Fed balance sheet shrinks in latest week (Reuters) - The Federal Reserve's balance sheet shrank in the latest week on lower holdings of mortgage-backed securities and agency debt, Fed data released on Thursday showed. The Fed's balance sheet, which is a broad gauge of its lending to the financial system, stood at $3.342 trillion on May 29, compared to $3.356 trillion on May 22. The Fed's holdings of Treasuries rose to $1.884 trillion as of Wednesday, May 29, from $1.877 trillion the previous week. The Fed's overnight direct loans to credit-worthy banks via its discount window averaged $10 million a day during the week versus $23 million a day the previous week. The Fed's ownership of mortgage bonds guaranteed by Fannie Mae, Freddie Mac (FMCC.OB) and the Government National Mortgage Association (Ginnie Mae) slipped to $1.165 trillion from $1.179 trillion. The Fed's holdings of debt issued by Fannie Mae, Freddie Mac and the Federal Home Loan Bank system totaled $70.89 billion compared with $72.05 billion the previous week.

FRB: H.4.1 Release-- Factors Affecting Reserve Balances -- Thursday, May 30, 2013: Federal Reserve statistical release

Fed Wrestles With Market Expectations About Pace of QE -- Managing market expectations is one of the Fed’s most challenging tasks. If market expectations get out of sync with what the Fed plans to deliver, it could be the source of unpleasant volatility. Fed officials have been struggling of late managing expectations about its plans for the $85-billion-a-month bond-buying program, known as “quantitative easing.” At their policy meeting in May, Federal Reserve officials expressed anxiety about shifting market expectations for the Fed’s $85 billion-per-month bond buying program. “A few members expressed concerns that investor expectations of the cumulative size of the asset purchase program appeared to have increased somewhat since it was launched last September despite a notable decline in the unemployment rate and other improvements in the labor market since then,” according to the minutes of the meeting released last week.As our former college, Greg Ip, now at The Economist notes, “Because markets are forward-looking, bond yields respond to what investors expect the Fed to buy, not just what it does buy. So if the Fed signals QE will continue at a slower pace than investors expected, it will ultimately buy less than expected and yields should go up.” That’s what happened last week.

The Fed's tricky messaging: Tapering is not tightening - The Federal Reserve is famous for its verbal acrobatics, but it is now facing a particularly high hurdle: convincing the markets that doing less actually means doing more. Since September, the central bank has been buying $85 billion in bonds every month, aiming to lower long-term interest rates and boost economic growth. There are signs that it is working – the Dow is at a record high and the housing market is bumping – and the Fed has promised to keep the money flowing until there is “substantial improvement” in the job market. It looks like we’re getting close to that point. Job growth has averaged 200,000 a month for the past six months, and the unemployment rate has dropped a three-tenths of a percent since the program started. Fed officials are now starting to think about how to end the program – and opening a whole new can of worms in the process. But the Fed is worried that as soon as it slows down its bond-buying, the markets will act as if the shop is closed for business, negating the benefits of any stimulus the central bank is still providing. Bernanke has tried to dispel that notion by framing a reduction in purchases as simply a slowdown of the rate of Fed stimulus, rather than actually doing less to stimulate the economy. Tapering, Fed leaders want the world to understand, is not tightening.

QE: Because Nobody’s Got Any Better Ideas - QE: What you’d call a bit of a controversial policy. Asset prices have shot up recovering pre-crisis highs. Meanwhile the real economy – especially those bits that affect the poor and the young – remain deep in a pit of despair. I don’t agree with Frances Coppola on this, but she’s got some good posts accusing QE of making things worse , especially in the UK. (there’s also this excellent subsite for discussion on the topic). And of course we have the insistence – from the reasonable to the reliably demented that this is all a bubble and that the next hard landing will be worse. But I come not to bury QE, but to praise it. Or at least point out that it’s probably better than doing nothing, and that “nothing” seems to be a pretty good description of the other politically-acceptable alternatives globally.First, let’s deal with the “QE distorts prices and changes the behaviour of investors”. This is like complaining that “cars carry people to different places”. It’s not an objection, it’s a description of the WHOLE DAMN POINT of the exercise. A case in point: the recovery of the housing market has been driven by investor demand. And it’s the big institutions – the WSJ link points to 20,000 homes snapped up by Blackstone. This is what happens when the search for income, driven out of Treasuries by low yields turns into activity. This is FoBOR at work (Forced Buyers Of Risk to use Dan Davies‘ term)

Kansas City Fed Wanted to Raise Discount Rate - Federal Reserve officials said they view the pace of economic expansion as “moderate” and voted to maintain its primary credit rate. The Fed’s Board of Governors kept its primary discount rate at 0.75%, according to minutes from meetings on April 8 and April 29, which were released Tuesday. The rate is what banks are charged on short-term loans they receive from the Fed. Eleven of 12 regional banks recommended keeping the discount rate unchanged. Directors from the Kansas City Fed voted to raise the rate to 1.0%, as they have done previously. Directors from the Boston Fed have called for the bank to lower the rate to 0.50% in recent months, but since March have voted with the 10 other regional Fed banks to re-establish the existing rate. Regional Fed bank directors send their request for the discount rate every two weeks, but the Board of Governors makes the final decision. In general, the directors said the economic expansion is “moderate,” with further improvements in the housing sector, modest job growth and a still-elevated unemployment rate. Against that backdrop, most directors recommended maintaining the current primary credit rate.

Fed’s Rosengren Open to ‘Modest’ Cut in Bond Buys in a ‘Few’ Months - A Federal Reserve official who has strongly supported the central bank’s bond-buying stimulus efforts is willing to see the purchases pared back sometime soon if the economy continues to recover at its current pace. “It may be undesirable to abruptly stop purchases, so it may make sense to consider a modest reduction in the pace of asset purchases if we see a few months more of gradual improvement in labor markets and improvement in the overall growth rate in the economy,” Federal Reserve Bank of Boston President Eric Rosengren said in a speech Wednesday. The official noted that he expects the recovery to continue, which suggests Mr. Rosengren, who is also a voting member of the monetary policy-setting Federal Open Market Committee, is joining with other key officials in the expectation the Fed is nearing the day when it can dial down its purchases of Treasury and mortgage bond debt. Mr. Rosengren spoke in the wake of testimony last week by Fed Chairman Ben Bernanke, who also signaled a willingness to reduce the pace of what are now $85 billion in monthly bond purchases. While a number of Fed officials have been hinted that they are gravitating to the view the Fed can soon begin to do less to aid the economy, Mr. Bernanke’s words hit financial markets hard, driving down bond prices and driving up yields, as investors brace for a reduction in the level of central bank stimulus. The Fed’s bond-buying stimulus has aimed to keep yields low to help stimulate growth. Fed officials who have spoken on the matter generally support slowing bond purchases as a prelude to stopping them outright. A number of officials, like New York Fed President William Dudley, have said the central bank could easily increase the asset buying again if the economy warranted that action.

Fed Watch: September Looking Good - Boston Federal Reserve President Eric Rosengren, considered to be on the dovish side of the Federal Reserve, had this to say about the outlook for monetary policy: However, I would also say that it may be undesirable to abruptly stop purchases, so it may make sense to consider a modest reduction in the pace of asset purchases if we see a few months more of gradual improvement in labor markets and improvement in the overall growth rate in the economy – consistent, by the way, with my forecast, which is somewhat more optimistic than that of many private forecasters. A "few more months" I interpret as June, July, and August, which puts the beginning of tapering at the September FOMC meeting. I think that Fed speakers are sending pretty clear signals to prepare for a September policy change. Some big names on Wall Street don't agree. Vincent Reinhart at Morgan Stanley believes the data will push the Fed back to December. The view at Goldman Sachs is reportedly similar. To be sure, the data might cut in that direction, but I think that the bar to tapering might be lower than believed by those looking for a shift in December. We may believe the Federal Reserve's dual mandate argues for a longer period of QE at its current pace, but I am thinking that for the Federal Reserve, the dual mandate has more to do with the lift-off date from ZIRP than the end of QE. They have tended to argue for more or less QE on the basis of "stronger and sustainable" improvement in labor markets, and, given the obvious shift in tone among Fed speakers, I think we have reached that benchmark. At this point, they are just looking for a little more confirmation, in their minds erring on the side of being "too easy." Bottom Line: I think the Federal Reserve is leaning toward a September policy shift. While it is as always data dependent, I think the data will need to be pretty weak to push the Fed to December.

