. And the banking system is awash with the excess reserves created as a consequence of those purchases It is clear now that monetary base creation on this scale does not cause runaway inflation, as was feared by many. And it does appear to have prevented the US from experiencing severe deflation in the aftermath of the financial crisis. But as the US economy recovers, the question arises whether the Fed should start shrinking its balance sheet – unwinding QE. There has been considerable debate about whether the Federal Reserve should unwind QE at all. Some have suggested that they may not be able to, because selling off all those USTs and MBS would cause yields to spike, causing distress to asset holders and the US government. Others have argued that they shouldn’t, because having excess reserves improves the liquidity of banks and protects them from runs. However, the FOMC has made its intention eventually to unwind QE clear. After its September meeting, the FOMC issued a statement outlining the principles and plans for normalization of monetary policy.

FRB: H.4.1 Release--Factors Affecting Reserve Balances--October 9, 2014: Factors Affecting Reserve Balances of Depository Institutions and Condition Statement of Federal Reserve Banks

Fed’s Dudley Says Bets on Mid-2015 Rate Increases Look Reasonable - Federal Reserve Bank of New York President William Dudley said Tuesday the U.S. central bank can likely hold off on raising short-term interest rates until 2015 given the expected path of the economy. “It still is premature to begin to raise interest rates–the labor market still has too much slack and the inflation rate is too low,” Mr. Dudley said. But, he added, “the consensus view” that the Fed will lift its interest rate target off the current near-zero level by the middle of next year “seems like a reasonable view to me.” Mr. Dudley suggested that it is unlikely the economy will heat up in a way that causes the Fed to chart a more aggressive path than most currently expect. “There still is a significant underutilization of labor market resources,” he said, despite clear progress in mending the job market. More broadly, he said “the likelihood that growth will be substantially stronger than the point forecast is probably relatively low.” That said, Mr. Dudley, who also serves as vice chairman of the monetary policy-setting Federal Open Market Committee, also said that the path of central bank policy isn’t fixed. “What we do will depend on the flow of economic news and how that affects the economic outlook. “Firmer growth, higher inflation, and a more rapid tightening of the labor market could cause us to move earlier. Conversely, should economic growth disappoint, the timing of lift-off could be pushed later,” Mr. Dudley said.

Falling Unemployment Alone Not Reason to Raise Rates, Fed’s Kocherlakota Says - Minneapolis Federal Reserve Bank President Narayana Kocherlakota said an improving employment picture alone isn’t reason enough for the central bank to boost interest rates. The central banker also during a press briefing after a speech in Rapid City, S.D., Tuesday said the Fed must put more focus on the rate of inflation. He forecasts the rate will continue to fall short of the central bank target of 2% for the next three years, and until that outlook changes, the Fed shouldn’t be considering raising interest rates. “Just because unemployment is falling that’s not a reason to raise rates,” Mr. Kocherlakota said. “There is no harm in having low unemployment in the country except in so far as that generates wage pressures and that shows up in inflation. But I don’t see that in my inflation outlook.” The central banker is seeing improvements in the labor market and expects a further pick up in the economy next year, forecasting GDP growth for 2015 at 3%. However, he added the low rate of inflation is a signal that people remain out of work because there isn’t enough demand for goods and services in the economy. Mr. Kocherlakota, who is a voting member of the interest-rate setting Federal Open Market Committee, has been one of its strongest advocates for continued aggressive action by the central bank to spur the economy.

Fed Officials to Be Flexible on How They Raise Rates - Federal Reserve officials agreed at their September policy meeting to be flexible in implementing a new plan on managing future interest rate increases. Fed officials decided at the meeting to use new tools when the time comes to raise rates. These include an interest rate the Fed pays banks for the money they deposit at the central bank, called reserves, and the interest it pays money market funds and other non-banks for cash they temporarily park at the central bank. The minutes of the Sept. 16-17 meeting, released with a three-week lag, made clear these plans aren’t set in stone, in part because they’re experimental. “It was emphasized that the Committee would need to be flexible and pragmatic during normalization, adjusting the details of its approach, if necessary, in light of changing conditions,” the minutes said. This flexibility might be especially important in the Fed’s dealings with money market funds through instruments known as overnight reverse repurchase agreements. It will use these trades to draw funds out of the nonbank financial sector in exchange for interest set a quarter percentage point lower than the rate banks get for cash. The Fed has set limits on using these trades, in part because of its inexperience with such instruments and its preference in dealing with banks. Currently, it won’t do more than $300 billion worth of reverse repo trades per day. (The $300 billion number looks big, but is a small fraction of the $3 trillion of reserves the Fed has placed in the financial system and the overall size of its holdings, which is in excess of $4 trillion.)

FOMC Minutes: "Costs of downside shocks to the economy would be larger than those of upside shocks" -- Note: Not every member of the FOMC agrees, but I think this is the key sentence: "the costs of downside shocks to the economy would be larger than those of upside shocks because, in current circumstances, it would be less problematic to remove accommodation quickly, if doing so becomes necessary, than to add accommodation". There was also some discussion about the impact of a strong dollar (weaker exports, lower inflation). From the Fed: Minutes of the Federal Open Market Committee, September 16-17, 2014. Excerpts: Inflation had been running below the Committee's longer-run objective, and the readings on consumer prices over the intermeeting period were somewhat softer than during the preceding four months, in part because of declining energy prices. Most participants anticipated that inflation would move gradually back toward its objective over the medium term. However, participants differed somewhat in their assessments of how quickly inflation would move up. Some cited the stability of longer-run inflation expectations at a level consistent with the Committee's objective as an important factor in their forecasts that inflation would reach 2 percent in coming years. Participants' views on the responsiveness of inflation to the level and change in resource utilization varied, with a few seeing labor markets as sufficiently tight that wages and prices would soon begin to move up noticeably but with some others indicating that inflation was unlikely to approach 2 percent until the unemployment rate falls below its longer-run normal level. While most viewed the risk that inflation would run persistently below 2 percent as having diminished somewhat since earlier in the year, a couple noted the possibility that longer-term inflation expectations might be slightly lower than the Committee's 2 percent objective or that domestic inflation might be held down by persistent disinflation among U.S. trading partners and further appreciation of the dollar. .

The FOMC takes dollar strength into account; liftoff expectations shift to a year from now -- The Fed is finally expressing unease with the world outside the US borders and its impact on the US economy. FOMC Sep-14 Minutes: - "During participants’ discussion of prospects for economic activity abroad, they commented on a number of uncertainties and risks attending the outlook. Over the intermeeting period, the foreign exchange value of the dollar had appreciated, particularly against the euro, the yen, and the pound sterling. Some participants ex-pressed concern that the persistent shortfall of economic growth and inflation in the euro area could lead to a further appreciation of the dollar and have adverse effects on the U.S. external sector. Several participants added that slower economic growth in China or Japan or unanticipated events in the Middle East or Ukraine might pose a similar risk. At the same time, a couple of participants pointed out that the appreciation of the dollar might also tend to slow the gradual increase in inflation toward the FOMC’s 2 percent goal." In a single paragraph the FOMC minutes conveyed the concerns about the rising US dollar and risks of further dollar appreciation due to economic weakness across major economies. Strong dollar hurts US exporters and reduces dollar denominated revenues for firms that conduct a great deal of business abroad. It also puts downward pressure on inflation (see post), elevating disinflationary risks. This is clearly visible in TIPS-based inflation expectations (breakevens) that continue to decline.

Fed Officials Affirm Rate Outlook, but Seek Flexibility - Federal Reserve officials are looking for a new way to reassure investors that they are not ready to start raising interest rates, according to an account of the most recent meeting of the Fed’s policy-making committee released on Wednesday.The Fed, pleased that the economy is improving and more Americans are finding jobs, plans to finish its latest bond-buying campaign at the end of October. But most officials at the September meeting said that they were far from satisfied with the economy’s progress. And the account said some officials expressed concern that the slow growth of other major economies would start to weigh on the United States. The Fed sees a need to replace its guidance that it plans to keep short-term rates near zero for a “considerable time” after the end of its bond-buying campaign. The account suggests that officials are trying to find a new way to say the same thing. Most officials want to preserve the general perception that a first increase is most likely around the middle of the year. But they also are going out of their way to emphasize that the timing could change if job growth either exceeds or disappoints their expectations.“The consensus view is that liftoff will take place around the middle of next year,” William C. Dudley, the president of the Federal Reserve Bank of New York and the influential vice chairman of the Fed’s policy-making committee, said on Tuesday. “That seems like a reasonable view to me. But, again, it is just a forecast. What we do will depend on the flow of economic news and how that affects the economic outlook.”

