US Fed's balance sheet edges up in latest week - The U.S. Federal Reserve's balance sheet rose in the latest week, Fed data released on Thursday showed. The balance sheet rose to $2.327 trillion in the week ended June 16 from $2.314 trillion in the week ended June 9. For link to graphic see link.reuters.com/buf92kThe Fed's holdings of mortgage-backed securities backed by housing finance companies Fannie Mae (FNM.N) and Freddie Mac (FRE.N) totaled $1.128 trillion on June 16, versus $1.114 trillion the previous week.The U.S. central bank's ownership of debt issued by Fannie Mae, Freddie Mac and the Federal Home Loan Bank System was $166.21 billion compared with $166.72 billion a week earlier.Primary credit via the Fed's discount window averaged $104 million a day in the latest week compared with $105 million per day in the previous week.

FRB: H.4.1 Release--Factors Affecting Reserve Balances--June 17, 2010

Rudebusch: The Fed's Exit Strategy for Monetary Policy - Glenn Rudebusch looks at the Fed's exit strategy for its special liquidity facilities, the lowering of short-term interest rates, and the increase in the Fed’s securities holdings. (The Fed's Exit Strategy for Monetary Policy, SF Fed) Along the way he tries to dispel worries about the "inflation monster"(see figure 4). The bottom line for interest rates is that "it seems likely that the Fed’s exit from the current accommodative stance of monetary policy will take a significant period of time." This is in contrast to Raghu Rajan who continues to argue that rates should go up, partly on the basis of the effects of low interest rates on countries like Brazil. This serves as a counterpoint to the argument that low interest rates will cause "dangerous financial imbalances, such as asset price misalignments, bubbles, or excessive leverage and speculation", e.g. see the discussion just before figure 2, as well as a more general counterpoint to the "we need to raise rates" argument.

A Near-Zero Fed Funds Rate Until 2012? - Observers of the Federal Reserve have been speculating for months about when the central bank might start lifting the benchmark short-term interest rate from near-zero, where it has been since December 2008.At first, many economists predicted that the Fed would start to tighten monetary policy by the end of 2010. Then, a growing number began to revise that prediction to the early part of 2011.But a new research paper from the Federal Reserve Bank of San Francisco suggests that if the Fed continues to follow the course of monetary policy it has pursued since the crisis, the fed funds rate won’t lift off from near-zero until 2012.If unemployment remains high while inflation remains very low, as is currently projected, “it seems likely that the Fed’s exit from the current accommodative stance of monetary policy will take a significant period of time,” according to the paper, by Glenn D. Rudebusch, a senior vice president and associate director of research at the San Francisco Fed.

Shouting fire amid a flood - SAN FRANCISCO Fed economist Glenn Rudebusch has written an interesting paper on the timing of the Federal Reserve's exit from its accommodative monetary policy stance. It's worth a read, but I just want to reproduce two charts for your consideration. This: And this: What we see in the first image is that even if one takes into account the unconventional monetary policy actions the Fed has used through this crisis, the federal funds rate target remains nearly 4 percentage points above the level at which you'd want it. And in the second image we see that the huge growth of the Fed's balance sheet has basically done nothing to increase long-run inflation expectations. Inflation is no concern at all; in fact the Fed should be doing more. As it stands, the question of the day is not what more the Fed should do but how long the Fed should wait before undoing.

Fed to Touch Extension Chord--- FED WATCHERS MAY as well take next Wednesday off. In part, that's because any mystery about the Federal Reserve's plans for its near-term monetary policy has been all but erased by events and news leaks. In the case of the latter, the page one lead story in Tuesday's Wall Street Journal reported Fed officials were mulling what steps to take if the economy stumbles or inflation diminishes further. At recent FOMC meetings, the policy-setting panel has maintained the status quo of a federal-funds target of 0-0.25% and holding policy interest rates at low levels "for an extended period." But the question always was when that extended period would expire. Indeed, Kansas City Fed President Thomas Hoenig dissented at the past three meetings because the "extended period" language appeared to shackle the Fed should an interest-rate increase be needed sooner rather than later.That no longer seems to be a concern.

Exit strategies for central banks: Lessons from the 1930s - VoxEU - Many commentators have compared the global crisis to the Great Depression. This column explores lessons that can be applied to help shape expectations and guide exit policy for central banks. It argues that the need for credit stimulus should end when failed intermediaries are resolved and positive net present value credits are reallocated to solvent lenders

Bullard: U.S. Economic Recovery Insufficient For Rate Increase - A U.S. central bank official said Monday the recent recovery in the country’s economy remains insufficient to prompt an increase in the benchmark interest rate.“The recovery will have to be firmer than it is right now and we’ll have to see more improvement” before the central bank raises its Fed funds rate, Federal Reserve Bank of St. Louis President James Bullard told reporters Mr. Bullard also said that given recent global financial market turbulence, this isn’t time to raise the Fed’s discount rate further.Still, he said sovereign debt problems in Europe won’t likely affect the timing of eventual Fed monetary tightening.

When will the Fed raise rates? -Over the last year a number of analysts have predicted the Fed would raise the Fed Funds rate "soon". They have all been wrong. The Fed's mission is to conduct "monetary policy by influencing the monetary and credit conditions in the economy in pursuit of maximum employment, stable prices, and moderate long-term interest rates". Historically the Fed has not raised the Fed Funds rate until unemployment drops significantly. Based on the the Fed's own forecasts of the unemployment rate and inflation, the Fed will probably not raise the Fed Funds rate until late 2011 at the earliest. San Francisco Fed senior vice president and associate director of research Glenn Rudebusch writes: The Fed's Exit Strategy for Monetary Policy Rudebusch's economic letter suggests that the Fed might not raise rates until 2012 ...

J.P. Morgan Pushes Back Rate Hike Forecast to Late 2011 - J.P. Morgan’s economists are pushing back their expectations of when the Federal Reserve will raise interest rates as next week’s central bank meeting quickly approaches.Bank economist Michael Feroli told clients Thursday his bank now expects the Fed to first raise rates in the fourth quarter of 2011, rather than the second quarter. “The prime motivation for the change is the behavior of inflation,” the economist wrote.“While we have been expecting core inflation to fall below 1%, the degree to which this has been located in the more persistent service price component, as well as the extent to which wage inflation has slowed, both suggest the disinflation we have witnessed could be with us for some time,” Feroli said. Pushing back estimates of rate hikes has been in fashion on Wall Street over recent weeks. Central bankers meet next week in a gathering that’s almost certain to result in the overnight target rate left at its effectively 0% stance.

Bank Currency Mismatches Adding Further Stress to Global Financial System —The Federal Reserve (FRB) has established temporary USD swap facilities with other Central Banks during each of the periods of exceptional intervention during the last 2 years (Oct 2008 and May 2010). This action provided evidence of underlying stress. A recent BIS paper (see here), presents evidence of this stress and why the FRB’s action was important and essential. The BIS reviewed banking statistics to separate banks into those with more dollar assets than dollar liabilities (i.e. long dollar) and those with fewer dollar assets than dollar liabilities (i.e. short dollar). The larger the long or short dollar position of a bank, the larger the gross currency mismatch (before hedging). Banks with long dollar positions would have either borrowed in the wholesale market or entered into an fx (dollar/domestic currency) swap. The BIS analysis is shown in the chart below.

House Lawmakers Seek Wider Fed Audit - U.S. House lawmakers negotiating changes to wide-ranging financial markets legislation plan on Wednesday to seek a limited expansion of a provision to provide greater scrutiny of the Federal Reserve.U.S. House members of the bicameral “conference committee” plan to offer an amendment to the nearly 2,000-page bill that would allow government auditors to review discount window and open market transactions by the central bank. The information collected by the Government Accountability Office would be required to be disclosed to the public within three years after the Fed enters into the transactions, according to a summary obtained by Dow Jones Newswires.