There's a problem with the transmission.... In my last post, I pointed out that QE does not work when the transmission mechanism for monetary policy is impaired because of a damaged and risk-averse financial sector. This caused some confusion among those who think that throwing money at banks automatically makes them lend, so I attempted to explain it on twitter. Predictably, I ended up in an extended discussion first with David Beckworth and then with Andrew Lilico, in the course of which it became clear - to me, at any rate - that not only does QE fail when damaged banks aren't lending normally, but it actually impairs the transmission mechanism itself. This might explain why QE seems to become less effective the more of it you do. It's like hard water. It gradually clogs up its own pipes. To explain this, let me first go through the money creation process in our fiat money system and the ways in which QE influences that process.

What will happen to markets when QE ends? - Davies - Last week’s market reaction to Fed Chairman Bernanke’s suggestion that the FOMC might begin to taper back QE “within a few meetings” represented a trial run for what might happen when central bankers really do remove the punch bowl at some point in the future. The largest reaction came in the most leveraged markets (notably the Nikkei, which fell by 6.5 per cent), but there were simultaneous across-the-board declines in global bonds and equities. When the Fed ended QE1 and QE2, there were declines in the S&P 500 index of 15 per cent and 23 per cent respectively. These events, however, proved to be only minor fluctuations in the great bull market, which quickly resumed when the central banks announced new asset purchases. Many analysts [1] believe that QE has caused a major bubble to appear in asset prices, the full extent of which will be unveiled only when the central banks start to shrink their balance sheets. Others reply that the rise in both bond and equity prices has been justified by economic fundamentals.This is probably the most important debate in the financial markets today, with enormous ramifications for both policy makers and investors. Bubbles are notoriously difficult to identify in real time, and it is wise not to be too dogmatic about this. However, I would like to comment on three elements of the debate.

Looking forward to the end of QE - - Good piece in the FT online today by Gavyn Davies on what wil happen to markets when QE (quantitative easing) ends. As we have witnessed last week, comments on the potential end to QE can generate significant volatility in financial markets. But there is something in this debate that still confuses me and it has to do with the interpretation that some make of the end of QE. QE will end one day, this must be the assumption of anyone who understands monetary policy. The day the recovery is strong enough, when central banks feel that the economy is close enough to full employment we will see a normalization of monetary policy conditions. From an expansionary stance we will move towards a more neutral stance. This has always been the case in the past although we used to think only in terms of interest rates and not QE. One way to see how this will happen is the chart below (which I am borrowing from a recent Brad DeLong blog post). This is a plot of long-term (10 years) and short-term (3 months) interest rates for the US. The pattern that we see after each of the last recessions is that short-term rates deviate from long-term rates as a sign that monetary policy is hitting the accelerator (the yield curve becomes steep). A few years after the recession is over, short-term rates are raised and they reach a level similar to long-term rates. After that we see the two continuing at similar levels until the next recession comes.

What would the Fed's policy "step down" look like? - A number of economists are trying to read into the meaning of Bernanke's statement last week. The comment that put a damper on the relentless equities rally and sent prices of treasuries lower. In particular the comment "we could take a step down in our pace of purchases" at the next FOMC meeting is causing angst in the investor community (see post). But what would such "tapering" in monetary expansion look like? The most likely outcome is a shift from $85 billion of purchases a month to something like $60 billion. Here is the impact such a policy would have on the central bank's portfolio of securities.

Will the Expected End of QE Lead to a Bond Meltdown? - Yesterday, bonds fell sharply due to stronger-than-expected housing price and consumer confidence reports. That reflects the belief that the economy is mending, and as a result, the Fed will deliver on its promise to dial back and then end QE. Ten year Treasury yields rose to the 2.10%-2.11% level. Various commentators claim that rates will zoom higher either right over that point or at 2.25%. Russ Certo of Brean Capital claim’s there’s a “technical vacuum” at 2.11% that will lead 10 year rates to gap up to 2.25%. And Bruce Krasting wrote over the long weekend about an apparently widespread concern among investors, that convexity in mortgage-backed securities market could produce a nasty feedback loop, or convexity vortex, at 10-year Treasury yields of around 2.25%. The guts of his argument, starting with a quote from a hedgie buddy: Some familiar with it say the vortex is 19 bps away..2.2% on ten year treasury, 3% on the CMM..if breaks, MBS holders subject to extension and duration risk. Would now have to increase convexity hedging. Would lead to price gaps and significant selling. With shortage of treasuries due to bernank and co. and low liquidity, could be very disruptive.Krasting did say this source was a perma bond bear, so he consulted a perma bond bull, who remarked: I don’t disagree – I would guess we have a huge concentration of mortgages that would go out of the money at 2.25% 10yr UST, slowing prepays, extending servicer portfolios, bringing on longer duration UST selling ……So we have bulls and bears agreeing. Must be true, right? Maybe not. First remember we’ve had some dire bond market calls in the past produce some short term perturbations but none of the expected follow-through. The freakout over the S&P downgrade of US Treasuries saw the bonds increase in price shortly after the event took place. Reader AU, commenting on the Krasting post, recalled November-December 2010. The QE2 FOMC meeting coincided with the midterm elections, and bond prices fell in the following weeks. There were similar concerns that convexity would beget more selling, but after the correction, prices settled down.

Debating Helicopter Money - Vox has published an excellent summary account of a debate between Adair Turner and Michael Woodford (skilfully moderated by Lucrezia Reichlin) on helicopter money. My line on helicopter money has been that it is formally equivalent to fiscal expansion coupled with an increase in the central bank’s inflation target (or whatever nominal target it uses), and so adds nothing new to current policy discussions. I think the Woodford/Turner debate confirms that basic point, but as this may not be obvious from the discussion (it was a debate), let me try to make the argument here. Turner calls his proposal ‘Outright Money Financing’ (OMF), so let’s use that term to avoid confusion with other versions of helicopter money. Under OMF, the central bank would decide to permanently print a certain amount of extra money, which the government would spend in a way of its choosing. The alternative that Woodford proposes is that the government spends more money by issuing debt, but the central bank buys that debt by printing more money (Quantitative Easing), gives any interest it receives straight back to the government, and promises to ‘never’ sell the debt. (If it reaches maturity, it uses the proceeds to buy more.) Let’s call this Indirect Money Financing (IMF). If everyone realises what is going on in each case, and policymakers stick to their plans, the two policies have the same impact.

Steve Keen: Is QE Quantitatively Irrelevant? - Yves here. Some readers still equate quantitative easing with “printing money”, and Keen’s post explains what (little) QE actually does and does not accomplish. America is a land of contention, and one of the most contentious topics here (I’m in Seattle as I write) is the impact of the Federal Reserve’s policy of “Quantitative Easing” – otherwise known as ‘QE’. The Federal Reserve has committed to spending $85 billion every month buying a wide range of bonds from banks, until such time as the US unemployment rate falls below 6.5 per cent.The Fed has implemented this policy because it believes it is the best way to stimulate demand in a depressed economy. Its critics oppose it because they believe this massive amount of ‘money printing’ must inevitably lead to ruinous inflation. I reckon they’re both wrong, and in a seriously wonky post I’ll try to explain why, using my modelling program Minsky.