Esther George Says Fed Should Move Toward Raising Rates – Federal Reserve Bank of Kansas City President Esther George reiterated Monday that a growing economy means the U.S. central bank needs to move toward raising short-term interest rates. “The time has come” for Fed officials to start talking seriously about boosting short-term rates, she said. “Starting this process sooner rather than later is important. If we continue to wait–if we continue to wait to see full employment, to see inflation running beyond the 2% target–then we risk having to move faster and steeper with interest rates in a way that is destabilizing to the economy in the long term.” Her comments came from a speech given in Albuquerque, N.M. The official, who doesn’t hold a voting role on the monetary-policy-setting Federal Open Market Committee, has long been a critic of the U.S. central bank’s ultra-easy-money policies. The Fed has had its short-term interest rate target set near zero since the end of 2008, and most officials expect to keep it around there until sometime next year. The Fed is on track to end its bond-buying stimulus program this month. Ms. George has argued in favor of raising interest rates in past speeches, believing the economy has recovered enough to see monetary policy move back toward more historically normal levels. Ms. George has argued in favor of raising rates because she believes if monetary policy stays at its current levels it could lead to a breakout of inflation and spur financial instability. Top Fed officials like Chairwoman Janet Yellen and New York Fed President William Dudley, however, support the Fed’s aggressive stimulus, and note that inflation has been and remains well under the central bank’s 2% target. Ms. George’s arguments haven’t proved influential with most other central bankers, although a small group of regional Fed bank presidents share her appetite for raising rates.

Fed’s Charles Evans ‘Very Uncomfortable’ With Calls to Raise Rates - Federal Reserve Bank of Chicago President Charles Evans repeated Wednesday his view that raising rates anytime soon would be a major blunder on the part of the central bank. “I look forward to the day when we can return to business-as-usual monetary policy, but that time has not yet arrived,” Mr. Evans said. But he added, “I am very uncomfortable with calls to raise our policy rate sooner than later,” adding “I favor delaying liftoff until I am more certain that we have sufficient momentum in place toward our policy goals.” “We should be exceptionally patient in adjusting the stance of U.S. monetary policy,” he said. Mr. Evans, who doesn’t currently have a voting slot on the monetary-policy setting Federal Open Market Committee, has long been a supporter of aggressive Fed action to help the economy get back on track. Mr. Evans’ concern about the growing talk of rate rises is rooted in his fear that the central bank might be overestimating the economy’s strength. He also notes, as he has in recent remarks, that inflation remains very low. “We ought to get it up to 2% as quickly as feasible,” Mr. Evans said of inflation. And even with Fed efforts, inflation likely won’t hit that mark until sometime in 2018, he said. If inflation lags at 1.5% over a long period it would be a “remarkably negative hit” to the Fed’s credibility, he added. Mr. Evans also said job market gains, while real, haven’t yet erased the damage incurred over recent years.

Fed’s Williams Is Still On Board With Fed Raising Rates in Mid-2015 - Federal Reserve Bank of San Francisco President John Williams said Thursday in a speech that if the economy meets his expectations, it is likely the U.S. central bank will be able to raise rates in the middle of next year. “Based on my current forecast for economic growth, employment, and inflation, it would be appropriate to start raising the fed funds rate sometime in the middle of 2015,” Mr. Williams said. “We still have a way to go to get to full health,” and premature action would get in the way of the recovery effort, he said. That said, Mr. Williams emphasized “the decision to raise rates will be data-driven, not date-driven.” He said, “If the economy or inflation heat up faster than I expect, we should lift rates sooner,” adding, “If progress on these fronts slows, we should wait longer” to push short-term rates higher. And when rate rises do take place, he expects them to be gradual in nature. The official said monetary policy will need to remain very supportive of the economy for a long time to come. He also said he continues to support the coming end of the Fed’s bond-buying stimulus effort, which is likely to conclude this month.

The Fed Shouldn't Raise Interest Rates Too Soon -- My latest column discusses the proper course of Fed policy now that the unemployment rate is below six percent. I argue that the Fed should continue to keep interest rates low due to the considerable slack that remains in the labor market.We learned last Friday that in September the unemployment rate fell below 6 percent. This is, of course, good news. But “irrational exuberance” — to quote a former Federal Reserve chair — over the unemployment rate’s rapid decline may undermine the very recovery the Fed is trying to push forward. How so? By giving additional credence to the argument that the Fed should raise interest rates sooner and faster. It shouldn’t.[...]The fundamental logic of monetary policy is the same as it’s been for years now: Prices aren’t rising as rapidly as the Fed would like them to, and the labor market isn’t using workers to their fullest extent. The Fed is still missing on both sides of its “dual mandate.”Prudence thus dictates a patient return to normal monetary policy. And the unemployment rate falling below 6 percent shouldn’t fundamentally change anything. You can read the column here.

The Federal Reserve Won't Save the Economy for All -- Inflation hawks have been the talk of the town in elite economic circles in recent weeks. More liberal-leaning minds critique their (frankly) unsubstantiated concerns that the Federal Reserve is driving the U.S. economy toward high levels of inflation. Hawks are concerned that high levels of inflation due to expansionary monetary policy will lead to negative economic outcomes for major firms and, in turn, the rest of the American public. Instead of worrying about inflation, which has remained at or below 1.5 percent for a year and a half, many prominent economists argue that we should focus on wage growth and jobs. We have seen profits for corporations rise to nearly pre-recession rates, while the poverty rate is not declining as fast as it should be. It’s clear there are some big policies that need changing: the minimum wage, the corporate tax structure, federal budget priorities, and regulations ranging across industries. So why is there so much focus on the Fed and the inflation hawks that circle it? Is there some policy lever we can pull here that would raise outcomes for the working class? Let’s lay it out on the table: Current economic debates have focused on U.S. and global monetary policy because our fiscal policy problems appear to be inoperable. A Congressional stagnation, of sorts, has led to a fixation on a different institution, the Federal Reserve. But, overall, can this fixation actually translate into outcomes for the middle class? With a gridlocked federal system, where can we push for substantial changes in wages and investment infrastructure that support the working class? Executive orders have their limits, of course. Advancements in cities like Seattle and New York City or states like Maryland have started to take effect. But at some point, a deeper, sustainable change must take place. This is a change in who leads in governance and who leads on policy change.

Forget QE, Send in the Helicopters! -- After the Great Recession had officially began (but prior to the stock market crash of 2008/09) George W. Bush responded to the early signs of economic trouble with a "helicopter drop" in the form of lump sum tax rebates to wage earners to help stimulate the economy. They were provided for in the Economic Stimulus Act of 2008, with support from both the Democrats and the Republicans. The bill was signed into law on February 13, 2008. Most taxpayers received a rebate between $300 to $600 per person (based on adjusted gross incomes from 2007) — and eligible taxpayers also received an additional $300 per dependent child. The rebates were phased out for taxpayers with AGIs greater than $75,000. The total cost of this bill was projected to be $152 billion — just peanuts compared to quantitative easing. The U.S. Federal Reserve used quantitative easing (QE) as another unconventional monetary policy to stimulate the economy. Before the onset of the Great Recession in 2007, the Fed only held a fraction of what it does today in Treasury notes (almost $800 billion). But beginning in November 2008, they started buying up billions in mortgage-backed securities. The Fed bought billions in these securities and Treasury notes every month in what is known as QE1, QE2 and QE3. (Because of its open-ended nature, QE3 had earned the nickname of "QE Infinity".) Currently the Fed holds a total of $2.7 trillion in federal debt (about what JPMorgan has in total assets). But before we talk about the tapering of quantitative easing (or expanding it with "QE4"), we really should be discussing another viable alternative: "helicopter drops". Lately there's been an interesting and ongoing debate, where some have been arguing: rather than using quantitative easing to stimulate the economy, instead, why not use direct cash transfers (like George W. Bush's tax rebates) and give money directly to "people" rather than to banks to boost demand and create more spending — regenerating more growth in the economy.