House-Senate Panel Broadens Audits of Fed - House and Senate negotiators agreed Thursday to broaden the scope of a new set of audits of the Federal Reserve by the Government Accountability Office to include transactions involving the Fed’s discount window and open market operations. But the Federal Reserve dodged attempts to extend Congressional review over its monetary policy decisions. The Senate had previously approved a provision that would require a government audit of the Federal Reserve’s emergency lending authority, a move that arose in response to the Fed’s actions in the 2008 financial crisis. But the House-Senate conference committee wanted to go further, subjecting the Fed to regular audits of its routine operations

Senate Negotiators Agree to No Confirmation of NY Fed President - Senate lawmakers negotiating the final version of a broad financial overhaul bill Thursday rejected a move to require the president of the New York Federal Reserve Bank be a presidential appointee, virtually ensuring that the proposal won’t make it into the final bill. Sen. Jack Reed (D., R.I.) had asked for the change in a House proposal to reduce the influence of commercial banks on the appointment of regional Federal Reserve bank presidents.Reed argued that the New York Fed president “has huge regulatory power,” noting that when Treasury Secretary Timothy Geithner held the position, he presided over the collapse of Lehman Brothers and the purchase of Bear Stearns.

Lawmakers Agree to Limit Banks’ Influence on Regional Fed Presidents - Senate lawmakers on the financial overhaul “conference committee” moved toward accepting a House proposal that would eliminate the vote of “class A” directors in picking regional Fed bank presidents, according to a summary distributed to reporters. Directors deemed “class A” are elected by banks to represent the interests of the industry, as opposed to the public. The agreement between the two sides would also eliminate a Senate proposal that called for the president of the Federal Reserve Bank of New York to be presidentially appointed. Critics of the proposal said it would have politicized the position. Additionally, the two sides agreed that a widely watched proposal to conduct an audit of the Fed’s response to the 2008 financial crisis would include a review of discount window and open market transactions the central bank enters into with financial firms.

Fed Emerging Intact From Challenge to Its Power - WSJ - On Thursday, senators on a panel meant to reconcile competing versions of the bill voted 10-2 to kill a provision that would have made the president of the Federal Reserve Bank of New York a White House appointment. The position is now an internal Fed appointee. Fed officials said the change would have politicized the institution. A rethink of the Fed has been part of the broader financial overhaul legislation expected to be completed in Congress this month. The House-Senate conference also has resisted a House attempt—popular in Congress but adamantly opposed by the Fed—to subject the Fed's interest-rate decisions to regular audits by the Government Accountability Office, which Congress oversees.

FedViews (Latest Forecast) - SF Fed Research (summary; series of bullet points)

US Dollar: The Mother of All Bubbles -A bubble is a significant increase in valuation supported by a set of artificial, inexplicable, and otherwise unsustainable conditions. The 'increase in valuation' can be nominal as in a price that goes 'higher' without a corresponding increase in value, or a decline in the value underlying the asset while the price remains nominally the same. (note 1) The duration of a bubble does not make it valid or 'the new normal.' Like most chronic conditions it just means that the adjustment will be all the more difficult. The US dollar as the world's reserve currency, and the unusual period of US prosperity, is an historical artifact of the post World War II era that will not continue indefinitely. When the reversion to the mean occurs, it is likely that the dollar will have to be reissued as 'the new dollar' similar to the rouble in the post-Soviet adjustment. For the UK, it looks like Argentina, or Iceland writ large, but with the sharp edge of a police state.

Monetarists warn of crunch across Atlantic economies (chart series)The money supply data from the US, Britain, and now Europe, has begun to flash warning signals of a potential crunch. Monetarists are increasingly worried that the entire economic system of the North Atlantic could tip into debt deflation over the next two years if the authorities misjudge the risk. The key measures of US cash, checking accounts, and time deposits - M1 and M2 - have been contracting in real terms for several months. A dramatic slowdown in Britain's broader M4 aggregates is setting off alarm bells here. Money data - a leading indicator - is telling a very different story from the daily headlines on inflation, now 4.1pc in the US, 3.7pc in Europe, and 3.3pc in Britain,

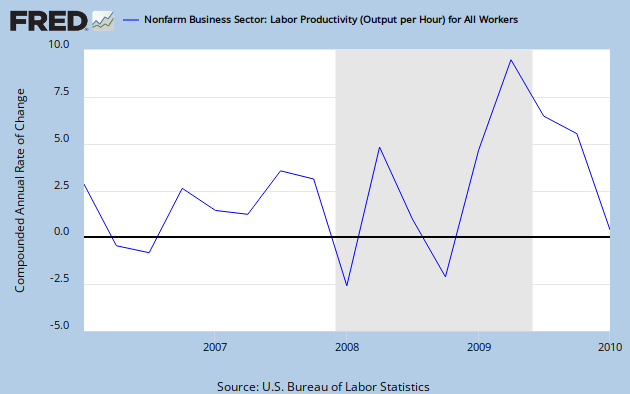

The Phillips Curve Today: Beware the White Swan -So much for the theory--let’s just stop here and take a look at the evidence in its simplest form. (To produce the chart below, I first took the rate of change in the core CPI from December to December for each year. Then I subtracted the previous year’s rate of change from the current year’s rate of change, for each year in the sample, and I plotted the result against the average unemployment rate for the current year. The core CPI series starts in 1957, so the first observation for which I could compute the change in the inflation rate is 1959. All the underlying data are from the Bureau of Labor Statistics.)The correlation isn’t perfect – and we wouldn’t expect it to be, since there are other factors that affect the inflation rate in the short run. But it’s strong enough to be quite statistically significant. And under today’s circumstances, it’s strong enough to be disturbing. The core inflation rate for 2009 was 1.8 percent. If you take the regression line at face value and plug in an average unemployment rate of 9.6 percent – a little toward the low end of what most economists expect for the year – it implies a 1.8 percentage point decline in the core inflation rate. And if you look at the actual data for January through April 2010, we are right on target for a zero percent core inflation rate.

This Does Not Look Good - Take a look at the figure below. This figure shows the difference between the nominal interest rate on the 5-year Treasury and the real interest rate on the 5-year Treasury inflation protected security (TIPS). This difference amounts to the markets expectation of future inflation. This figure, which goes through June 15, 2010, reveals a clear downward trend in inflation expectations over the first half of this year. I would like to attribute this decline to productivity growth, but it too appears to be coming down. That leaves us with one troubling possibility: the market is expecting aggregate demand to decline going forward. And unless the Fed acts to stabilize this expected fall in total spending it will effectively amount to a tightening of monetary policy. Obviously, the last thing the U.S. economy needs is a tightening of policy during an anemic recovery. I hope Ben Bernanke and the Fed are taking notice.

Deflation Fears Stir in Developed Economies - WSJ - The fears are most pronounced in Europe, where policy makers are under pressure to reduce large budget deficits now, before durable recoveries emerge. A combination of spending cuts and tax increases could weigh on economic growth and feed into deflation, which is a broad decline in consumer prices.Deflation makes it harder for consumers, businesses and governments to pay off debts. Principal repayments on debt are fixed but deflation is marked by falling incomes, so as deflation sets in the burden of paying off old debts gets greater. Officials fret about deflation because it is hard to stop. Interest rates are already near zero in the U.S. and elsewhere, so policy makers can't use the traditional tool of rate cuts to spur growth and stop deflation.

Deflation Advice, via Gary Shilling – Kalpa - If you are paying attention to the media, the Federal Reserve board members, and the global economic world, in general, you are noticing a growing concern about deflation. The June 15th WSJ cover page article by Hilsenrath began like this . . . Federal Reserve officials are beginning to debate quietly what steps they might take if the recovery surprisingly falters or if the inflation rate falls much more... While it has always been on radar screens, fear is growing that government weapons against deflation are losing the battle. A most interesting paragraph from the article describes that we should, in actuality, have negative interest rates right now:

Strange Arguments For Higher Rates, by Paul Krugman: So Raghuram Rajan has posted a further explanation of his case for raising interest rates in the face of very high unemployment, presumably a response to Mark Thoma. It’s good to see Rajan put his cards on the table — but what he says only further confirms my sense that we’re talking about some kind of psychological desire to be tough... Rajan’s argument boils down to two assertions: 1. Raising rates a bit wouldn’t significantly deter investment.2. “Unnaturally low” interest rates are distorting asset prices. The first thing to say about these two assertions is that they are essentially contradictory. If the difference between current rates and the rates Rajan wants is trivial — just a wafer thin mint — how can that same difference be leading to a major distortion in financial markets? Are we to believe that an interest rate change that matters not at all to firms making real investments somehow has huge effects on speculators? And actually, don’t asset prices themselves matter for real investment?