At Least One Reason Why People Shouldn't Hate QE - Atlanta Fed's macroblog - You might not expect me to endorse an article titled "The 7 Reasons Why People Hate QE." I won't disappoint that expectation, but I will say that I do endorse, and appreciate, the civil spirit in which the author of the piece, Eric Parnell, offers his criticism. We here at macroblog, like our colleagues in the Federal Reserve System more generally, pride ourselves on striving for unfailing civility, and it is a pleasure to engage skeptics who share (and exhibit) the same disposition. Let me instead appropriate some of Mr. Parnell's language. It is worthwhile to explore some of the reasons that people do not like QE from someone who does not share this opposing sentiment. In particular, let me focus on the first of seven reasons offered in the Parnell post:First, a primary objection I have with QE is that it results in a government policy making and regulatory institution in the U.S. Federal Reserve directly determining how private sector capital is being allocated... in recent years, the Fed has dramatically expanded its policy scope into areas that are normally the territory of fiscal policy. This has included specifically targeting selected areas of the economy such as the U.S. housing market including the aggressive purchase of mortgage backed securities (MBS) since the outbreak of the financial crisis. This statement seems to presume that monetary policy does not normally have differential impacts across distinct sectors of the economy. I think this presumption is erroneous.

Here’s Why the Titans of Finance and Economics Are Wrong - There is zero correlation between the Fed printing and the money supply. If you don’t believe this, you owe it to yourself to study up on monetary policy until you do. This is an issue that brings them out of the bunker like no other in economics. But if you are an investor, trader or economist, understanding—and I mean really understanding, not just recycling things you overheard on a trading desk or recall from Econ 101—the mechanics of monetary policy should be at the top of your checklist. With the US, Japan, the UK and maybe soon Europe all with their pedals to the monetary metal, more hinges on understanding this now than ever before. And, as we saw recently, even many of the Titans of finance and economics have it wrong. “Wrong? You’re saying they’re wrong? They have tons of money. They have long track records. I mean, they’ve seen it all. How can you say that? That’s just arrogant. Besides, did I mention they have tons of money?”

Fed Watch: More Uncertainty? - I was reading this Business Insider report on an analyst's mea culpa on a bad trade when this jumped out: Last week, we advised investors to add to their 7s/30s and 10s/30s yield curve steepening positions with the view that Chairman Bernanke would calm expectations for tapering by September this year – helping keep rates and volatility low. These curves have since flattened back to the levels at which we suggested investors enter steepeners. Given the uncertainty Bernanke injected into the market, we suggest investors pare down positions to more sustainable levels. At the same time, we keep to our core steepening view. I find it curious the analyst believes that Federal Reserve Chairman Ben Bernanke increased uncertainty. I think it was just the opposite. Prior to Bernanke's remarks, opinion on policy was scattered among some looking for the Fed to scale back asset purchases as early as June and as late as 2014. Bernake narrowed that range to September as a likely date, and cleared the way for New York Federal Reserve President WIlliam Dudley and Boston Federal Reserve President Eric Rosengren to point us at September as well. Overall, it looks like more, not less, certainty. Perhaps market participants are unhappy with the path Bernanke laid out, but that path is more obvious than it was a week ago.

Inflation, deflation and QE - Inflation is dead. Well, in the US, anyway:What is curious is that the US is doing QE. Lots of it. Which is supposed to raise inflation, isn't it? Then there is Japan. Japan recently embarked on an extensive QE programme designed to raise inflation to 2%. Here's the path of Japanese inflation: It's very easy to see where QE started. It's when inflation fell off a cliff. Well, ok, it might have done that anyway, I suppose. Correlation doesn't equal causation, and all that. But it is curious. Japan has, of course, done QE before. A look at the inflation path for the period 2001-2006, when Japan was doing QE, doesn't suggest a close relationship between QE and inflation. The initial impact seems to have been deflation, though again we could do with a counterfactual. But for the rest of the period QE seems to have had little impact on inflation. In fact a researcher at the IMF concluded that QE's effect on inflation was small. The UK does appear to buck the trend, since it experienced above-target inflation ever since commencing its QE programme, still the largest in the world relative to GDP although it is currently suspended. Though it is interesting that throughout 2012, when the Bank of England was doing QE, CPI was falling - it picked up in November 2012 when QE stopped: But this isn't quite what it appears. The UK's CPI was pushed up by tax rises, student tuition fee increases (what on EARTH are they doing in measures of CPI anyway?) and above-inflation rises in near-monopoly privatised utilities which are subject to government price controls. Yes, really. Government not only allowed those above-inflation rises, it encouraged them in the name of investment - though why it thinks utilities should invest for the future now when it isn't doing so itself is a mystery.

The 4% Inflation Target: Two Other Points - I’m a little late to this 4%-inflation-target party set off by the economist Lawrence Ball (whose work shows up here more than random chance would predict) and picked up by Paul K. I have a few things to add to the discussion, but first, a very brief recap of this simple, sensible argument. Ball contends that when the central bank maintains a 2% target, the economy is over-exposed to zero-lower-bound (zlb) risk when we hit a downturn. Since the real interest rate (r) is the nominal rate (nom) minus inflation (inf), or r=nom-inf, then, as Ball points out, since nom can’t go below zero, the real rate can’t fall below -inf. In this way, the problem with “…low inflation is that it raises the lower bound on the real interest rate.”That’s only a danger if the real rate needs to go below –inf, so one important question here is “how likely is that?” The answer, according to Ball and others, is “more likely than a lot of people think,” and there’s a lot of analysis showing this to clearly be the case in the great recession we’re still slogging our way out of.Thus, the danger is not just inflation that’s “too low” such that it invokes zlb risk. It’s low inflation in tandem with a recession deep enough that we need real interest rates to go well below zero. One lesson to take from this research is that low inflation and asset bubbles are a particularly toxic combination, and they’re increasingly common.

PCE Price Index Update: Sorry Fed, The Disinflationary Trend Continues - The May Personal Income and Outlays report for April was published today by the Bureau of Economic Analysis. The latest Headline PCE price index year-over-year (YoY) rate of 0.74% is a decrease from last month's adjusted 1.01%. The Core PCE index of 1.05% is decrease from the previous month's adjusted 1.17%. The continuing disinflationary trend in core PCE (the blue line in the charts below) must be troubling to the Fed. After years of ZIRP and waves of QE, this closely watched indicator has been consistently moving in the wrong direction for over a year. It has contracted month-over-month for ten of the last 13 months since its interim high of 1.96% in March of 2012 and is now approaching half that YoY rate. The first chart shows the monthly year-over-year change in the personal consumption expenditures (PCE) price index since 2000. I've also included an overlay of the Core PCE (less Food and Energy) price index, which is Fed's preferred indicator for gauging inflation. I've highlighted 2 to 2.5 percent range. Two percent had generally been understood to be the Fed's target for core inflation. However, the December 12 FOMC meeting raised the inflation ceiling to 2.5% for the next year or two while their accommodative measures (low FFR and quantitative easing) are in place. I've calculated the index data to two decimal points to highlight the change more accurately. For a long-term perspective, here are the same two metrics spanning five decades.

With All Eyes on Fed, Prices Barely Rise - WSJ.com: Inflation is slowing in the U.S. and elsewhere, despite central banks' historic easy-money programs that some have argued could push prices much higher. A key gauge of inflation fell in April to its lowest level on record, a reduction that could take pressure off the Federal Reserve to wind down an $85 billion-a-month bond-buying program despite other signs of a strengthening economy. Core prices, which exclude volatile food and energy costs, rose 1.1% in April from a year earlier, the Commerce Department said Friday. That matched the smallest increase in underlying prices since the agency began tracking them in 1960. Overall prices rose even less—just 0.7% in April from a year earlier. A strengthening economy should boost inflation over time as consumers demand pay raises and firms gain latitude to boost prices. But considerable slack across the economy—due to high unemployment and weak demand—have kept inflation tame during the four-year recovery.It isn't clear how Fed officials will respond to the drop in price pressures. Minutes of the Fed's latest policy meeting show officials believed the drop in inflation pressures was temporary and expected price measures to move back toward the central bank's 2% target. But the latest readings could allow the Fed to keep its foot on the accelerator longer. Core inflation reached its current level three other times during the current recovery, in late 2010 and early 2011, a period that coincided with the Fed's launch of an earlier bond-buying program

Behind the Numbers: PCE Inflation Update, April 2013 - Dallas Fed - The headline, or all-items, PCE price index fell at an annualized rate of 3 percent in April on the heels of a 1.4 percent annualized rate of decline in March. A steep decline in the price index for gasoline and other motor fuel—8.1 percent at a monthly rate or about 64 percent annualized—was the biggest drag on the headline index. Gasoline and other motor fuel contributed about –3.5 annualized percentage points to April’s headline rate, in the sense that an index of all items except gasoline and motor fuel would have increased at an annualized rate of about 0.5 percent. As we expected in last month’s Inflation Update, the 12-month headline inflation rate has now dipped below 1 percent, falling to 0.7 percent in April from 1.0 percent a month earlier. The six-month headline rate fell to an annualized –0.1 percent from 0.7 percent in March. Similar to last month, while gasoline was the main culprit behind the decline in the headline index, it must have many accomplices since our Dallas Fed trimmed mean inflation rate—which excludes all extreme price swings—posted a –0.1 percent annualized rate in April. A monthly change that annualizes to just a tenth of a percent is, for all practical purposes, effectively zero (before annualizing, the trimmed mean inflation rate for April was –0.01 percent); even so, April’s reading is the first negative trimmed mean rate we’ve seen in the history of the series, which begins in 1977.