Fischer Says Fed Officials Will Watch Dollar for Impact on Aggregate Demand - Federal Reserve officials will watch the rising U.S. dollar in the context of its effect on demand for the goods and services produced by the U.S. economy, Vice Chairman Stanley Fischer said Thursday. Stanley Fischer, vice chairman of the Federal Reserve Board of GovernorsReutersMr. Fischer, during an event at the Brookings Institution think tank, said the Fed’s focus is on inflation and employment. “We have to take into account the impact on aggregate demand of the factors that affect aggregate demand, and the exchange rate will, to some extent, affect aggregate demand,” he said. “So that is the channel through which the exchange rate will affect our decisions. It won’t be a separate factor.” The U.S. dollar has been strengthening in recent months against other major currencies, which could hold down inflation and make U.S. exports more expensive abroad. At the Fed’s Sept. 16-17 meeting, “some participants expressed concern that the persistent shortfall of economic growth and inflation in the euro area could lead to a further appreciation of the dollar and have adverse effects on the U.S. external sector,” according to minutes released Wednesday. “I’m sure we’ll talk about it at the next meeting,” Mr. Fischer said.

N.Y. Fed’s Simon Potter: Reverse Repos Effective in Setting Rate Floor - The man responsible for implementing Federal Reserve monetary-policy decisions defended limitations set recently on a new tool designed to help set a floor underneath short-term interest rates. Simon Potter, who leads the bank’s Markets Group, was discussing officials’ decision in September to put new limitations on the bank’s overnight reverse repurchase agreement facility. His comments came from the text of a speech delivered in New York at the Securities Financing Transactions Conference. The tool takes in cash from eligible financial firms. The rate the Fed sets on the transactions is supposed to represent a floor for short-term rates. The reverse repos will be a key part of the toolkit the Fed employs when it decides to raise short-term interest rates, which most expect to happen sometime next year. In September, the Fed capped the individual and total bids available to program participants. The Fed now limits the total overall bid to $300 billion. If that limit is breached, rules kick in that can lower the rate the program pays to program participants, which can lead to the rate offered on the facility to fall under its normal level, affecting other short-term rates. Many market participants said the new limits compromised the ability of the reverse repos to effectively define the baseline for short-term interest rates. In its first big test on the final day of September, quarter-end pressures saw bids overshoot the $300 billion cap, leading investors to get no return on their investment, compared with the five basis points they would have normally earned. Other short-term rates also tilted into negative territory. Mr. Potter said that the Fed can look through these short-term gyrations. “As many market participants anticipated, the aggregate cap did bind on quarter end,” he said. “The auction procedure went smoothly and while rates did trade soft on the quarter end, this was only a temporary phenomenon and there was no evidence of market disruption from the unfilled bids at the auction.”

Fed’s ‘Reverse Repo’ Tool Catches Republican Criticism - –Two senior House Republicans are criticizing the Federal Reserve’s new tool for influencing interest rates, saying it “injects needless uncertainty and volatility” into financial markets and questioning the central bank’s legal authority for employing it. Reps. Scott Garrett (R., N.J.) and Patrick McHenry (R., N.C.) took on the Fed’s reverse repurchase agreement program in a Thursday letter to Fed Chairwoman Janet Yellen that was viewed by The Wall Street Journal. Each lawmaker chairs a subcommittee on the House Financial Services Committee. The Fed has been testing the program for a year as a way to manage short-term interest rates when it comes time to raise them from near zero. The central bank is borrowing cash and lending securities in overnight deals known as reverse repurchase agreements, or reverse repos. The program’s popularity in the markets has grown rapidly. On Sept. 30, 2013, money-market mutual funds and other market players parked about $58.2 billion at the Fed through the reverse repo facility. On that date this year, investors sought to park about $407 billion at the bank through reverse repos, hitting the Fed’s daily cap of $300 billion. Messrs. Garrett and McHenry asked the Fed to explain the “specific statutory and regulatory authority” it has for the program and explain steps it has taken “to ensure that the Federal Reserve’s increasing presence in the repo market will not crowd out other participants in that market.” “We also urge you to let this temporary tool lapse when it expires at the end of this year,”

WSJ Survey: Most Economists Confident in Fed’s Exit Tools - Most economists surveyed by the Wall Street Journal are comfortable with the Federal Reserve’s toolkit for eventually raising interest rates. But nearly all think the central bank will have to make additional changes to its closely watched overnight reverse repurchase agreement facility. Economists also appear increasingly confident the Fed will begin to raise short-term interest rates from near zero in mid-2015, with a near-majority expecting an initial rate hike in June. In the Journal’s monthly survey of business and academic economists, conducted Friday through Tuesday, 62% said they were “somewhat” or “very” confident that the Fed’s exit tools would work as needed to adjust short-term interest rates. About 38% said they were “not very” or “not at all” confident they would work.The Fed’s plan, announced last month, is to target a range for the benchmark federal funds rate and use the interest rate on excess reserves, the money banks park at the central bank, as the primary lever to move rates into that range. An overnight reverse repo facility will play a supporting role by setting a floor under rates. Some analysts are concerned the Fed’s daily limit of $300 billion for the reverse repo facility will make it less effective at supporting rates. In an early test, heavy demand at the end of September caused the repo rate, set at 0.05%, to fall to zero.

Fisher Says Fed Has Overshot Mark On Stimulus - Federal Reserve Bank of Dallas President Richard Fisher said the Fed has “overshot the mark” with its stimulus policy, creating an ebullience in credit markets that he likened to the effect of “beer goggles” on college students. Mr. Fisher also said wage inflation may soon show up in data, leading to price inflation earlier than most economists anticipate. Speaking at a meeting of the Council for Economic Education, a group that promotes financial literacy at the K-through-12 level, in Dallas, Mr. Fisher said the U.S. economy isn’t facing much “inflationary pressure.” When asked what the Fed’s target for full employment was, he said it was about 5.5%. But, he added, what the Fed was really waiting for in labor markets were signs of wages lifting. In a questions and answers session after the speech, Mr. Fisher said wage inflation was happening in Texas but not at a national level. Nevertheless, he said, recent Texas experience showed that wage inflation could “happen quicker than one might expect.” Rising wages have translated into rising prices in Texas, according to data cited by Mr. Fisher. In a broad overview of the U.S. economy, he said: “We don’t have much inflation, we’re picking up our rate of growth, and unemployment is coming down.” On inflation, Mr. Fisher said he wasn’t concerned that consumer price increases appeared to be retreating from the Fed’s 2% core inflation target. “The key is price stability,” he said. “I know a lot of my colleagues hang their hats on 2%. What I care about is, we’re not going to deflate or going to inflate above 2%. From my standpoint, and I only speak for myself, I’m quite pleased with price stability.”

Fed’s Bullard Worried Markets, Fed Not on Same Page on Rate Outlook - In a speech that offered an upbeat assessment of the economy, Federal Reserve Bank of St. Louis President James Bullard said Thursday he is worried about what he sees as disconnect between what central bankers think will happen with monetary policy, and the view held by many in the market. “When there is a mismatch between what the central bank is thinking and the market is thinking, that sometimes doesn’t end well, because there can be a surprise later on,” Mr. Bullard told reporters. Right now, “the markets are making a mistake” and expect the Fed to maintain its ultra-easy policy stance longer than Fed officials themselves currently expect, Mr. Bullard said. When it comes to these expectations, “I would prefer that those be better aligned than they are.” Most central bankers continue to support raising what are now near-zero short-term rates some time in 2015. Influential officials, like New York Fed President William Dudley, expect that the increase could come around the middle of year, while a small group of Fed officials would like to see rates rise sooner. In his comments to reporters, Mr. Bullard said “I think there’s a risk” in holding off on rate hikes until the middle of the year. “We should act on good news. We’ve got a pretty good performing economy. We should be willing to remove some accommodation,” and it would be better to get this process started and not wait too long, he said.