Antipathy To Low Rates - Krugman - Richard Serlin, in comments at Mark Thoma’s place, makes a very good point about the efforts of Rajan and others to come up with a reason to raise interest rates even in the face of high unemployment and incipient deflation. He suggests that it reflects a general distaste for anything that looks like government intervention to support the economy:I think the thinking of the libertarians and freshwater believers is that if there’s a recession, then the free market has a good reason for it. It’s a “real” business cycle phenomenon, and the best thing to do is let the free market have its recession or depression for as long as the free market wants (and we had some doozys before Keynes, and often). The Fed shouldn’t tamper with the free market, just like the fiscal branch of government shouldn’t. These days, relatively few economists are willing to say straight out that they regard persistent high unemployment as a good thing. But they find reasons to oppose any and all suggestions to use government policy — including monetary policy — to alleviate the slump. Same as it ever was.

China and other countries buy US Treasury debt - China boosted its holdings of U.S. Treasury debt in April for the second straight month as total foreign holdings of U.S. government debt increased. China's holdings of U.S. Treasury securities rose by $5 billion to $900.2 billion in April, the Treasury Department said Tuesday. Total foreign holdings rose by $72.8 billion to $3.96 trillion.The sizable gains are being driven by fears that Greece and other European governments could default on their debt. Worries over possible defaults have sparked a flight to safety and that has benefited U.S. Treasury securities. Treasurys are considered the world's safest investment — the U.S. government has never defaulted on its debt.The April increases eased concerns that lagging foreign demand will force the U.S. government to pay higher interest rates to finance its debt with private economists forecasting strong gains in May as well because of the debt crisis.

"UK" Holdings Of US Treasuries Go Exponential, As Foreigners Now Hold $3.96 Trillion Of American Debt - According to the latest Treasury International Capital release, total foreign holdings of US debt in April increased to just under $4 trillion, or $3,957 billion, a $73 billion increase. This represents 47% of total debt held by public at the end of April of $8,434 billion. And while two of the three usual suspects increased their US debt holdings marginally, China buying $5 billion and Japan buying $11 billion, the "UK's" purchases of US debt continue to grow at an exponential phase: these have now hit $321 billion in April, having tripled over the past 6 months ($108.1 billion in October 2009), and increasing by a whopping $42 billion month over month. We put the UK in parentheses as the end purchaser in this case is anyone but an an austerity-strapped and deficit reducing UK. Whether this is the domain of the mysterious direct bidders, an offshore FRBNY holdco, or just Chinese buyers domiciled in the UK, continues to be unknown. Yet one look at the chart of UK holdings below demonstrates that something is very much wrong with this series.

Pimco Holdings Of US Government Debt Surge, Its European Debt Experiment Is Now Over - Even as most asset managers experienced a devastating May, with many recording drops in AUM of -10% or worse, there is nothing that can topple the trillion+ bond giant out of Newport, which is so large it is now virtually the market in most of its product verticals. In the May performance report, of Pimco's flagship Total Return Fund, the fund's total assets grew once again, hitting $228 billion, an increase of $3.4 billion over April, and 45% higher than last year. Combing through the fund's holdings, the firm has now officially said goodbye to the "foreign developed" bond experiment, with non US developed holdings plunging by more than 50%, to just 6%, compared to 13% in April, and a high of 19% in February. The beneficiary of this adjustment were US bond holdings, which surged from 36% to 51% of all holdings, or a MOM increase of over $35 billion! This represents about a third of all (settled) US bond issuance in May. Who needs QE2 when you have Pimco. Another notable observation is that the fund is now once again acting on margin, with a -4% net cash position. The last time the fund was on margin was in October 2009.

Debt Default: It Can Happen Here - The recent financial crisis in Greece has led to a lot of discussion about whether the United States might one day have a public debt so large that default becomes a real possibility. While the sort of problem Greece is experiencing is impossible here, we have another problem that, to my knowledge, no other nation on Earth has: a legal limit on government debt that Congress must raise periodically. This peculiarity of our fiscal system could indeed lead to a default on the debt, with repercussions that advocates of default — yes, they exist — have absolutely no clue about.

The Correlation Between Debt Levels and Worried Markets - Here's an interesting observation from the latest economic outlook from the SF Fed: looking only at current and projected debt levels, it becomes hard to distinguish the countries that markets are worried about from the countries markets are not worried about. So the message for the debt-heads is that it's not just debt levels that matter. What else matters?: History may matter as well ..., countries of most concern are those that have defaulted more frequently in the past. (See Carmen M. Reinhart and Kenneth Rogoff, This Time is Different...) None of those defaults are recent, but there were defaults that occurred during the Great Depression. That is relevant to the present because the financial shocks of the past few years are among the biggest that have happened since that time. When was the last time the US defaulted? Finally: While there is some risk that Europe's sovereign debt crisis could get much worse, the most likely outcome is that it will not. In that case, its effects on the U.S. economy are likely to be small.

Greenspan Says U.S. May Soon Reach Borrowing Limit - Former Federal Reserve Chairman Alan Greenspan said the U.S. may soon face higher borrowing costs on its swelling debt and called for a “tectonic shift” in fiscal policy to contain borrowing. “Perceptions of a large U.S. borrowing capacity are misleading,” and current long-term bond yields are masking America’s debt challenge, Greenspan wrote in an opinion piece posted on the Wall Street Journal’s website. “Long-term rate increases can emerge with unexpected suddenness,” such as the 4 percentage point surge over four months in 1979-80, he said. Greenspan rebutted “misplaced” concern that reducing the deficit would put the economic recovery in danger, entering a debate among global policy makers about how quickly to exit from stimulus measures adopted during the financial crisis. U.S. Treasury Secretary Timothy F. Geithner said this month that while fiscal tightening is needed over the “medium term,” governments must reinforce the recovery in private demand.

Greenspan: We're In Danger Of Being The Next Greece! - Former Fed Chair Alan Greenspan has an op-ed in the WSJ arguing that the runaway Federal Deficit threatens to turn the US into the next Greece.He doesn't actually think that the US debt bears any credit risk, due to our ability to print at will, but that there is a substantial risk that borrowing costs will soar.Of course, market participants are aware of our towering deficit, and yet yields continue their long march lower, so that's kind of problematic to his world view. Says Greenspan: "This is regrettable, because it is fostering a sense of complacency that can have dire consequences."

Time to Slip into Something Less Comfortable? – During the great credit party that raged around the world for the five years leading up to 2008, a few economists and investors studiously avoided the punch bowl. They stood in the corner, muttering darkly about how it would all end with the hangover of the century. They were outcasts.Now, as the markets show fresh signs of panic, much of it emanating from the sovereign debt crisis in Europe, the spotlight is swinging back their way. Despite evidence of improving conditions, most bears have changed their outlooks only marginally, if at all. Which raises the question: Is their persistent pessimism a mark of brave, nonconformist thinking, or has their negativity become a kind of crisis schtick—contrariness for the sake of notoriety? To find out if they should be feared or ignored, Bloomberg Businessweek assembled a cast of the most prominent bears from 2008, traced the development of their dark outlooks, and assessed where they see the economy going from here.