Two Measures of Inflation: Core PCE at Its All-Time Low - The BEA's Personal Consumption Expenditures Chain-type Price Index for April shows core inflation well below the Federal Reserve's 2% long-term target at 1.05%, the lowest Core PCE ever recorded; the previous all-time low was 1.06% in March 1963, fifty years ago. The Core Consumer Price Index release earlier this month, also data through April, is significantly higher at 1.72%. The Fed is on record as using PCE as its primary inflation gauge. Elsewhere the Fed stresses the importance of longer-term inflation patterns, the likelihood of persistence and the importance of "core" inflation (less food and energy). Why the emphasis on core? The October 2010 core CPI of 0.61% was the lowest ever recorded, and two months later the core PCE of 1.08% was an all-time low, until today's 1.05%. However, we have seen a significant divergence between the headline and core numbers for both indicators, especially the CPI, at least until a few months ago, when energy prices began moderating. The latest headline CPI and PCE are both well off their respective interim highs set in September. This close-up comparison gives us clues as to why the Federal Reserve prefers Core PCE over Core CPI as an indicator of its success in managing inflation: Core PCE is lower than Core CPI and less volatile. Given the Fed's twin mandates of price stability and maximizing employment, it's not surprising that in the past the less volatile Core PCE has been their metric of choice. On the other hand, the disinflationary trend of late give PCE additional significance as support for a sustained policy of quantitative easing. The Bureau of Labor Statistic's Consumer Price Index and The Bureau of Economic Analysis's monthly Personal Income and Outlays report are the main indicators for price trends in the U.S. The chart below is an overlay of core CPI and core PCE since 2000.

Fed Not Constrained Amid Tame Inflation - Inflation is getting tamer, a development that will surely fuel the debate over the Federal Reserve‘s bond-buying. “Core” prices, a closely watched measure of inflation that excludes food and energy costs, were essentially unchanged in April, the Commerce Department said Friday. Core prices rose less than 0.1% from March. It was the first time since December that the index failed to budge. Overall prices–including volatile food and energy costs–slipped by 0.3% in April from the prior month. It was the second consecutive month that overall prices fell. Friday’s report–coupled with recent data suggesting a mild slowdown in hiring–will factor into the debate within the Fed about whether and when to rein in the central bank’s $85 billion-a-month bond-buying program. On Thursday, the Labor Department reported that initial jobless claims–a measure of layoffs–have, on average, risen over the past month. That could point to a continued slowdown in hiring. Those favoring a pullback by the Fed have argued, in part, that the Fed’s policies could lead to higher inflation. But the latest data suggest that’s not happening yet.

Little Cause for Inflation Worries - Periodically I am asked whether we should worry about inflation, given how much money the Federal Reserve has pumped into the economy. Based on the Bureau of Economic Analysis data released Friday morning, this answer is still emphatically no. The personal consumption expenditures, or P.C.E., price index, which the Fed has said it prefers to other measures of inflation, fell from March to April by 0.25 percent. On a year-over-year basis, it was up by just 0.74 percent. Those figures are quite low by historical standards, and helped push consumer spending up. (Measured in nominal terms, consumer spending fell slightly in April. After adjusting for inflation, it rose.) When looking at price changes, a lot of economists like to strip out food and energy, since costs in those spending categories can be volatile. Instead they focus on so-called “core inflation.” On a monthly basis, core inflation was flat. But year over year, this core index grew just 1.05 percent, which is the lowest pace since the government started keeping track more than five decades ago.

A Failure to Act: Fed Policy and Interest Rates - Is the Fed responsible for the pernicious low-interest rate environment? Yes, but not for the reasons you think. I explain why in a new National Review article: While this absolves the Fed of direct responsibility for the low-interest-rate environment, it does not absolve it for its indirect influence. Through its control of the monetary base, the Fed can shape expectations of the future path of current-dollar or nominal spending. Thus, for every spike in broad money demand, the Fed could have responded in a systematic manner to prevent the spike from depressing both spending and interest rates. In other words, the Fed could have adopted a monetary-policy rule that would have committed it to maintaining stable growth of total-dollar spending no matter what happened to money demand. A promise from the Fed to do “whatever it takes” to maintain stable nominal-spending growth would have done much by itself to prevent the money-demand spikes from emerging at all. Why hold a greater number of safe, liquid assets if you believe the Fed will keep the dollar value of the economy stable?

Rate Stories - Paul Krugman - I’ve been getting some questions about the recent rise in long-term interest rates. Those rates are still at levels that would have seemed absurdly low not long ago — but they are up significantly from a few months ago. So when long-term interest rates rise, there are three main stories you hear. One is that the bond vigilantes have arrived, and are selling US debt because they now believe in the horror stories. Another is that the Fed has changed, that it may be ready to snatch away the punch bowl sooner than previously believed. And the third is that the economy is looking stronger than expected, which means that the Fed, although just as soft-hearted as before, will nonetheless start raising rates sooner than previously believed. All three of these stories would imply falling bond prices, that is, rising interest rates. But they have different implications for other markets, in particular for stocks and the dollar. Debt fears — basically, a run on America — should send stocks and the dollar down along with bonds. A perceived tougher Fed should send stocks down but the dollar up. And a better recovery should send both stocks up (because of higher expected profits) and drive the dollar higher. OK, there are possible complications; you can manage, just, to tell stories that don’t quite work as I’ve described. But these are surely what you should have in mind in your first pass at the issue. Here it is in a table:

“Public” Debt and Safe Assets: A View from Space - The meaning of “public debt” depends on the accounting/balance-sheet view you’re adopting. Each is a perfectly valid accounting construct; each depicts the situation differently. Some views may be more useful than others in sussing out how things work/are working.

- 1. The view from the Treasury balance sheet, with 1. government trust funds (Social Security, etc.) and 2. the Fed viewed as external entities. Generally referred to as “gross public debt.” The treasury bonds/bills held by those external entities are liabilities of Treasury. It must pay interest, and eventually principal, to those entities.

- 2. The view from the “unified” balance sheet. Generally called “debt held by the public.” This consolidates the Treasury and trust-fund balances (viz: the “unified budget“) into a single “government” balance sheet. Treasury’s debt/liability to those funds is internal to government (one department just owes another), so they vanish from this consolidated view.

- 3. The view from a fully consolidated “government” balance sheet, including Treasury, the trust funds, and the Fed. Debt consists of bonds/bills held by parties external to that “government.” There is no common name for this construct, and you rarely if ever see the situation depicted this way.

- 4. The view including GSEs (Fannie/Freddie). The Fed is buying $40 billion/month in mortgage-backed securities from these entities. They owe the Fed money, just like Treasury owes money to the trust funds. Those entities are quite arguably part of “government” (Treasury will always cover their liabilities, though perhaps using Fed machinations as the vehicle), so it’s not crazy to view this as another instance of “government owing money to itself.”