Fed’s Charles Plosser: Public Has Come to Expect Too Much From Fed - Federal Reserve Bank of Philadelphia President Charles Plosser said Friday that inflation levels that have fallen persistently short of where the central bank wants them to be are not a significant issue to him right now. It’s true that inflation levels are “a little bit low” relative to the Fed’s desire to have price pressures hit 2%, Mr. Plosser said at an appearance in New York. But, “for the most part, I’m not too concerned about that,” he said. Given the huge level of reserves that are currently in the banking system as a result of Fed stimulus activities, the Fed can “create any inflation level we choose,” Mr. Plosser said. He added “it’s very important we remain committed” to hitting the 2% price target, which is likely to happen over time, the policymaker said. Mr. Plosser was addressing the economy’s long-running inability to get inflation back toward levels the central bank would like to see. The weakness of inflation to reach that goal has proved problematic to officials, including Mr. Plosser, who believe the time is soon coming to raise rates. Many Fed officials see inflation weakness as a reflection of the fact that as well as the economy has been doing, underlying weakness, most notably in the job market, still persists. These officials see under-target inflation as a reason to refrain from raising short-term interest rates off of what are currently near zero levels. In a speech Thursday, San Francisco Fed President John Williams said it could take a couple of years before the Fed sees inflation back at 2%. In Mr. Plosser’s formal speech, he reiterated his belief that there are limits to what monetary policy can do for the job market. “I fear that the public has come to expect too much from its central bank and too much from monetary policy, in particular,”

Nobody Understands the Liquidity Trap, Still - Paul Krugman -- A correspondent points me to Bill Gross in 2010, declaring that we are in a liquidity trap — and that therefore the Fed’s expansionary policies won’t create jobs, but will simply cause inflation. There’s only one thing to say: But a lot of people seem to have fallen into that curious fallacy, as I pointed out in the same year. Look, the liquidity trap — which is basically the same as saying that even a zero short-term interest rate isn’t low enough to produce full employment — is a situation in which increasing the monetary base has no effect on aggregate demand, because you’re substituting one zero (or very low) interest asset — monetary base — for another zero or low interest rate asset, short-term government debt. Conventional monetary policy is completely sterile on all fronts. I don’t know why this very simple point is so hard to grasp, but people keep making a hash of it. I have no idea why Cullen Roche thinks that the TED spread has anything at all to do with the question of whether we’re in a liquidity trap; nor do I know what I can do, after all the times I’ve written about it, to make the point more clearly.

Fed's Lacker Slams Fed For "Inappropriate" Bond-Buying, "Distorting Markets & Undermining Independence" - by Richmond Fed head Jeffrey Lacker, op-ed via The Wall Street Journal, Since 2009 the Fed has acquired $1.7 trillion in mortgage-backed securities underwritten by Fannie Mae and Freddie Mac , the mortgage companies now under government conservatorship. Housing finance was at the heart of the financial crisis, and these purchases began in early 2009 out of concern for the stability of the housing-finance system. Mortgage markets have since stabilized, but the purchases have resumed, with more than $800 billion accumulated since September 2012. We were skeptical of the need for the purchase of mortgage assets, even in 2009, believing that the Fed could achieve its goals through the purchase of Treasury securities alone. Now, as the Fed looks to raise the federal-funds rate and other short-term interest rates to more normal levels, that normalization should include a plan to sell these assets at a predictable pace, so that we can minimize our distortion of credit markets. The Federal Open Market Committee’s recent statement of normalization principles did not include such a plan. For this reason, the first author, an FOMC participant, was unwilling to support the principles.The Fed’s MBS holdings go well beyond what is required to conduct monetary policy, even with interest rates near zero. The Federal Reserve has two main policy mandates: price stability and maximum employment. In the past, the pursuit of higher employment has sometimes led the Fed (and other central banks) to sacrifice monetary stability for the short-term employment gains that easier policy can provide. This sacrifice can bring unfortunate consequences such as the double-digit inflation seen in the 1960s and 1970s.

The IMF’s $3.8 trillion warning to the Fed - — A rocky exit from low interest rates by the Federal Reserve risks $3.8 trillion of losses to global bond portfolios, the International Monetary Fund warned Wednesday in its latest global financial stability report. The IMF was at pains to emphasize that it’s not forecasting such losses, but it did point out that tightening in the past has been a key trigger for declines in fixed-income markets. The IMF came up with the $3.8 trillion figure by assuming a rapid adjustment that causes term premiums to go back to historic norms and credit risk premiums to normalize, with moves of 100 basis points each. That would trigger losses by more than 8%, which could “trigger significant disruption in global markets.” The IMF also pointed to the low volatility term structure VIX, -12.15% for the S&P 500, suggesting equities also may be underpricing the risk of higher volatility in the future. It’s these concerns that have led the Federal Reserve to increase their communication to the public, through quarterly press conferences as well as interest-rate and economic forecasts. Observers both inside and outside the Fed expect the first rate hike to occur in the middle of 2015. But there remains considerable debate over the pace of subsequent hikes.

Fed Chair Janet Yellen Has a New York Problem - America’s central bank, the Federal Reserve, has a credibility problem and a management crisis unique to its unusual structure. If the Chair of the Federal Reserve Board of Governors, Janet Yellen, had any real management powers, she would have immediately asked William Dudley, President of the New York Fed, to step down after internal tape recordings revealed that his staff rubber stamps “legal but shady” deals at the big Wall Street banks it supervises. “Legal but shady” and patently illegal dressed up as just shady deals collapsed this Nation’s financial system only six years ago and continues to depress the country’s economic growth.The tapes were released by former New York Fed bank examiner, Carmen Segarra, via the public interest web site ProPublica and public radio’s “This American Life.” Segarra is suing the New York Fed, charging that she was terminated when she refused to change her negative examination of Goldman Sachs – a position given substantive credibility with the release of the tapes. Yellen’s credibility as the head of America’s central bank is undermined by these disclosures because many Americans believe that “the Fed” is the New York Fed because of its gold vault, historic building and decades of guided tours. But the New York Fed is just one of 12 regional Federal Reserve banks over which the Federal Reserve Board of Governors in Washington D.C., chaired by Yellen, oversees in what must be considered a titular capacity.

Hilsenrath Confirms Dovish Fed Talking Down The Dollar -- Federal Reserve officials have become more concerned about weak growth overseas and the impact of a strengthening U.S. dollar on the domestic economy, warns WSJ Fed-whisperer Jon Hilsenrath, adding that, the stronger currency, by reducing the cost of imported goods and services, could hold U.S. inflation below the Fed’s 2% objective. Fed staff also reduced its projection for medium-run growth in part because of these concerns. The minutes showed more clearly than before that concerns about global growth and the disinflationary impact of a strong currency are giving officials additional pause about moving quickly on rates.

The Fed Notices the Dollar -- Well, that was an interesting set of Fed minutes, in much the same way that colon exams are interesting to their unhappy recipients. Your author doesn't intend to engage in a thorough exegesis of the minutes, but there were a number of points which struck him. The shot which hit the market's bow was, of course, the explicit reference to the dollar, and how it might impact both America's external accounts (X-M in GDP accounting) and, of course, the all-important 2% target for the core PCE deflator. We can leave aside comments that the inflation target is really nonsensical- the average for the decade before the crisis was 1.75%, for example- and instead focus on why the Fed chose to raise the issue. The Fed cited the euro, yen and sterling as weakening against the dollar. Hmmm...let's see....the ECB had just announced an asset purchase program, speculation was mounting that the BOJ would add to its own QQE program, and the Fed meeting took place the day before the Scottish referendum, thus putting a significant risk premium on sterling. More broadly, even in the absence of idiosyncratic factors elsewhere (the same sort of idiosyncratic factors, it need not be said, that provided a US tailwind via a weakening dollar for much of the Fed's QE adventures), does it really come as a surprise that the dollar might strengthen as the Fed starts to contemplate its first tightening in nearly a decade? Really? Perhaps Macro Man's reading too much into this, but it looks like one of those cases where those PhD models that assume "all else being equal" might have allowed its range of adjustable factors to be a little too narrow. Either that or, as Yellen herself suggested, the Fed might be able to learn something from markets. Sadly, if the recent dollar rally came as any sort of surprise, the FOMC might have to start with the basics- defining "mine", "yours", etc., because it would appear they have a LOT to learn.