Does Fiscal Austerity Reassure Markets? - Krugman - Consider, if you will, the comparative cases of Ireland and Spain. Both countries appeared, on the surface, to be fiscally responsible until the crisis hit, with balanced budgets and relatively low debt. Both discovered that this was an illusion: revenues were buoyed by immense real estate bubbles, and when the bubbles burst they plunged into deficit — and found themselves potentially on the hook for large bank losses. The countries responded differently, however. Ireland quickly embraced harsh austerity; Spain has had to be dragged into austerity, and still faces major political unrest. So, how’s it going? This article is typical of what you read: it describes the Irish as doing what has to be done, while the Spaniards dither. And it has good things to say about how the Irish response is working: Well, I guess that’s right — if by “markets impressed” you mean a CDS spread of 226 basis points, compared with 206 points for Spain; not to mention a 10-year bond rate of 5.11 percent, compared with 4.46 percent for Spain.

The Bad Logic Of Fiscal Austerity - Krugman - So, one more time: here’s an attempt to put together some key arguments about why the rush to fiscal austerity is deeply misguided. Let me start with the budget arithmetic, borrowing an approach from Brad DeLong. Consider the long-run budget implications for the United States of spending $1 trillion on stimulus at a time when the economy is suffering from severe unemployment.That sounds like a lot of money. But the US Treasury can currently issue long-term inflation-protected securities at an interest rate of 1.75%. So the long-term cost of servicing an extra trillion dollars of borrowing is $17.5 billion, or around 0.13 percent of GDP. And bear in mind that additional stimulus would lead to at least a somewhat stronger economy, and hence higher revenues. Almost surely, the true budget cost of $1 trillion in stimulus would be less than one-tenth of one percent of GDP – not much cost to pay for generating jobs when they’re badly needed and avoiding disastrous cuts in government services.

Magical Foreigners, Austerity Edition -- Krugman - For a while there, everyone on the right was in love with Chile — land of the wonderful, perfect retirement system, which proved beyond a shadow of a doubt that private accounts were the way to go. Then some people started looking at the Chilean reality, discovered that the system had big problems, and that the Chilean public actually hated the thing. So now the cause is fiscal austerity — and we keep hearing about supposed examples of countries that experienced a boom after tightening fiscal policy, supposedly demonstrating that austerity is good, not bad, for employment. First was Canada in the 1990s, which turns out to be a quite different story. Now we’re hearing about Ireland in the 1980s. So, time for a little research. And whaddya know: this story is also not at all the way it’s being told (pdf). Yes, Ireland had fiscal austerity — but it also benefited from a devaluation and an inflationary boom in the UK. Oh, and Irish interest rates fell sharply, which was possible because they were very high to begin with; that’s not much of a precedent for the United States today, which starts with very low rates.

Will austerity programs doom the recovery? -One of the great uncertainties facing the global economy heading into 2010 concerned exit strategies. At what point was it safe for governments to begin unwinding the massive stimulus programs implemented to fight off the Great Recession? We always knew this was going to be a tricky question. Cut back too soon and sink the global economy into a “double-dip” recession; wait too long and run the risk of pumping up asset bubbles, inflation and government debt. Unfortunately, jittery markets have answered this question for us, at least in part. In the wake of the Greek sovereign debt crisis, investor attention has been squarely focused on rising government debt and deficits throughout the developed world, putting pressure on policymakers to rein in fiscal spending no matter what underlying economic conditions they face. Governments are clearly getting ushered to the exits. That has raised the scary question: Are we exiting from stimulus too soon? And will the new commitment to austerity imperil the global economic rebound?

Why the United States and Europe can't cut their way to economic prosperity. - If British voters thought they had replaced the dour visage of Labour Prime Minister Gordon Brown with an optimistic one in fresh-faced Tory David Cameron, they were sadly mistaken. On June 7, the new PM Cameron brought down the hammer, telling the British public that the most urgent issue ahead "is our massive deficit and our growing debt. How we deal with these things will affect our economy and our society, indeed our whole way of life." We're not hearing that kind of rhetoric in the United States yet, but the new austerity has crossed the pond. Even though unemployment remains at 9.7 percent, the House of Representatives in May scaled back a proposed jobs bill out of concern for the deficit. President Obama recently called for federal agencies to identify cuts of up to 5 percent in 2012. States and cities are slashing budgets and raising taxes. Around the world, what economist and New York Times columnist Paul Krugman has called "the pain caucus" is in the ascendancy.

Jobless aid bill hits deficit wall in Senate -– President Barack Obama's plea for more stimulus spending as insurance against a double-dip recession hit a roadblock in the Senate on Wednesday, the victim of election-year anxiety over huge federal deficits. A dozen Democrats joined Republicans on a key 52-45 test vote rejecting an Obama-endorsed, $140 billion package of unemployment benefits, aid to states, business and family tax breaks and Medicare payments for doctors because it would swell the federal debt by $80 billion. The swing toward frugality runs counter to the advice of economists who support the bill's funding for additional jobless benefits and help to states to avoid layoffs of public service jobs. They fear that the economy could slip back into recession just as it's emerging from the biggest economic downturn since the Great Depression.

Democrats Embrace Flat Earth Economics - I had a phone call the other day from someone from the DNC, asking for a donation and preying on my fears that the GOP might retake control of Congress in 2011. My response: “What’s the difference?” Policy specifics aside, if looks like flat earth economics is going to keep a lid on aggregate demand for a long time. Just look at this article in the Washington Post on Democrats joining the effort to dismantle an unemployment aid package because of deficit fears: President Obama’s urgent plea for more spending on the economy ran into the political buzz saw of the Senate on Tuesday, where Democratic leaders began chopping apart an aid package for unemployed workers and state governments in an effort to lessen its impact on the deficit.

The Non-Jobs Bill - Congress' effort to pass a jobs bill stalled in the Senate on Wednesday. In part, the upper chamber tied itself into Senate-like knots thanks to the usual partisan wrangling. But the proposal has also rekindled a debate over the need for more economic stimulus versus fear of rising deficits. This argument is important and healthy, but wildly overblown in the context of such a small and poorly-targeted bill. In one corner are those liberals who argue that failure to pass this measure will send the economy spiraling into a catastrophic double-dip recession. This, they say, is what happened in the mid-1930s, when Congress tightened fiscal policy and a nascent post-Depression expansion collapsed. By contrast, fiscal hawks say this bill, on top of President Obama’s earlier $862 billion stimulus, is the last straw. We cannot continue to spend money we do not have without turning ourselves into Greece.

Unemployment may be at 9.7%, but the Senate is moving on - Or, at the least, they care about the deficit more. By a vote of 52 to 45, the Senate rejected a jobs package that would've extended unemployment insurance, offered some tax breaks to individuals and businesses, kept doctors in the Medicare program and more. "$77 billion or more of this is not paid for," said Sen. Ben Nelson, "and that translates into deficit spending and adding to the debt, and the American people are right: We've got to stop doing that."No, sir, they're wrong, and we don't. It's hard to say this loudly enough, but it really doesn't make sense to offset stimulus spending, at least in the short term. The point of the money is to get the economy moving faster, to give people cash to spend. This isn't like health-care reform, where you're purchasing something and you should pay for it. When you're trying to expand the economy, you need to use debt to put more money into it than would otherwise be there. There'll come a time when we need to start reducing the deficit. If we can get the economy back into gear, that time might even be soon. But for now, increasing the size of the deficit isn't some nasty side effect of stimulus spending. It is, quite literally, the point of the enterprise.

Fiscal policy: Not serious | The Economist - LAST night, the Senate opted to kill an economic assistance package consisting of measures like extensions to unemployment benefits and targeted tax breaks to individuals and businesses aiming to boost spending and hiring. The reason? Well, according to Ben Nelson the problem was that, "$77 billion or more of this is not paid for...and that translates into deficit spending and adding to the debt, and the American people are right: We've got to stop doing that." This is what passes for wisdom in the upper house, but it's completely absurd. The reasons to be concerned about debt levels are that you're worried about the ability to continue funding the government, or you're worried about high interest rates crowding out private investment, or you're worried about the fiscal burden you're passing on to future generations, or some such thing. On all of those counts, the $77 billion in deficit spending associated with this package is essentially a non-issue. It won't prevent the deficit from declining through the middle of the decade, and it won't have anything to do with the big jump in borrowing thereafter, associated with increased spending on entitlements.