First Quarter GDP Revised Slightly Downward - The first revision to the first quarter GDP report released last month came out this morning and it showed a slight revision downward, but otherwise actually had some positive news:— A drop in government spending dragged more on the U.S. economy than initially thought in the first three months of the year, although consumer spending looked relatively resilient to Washington’s austerity drive. Other reports on Thursday showed the number of new jobless claims rose modestly last week while contracts on previously owned homes climbed to a three-year high in April. Gross domestic product, a measure of the country’s total economic output, expanded at a 2.4 percent annual rate during the first quarter, down a tenth of a point from an initial estimate, the Commerce Department said. Government spending tumbled at a 4.9 percent annual rate, which was faster than the 4.1 percent rate initially estimated. Also holding back growth during the quarter, businesses outside the farm sector stocked their shelves at a slower pace. The one bit of positive news is the fact that there was an increase of real final sales of domestic product from 1.5% in the “advance” report issued last month to 1.8% in the report released today. That didn’t impact the bottom line number, but it is an indication that the economy was relatively solid in the 1st quarter and that we’re unlikely to see a major change in the numbers when the final report comes out at the end of June. Of greater interest will be the numbers for the 2nd quarter and the question of whether or not the sequester has had a significant impact on the economy. The fact that the first quarter saw declines in government spending during a period that mostly covered the period before the sequester took place suggests that government agencies were already planning for the sequester by cutting back spending earlier in the year.

GDP Q1 Second Estimate at 2.4%: A Small Downward Revision from 2.5% - The Second Estimate for Q1 GDP came in at 2.4 percent, a slight downward revision from the 2.5 percent Advance Estimate. Both Investing.com and Briefing.com had forecast no change. Here is an excerpt from the Bureau of Economic Analysis news release: Real gross domestic product -- the output of goods and services produced by labor and property located in the United States -- increased at an annual rate of 2.4 percent in the first quarter of 2013 (that is, from the fourth quarter to the first quarter), according to the "second" estimate released by the Bureau of Economic Analysis. In the fourth quarter, real GDP increased 0.4 percent.... The "second" estimate of the third-quarter percent change in GDP is 0.1 percentage point, or $3.9 billion, less than the advance estimate issued last month, primarily reflecting downward revisions to private inventory investment, to exports, and to state and local government spending that were partly offset by a downward revision to imports and an upward revision to personal consumption expenditures. [Full Release] Here is a look at GDP since Q2 1947 together with the real (inflation-adjusted) S&P Composite. The start date is when the BEA began reporting GDP on a quarterly basis. Prior to 1947, GDP was reported annually. To be more precise, what the lower half of the chart shows is the percent change from the preceding period in Real (inflation-adjusted) Gross Domestic Product. I've also included recessions, which are determined by the National Bureau of Economic Research (NBER).

BEA Revises 1st Quarter 2013 GDP Growth Down Slightly To 2.38% Annual Rate - In their second estimate of the US GDP for the first quarter of 2013, the Bureau of Economic Analysis (BEA) reported that the economy was growing at a 2.38% annualized rate, only 0.12% lower than the 2.50% growth rate previously published.Nearly all of the revisions in the details of the report were similarly modest. Consumer spending on goods is now reported to have been slightly better, while consumer spending on services was essentially unchanged. Aggregate consumer spending is now reported to have provided the entire net growth of the economy. The biggest changes in the report came from inventories (which are still growing, but at a much slower rate), and foreign trade -- where both exports and imports weakened. For this set of revisions the BEA assumed annualized net aggregate inflation of 1.18%. In contrast, during the first quarter (i.e., from December to March) the seasonally adjusted CPI-U index published by the Bureau of Labor Statistics (BLS) rose by 2.10% (annualized). As a reminder: an understatement of assumed inflation increases the reported headline number -- and in this case the BEA's relatively low "deflater" (nearly a full percent below the CPI-U) boosted the published headline rate. If the CPI-U had been used to convert the "nominal" GDP numbers into "real" numbers, the reported headline growth rate would have been a much more modest 1.49%. Finally, real per capita disposable income was revised lower yet again. In fact, real per capita disposable income contracted during the quarter at an astonishing -9.03% annualized rate, taking it to a level below where it was two years ago. And the personal savings rate was adjusted down once more -- this time to 2.3%. Among the notable items in the report:

GDP Revised Down Slightly to 2.4% for Q1 2013 - Q1 2013 real GDP was revised downward slightly to 2.4% from 2.5%. This is still an improvement, from the fourth quarter 0.4% GDP showing a stagnant economy. Consumer spending was the biggest improvement while increased imports posed a major economic drag. Government spending declines continue to be an economic damper. The revision shows more consumer spending than originally reported, less investment, less imports, less exports and government expenditures were less than previously estimated. Generally speaking a 2.4% GDP implies moderate economic growth, yet overall real demand in the economy is still fairly weak. As a reminder, GDP is made up of: Y=C+I+G+(X-M) where Y=GDP, C=Consumption, I=Investment, G=Government Spending, (X-M)=Net Exports, X=Exports, M=Imports*. The below table shows the percentage point spread breakdown from Q4 to Q1 GDP major components. GDP percentage point component contributions are calculated individually. Consumer spending, C in our GDP equation, shows an increase from Q4. In terms of percentage changes, real consumer spending increased 3.4% in Q1 in comparison to a 1.8% increase in Q4. Services drove consumer spending with a 1.42 percentage point contribution in household consumption expenditures. Goods consumer spending contributed 0.98 percentage points to personal consumption expenditures. Below is a percentage change graph in real consumer spending going back to 2000. Graphed below is PCE with the quarterly annualized percentage change breakdown of durable goods (red or bright red), nondurable goods (blue) versus services (maroon).

Fed Watch: Steady As She Goes - The BEA released revisions to Q1 GDP numbers today, taking growth down a hair from the original 2.5% to 2.4%. Bloomberg is claiming that the downward revision to GDP and a rise in initial unemployment claims account for today's gain in equities. The idea is that the weaker data will dissuade the Fed from slowing down the pace of asset purchases this year. It is of course dangerous to assign a cause to every fluctuation in asset prices. In this case, I am hard pressed to see that today's data has any meaningful impact on policy. If anything, a focus on the data over a longer period rather than the month-to-month or quarter-to-quarter movements should convince you that little has changed since 2010. Gross domestic product and income in levels: Abstracting from inventory changes, look at the remarkable consistency of real final sales growth: And as far as initial claims are concerned, you must have pretty sharp eyesight to conclude that something fundamentally changed last week: Also note the the Fed may discount soft GDP numbers in any event. Recall the words of New York Federal Reserve President William Dudley:“The important thing to recognize about the U.S. economy is that things are actually improving underneath the surface,” Dudley said in the interview. “We don’t really see that so much in the activity data yet because of the large amount of fiscal drag.” Policymakers are trying to look past the fiscal drag to see if it is bleeding through to the broader economy. If not, they will conclude that growth is set to jump next year as the fiscal impact wanes. And they want to be ahead of the jump with respect to QE. Hence why the next few months of data are so important.