Dollar strength and inflation expectations - The ongoing strengthening of the US dollar could shift the FOMC further into dovish territory. While the labor situation continues to improve, the dollar's recent appreciation has contributed to declines in inflation expectations (based on TIPS breakevens) to multi-year lows.Another way to think about this is that lower inflation expectations are equivalent to higher real interest rates - a form of "market-generated" tightening in monetary conditions. Central banks generally don't like to tighten policy when real rates rise sharply. Part of the reason for weaker inflation expectations has been the decline in commodity prices - which to a large extent resulted from stronger US dollar (as well as slower growth expectations in China). A widely-tracked broad commodity indicator called the Continuous Commodity Index is now at the lowest level since 2010. Moreover, stronger dollar lowers prices of imported goods in the US. After a period of declines last year, growth in import prices finally turned positive this summer, providing support to the CPI. But as the dollar started appreciating, import prices began falling again, lowering US inflation (and inflation expectations). We saw signs of that in August and import prices are likely to be even lower for September. The Fed watches market-based inflation expectations quite closely and the dovish FOMC members may use this as an excuse to press for delays in rate normalization. If the US dollar appreciation continues at the current pace, the FOMC dot-charts will begin to move lower.

WSJ Survey: Economists Downgrade Their Inflation Outlook - Inflation should remain quite low until the end of 2015, say economists surveyed this month by The Wall Street Journal. On average, the forecasters expect inflation—defined as the 12-month percent change in the consumer price index—will end this year at 1.9% and still be running at a mild 2% in the final month of 2015. The projections represent a downgrade to the inflation outlook compared to the results of the April and July surveys. What’s behind the inflation reset? Falling oil prices and a strengthening dollar should combine to hold down price pressures into next year. The Federal Reserve uses the personal consumption expenditures price index as its preferred inflation gauge. But the private economists’ expectations for low CPI inflation through 2015 suggest policy makers will not have to worry about rising inflation when making interest-rate decisions next year. In fact, disinflation worries may be a bigger concern. In a speech Wednesday, Chicago Fed President Charles Evans said, “There is a risk… that inflation expectations themselves could fall—indeed, I would note that longer-dated TIPS break-evens have recently dropped to the lower end of their post-crisis range.”

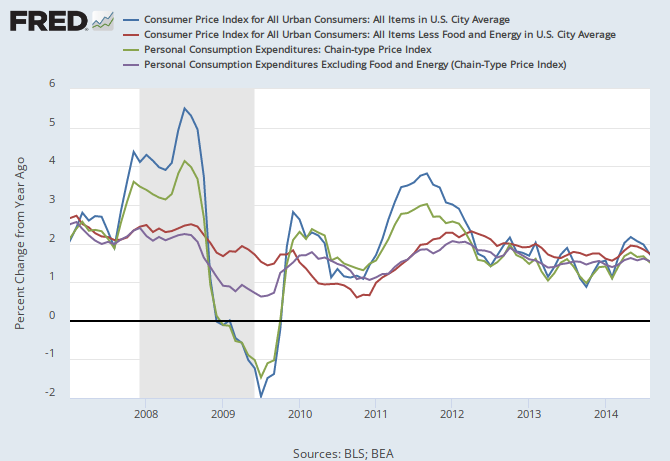

Look Out for Falling U.S. Inflation Expectations -- Here’s another new reason Federal Reserve officials might be wary of raising short-term interest rates very quickly: Inflation expectations in the U.S. are sinking. By one measure they’ve dropped by a greater magnitude in the U.S. than in Europe in the past few months. Market expectations for U.S. inflation in five to ten years have dropped from 2.91% in July to 2.57% in October, according to calculations by Barclays Capital, using trading in options contracts to gauge expectations.(This is based on expected readings of the consumer price index, which Fed officials believe slightly overstate actual inflation.) In Europe, where actual inflation is much lower, expectations for inflation in five to ten years are also lower, but they haven’t fallen as much lately. Expectations there dropped from 2.13% in July to 1.90% in October, Barclays calculates. In a written commentary, Barclays strategist Michael Pond said the drop can be explained in part by falling oil prices and concerns about slow global economic growth. Expected inflation is “now at levels seen only when financial markets were stressed and the US outlook was weak,” he Central bankers pay attention to expectations because they are believed to play an important role in the inflation that actually occurs. When households, businesses or investors expect inflation to rise, they respond by pushing up wages or prices in anticipation of such a move. Falling expectations, in turn, can create downward pressure on inflation. With inflation expectations still well above 2% in the U.S. and the jobless rate falling below 6% in September, it’s very hard to imagine the Fed adding stimulus now. But the drop in expected inflation supports the arguments of Fed “doves” who want to keep rates low for a long time.

Fed’s Lacker Sees No Sign Inflation Expectations Are Drifting From 2% Target - Federal Reserve Bank of Richmond President Jeffrey Lacker, known as a “hawk” for his emphasis on the risk of runaway prices, said Thursday he sees no sign of inflation expectations moving away from the central bank’s 2% target. Bloomberg NewsInflation measures have run below that goal for more than two years, though they have picked up this year. Critics of the Federal Reserve’s easy money policies, including Mr. Lacker, have warned about the risks of higher inflation from the Fed’s efforts to pump up the economy, including bond purchases and near-zero interest rates, since the recession. Mr. Lacker, in prepared remarks to be delivered before business and community leaders here, said he still expects inflation to gradually reach the Fed’s target. “Thankfully, there are no signs that business and consumer expectations for future inflation have drifted away from 2 percent,” he added. “Of course, monetary policy must ensure that we never see such a drift in expectations materialize, for if it does, it will have been too late.”

Fed’s Plosser: Weak Inflation Not A Worry, Prices Back To 2% Eventually - Federal Reserve Bank of Philadelphia President Charles Plosser said Friday that inflation levels that have fallen persistently short of where the central bank wants them to be are not a significant issue to him right now. It’s true that inflation levels are “a little bit low” relative to the Fed’s desire to have price pressures hit 2%, Mr. Plosser said at an appearance in New York. But, “for the most part, I’m not too concerned about that,” he said. Given the huge level of reserves that are currently in the banking system as a result of Fed stimulus activities, the Fed can “create any inflation level we choose,” Mr. Plosser said. He added “it’s very important we remain committed” to hitting the 2% price target, which is likely to happen over time, the policymaker said. Mr. Plosser was addressing the economy’s long-running inability to get inflation back toward levels the central bank would like to see. The weakness of inflation to reach that goal has proved problematic to officials, including Mr. Plosser, who believe the time is soon coming to raise rates. Many Fed officials see inflation weakness as a reflection of the fact that as well as the economy has been doing, underlying weakness, most notably in the job market, still persists. These officials see under-target inflation as a reason to refrain from raising short-term interest rates off of what are currently near zero levels. In a speech Thursday, San Francisco Fed President John Williams said it could take a couple of years before the Fed sees inflation back at 2%.