No Clear Path Forward After Jobs Bill Fails Again In Senate - Deficit concerns once again trumped jobless aid in the Senate as Republicans, a lone Democrat and Sen. Joe Lieberman (I-Conn.) on Thursday evening defeated an urgent bill to reauthorize expired several expired domestic aid programs. The 56-to-40 vote left Democrats with no clear path forward on legislation that, among other things, would protect doctors from a 21 percent drop in Medicare reimbursement rates, reauthorize extended unemployment benefits, and provide $24 billion in federal assistance to state Medicaid programs, preventing an expected wave of public sector layoffs. "Tonight, every single Republican voted to deny states critical aid that would keep firefighters, police offices and teachers employed,""And tonight, every single Republican voted to tell the one in ten Americans who have lost their jobs that they are on their own."By the end of this week, 903,000 people who have been unemployed for longer than six months will have missed benefits checks they would otherwise have received had Congress managed to reauthorize the stimulus bill provisions that expired on June 1. By the end of next week, that number will climb to 1.2 million.

The Top 10 Reasons Congress Needs to Stand Tall on Stimulus - CBPP - “Most striking is the sense of political paralysis in both chambers and an almost visceral hunkering down in the face of the tough choices ahead,” Politico’s David Rogers wrote this morning regarding the Senate’s failure thus far to approve pending jobs legislation. There’s nothing funny about any of this, but with apologies to David Letterman, below is our top 10 list of reasons why Congress needs to find the courage to pass a serious jobs bill that (among other things) extends key pieces of last year’s Recovery Act that would provide additional unemployment insurance (UI) benefits, especially for the long-term unemployed, and fiscal assistance for states. These provisions helped the Recovery Act provide jobs for as many as 2.8 million workers as of the first quarter of this year, and extending them would give the economic recovery a needed boost over the rest of this year

How Victorianism Pervades Our Economic Debates - A depressing pall has been cast over American political and economic discourse -- the specter of deficit reduction. Sixteen months after a greatly pared-down stimulus package was passed by Congress, as a response to the worst economic crisis since the Great Depression, public discussion about appropriate taxing and spending priorities have become warped by an insidious, if often implicit, moralism. Official unemployment hovers around ten percent. Accounting for those who are involuntarily working part-time, or have dropped out of the labor force because they've given up looking for work (understandable, since there are about five unemployed people for every job opening), the so-called U-6 figure is closer to seventeen percent. About one in five American children lives below the poverty line and the figure is rising. Public infrastructure and public schools are suffering under the weight of long-term neglect and savage budget cuts.

The President’s fiscal dilemma - The President sent an off-key letter to Congressional leaders last Saturday. While our efforts over the past 18 months have helped break the freefall and restore growth, it is essential that we continue to explore additional measures to spur job creation and build momentum toward recovery, even as we establish a path to long-term fiscal discipline. In the letter the President presses Congress to enact the “extenders bill.” You can see his list of spending priorities for the bill. The letter is being interpreted primarily as a push for nearly $50 B in new aid to States: $23 B for teachers, and $25 B for Medicaid. The letter includes a key sentence with technical meaning: “We must take these emergency measures.” The word emergency is code for “you don’t have to offset the deficit increase resulting from this spending.” This is the green light for Congress to spend away. The letter then pivots to deficit reduction:

Ezra Klein - Worst-of-both-worlds fiscal policy - A lot of the debate over deficits right now comes down to how you feel about interest rates. Normally, interest rates should be a conversation-ending indicator. If our deficits are too high, interest rates on government debt should be high, too, as that's how the market would compensate for the risk that we won't pay people back. But interest rates, of course, are very low. Even historically low. That should mean that our deficits aren't a problem, at least not in the short term. That's the stance taken by Paul Krugman and Brad DeLong. But these are abnormal times, and some people think that our low interest rates are a product of, in the first case, catastrophes everywhere else, and in the second case, the fact that the market is staffed by idiots who miss important information for a long time and then all panic about it at once (remember the subprime crisis?). Rather than showing us that we don't have a problem, our low interest rates, according to this school of thought, are masking the fact that we do -- and making the eventual reckoning worse.

Ryan Avent; Fiscal austerity: The health deficit - PETER ORSZAG head of President Obama's Office of Management and Budget, has argued tirelessly that health reform in America is fiscal reform. And he's right. A look at the CBO's long-term budget forecast indicates that the solvency-threatening spending growth in America is overwhelmingly about Medicare and Medicaid. To get another sense of the challenge, have a look at chart below, from the IMF's latest Fiscal Monitor:On the x-axis, we have the projected fiscal adjustment over the next two decades, and on the y-axis we have projected health and pension spending increases over the next two decades. You can see America's precarious position. This is a significant problem. The conventional wisdom is that America's fiscal adjustments should be easier than those in places like Europe and Japan, thanks to more favourable demographics associated with a younger population. But while other indebted nations have older populations, they also have done much more to slow the growth of health spending.

That ’30s Feeling - Krugman - NY Times Suddenly, creating jobs is out, inflicting pain is in. Condemning deficits and refusing to help a still-struggling economy has become the new fashion everywhere, including the United States, where 52 senators voted against extending aid to the unemployed despite the highest rate of long-term joblessness since the 1930s. Many economists, myself included, regard this turn to austerity as a huge mistake. It raises memories of 1937, when F.D.R.’s premature attempt to balance the budget helped plunge a recovering economy back into severe recession. But despite these warnings, the deficit hawks are prevailing in most places — nowhere more than here, where the government has pledged 80 billion euros, almost $100 billion, in tax increases and spending cuts even though the economy continues to operate far below capacity. What’s the economic logic behind the government’s moves? The answer, as far as I can tell, is that there isn’t any

The dubious nature of Money - We have another proclamation that Keynesian policies are dead. My difficulty with that claim consists of the fact that there has not been a burial as yet, and Keynesian policy has always been a rotting corpse. Even Lord Keynes had great doubts about Keynesian policy. The delayed Death scene is basically caused by the allowance Keynesian policies give Politicians to spend other peoples’ money, all without taxing anyone for anything. One has to kill that Skunk every day, and everyone gets tired of the repetitive labor. I once advocated a plan where legislators had to pay a percentage of any deficit aroused from their own Salaries, but legislative passage proved impractical. James Galbraith presents another side to the argument. His entire contention states that the elements which are functioning well should not be distorted in the balanced budget debate; a factor on which I could agree. It is not the fault of the Poor and the Elderly that Congress spent the Social Security Fund. Taxpayers paid the taxes in good faith, while legislators only used the circumstance to further their own agenda, without resort to actually funding a sound tax system.

Ezra on “Worst of Both Worlds” (Neither Walking Nor Chewing Gum) -economistmom - On his Washington Post blog today, Ezra Klein basically says the same thing I did a few days ago. The deficit hawks and stimulus lovers are so busy arguing that the other party is completely insane that they’re unable to recognize that they actually are working for the same cause (the economy, stupid)–and should be instead coming together symbiotically: It seems we’re getting the worst of both worlds: The argument over deficits is keeping us from doing what we need to do to help the economy grow right now, but it isn’t going to be enough to get us to do what we need to do to help the economy grow later, either. And the outcome of that could be ugly: If growth is anemic when the eventual fiscal crisis does come, that’s going to make a response much, much harder. I think policymakers need to be reminded that in keeping with the desirable “symbiotic” relationship, not all deficit-financed policies for short-term stimulus, and not all deficit-reducing policies for longer-term fiscal sustainability, are created equal.