Bad News Is Good As GDP, Claims Miss Pushes Futures Higher; Five States' Data "Estimated" - Just when there was some concern that the US economy was no longer imploding at the usual pace, we get confirmation that nothing is actually better, following the one-two punch of weaker than expected Q1 revised GDP data, printing at 2.4% on expectations of an unchanged 2.5% print driven by a revision in Private Inventories (from 1.03% to 0.63% of total GDP, offset by a plunge in imports sliding from -0.9% to -0.32%). Personal Consumption posted a tiny increase from 2.24% to 2.40% which can only mean the consumer overextended themselves in Q1 - perhaps it is about time to ask the question of how consumption in the "sequester" and tax-hike quarter was the highest since Q4 2010. Additionally, initial claims increased from the as usual upward-revised 344K to 354K, on expectations of a 340K print. GDP broken down by components:

Latest US GDP Numbers Confirm Consumer-Led Expansion but Government and Exports were Weaker than Previously Thought - The second revision of GDP data released today by the Bureau of Economic Analysis confirmed that the U.S. economy expanded at a moderate 2.4 percent annual rate in the first quarter of 2013. The figure for overall growth was almost unchanged from the 2.5 percent of last month’s advance estimate. However, there were significant changes in several of the components of GDP growth, as the following table shows. Growth of consumer spending was even stronger than previously reported. In fact, we could say that consumers accounted for all of the reported growth, since pluses and minuses in other sectors just cancelled each other out. Increases in consumer spending were broad-based, with durable goods, nondurable goods, and services all showing solid gains. As a whole, investment was weaker than previously reported, contributing just 1.16 percentage points to total growth, down from 1.56 points in the advance estimate. However, the news was not all bad. Fixed investment held up well. The decrease came entirely from slower growth of nonfarm inventories than had previously been reported. Looking ahead, the slower pace of inventory increase in Q1 is a moderately good sign. It makes it less likely that factories and stores will have to cut back orders in Q2 to work off unwanted stocks of unsold goods. Not surprisingly, fiscal drag continued to be a factor slowing GDP growth. As the next chart shows, federal, state, and local governments all made negative contributions to growth in Q1. The biggest decrease came in federal defense spending. The measure of government activity reported in the GDP accounts, government consumption expenditure and gross investment, excludes entitlement spending and interest payments on government debt

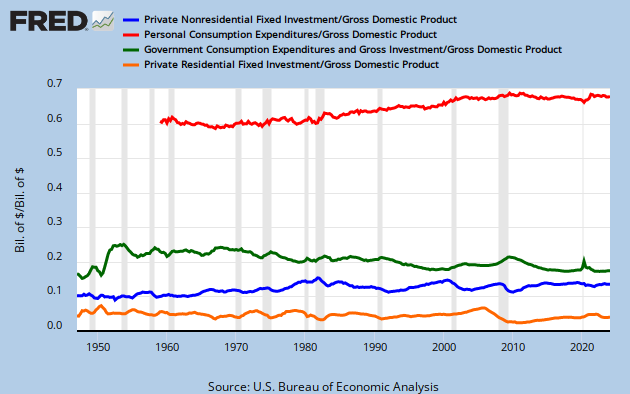

A few comments on 2nd Estimate of GDP - Earlier the BEA reported the second estimate of Q1 GDP. The revisions were fairly small, as the BEA reported that real GDP increased at a 2.4% annual rate in Q1, revised down from the advanced estimate of 2.5%. The underlying details were slightly positive.Personal consumption expenditure (PCE) grew at a 3.4% annualized real rate in Q1, revised up from 3.2%.The change in private inventories was revised down to a 0.63 percentage point contribution from a 1.03 percentage point contribution in the advance report (a 0.40 percentage point decline between estimates). This smaller buildup in inventories for Q1 is probably a positive for Q2.A key negative was the contribution from state and local government from -0.14 percentage points to -0.29 percentage points - the largest drag since Q2 2011. This graph shows the contribution to percent change in GDP for residential investment and state and local governments since 2005.The blue bars are for residential investment (RI), and RI was a significant drag on GDP for several years - and is now adding to the economy. However the drag from state and local governments has continued. Just ending this drag will be a positive for the economy. Note: In real terms, state and local government spending is at the lowest level since Q1 2001.With consumer spending holding up, residential investment increasing - and state and local governments near the bottom - this suggests decent growth going forward. Of course there will be a substantial drag from Federal fiscal policy over the next couple of quarters

Is Economy Doing Better Than GDP Suggests? - Why has job growth been decent over the past year, even as gross domestic product has remained weak? Maybe because the economy is doing better than GDP suggests. Employers have added a bit better than two million jobs over the past year, or about 173,000 jobs per month. That’s hardly robust growth, but it’s significantly better than would be expected given that the economy as a whole — as measured by GDP — has grown only 1.7% over the past year. That’s led some economists to question whether there’s been a shift in longstanding relationships between the labor market and the broader economy. But Thursday’s GDP report offers an alternate explanation: Perhaps GDP isn’t fully capturing recent economic growth. An alternate, lesser-known measure of output, known as gross domestic income, or GDI, shows the economy growing 2.2% over the same period — still not great, but more in line with recent job gains. In a nutshell, gross domestic product measures expenditures — consumer spending, business investment, international trade and everything else that people, companies and governments spend money on. Gross domestic income, as the name implies, measures income, including both personal income and corporate profits. In theory, the two numbers should be the same: They’re measuring the same thing, just from different directions. And in the long run, the two do generally line up. In the short run, however, they often diverge, with GDI typically showing more volatility.

Real GDP Per Capita: Another Perspective on the Economy - Earlier today we learned that the Second Estimate for Q1 2013 real GDP came in at 2.4 percent, down from 0.1 percent in the Advance Estimate released last month. Let's now review the numbers on a per-capita basis. For an alternate historical view of the economy, here is a chart of real GDP per-capita growth since 1960. For this analysis I've chained in today's dollar for the inflation adjustment. The per-capita calculation is based on quarterly aggregates of mid-month population estimates by the Bureau of Economic Analysis, which date from 1959 (hence my 1960 starting date for this chart, even though quarterly GDP has is available since 1947). The population data is available in the FRED series POPTHM. The logarithmic vertical axis ensures that the highlighted contractions have the same relative scale. I've drawn an exponential regression through the data using the Excel GROWTH() function to give us a sense of the historical trend. The regression illustrates the fact that the trend since the Great Recession has a visibly lower slope than long-term trend. In fact, the current GDP per-capita is 11.6% below the regression trend. The real per-capita series gives us a better understanding of the depth and duration of GDP contractions. As we can see, since our 1960 starting point, the recession that began in December 2007 is associated with a deeper trough than previous contractions, which perhaps justifies its nickname as the Great Recession. In fact, at this point, 20 quarters beyond the 2007 GDP peak, real GDP per capita is still 1.04% off the all-time high following the deepest trough in the series. Here is a more revealing snapshot of real GDP per capita, specifically illustrating the percent off the most recent peak across time, with recessions highlighted. The underlying calculation is to show peaks at 0% on the right axis. The callouts shows the percent off real GDP per-capita at significant troughs as well as the current reading for this metric.

Government Potholes on Road to Recovery - The private economy looks to be revving up to motor through the next couple quarters. The public sector will be a big pothole along the way. Although Thursday’s revisions to first-quarter U.S. gross domestic product lowered the top-line annualized growth rate, the details offer a better profile for future growth. That’s because the slightly slower pace — now 2.4% from 2.5% reported earlier — largely reflects less inventory accumulation over the winter. According to the Commerce Department‘s new figures, real inventories grew by $38.3 billion last quarter, less than the $50.3 billion reported a month ago. Demand from businesses and consumers held up, despite higher taxes. Plus, housing growth while revised lower still stood at a healthy 12.1%. Monthly indicators suggest spending by households and companies will continue to rise this quarter, although perhaps not as strongly as in the first quarter. Because inventories aren’t excessively large, companies will need to satisfy growing private demand by lifting output and hopefully payrolls. Then there is the public sector. Federal spending dropped at an 8.7% annual rate and state and local governments shrank by 2.4% (the 13th decline in the past 14 quarters). The government sector subtracted almost one percentage point from GDP growth last quarter, although that’s an improvement from the 1.41-point drag in the fourth quarter of 2012. But there are more minus signs ahead.

Why hasn't austerity been more of a drag on the U.S. economy? - This is the U.S. economy in a nutshell, as revealed in Tuesday’s news ticker: Housing prices rose faster over the past year than they have in the past seven. Consumer confidence hit its highest level in five years. The stock market rallied another 0.9 percent to hover near an all-time high, as measured by the Standard & Poor’s 500. And the national retail price of gasoline has fallen for six days straight and is down 16 cents a gallon since late February, providing nice relief to drivers. Which all raises an obvious question: Whatever happened to the austerity economy? At the start of the year, it looked like 2013 would be a battle between positive and negative forces shaping the economy. On the positive side of the ledger, arguing for stronger growth to finally burst out, housing was finally gaining momentum after a six-year slump and consumers had made major progress toward righting their household finances, enabling them to ramp up consumption. On the negative side, federal fiscal policy seemed to be fighting it tooth and nail, with tax increases and spending cuts that threatened to suck the wind out of any nascent economic boom. So far, the positives seem to be winning. Gross domestic product rose at a 2.5 percent rate in the first quarter, a bit better than the average over the past several years, and the nation added an average of 196,000 jobs a month in the first four months of 2013, a solid step up from the past few years.