Tapering is tightening? -- A funny thing has happened since the Federal Reserve announced it would begin cutting back on its bond-buying on December 18, 2013: the yield curve has flattened like a pancake. In particular, 30-year bond yields have dropped by nearly a full percentage point since tapering was first announced: These results ought to surprise those who hold the common belief that asset purchases depress the “term premium” between near and far interest rates. Those worried about slowing inflation should take heart. For better or worse, the changes in nominal interest rates are not really being driven by changes in inflation expectations so much as changes in real yields. As you can see from this chart comparing yields on 5-year Treasury inflation protected securities against 30-year TIPS, the total change in the slope of the real yield curve is basically the same as the total change in the slope of the nominal yield curve:

Wages and the Fed - Paul Krugman -- My inbox is already starting to fill up with predictions and demands that the Fed accelerate the pace of “normalization” because today’s jobs report was better than expected. But the case for wait-and-see actually remains as strong as ever, and maybe a bit stronger.There are, as I’ve tried to explain, two key points for Fed policy. The first is that we don’t know how much slack there is in the labor market. The second is that the consequences of overestimating slack and waiting too long to raise rates would be relatively minor, while the costs of underestimating slack and hiking rates too soon could be immense. On the first point: we really, really don’t know how much slack there is. Don’t show me your new estimation method and claim that it proves that there is x percent of slack — there are lots of clever people doing clever estimates, they don’t agree, and nobody really believes in econometrics anyway unless it tells them what they want to hear. (Sorry, but that’s reality.) We really won’t know until after the fact, if and when we finally see a notable pickup in inflation, and in particular in wages. On the second point: if the Fed waits too long, inflation might pick up for a while, and getting it back down to target would hurt (although the target really should be higher.) But that’s minor compared with the alternative, of raising rates too soon and then finding that we’ve entered a deflationary trap that’s really, really hard to exit. If you’re at the Fed, would you rather wake up and discover that core inflation has risen to 3 percent or that you’ve become Mario Draghi? So, what did we learn about inflation from the latest employment report? Here’s wage growth:

Fed Watch: Is There a Wage Growth Puzzle? -- Justin Wolfers says there is, and uses this picture: to claim:This puzzle isn’t entirely new, as the usual link between unemployment and the rate of wage growth has totally broken down over recent years. The recent data have made a sharp departure from the usual textbook analysis in which a tighter labor market leads to faster wage growth, and subsequent cost pressures feed through to higher inflation. But has the link between wage growth and unemployment "totally broken down"? Eyeball econometrics alone suggests reason to be cautious with this claim as the only deviation from the typical unemployment/wage growth relationship is the "swirlogram" of fairly high wage growth relative to unemployment through the end of 2011 or so. But is this a breakdown or a typical pattern of a fairly severe recession? While, it might seem unusual if you begin the sample at 1985 as Wolfers did, so let's see what the 1980-85 episode looks like: Same swirlogram. Compare the two recessions: Fairly similar patterns, although in the 80-85 episode there was more room to push down the inflation expectations component of wage growth. It would appear that in the face of severe contractions, wage adjustment is slow. Now consider the 1985-1990 period: Notice that wage growth is stagnant until unemployment moves below 6% - past experience thus suggests that we should not expect significant wage growth until we move well below 6% (you could argue the response actually began at 6.5%). Thus, it is premature to believe that there has been a breakdown in this relationship. So far, the response of wages is exactly what you should have expected in light of the 1980's dynamics. Which leads to two points:

- I am no fan of Dallas Federal Reserve President Richard Fisher. That said, he did not pick 6.1% out of a hat when he said that was the point at which wage growth has tended to accelerate in the past. That number fell out of his staff's research for a reason and surprises me not one bit.

- There is a reason the Fed picked 6.5% unemployment for the Evan's rule. There was absolutely no chance that that would be a meaningful number as far as labor market healing is concerned.

Fed Watch: The Labor Market Conditions Index: Use With Care -- I was curious to see how the press would report on the Federal Reserve Board's new Labor Market Conditions Index. My prior was that the reporting should be confusing at best. My favorite so far is from Reuters, via the WSJ:Fed Chairwoman Janet Yellen has cited the new index as a broader gauge of employment conditions than the unemployment rate, which has fallen faster than expected in recent months. The index’s slowdown over the summer could bolster the argument that the Fed should be patient in watching the economy improve before raising rates.But its pickup last month could strengthen the case that the labor market is tightening fast and officials should consider raising rates sooner than widely expected. Many investors anticipate the Fed will make its first move in the middle of next year, a perception some top officials have encouraged. Translation: We don't know what it means. Now, this is not exactly the fault of the press. The Fed appears to want you to believe the LCMI is important, but they really don't give you reason to believe it should be important. They don't even release the LCMI - the charts on Business Week and US News and World Report are titled erroneously. The Fed releases the monthly change of the LCMI, as noted by Business Insider. But wait, no that's not right either. They actually release the six-month moving average of the LCMI, which means we really don't know the monthly change.1 What the Fed releases might actually be more impacted by what left the average six months ago than the reading from the most recent month. And you should recognize the danger of the six-month moving average - the longer the smoothing process, the more likely to miss turning points in the data. Unless of course the Fed released the raw data to follow as well. Which they don't.

Punished for the Dollar's Virtue? - Paul Krugman -- I rarely disagree with Jared Bernstein, and actually agree with most of his latest post. Yes, the persistent US trade deficit is a problem for achieving full employment, and we should have a weak-dollar, not strong-dollar policy. But is the dollar’s reserve-currency status the root of the problem? I have long argued that reserve-currency status is a much overrated phenomenon — it’s not actually a significant benefit to the country that issues the currency, even aside from the employment issues. But I’m also not convinced that it’s that big a deal when we try to understand persistent trade deficits. After all, we’re not the only country that has run persistent external deficits: We do have things that cause a global savings glut to spill into America — a big, deep financial market, with lots of players willing to create what look like safe assets, a general sense that America is the refuge of last resort, and so on. But Britain offers many of the same things, and has in fact a comparable record of persistent capital inflows and deficits; while Australia has run really big external deficits for a very long time. As a policy issue I don’t think this matters too much — we should seek a weaker dollar. But I don’t think phrasing it in terms of the reserve currency status is helpful.

The Long Cryptocon - Paul Krugman -- At the end of 2013 I wrote a post titled “Bitcoin is evil,” riffing off Charlie Stross’s “Why I want Bitcoin to die in a fire.” Charlie and I both keyed in on the obvious ideological agenda: Bitcoin fever was and is intimately tied up with libertarian anti-government fantasies. So how’s it going? Bitcoin prices are down by two-thirds from their peak, and Izabella Kaminska, who has stayed with the subject, finds the sad story of a gullible rube who appears to have impoverished himself by believing in the hype. She comments: Some extremely wealthy libertarians have a lot to answer for if these sorts of ppl lose all due to believing in them But this is nothing new. Back in 2012 Rick Perlstein published an eye-opening piece titled The Long Con, in which he documented the close association that has always existed between right-wing organizing and direct-mail commercial scams — in fact, it’s pretty much impossible to tell where one ends and the other begins. Send us money to keep Obama from imposing Sharia law; invest in this sure-fire scheme to profit from the coming hyperinflation. Was Glenn Beck selling paranoid politics or Goldline? Yes. Bitcoin may be sold as a technical marvel, and it does indeed solve an interesting information problem — although it’s not at all clear whether solving that problem has any economic value. But the psychology and sociology of the phenomenon are the same old same old.

Right now, the US is a 1% growth economy – JPMorgan -- President Obama has been worrying about the wrong “1%.” More attention should be paid to a US economy where potential GDP growth may have fallen to levels more commonly associated with sclerotic Europe and Japan. The one-handle. From JP Morgan economist Robert Mellman: A 2013 Special Report by J.P. Morgan examined the prospects for US potential real GDP growth (how fast the economy would grow without putting downward pressure on the unemployment rate), and concluded that it was probably slowing to only 1.75%. This was calculated by combining a 0.5% potential growth rate for the labor supply and a 1.25% growth rate for labor productivity. This still seems to us like a reasonable forecast of potential growth over the next several years, but labor supply and labor productivity growth have fallen below these estimates, both over the past year and over the past three years. The actual performance of the economy suggests that potential GDP has been increasing at a pace below 1.25%. The supply side of the economy has disappointed already-modest expectations. Whatever the adverse effects of slow potential growth, it has allowed a rapid decline in the unemployment rate despite only middling real GDP growth. From the point of view of improving job prospects for those looking for work, weak labor force growth (less competition for jobs) and weak labor productivity (strong growth of labor demand relative to real GDP) has proved to be a very helpful combination.