Austerity is stupid, stimulus is dangerous, lying is optimal, economic choices are not scalar - When I checked out out a few weeks ago, there was a debate raging on “fiscal austerity”. Checking back in, it continues to rage. In the course of about a half an hour, I’ve read about ten posts on the subject. See e.g. Martin Wolf and Yves Smith, Mike Konczal, and just about everything Paul Krugman has written lately. While I’ve been writing, Tyler Cowen has a new post, which is fantastic. Mark Thoma has delightfully named one side of the debate the “austerians”. Surely someone can come up with a cleverly risqué coinage for those in favor of stimulus? Here are some obvious points:

I Hate Austerity - Noni Mausa -Austerity is one of several American images of virtue. Austere people are not wasteful, they save their money, they use the same dining room table and dishes for 50 years, they subscribe to Consumer Reports --and take notes. They steadily save 20% of their income for decades on end, and they buy with cash when they buy it all. They think about what they're going to say before they say it, and often say little or nothing. In any event, an austere person probably exhibits all four of the earthly virtues, and this doesn’t make him a very desirable consumer from the point of view of business. So why are we suddenly being told that the ownership society ought to be replaced by the Benedictine society, or possibly something along Buddhist lines? Ah, but you see this particular "austerity" is only intended to be temporary, partial austerity, nothing permanent.

Joseph Stiglitz: Fiscal conservatism may be good for one nation, but threatens collective disaster - What is unambiguously clear about the European economies, including that of the UK, is that if they all decide to cut their borrowing, slash spending and raise taxes, and do so at the same time, growth will be lower than it otherwise would have been. It means that there will be fewer people in work than would otherwise have been the case, and, because tax revenues will be depressed and unemployment benefit payments higher, the improvement in budget deficits will be much less than hoped for. It a classic Keynesian paradox; what is good for one nation can be disastrous for all. There is a risk that the European economy will go into a "double-dip" recession. Although obviously important, that doesn't matter so much as the big picture: stagnant economies poised on the edge of deflation. In the US, the forces of conservatism are also at work, although there are more voices, mine included, arguing for continuing public investment in the economy.But the fiscal conservatives do seem to be gaining ground, which adds to the risk of a global weakening of all the advanced industrial economies.

Richard Koo and Potential Motivations for the Pain Caucus - Krugman has been on a roll dealing with the notion that austerity needs to be introduced now, now, now in order to Appear Serious. Lately, he’s been looking, along with Mark Thoma, Yglesias, Brad Delong among others, as to what are the potential motivations behind this push.My 2 cents: I wonder if part of the motivating factor for beltway insiders and talking heads, if not academia, is that they vaguely remember the Federal Reserve “getting tough” in the early 1980s, introducing pain, and then the problems went away. And nowadays “structural reform” is in the air, Paul Volcker is back in the headlines, and it’s like it’s 1982 all over again. Except of course everything is different. I might just go ahead and live-blog Richard Koo’s book, The Holy Grail of Macroeconomics: Lessons From Japan’s Great Recession, but here’s a chart:

Fiscal Fantasies- Krugman - It’s really amazing to see how quickly the notion that contractionary fiscal policy is actually expansionary is spreading. As I noted yesterday, the Panglossian view has now become official doctrine at the ECB. So what does this view rest on? Partly on vague ideas about credibility and confidence; but largely on the supposed lessons of experience, of countries that saw economic expansion after major austerity programs. Yet if you look at these cases, every one turns out to involve key elements that make it useless as a precedent for our current situation. Here’s a list of fiscal turnarounds, which are supposed to serve as role models. What can we say about them?

Krugman: Right Result, Wrong Reason - PK continues to fight the good fight for Keynesian common sense in the face of resurgent austerity. The austerity front, which brings together Tea Partiers and Tories, blue dogs and Bundesministerien, wants to snuff out last year’s stimulus and force the North Atlantic economy to sink or swim. It’s chances of sinking are frighteningly large. Krugman says we should keep applying fiscal CPR until economic growth is in full recovery and unemployment has dropped—and until the zero lower bound on interest rates no longer binds, and normal monetary policy becomes an option.Yes but. There is an enormous hole in Krugman’s argument. A chief worry of the austeritarians is that their country—Britain, Germany, even the US—will be the new Greece, abandoned by creditors and teetering on default. Krugman’s response is that the creditor flight threat is imaginary.The markets aren’t worried, so why should we be? Does anyone else notice that this argument rests on the assumption that low interest rates today guarantee low rates tomorrow?

US political figures attack European austerity measures - An alliance of hard-right Republicans and liberal economists are increasingly anxious about the economic impact of austerity in Europe. Germany is the chief target of several angry outpourings for its plans to achieve austerity at home while maintaining exports, chiefly to the US. The net effect of chancellor Angela Merkel's plans is to limit German consumer debt while US consumers carry on spending with their credit cards. By the end of the year the German debt will be only slightly larger, while the US debt balloons. France and Britain are operating a similar policy, with the UK benefiting from a cheap pound and France a cheap euro that makes exports more affordable, but they tend to creep under the political radar. Only the US is maintaining a Keynesian stimulus package that artificially boosts demand, while mainly right-wing governments in Europe enforce austerity.

Faced with bailout or collapse, should US choose collapse…The big debate is between those who think the authorities are being too tight and those who think they are being too loose. Broadly, Europeans are on one side. Americans are on the other. The Europeans are tightening up. The Americans are letting rip. They’re both wrong, as far as we’re concerned. It’s all nonsense. Just goes to prove our dictum that people come to think what they must think when they must think it. The Euro-feds can’t afford to think they can loosen up. Their lenders have already laid down the law: ‘Keep spending like the Greeks and we’ll hit you with Greek-style interest rates.’ Just a few weeks ago the Greeks were forced to pay 16% interest. At that rate, borrowing is out of the question. The US doesn’t have to think about austerity. Not yet, at any rate. They’ve got the whole world ready to lend them money. ‘Here, take a drink of rice wine,’ say the Chinese. ‘Here is some champagne,’ say the Europeans. ‘And here’s a bottle of whiskey,’ say the jokers in the back of the room. It is only a matter of time before Americans fall down. Not so, say the Keynesians – led by Paul Krugman and Martin Wolf. They say it’s just a matter of managing the situation. Enjoy the party. You can pull yourself together later.

On the lessons from the Canadian federal deficit in the 1990s - It would appear that there is a significant constituency in both the US and in Europe agitating for immediate efforts to reduce their respective governments' deficits, and some are pointing to the Canadian experience of the 1990s. If Canada could make the swift transition from decades of large and chronic deficits to being the poster child of fiscal rectitude with no apparent ill effects, then why can't everyone else? The answer is that Europe and the US in 2010 is not Canada in 1995, in pretty much every way that matters.

Pete Peterson and the Deficit - Some commentators have vilified Peter Peterson, the investor and former Commerce secretary, for raising alarms about the deficit. They argue that Mr. Peterson is really trying to shred the American safety net. I’m not among the vilifiers. We should be taking the deficit more seriously, and Mr. Peterson is trying to make that happen. But it’s certainly true that he and his foundation would help their case by supporting more deficit-reduction measures that hurt wealthy investors like him. Landon Thomas Jr. of The Times wrote a good article in 2008 explaining Mr. Peterson’s support for a special tax provision for investment income, and now the group Citizens for Tax Justice points out the following: The Peter G. Peterson Institute, which is ostensibly concerned about the U.S. fiscal imbalance, has come out against provisions in [a Senate bill] that would prevent multinational corporations from abusing foreign tax credits….