No cause for relief—austerity will indeed drag hard on the economy in 2013 and 2014 - The normally excellent Neil Irwin and Ylan Q. Mui at Wonkblog are mostly wrong, I think, in arguing that the economy is “holding up surprisingly well” in a year of austerity. The data they cite to make this judgment are rising prices in both the stock market and home prices and falling gasoline prices. But rising stock prices are actually pretty irrelevant to most American families, and today they mostly reflect the stunningly high profit margins of American corporations. These profit-margins in turn are boosted by extremely weak wage-growth, as inflation-adjusted wages for the vast majority of American workers have fallen in each of the last three years. In short, one could easily make the case that today’s high stock prices are actually mostly a sign of bad news for American workers. Rising home prices do indeed spur consumption across the board. But given that today’s home prices are in line with long-run historical averages, and given as well that we know bad things happen when these prices rise above their long-run historical averages and people begin borrowing against their appreciated home equity, rising home prices are, to me, a sign of worry, not celebration. A part of the macroeconomic bundle that led to the crisis was a sharp fall in the personal savings rate, as people bought consumption gains by borrowing against the value of their homes (as opposed to being able to purchase these consumption gains with robust wage-increases). And guess what? Last quarter’s modest-but-decent growth in consumption spending was accompanied by a large fall in the savings rate, as it reached its lowest level since before the Great Recession began.

The Fed's been keeping the economy afloat. That's the problem. -- The U.S. economy, as I wrote yesterday, seems to be holding up well despite the onset of fiscal austerity. Jared Bernstein, Scott Sumner and Ezra say I should have mentioned an important reason: the apparent success of the Federal Reserve’s policies, introduced last September, of pumping more money into the economy and pledging to keep rates low even after the economy improves. They’re right! But that may not be a good thing. There is good reason to think that monetary easing is doing quite a bit of the work offsetting tighter fiscal policy. The Fed’s policies, including buying $85 billion in bonds each month with newly created money, are directly aimed at housing; $40 billion of those purchases are of mortgage-backed securities, meaning the money is being funneled directly toward the sector. And sure enough, a solidifying housing market is an important part of the economy’s holding up. And a second important consequence of Fed easing is to boost the prices of other financial assets, including the stock market. So far so good. The bad news, though, is that these channels through which monetary policy affects the economy tend to offer the most direct benefits to those who already have high incomes and high levels of wealth.

Does Steady GDP Growth “Prove” that Market Monetarists Are Right About Ineffective Fiscal Policy and Foolish Keynesianism? - You’re seeing a lot of crowing these days from the likes of Scott Sumner, David Beckworth, Lars Christensen, et al., claiming that fiscal austerity has obviously had no effect on GDP growth. “Look!” they say: “Even with the sequester and all the other government spending cuts, growth in 2013 has been the same as 2012! The notion that government spending affects GDP growth (“Keynesianism”) is obviously false and stupid.” As Scott says in a recent post:The left predicts fiscal austerity will slow the recovery, and yet both GDP and jobs are actually a bit ahead of the 2012 pace so far this year.This is specious reasoning. The “left” prediction has been that “fiscal austerity will will slow the recovery” relative to what it would be otherwise, not relative to 2012, or Q1 2012. Scott, not the lefties, chose 2012 as the benchmark. But I know they know: when you compare 2012 to 2013, ceteris is not paribus. Look at the four highlighted numbers here, showing growth/decline in the two GDP-component numbers that dominate our economy:

More on Ineffective Fiscal Policy - This is a companion piece to Steve’s AB post from earlier today, where he points out the specious reasoning of “the likes of Scott Sumner, David Beckworth, Lars Christensen, et al., claiming that fiscal austerity has obviously had no effect on GDP growth.” I wrote Sumner off a few years ago due to a highly unfavorable chaff/wheat ratio. I’ve tried really hard to like Beckworth, but these guys simply wallow in confirmation bias. I’ve repeatedly criticized Beckworth at his blog for cherry picking short-term time series data to make his points. Comparing 2013 to ’12 is an example of time series cherry picking used to justify absolutist dogma. Back on Feb 10, Beckworth said: “despite this austerity happening at a time of high unemployment and a large output gap, a slowdown in aggregate demand growth has failed to materialize.” And also: “we should at least see aggregate demand faltering over the past few years while this unfolded. But in fact, we see relatively stable aggregate demand growth, as measured by NGDP” He does admit in the end that, “the Fed has failed to restore NGDP to its pre-crisis trend.” but uses this to get in a dig at the Fed for not following his preferred agenda.

The “Dutch Disease” and Once and Future Economic Crises in the US - The term Dutch Disease refers to negative macro-economic effects on a country of a boom in commodity exports or other developments that result in large capital inflows. The negative effects are most apparent when the boom ends and the country is faced with the need to simultaneously adopt counter-cyclical, trade/exchange rate and structural policies if it is to enjoy a return to sustainable full employment. Despite the original example – the Netherlands – the Dutch Disease has generally been associated with difficulties experienced by emerging market economies. However, the term encompasses economic dislocations arising from a variety of external shocks, as well as across economies with differing levels of development. The piece will argue that it is also possible that the Dutch Disease contributed to the recent US recession and that the prospective energy-led US economic recovery could amount to nothing more than another bout of the Dutch Disease. Definition The term Dutch Disease was first used in 1977 by The Economist. It linked the exploitation of a large natural gas field discovered in 1959 off the coast of Holland to a subsequent decline in Dutch manufacturing. The narrow definition (from Wikipedia): Dutch Disease is the apparent relationship between the increase in exploitation of natural resources and a decline in the manufacturing sector. The mechanism is that an increase in revenues from natural resources (or inflows of foreign aid) will make a given nation’s currency stronger compared to that of other nations (manifest in an exchange rate), resulting in the nation’s other exports becoming more expensive for other countries to buy, making the manufacturing sector less competitive.

Treasury Yield Snapshot: 10-Year Yield Highest Since Early April of 2012 - I've updated the charts below through Tuesday's close. The yield on the 10-year note stands at 2.15%, up 72 bps from its all-time closing low of 1.43% set last July and at its highest level since early April of 2012. The S&P 500 is now up 16.75% for 2013, fractionally below its all-time closing high set last Tuesday. The latest Freddie Mac Weekly Primary Mortgage Market Survey (which will be updated tomorrow) puts the 30-year fixed at 3.59%, slightly off its 3.63% interim high in mid-March but well above its all-time low of 3.31%, which dates from the third week in November of last year. Here is a snapshot of selected yields and the 30-year fixed mortgage starting shortly before the Fed announced Operation Twist. For a eye-opening context on the 30-year fixed, here is the complete Freddie Mac survey data from the Fed's repository. Many first-wave boomers (my household included) were buying homes in the early 1980s. At its peak in October 1981, the 30-year fixed was at 18.63 percent. The 30-year fixed mortgage at the current level is a confirmation of a key aspect of the Fed's QE success, and the low yields have certainly reduced the pain of Uncle Sam's interest payments on Treasuries (although the yields are up from recent historic lows of last summer). But, as for loans to small businesses, the Fed strategy is a solution to a non-problem.

U.S. Deficit Shrinking At Fastest Pace Since WWII, Before Fiscal Cliff - Believe it or not, the federal deficit has fallen faster over the past three years than it has in any such stretch since demobilization from World War II. In fact, outside of that post-WWII era, the only time the deficit has fallen faster was when the economy relapsed in 1937, turning the Great Depression into a decade-long affair. If U.S. history offers any guide, we are already testing the speed limits of a fiscal consolidation that doesn’t risk backfiring. That’s why the best way to address the fiscal cliff likely is to postpone it. While long-term deficit reduction is important and deficits remain very large by historical standards, the reality is that the government already has its foot on the brakes. In this sense, the “fiscal cliff” metaphor is especially poor. The government doesn’t need to apply the brakes with more force to avoid disaster. Rather the “cliff” is an artificial one that has sprung up because the two parties are able to agree on so little.