Why is the recovery so weak? It’s the austerity, stupid. - Welcome to Austerity U.S.A., where the deficit is back below 3 percent of GDP and growth is still disappointing—which aren't unrelated facts. It started when the stimulus ran out. Then state and local governments had to balance their budgets amidst a still-weak economy. And finally, there was the debt ceiling deal with its staggered $2.1 trillion of cuts over the next decade. Add it all up, and there's been a big fiscal tightening the past few years, something like 4 percent of potential GDP. Indeed, as Paul Krugman points out, real government spending per capita has been falling faster now than any time since the Korean War demobilization. And, as you can see above, all this austerity has been hurting GDP growth since 2011. It shows the Hutchins Center's new "fiscal impact measure," which looks at how much total government tax-and-spending decisions have helped or harmed growth. The dark blue line is what policy has actually done, and the light blue one is what a neutral policy would have done. So, in other words, if the dark blue line is below the light blue one, like it has the last three years, then policy has subtracted from growth.

We can’t return to a ‘normal’ economy, but we can recognize our challenges and keep moving ahead. - Galbraith - Last month’s job gains extended America’s longest run of private-sector job growth and put unemployment back below 6 percent. Yet the labor force and the ratio of employment to population remain way down, and economic growth has been slower than in past expansions. It has been a mixed picture, without disaster but not without disappointment. “Secular stagnation” has become a fashionable view. But this phrase from the 1940s refers mainly to business psychology, suggesting that a better mood would bring a happier economic result. This is too easy. There are material reasons why we have done as well as we have — and also why we likely won’t see full recovery on the familiar model. Consider aging; the workforce falls as baby boomers retire. But this isn’t a bad thing, as many think; actually it’s been a big advantage. So long as older workers can retire — as long as Social Security, Medicare, and Medicaid continue to supply them with income and health care — they become a potent source of purchasing power, and this helps the economy achieve a new balance. The same goes for unemployment insurance, food stamps, and other programs that ward off destitution. Social insurance works; we should take note and be grateful. Yet these programs remain under threat. If they are cut, the support they give to the economy will decline.

Pavlina Tcherneva rightly says it is better to support labor income in a recovery rather than the financial sector. - The title of this post describes the main message of Pavlina Tcherneva’s research. This video is a “must see”. If her message becomes part of the policy approach for the next recovery, we will see much better net social benefits for society after the next recession. (video link)

Explaining “The most important chart about the American economy you’ll see this year” -- Pavlina Tcherneva’s chart has been getting a lot of play out there: Vox/Matthew Yglesias labeled it “The most important chart about the American economy you’ll see this year.” Scott Winship at Fortune came back at it on methodological grounds, with the headline “No, the Rich Are Not Taking All of the Economic Pie (In 8 Charts).” He ends up with what he calls the “money chart,” supporting his headline: some of Scott’s corrections help to usefully and informatively explain the situation better, or at least more. But to summarize the changes that are less informative or downright misinformative:

- • The blatant inaccuracy of ignoring cap gains in #5. It completely misrepresents the situation.

- • The omission of recent years in #2 — the very years where the trend is arguably most apparent and egregious. Hiding the elephant under the rug?

- • The blithely dismissive headline of Scott’s first post.

With these combined, I hope Scott can understand why many see his post as an effort to pooh-pooh and obfuscate the whole subject — the very antithesis of “explaining.”Part of that hand-waving, obfuscation, and general chaff-dispersal is the proleptic “but of course you’re right” rhetorical ploy, right up front in Scott’s second paragraph: Let’s stipulate that income inequality is at staggering levels in the U.S., and that income concentration at the top has probably risen (probably) One really must ask: if income inequality is at “staggering” levels, how did it get there…if it hasn’t risen?

U.S. fiscal 2014 budget deficit falls to $486 billion, CBO says - (Reuters) - The U.S. budget deficit fell by nearly a third during fiscal 2014 to $486 billion as federal revenues grew far faster than spending, the Congressional Budget Office said on Wednesday. Releasing preliminary estimates of final budget data for the year ended Sept. 30, the CBO said receipts grew nearly 9 percent from the previous year to $3.013 trillion, while outlays were up 1.4 percent to $3.499 trillion. The resulting fiscal 2014 deficit was down about $195 billion from the $680 billion budget gap recorded in fiscal 2013. The CBO estimated a September budget surplus of $106 billion, up from a $75 billion surplus a year earlier. The U.S. Treasury Department is expected to report final budget data for fiscal 2014 by Oct. 17. The fiscal 2014 deficit is slightly less than a $506 billion gap that the non-partisan agency forecast in August, when it predicted that many companies would reduce tax payments due to uncertainties over tax laws. The CBO has forecast a $469 billion deficit for fiscal 2015, which started on Oct. 1. Later in the decade, it expects deficits to rise again as costs associated with an aging population mount.

CBO Estimate: Budget Deficit declines to 2.8% of GDP From the CBO: Monthly Budget Review for September 2014 The federal government ran a budget deficit of $486 billion in fiscal year 2014, the Congressional Budget Office (CBO) estimates—$195 billion less than the shortfall recorded in fiscal year 2013, and the smallest deficit recorded since 2008. Relative to the size of the economy, that deficit—at an estimated 2.8 percent of gross domestic product (GDP)—was slightly below the average experienced over the past 40 years, and 2014 was the fifth consecutive year in which the deficit declined as a percentage of GDP since peaking at 9.8 percent in 2009. By CBO’s estimate, revenues were about 9 percent higher and outlays were about 1 percent higher in 2014 than they were in the previous fiscal year. CBO’s deficit estimate is based on data from the Daily Treasury Statements; the Treasury Department will report the actual deficit for fiscal year 2014 later this month. A deficit of $486 billion for 2014 would be $20 billion smaller than the shortfall that CBO projected in its August 2014 report An Update to the Budget and Economic Outlook: 2014 to 2024. This is an improvement over the recent estimate. The Treasury will release their fiscal year 2014 report on Friday.

The Deficit Is Down, and Nobody Knows or Cares - Paul Krugman -- The CBO tells us that the federal deficit is way down — under 3 percent of GDP. And Jared Bernstein notes that Obama seems to get no credit. You may ask, what did you expect? But the truth is that a few years ago many pundits claimed that Obama would reap big political rewards by being the grownup, the responsible guy who Did What Had To Be Done. Worse, some reports said that the White House political staff believed this. It was, of course, nonsense on multiple levels. While pundits may like to script out elaborate psychodramas about voter perceptions, real perceptions bear no relationship to their scripts — in fact, a majority think the deficit has gone up on Obama’s watch, while only a small minority know that it’s down.And the deficit scolds themselves are unappeasable — nothing that doesn’t involve severely damage Social Security and/or Medicare will satisfy them. Why, it’s almost as if shredding the safety net, not reducing the deficit, was their real goal. Deficit obsession has been immensely destructive as an economic matter. But it has also involved major political malpractice.

The Federal Deficit is Now Smaller than the Average Since the 1980s - The federal government’s deficit in fiscal year 2014 was $195 billion smaller than last year — clocking in at a shortfall of $486 billion, according to an estimate from the Congressional Budget Office. The deficit was $20 billion smaller than the CBO had estimated as recently as August. The rapid plunge in the deficit has reaped few political dividends for either party just weeks before the November midterm elections. The deficit remains large in absolute levels, and the headline number of $486 billion still draws ample attention from Republicans. At the same time, many Democrats are unhappy with cutting budgets in a weak economy and reducing borrowing when interest rates are low. But measuring the raw deficit only tells part of the story. The U.S. population and economy are much larger today than they were in the 1980s. In fact, adjusted for the size of the economy, today’s deficit is now smaller than the average deficit going back to the 1980s. The 2014 deficit came in at 2.8% according to the CBO estimate, compared to the 3.2% average since 1980. By that measure, President Barack Obama‘s deficit this year is one that would have been acceptable to President Ronald Reagan. During Mr. Reagan’s presidency, the deficit averaged 4% of GDP.