Ezra Klein - Opportunity knocks, but America probably wont answer…Ryan Avent posts a chart at his place that I find a bit hard to read but that takes dozens of countries and compares their total anticipated increase in health and pension spending from 2011 to 2030 with the total deficit reductions that they'll need to balance their budgets over that period. The United States does not look good on this chart. Which is a reminder that our eventual deficit reduction is primarily an issue of health-care costs. And they'll be going up at the exact moment our deficit needs them going down. Which is why, as Avent says, "the mark of someone serious about debt issues is an obsession with health cost control." Stimulus spending has nothing to do with it. If you wanted to be optimistic about this, you could say that this represents a sort of opportunity. In sharp contrast to, say, France's health-care sector, our health-care sector is dramatically, joyously, wildly inefficient. We pay so much more than anyone else and get so much less that it's easy to imagine a world in which we have a drastically different health-care system that's both better than the one we have now and that's wiped out our deficit. I've always like CEPR's budget-deficit calculator, which allows you to plug other nations' per-capita health-care spending into our budget picture and see what happens. And what happens is that our deficit problem disappears entirely:

How debt imperils national security - Several months ago, a group of logistics officers at the Industrial College of the Armed Forces developed a national security strategy as a class exercise. Their No. 1 recommendation for maintaining U.S. global leadership was "restore fiscal responsibility." That's a small illustration of what's becoming a consensus among national security experts inside and outside the Obama administration: To play an effective role in the world, the United States must rebuild its economic strength at home. After a decade of war and financial crisis, America has run up debts that pose a national security problem, not just an economic one. This need to restore domestic prosperity and share the costs and burdens of global problem-solving with other nations will be one theme of the new "national security strategy" that the White House releases this week.

The national security shell game - In American public discourse, national security is the first refuge of scoundrels. For six decades good and dreadful ideas alike have been buttressed by claims that they will help make us secure. President Eisenhower used the claim to promote spending on highways and education. President George W. Bush used it to justify wiretapping and torture. Now deficit hysterics have started trilling the national security song to justify a coming attack on Social Security and Medicare.

Left-Right Defense Wonk Coalition Looks to Cut $960 Billion From Bloated Pentagon Budget - Few communities of Washington wonks run into greater structural and institutional obstacles than advocates of reduced defense spending. Defense companies put billions into PR campaigns for the necessity of this or that project that runs over cost. But undeterred by all that is a coalition of liberal and conservative defense wonks from the Project on Defense Alternatives, the Center for American Progress, the Cato Institute, Taxpayers for Common Sense, the Center for Defense Information and more. Calling themselves the Sustainable Defense Task Force — thereby taking up the “sustainability” call for budget austerity from Defense Secretary Robert Gates and his undersecretary for policy (and likely successor), Michele Flournoy — they identify up to $960 billion in spending cuts over ten years. That’s in a new report they’re releasing this morning.

How Do You Budget When There's No Agreement On What 2+2 Equals? - I was wrong when I said in the June 1 Fiscal Fitness that zero-based budgeting hadn’t been a topic for polite conversation since it was tried in Washington, D.C., in the late in 1970s. At almost the precise time that I was writing those words Georgia was considering legislation to reimpose ZBB. Three days after Perdue’s veto, CNBC host Jim Cramer and Sen. Tom Coburn (R-Okla.) talked on air about another topic that seldom makes it even to the back burner, let alone the front, of most federal budget debates: They wanted to know why the government wasn’t locking in the relatively low interest rates by borrowing more in the long term instead of in the short term. They admitted that doing this would cost taxpayers more over the next few years. But they also said this strategy would save money in the future because federal interest costs will increase when the existing short-term securities are refinanced at the higher rates that they said were likely. These two seemingly unrelated topics — ZBB and federal borrowing costs — actually have one very important thing in common: They are both based on the faulty assumption that, even though it is done in a highly political and increasingly partisan environment, budget decisions somehow can be based on undisputed or indisputable facts and figures. To say the least, that’s anything but the case.

Focus on National Security - Concerns about budget deficits and rising debt levels are leading to fractures in the heretofore unified conservative support for ever-higher defense spending. At least a few Republicans are now openly suggesting significant cuts in the defense budget, raising concerns among conservatives primarily concerned about national security. I believe that ultimately national security conservatives will be forced to choose between cuts in the defense budget and tax increases to reduce deficits.

The Myth Of The Deficit And National Security - Over at Economist's View, Mark Thoma excerpts from an excellent op-ed by Jamie Galbraith on national security and the deficit that appeared in yesterday's Los Angeles Times. Here's the whole piece from the LA Times if you want to see it for yourself. Galbraith gets into a number of issues, but his key point is that those that say the deficit hurts this country's national security aren't relying on anything substantive to make their case. It's hard not to agree. If you believe, for example, that the U.S. military activities in Iraq and Afghanistan are/were needed to enhance security here at home, then you have to admit that the effort would have been far smaller or not taken at all had it not been for a willingness to borrow to finance the activities. That, of course, implies that others were willing to lend the U.S. money to make it happen.

Estate Tax--Kyl continues working for the ultra wealthy - Jon Kyl doesn't think much about the government helping the unemployed who have been laid off because of the financial crisis, triggered by greedy excesses at the nation's biggest banks and mortgage lenders. He's afraid that providing additional unemployment compensation will keep people from working--as though it is laziness and not trying circumstances that has forced people out of jobs and on the public dole. But Kyl does work hard for his friends. He would like to repeal the estate tax, so the country's millionaires and billionaires wouldn't ever have to pay their fair share of the tax burden. Most of them pay almost no taxes during their lifetimes--especially if their wealth is inherited and most of their income is financial. They get preferential rates for the taxes they do pay, they devise all kinds of scheme to defer payment (using loans to monetize assets that need not be sold til after death), and yet are the primary beneficiaries of the governmental stability and economy that ordinary folks' taxes pay for.

On Trimming the “Extenders” Bill Without Actually Trimming the Extenders - The Senate is having a lot of trouble trimming the cost of a bill intended to continue expiring tax cuts–the so-called “extenders” bill. Trouble is, they’re not willing to actually trim the actual “extenders.” In fact, the “extenders” are such legislatively-sacred cows that they are used as a vehicle for other policies that are (oddly) not considered as sacred–like extension of unemployment benefits or even extension of the so-called “doc fix.” What the Senate is tinkering with right now are these hitch-a-ride attachments to the extenders bill and the various revenue offsets designed especially to help pay for the extenders. So the House and Senate have both complained that extending the extenders is “too expensive.” But both the House and the Senate have yet to contemplate this: if we’re not willing to put up with the offsets required to pay for these tax extenders, then maybe this tells us these tax extenders are not worth their cost!

FATCA (foreign account tax compliance act - FATCA (foreign account tax compliance act--or is it the anti-fatcat act?) The attention of US tax enforcement has been focused on offshore issues for some time. Of course, the most conspicuous part of that has been the ongoing dispute with UBS, a Swiss bank that facilitated tax evasion by US taxpayers under the Swiss banking secrecy rules. After some breakthroughs, the US was at the point of prosecuting the bank and got it to agree to release information on 4500 of the most significant accounts. But then a Swiss court intervened, requiring a parliamentary approval of the agreement. The upper house approved, but the lower house balked. The upper house has now re-approved the measure, with the hope that the lower house will now act in time to have the agreement approved before the June 18 end of the session.Further, as part of the HIRE Act, Congress passed a number of provisions earlier this year intended to make it much harder for wealthy Americans to hide assets offshore and evade paying their fair share of taxes on the income from those financial assets.

U.S. Soon Could Be Number 1 in Corporate Taxes - It is well known that the U.S. has the second highest corporate income tax among the major industrialized countries at more than 39 percent when the federal and average state rates are combined. Only Japan has a higher overall rate at nearly 40 percent. That soon could change. Reuters is reporting that Japan's ruling Democratic Party will include a corporate rate cut in its platform for the upcoming upper house elections. Should Japan cut its corporate income tax rate, the U.S. would find itself with the highest corporate tax rate in the industrialized world. The U.S. would also stand alone as one of the last remaining OECD nations to impose a world-wide tax system on corporate profits. Last year, both Japan and the United Kingdom took steps to exempt foreign earned profits from domestic taxation in order to stem the flight of capital out of their respective nations.