So Much for the Impending Economic Armageddon Federal Budget Deficit - Surprise, when tax revenues increase the deficit goes down. Such was the news of a new CBO update on the budget deficit.If the current laws that govern federal taxes and spending do not change, the budget deficit will shrink this year to $642 billion, CBO estimates, the smallest shortfall since 2008. Relative to the size of the economy, the deficit this year—at 4.0 percent of gross domestic product (GDP)—will be less than half as large as the shortfall in 2009, which was 10.1 percent of GDP. Below is the CBO graph of the newly projected budget deficit. As economic activity increases, tax revenues increase, people need less social services and deficits go down. Winding down war also helps. Fannie Mae also gave Treasury a gift of $59.4 billion in unexpected Q1 profits and has paid $95 billion to the Treasury this year. As a result, the deficit has dropped dramatically. Who knew, unless one took a basic economics course, that budget deficits and a terrible economy are linked and highly correlated. Gouging health care costs are still a major problem, but this mega disaster so many rail about as the next great economic implosion has time to be averted. However, budget shortfalls are projected to increase later in the coming decade, reaching 3.5 percent of GDP in 2023, because of the pressures of an aging population, rising health care costs, an expansion of federal subsidies for health insurance, and growing interest payments on federal debt.

Sorry Folks, Austerity’s Not Dead Yet! It makes a good headline; but it’s dangerous to say “austerity is dead,” just because new budget projections indicate that the deficit has already been cut by $200 Billion more than in previous projections, and because the Reinhart-Rogoff study has been debunked successfully, and, hopefully, irretrievably. Austerity will only be dead when legislators, Presidents, Prime Ministers, Central Bankers, and international lending organizations stop trying to implement it, whether or not they stop because deficits have already been cut. Of course, those claiming austerity is dead, mean by their claim that deficit cutting efforts have already been successful enough in the United States that future projections in all the mainstream budget plans now show only “moderate” deficits (See the Table which now includes CBO revised budget projections.) These don’t signal a debt crisis, and instead suggest that we can now turn to the really serious economic, health, and environmental challenges we face.

Reasoning by Metaphor - We don’t make policy in this country based on our knowledge of the likely outcomes; instead we limit our actions to those possible in an age dominated by gut feelings and the irrational demands of the rich, driven by faulty reasoning. This week we see several examples of disrespect for knowledge and reasoning. On the more or less left, we have the spectacle of Michael Kinsley, currently an editor at large at The New Republic, exploring the Puritan within himself: Krugman also is on to something when he talks about paying a price for past sins. I don’t think suffering is good, but I do believe that we have to pay a price for past sins, and the longer we put it off, the higher the price will be. And future sufferers are not necessarily different people than the past and present sinners. I think that last sentence means that it is a least possible that the people who caused the Great Crash might suffer now or in the future, Kinsley’s nod at the unfairness of his solution. Matt Taibbi points out that our national debate is all about how government is just like a household that has run up too much debt, a stupid metaphor. It completely ignores all the ways that governments and households are radically different, not least of which is that governments don’t die. People use that metaphor to frame their thinking about how to cope with continuing federal deficits, and come up with answers that lead to austerity and the Republican refusal to raise the debt ceiling. The error in both cases comes from reasoning with a metaphor. Kinsley talks about a “we” who did bad things with money and the economy. By we, he means society. Then he uses individuals as a metaphor for society. If you commit a sin, you should be punished. If society commits a sin, it should be punished. This reasoning is identical to the reasoning from the household metaphor.

Economic policy is largely being driven by obstructionism, not economic advisers - Consequently, the U.S. economy will almost certainly continue muddling through an adverse equilibrium of anemic growth, severely depressed output, massive underemployment, large cyclical budget deficits, subdued price inflation, widespread real wage deflation and low interest rates. It’s really quite simple: a steep aggregate demand shortfall continues to keep the economy’s performance well below potential, and the Federal Reserve has been and will continue to be incapable of fully ameliorating this shortfall so long as contractionary fiscal policy is being pursued. (See this paper for a thorough treatment.) In short, the intellectual debate over austerity vs. stimulus has been totally decoupled from the policy debate and, more importantly, policy outcomes in Washington—despite having been resolved in a virtual TKO by those opposed to foisting austerity on depressed economies. The United States doesn’t face, or, perhaps more accurately, no longer faces a deficit of economists capable of opening up an intermediate macroeconomics textbook and relearning liquidity trap/depression economics. But the U.S. Congress faces a depressing deficit of

Macroeconomic Hippie-Punching - Paul Krugman - The usual form of macroeconomic hippie-punching in recent years has been the pro-stimulus or anti-austerity article that opens with several paragraphs of the dangers of long-term budget deficits and the importance of a medium-term debt strategy — often with a specific condemnation of Those Who deny the importance of such — followed by a discussion of the reasons why slashing spending right now is a very bad idea. And I’ve watched the response: the centrists who are the presumed audience read the first three paragraphs, say “Yes — the hippies are all wrong!” and never get to the part saying that, well, actually, the hippies are right on the important stuff. To some extent this is just about the fact that the hippies have indeed been right across the board on macro, the same way they were on the Iraq war. But it’s also about journalistic messaging: if you have a point you want to get across, you should always, always, put it right up at the front, and get to the qualifications later. The patient reader who will wade through your preemptive hippie-bashing to get to the good stuff is a myth — just as much a myth as the reasonable centrist who can be won over by hippie-bashing in the first place.

Optimal Civility - There has been some discussion of civility as a result of Reinhart and Rogoff’s open letter to Krugman, which included accusations of incivility:We admire your past scholarly work, which influences us to this day. So it has been with deep disappointment that we have experienced your spectacularly uncivil behavior the past few weeks. You have attacked us in very personal terms, virtually non-stop, in your New York Times column and blog posts.This has highlighted a question to me that is aside from the RR vs K debate, which is what optimal civility looks like? Civility is just one characteristic with which you could throw in the related writerly characteristics of generosity, harshness, and others. The case for writing with civility is that doing otherwise has a poisonous effect on debate. People who you might persuade stop reading you, those who write in disagreement are pressured to return the incivility, which in turn drivers other readers out of the conversation. I believe it also affects those you are being uncivil towards in more than their rhetoric. Through this process incivility leads to defensiveness, and this in turn drives polarization. In addition incivility drives people out of the debate. Writers may have counterarguments to some piece they read but don’t want to reply because they don’t wish to be the target of incivility and personal attacks. Overall, I would characterize the internet in suffering from too little rather than too much civility.

Nonsense in the Reinhart-Rogoff Rescue Effort - Dean Baker - The mainstream of the economics profession continue to try to rescue Carmen Reinhart and Ken Rogoff (R&R) from the consequences of their famous Excel spreadsheet error. The latest is Michael Heller, who has pronounced Paul Krugman the loser in his exchanges with R&R because he conceded that countries with debt-to-GDP ratios that exceed 90 percent of GDP have slower growth. This is the sort of piece that should really have the general public thinking about defunding economics programs everywhere. The fact that countries with higher debt-to-GDP ratios have slower growth than countries with lower debt-to-GDP ratios was never at issue. The corrected spreadsheet shows this to be true across the board at every debt level. There is no importance to 90 percent. The 90 percent cliff came about because of the Excel spreadsheet error, it does not otherwise exist in the data. Heller's claim that R&R never said anything about a 90 percent cliff is an effort to re-write history. This number was embedded in the Bowles-Simpson report that came to be the guidepost for debate on the deficit in Washington policy circles. It also has been used by top officials in the European Union and elsewhere as a basis for austerity. Using the corrected data the closest thing resembling a cliff can be found in the range of debt-to-GDP ratios of 20 percent of GDP. There would be no reason that 90 percent would ever appear in a discussion of debt in the corrected R&R debt-to-GDP data.