Shrinking Deficit? U.S. Government Debt Jumps By $1.1 Trillion In Fiscal 2014 -- When it comes to the Federal deficit, reliable numbers are as elusive as unicorns. Not that there aren't plenty of numbers out there, but they don't match reality. And reality is ultimately the change in the gross national debt which shows in its unvarnished manner just how much money the federal government actually had to borrow to fill the fiscal holes. Regardless of what has been proffered by the White House, the Congressional Budget Office, and others, the total gross national debt outstanding of the US of A hit $17.824 trillion in fiscal 2014 ended September 30; a jump for the fiscal year of $1.086 trillion. It could have been worse: note how it jumped on October 1, the first day of fiscal 2015, by another $51 billion. That's certainly one elegant way of putting some lipstick on the debt in fiscal 2014 - by kicking part of it into the next fiscal year. But hey, we all do that. From the Treasury Department: The fact that the total debt taxpayers will have to deal with in the future soared by $1.1 trillion in fiscal 2014 is in part due to last year's debt ceiling charade in Congress. Starting in March 2013, when Treasury debt outstanding hit the debt ceiling, the Treasury Department couldn't sell additional debt to bring in the money that the government continued to spend. So it borrowed that money via "extraordinary measures" from other accounts, to be repaid later. Then on October 16 last year, so in fiscal 2014, President Obama signed a deal into law that avoided default. The next day, the gross national debt jumped $328 billion to $17.075 trillion.

Secret Deficit Lovers, by Paul Krugman --What if they balanced the budget and nobody knew or cared? O.K., the federal budget hasn’t actually been balanced. But the Congressional Budget Office has tallied up the totals for fiscal 2014..., and reports that the deficit plunge of the past several years continues. ... Shouldn’t we be making a big deal of the fact that the alleged crisis is over? Well, we aren’t, and once you understand why, you also understand what fiscal hysteria was really about. First, ordinary Americans aren’t celebrating the deficit’s decline because they don’t know about it. That’s not mere speculation... Why doesn’t the public know better? Probably because of the way much of the news media report this and other issues, with bad news played up and good news downplayed if it’s reported at all. This has been glaringly obvious in the case of health reform, where every problem ... has been the subject of headlines, while in right-wing media — and to some extent in mainstream news sources — favorable developments go unremarked. As a result, many people — even, in my experience, liberals — have the impression that the rollout of Obamacare has been a disaster, and have no idea that enrollment is above expectations, costs are lower than expected, and the number of Americans without insurance has dropped sharply. Surely something similar has happened on the budget deficit. ...Deficit scolds actually love big budget deficits, and hate it when those deficits get smaller. Why? Because fears of a fiscal crisis — fears that they feed assiduously — are their best hope of getting what they really want: big cuts in social programs. ...

Paul Krugman Still Believes That “the debt” Can Be a Problem for the U.S. - The deficit is now down to under 3% of GDP, and in contemplating that fact, Paul Krugman asks why the deficit hawks aren’t celebrating the precipitous fall from nearly 10% of GDP a few years ago. He then explains that: Far from celebrating the deficit’s decline, the usual suspects — fiscal-scold think tanks, inside-the-Beltway pundits — seem annoyed by the news. It’s a “false victory,” they declare. “Trillion dollar deficits are coming back,” they warn. And they’re furious with President Obama for saying that it’s time to get past “mindless austerity” and “manufactured crises.” He’s declaring mission accomplished, they say, when he should be making another push for entitlement reform. So, he unmasks them and then goes on to say: Yes, current projections still show a rising ratio of debt to G.D.P. starting some years from now, and uncomfortable levels of debt a generation from now. But given all the clear and present dangers we face, it’s hard to see why dealing with that distant and uncertain prospect should be any kind of policy priority. That is, Paul Krugman is saying that

- – he doesn’t think it’s necessary to deal with a possible long-term rising debt-to-GDP ratio now, because of the many other problems we still have to face; but he’s also implying that if the projection of such a rise holds later, then we will have to deal with it at that time;

- – the lowered deficit now is due to both a strengthening economy and some austerity measures, thereby excluding the possibility that it is due to the recovering economy alone, in spite of the fiscal drag from reduced Government spending at the Federal level pulling in the opposite direction; and

- – “. . . uncomfortable levels of debt a generation from now” are a possibility, implying that high levels of debt, and debt-to-GDP ratios mean something to the fiscal sustainability of Government spending in the United States.

Deficit anxiety is not the answer - After a hard road and steady progress, the economic recovery is picking up steam. The unemployment rate fell to 5.9 percent in September, the lowest level since July 2008. Exports are up. Factories are churning out more goods, posting their strongest quarter in more than three years. And the biggest driver of our long-term debt — health-care costs that were on a seemingly inexorable rise for decades — has turned into the biggest driver of our shrinking deficits. I tweeted this good news to my friend Fred Hiatt last week. Unfortunately, he missed the bottom line, devoting his Monday column to a reprise of the deficit anxiety that has shaped the economic debate in Washington since 2010. The Affordable Care Act has already helped slow the rate of growth in health-care costs across the board, putting more money in Americans’ pockets and bringing down projected deficits even as millions more people sign up for health insurance and receive access to Medicaid. The improving economic picture means the deficit has been more than halved and is expected to come in under 3 percent of gross domestic product this year — down from nearly 10 percent in early 2009. The problem with Hiatt’s fixation on what’s going to happen to the budget in 2039 isn’t that high debt-to-GDP ratios don’t have consequences — it’s that deficit angst makes it all too easy for policymakers to ignore the fact that we still need to do more to repair the damage from the Great Recession, to grow wages and help middle-class families feel secure, and to invest in the future. This approach isn’t fiscally reckless; indeed, it’s the only serious way to further improve our economy today and strengthen our balance sheet in the future.

Disinvestment Madness - Paul Krugman -- I’m at an IMF seminar today, discussing infrastructure investment — or actually lack thereof. And this is a good time to think about what we’ve actually done. Consider the situation: real interest rates are extremely low, indicating that the private sector sees very little opportunity cost in using funds for public investment. There has been a lot of slack in the labor market, so that many of the workers one would employ in public investment would otherwise have been idle — so very little opportunity cost there either. This makes a very strong case for sharply increasing public investment in a depressed economy; a case that doesn’t rely on claims that there is a large multiplier, although there’s every reason to believe that this is also true. So, what has actually happened? Public construction spending as a share of GDP, along with the 10-year real interest rate: A brief uptick thanks to the ARRA, then a plunge. This is hugely dysfunctional policy.

Destroying a $30,000 Islamic State pickup truck can cost US $500,000 On Saturday, Oct. 4, Day 58 of the American campaign against the Islamic State, U.S. aircraft carried out nine strikes inside Iraq and Syria, destroying two tanks, three Humvees, one bulldozer and an unidentified vehicle. The strikes also hit several teams of Islamic State fighters and destroyed six of their firing positions. At first glance, that might seem like a lot of damage. Leaving aside the significance of killing Islamic State militants and only looking at equipment, the tanks were worth an estimated $4.5 to $6.5 million apiece and each Humvee cost $150,000 to $250,000, bringing the total value of the equipment destroyed to somewhere between $9.5 and $13.8 million. But that’s less impressive when one considers that each U.S. “strike” against the self-proclaimed Islamic State can involve several aircraft and munitions and cost up to $500,000, according to Todd Harrison, an expert with the Center for Strategic and Budgetary Assessments, a Washington-based defense think tank. Harrison said the cheapest possible strike could cost roughly $50,000 — assuming a single plane dropping one of the cheaper types of bombs. But the majority of airstrikes cost much more, involving F-15s, F-16s, F-22s and other aircraft that cost $9,000 to upward of $20,000 per hour to operate and explosives that cost tens to hundreds of thousands of dollars. Harrison noted that each strike’s price “depends on the distance to the target site, how long it may need to loiter, what type of aircraft is used, and whether it needs aerial refueling (and how many times).”