A Modest Tax Proposal - Here's the pitch: corporate income taxes are a drag on businesses and are ultimately paid by consumers anyway. That's bad. Conversely, a tax on carbon would reduce our oil use and spur energy efficiency. That's good! Likewise, a tax on financial transactions would reduce speculative volatility and help stabilize the financial sector. Also good! So we'd trade one bad tax for two good Pigovian taxes. What's more, although receipts from the corporate income tax are down right now thanks to the recession, within a couple of years they should be back up to around $400 billion a year. A financial services tax is probably worth around $100 billion a year, give or take, and that means we'd need a carbon tax of around $300 billion to keep everything revenue neutral. This is far higher than anything we could dream of without the grand corporate income tax bargain and holds out hope of being big enough to actually make a difference.

In Defense of Corporate Income Taxation - Kevin Drum suggests (modestly or “modestly”) that “everyone” should love the idea of trading the corporate income tax for carbon and financial transactions taxes. I should just have a chuckle and leave it at that, but then again I get emails from the Tax Foundation that are remarkably lacking in irony. Ezra Klein is happy with his policy-wonk hat on, but thinks there’s a political problem of giving fat cats an obvious break. I argue that the problem is not just political. Drum’s at least semi-serious claim is that taxing corporate income is bad because doing so is a drag on business and ends up getting paid by individuals anyway. Neither necessarily militates against corporate income taxation in the real world.Whether a “drag” on business or some other tax distortion that reduces private-sector activity (other things equal) is good or bad, on net, depends on the use to which the tax revenues are put.

Millions Pay No Income or Payroll Taxes Thanks to Refundable Credits - In 2008, the IRS paid out over $70 billion in refundable credits to people who had no income tax liability. Congress's Joint Committee on Taxation recently produced some estimates on the number of tax filers who receive refundable credits larger than what they pay in payroll taxes. This is an important contribution to the debate over the use of credits because in any discussion about the record number of non-payers, we frequently hear the refrain that "well, they do at least pay FICA taxes." In a May 28, 2010 letter to Representative Dave Camp and Senator Kent Conrad, JCT reports that between 2000 and 2006 the number of returns with refundable credits in excess of the employee's share of payroll taxes increased from 11.8 million to 16.1 million. In 2009 and 2010, those figures jumped to 23 million because of such things as the making work pay credit and the lowering of the income threshold for determining the refundable portion of the child credit to $3,000.JCT projects that the number of returns with refundable credits exceeding the employee's share of payroll taxes will hover between 14 million and 15 million for the next ten years.

Estimates of Average Federal Tax Rates – CBO Director's Blog - Yesterday CBO released estimates of average federal tax rates—households’ federal tax liability divided by their income—in 2007 for households with various amounts of income. For each income category, the report also presents estimates of average before-tax and after-tax household income; the number of households; and that category’s share of taxes and income. A page on our website, Average Federal Taxes by Income Group, includes CBO’s estimates of average federal tax rates going back to 1979, as well as other information and publications on household income and taxes.

Congressional Budget Office - Distribution of Federal Taxes…This page contains CBO's estimates of average federal tax rates (tax rates as a percentage of income) paid by households in various income categories for the four largest sources of federal revenues--individual income taxes, social insurance (payroll) taxes, corporate income taxes, and excise taxes--as well as the average rate for the four taxes combined. The page also contains estimates of average before- and after-tax household income; the number of households in each income category; shares of taxes, income, and households for each income group; information relating to the methodology used to construct the estimates; supplementary estimates for different types of households; and estimates of the number of households that pay more in payroll taxes than they do in income taxes.

The Growing Push to Impose a Transaction Tax - Among the hot button issues that Wall Street will be following closely next week at the Group of 20 economic summit meeting in Toronto is the idea of imposing a worldwide tax on financial transactions. The move, championed by the Europeans, is aimed at curbing excess speculation and building revenue. For now, the Obama administration is not supportive of such a tax, but international pressure and the widening budget deficit could possibly prod the United States to fall in line eventually. Financial transaction taxes are nothing new. Britain has had a 0.5 percent tax on stock transfers for years. The United States had a transaction tax from 1914 until it was phased out in 1966, and it has not been seriously considered as a revenue source until now. The Institute for Policy Studies, a left-leaning think tank, issued a report on Thursday promoting the benefits of such a tax. The report, titled “Taxing the Wall Street Casino,” contends that a transaction tax could raise $177 billion a year and could have even prevented last month’s so-called flash crash, in which stocks took a huge dive in just minutes and then suddenly shot back up.

Forget about deficits. Fix the banks - Levy senior scholar James K. Galbraith argues in the Los Angeles Times this morning that deficit hawks are pursuing the wrong prey. In a nutshell: The real cause of our deficits and rising public debt is our broken banking system. The debts our economic leaders deplore were largely due to the collapse of private credit, and to the vast giveaways the federal government made to banks to prevent their failure when credit collapsed. Yet those rescues have failed to reanimate private credit markets and job creation, as the latest employment reports show. And so long as that failure persists, public deficits and rising public debt must remain facts of life.Are broken banks a national security threat? Let’s avoid going that far. But the only way to reduce public deficits eventually is to revive private credit, and the only way to do that is build a new financial system to replace the one that has failed. .

The G-20 Needs to Refocus its Financial Regulatory Agenda -The G-20 leaders meet again in Toronto on June 26–27 and hopefully will make progress on reform of the International Monetary Fund and other issues of global economic governance. But on one distinctive part of their agenda, financial regulation, achievements so far are less impressive than the initial ambition. At the first G-20 summit in November 2008 in Washington, shortly after the Lehman Brothers collapse, there was much rhetoric, especially from Europeans, in support of “global solutions to global problems.” The implied goal was global harmonization of financial rules to restore financial stability, eliminate regulatory arbitrage (banks shopping around for the most favorable regulations), and ensure fairer competition. Financial regulation represented no fewer than 38 out of that summit’s 47 action items.Fast forward to the present and most flagship projects are in jeopardy. The Basel Committee’s negotiations on bank capital, leverage, and liquidity standards are proving difficult, and may not be completed this year as planned. Accounting standard setters are not achieving convergence on key issues, including financial instruments.

The Volcker Rule and the saga of State Street Bank -Cambridge Winter Center’s Raj Date has a new paper out: Test Case on the Charles: State Street and the Volcker Rule. In order to get a sense of why the Volcker Rule would be important, he walks his audience through the story of State Street bank, the 15th largest bank that had a nice, stable boring business model and decided to jump into the deep end of finance, necessitating a bailout at the end. Raj has many graphs that tell the story about why it is a good idea to silo out the high risk from the necessary, core functioning of the banking sector. I want to focus on three. Here’s what boring banking looks like:Click through on all three for a bigger graph with explanation. There it goes, making single basis point income off acting as a custodian for trillions of dollars of assets. This custody business is profitable, safe, and boring. So where do they dive into the deep end? Here’s what exciting banking looks like:

Richard Fisher of the Dallas Fed: Larry Summers, the G-20, and Financial Dementia - Richard Fisher, president of the Dallas Fed, has long been a proponent of serious financial sector reform. As a former commercial banker, he sees quite clearly that the legislation now headed into “reconciliation” between House and Senate versions amounts to very little. He also knows that pounding away repeatedly on this theme is the best way to influence his colleagues within the Fed and across the policy community more broadly. He is now taking his game to a new, higher level. Couched in the diplomatic language of senior officials, his speech on June 3 to the SW Graduate School of Banking was both a carefully calibrated assault on the administration’s general “softly, softly” approach to the big banks and a direct refutation of arguments put forward by Larry Summers in particular.

Fed’s Plosser: Reform Legislation Passage Not End Of The Process - A U.S. central bank official warned Wednesday that even as Congress nears the final whistle on efforts to reform the nation’s financial regulatory structure, the game won’t end. “This is certainly not the end of the process of regulatory reform,” Federal Reserve Bank of Philadelphia President Charles Plosser said. “Regulators will need to work out many details left open by the legislation” and “I don’t think that Congress’ approach is necessarily the final word on designing a resolution mechanism that will end the problem of firms that are too big to fail.” Plosser isn’t currently a voting member of the interest rate setting Federal Open Market Committee, and he didn’t comment on the monetary policy or economic outlook.