US Fed's balance sheet rises slightly in week - (Reuters) - The U.S. Federal Reserve's balance sheet rose slightly in the latest week, Fed data released on Thursday showed. The balance sheet rose to $2.328 trillion in the week ended June 23 from $2.327 trillion the previous week. The Fed's holdings of mortgage-backed securities backed by housing finance companies Fannie Mae (FNM.N) and Freddie Mac (FRE.N) totaled $1.129 trillion on June 23 versus $1.128 trillion on June 16. The U.S. central bank's ownership of debt issued by Fannie Mae, Freddie Mac and the Federal Home Loan Bank System was $165.61 billion on June 23 versus $166.21 billion on June 16. Primary credit via the Fed's discount window averaged $151 million per day in the latest week versus $104 million per day in the previous week.

FOMC Statement: Less Positive - The comments on the economy were slightly more negative than last meeting. The Fed noted the financial issues in Europe, and also commented that "underlying inflation has trended lower". Each statements was slightly less positive ...From the Fed: Financial conditions have become less supportive of economic growth on balance, largely reflecting developments abroad. The key language about rates stayed the same: "The Committee ... continues to anticipate that economic conditions, including low rates of resource utilization, subdued inflation trends, and stable inflation expectations, are likely to warrant exceptionally low levels of the federal funds rate for an extended period."

Parsing the Fed: How the Statement Changed - The Fed’s statement following the June meeting offered a more subdued assessment of the economy than April’s remarks. The central bank continues to see economic recovery, but makes no signal that rates are going to rise in the near term. (Read the full June statement.)

Redacted Version of the FOMC Statement - Changes in italics.

Federal Reserve Statement In English -- From The Fed: Information received since the Federal Open Market Committee met in April suggests that the economic recovery is proceeding and that the labor market is improving gradually. The economy is falling off a cliff. The Federal Government has blown over $1.5 trillion a year for the last two years to try to get private parties to lever up again, but they have no more credit capacity and still have no jobs. Household spending is increasing but remains constrained by high unemployment, modest income growth, lower housing wealth, and tight credit. Housholds can't spend what they don't have, and they don't have. There has been no income growth other than government handouts. Household "wealth" has been revealed to be an empty suit, devoid of any substance, as it was simply a $100,000 VISA credit line, which has now been slashed to $100.

The Lone Dissenter: Kansas City’s Hoenig Goes Four for Four - Four meetings, four dissents. Federal Reserve Bank of Kansas City President Thomas Hoenig kept his dissent streak going strong at today’s Federal Open Market Committee meeting. Given the rest of the FOMC’s stance — displaying more caution about the strength of the recovery — this probably won’t be Mr. Hoenig’s last dissent of the year.Mr. Hoenig was the lone opposing vote in the FOMC’s 9-1 decision to keep the federal funds rate near zero with the guidance that economic conditions “are likely to warrant exceptionally low levels of the federal funds rate for an extended period.”

What's Next For The Fed? Nothing, It Has Officially Become Useless - Today’s Fed decision is largely a non-event. The consensus believes the Fed will leave rates unchanged and is unlikely to alter their language too much as global double dip concerns have increased in recent months: “The FOMC announcement for the June 22-23 FOMC policy meeting is expected to leave the fed funds target rate unchanged. With continued market skittishness over sovereign debt problems in Greece and other European countries, the Fed is likely to be cautious about plans for unwinding its expanded balance sheet. Fed watchers likely will focus on statement wording regarding the status of the economy-notably any signs of labor market improvement.” But as the seemingly endless zero interest rate policy continues some at the FOMC are beginning to get antsy about the Fed potentially being behind the 8 ball as they were in 2002 and heading into the recession. Of course, I think we are looking more and more Japanese. The problems in Europe have almost certainly compounded our problems and that likely means the Fed will be even more hesitant to raise rates. A recent SF Fed paper confirms this thinking. They believe the current environment is similar to Japan:

Fed Is Likely to Remain on Sidelines Longer - The Federal Reserve left rates unchanged at its policy-setting meeting today, but low inflation and continued uncertainty about the recovery has economists pushing their forecasts for the eventual rate increase even further into the future. In a midmonth addendum to the Wall Street Journal’s economic forecasting survey conducted this week, 15 of 44 responding economists moved their expectations for when the Fed will raise rates further into the future compared to their responses just three weeks ago. Only three respondents pulled their estimates back. On average, the economists don’t see the central bank changing rates until March 2011. Futures markets see a 45% chance that rates will remain in the current 0-0.25% range through March, up from just 23% last month.“There are lots of reasons to stay on the sidelines– no reason to move,”

Fed holds the line; I predict an interesting 2nd half of 2010 -Here's the statement: Mark Thoma thinks that fiscal and monetary policy should be used more aggressively, citing this David Leonhardt column in the NY Times. Leonhardt's column is worth quoting at length as it pretty succinctly describes the feeling that has been building in my mind and I'm sure in others over the first half of this year. If you fear that the recovery is about to stall, today's news on new home sales probably increased your worries. And in the midst this, an FOMC member, Hoenig (Kansas City), dissented from the consensus opinion. Hoenig and Bernanke have similar concerns about stability. Hoenig is of the opinion that keeping rates low will lead to risks to that stability. Bernanke seems to be hoping that they can maintain the low rates, but seems to be drawing the line at providing any further support like, say, buying long-term bonds and pushing those rates down as well.But what if GDP stalls in the 2nd half of 2010? Do you pull the trigger and use unconventional monetary policy? What is worse, another year of 10% unemployment or instability in the financial markets? If you wait too long to decide, will you get both?

The Caution of the Fed Comes With a Risk: Ben Bernanke believes that he and his Federal Reserve colleagues have the ability to lift economic growth.... Mr. Bernanke also believes that the economy is growing “not fast enough”... that unemployment will remain high for years and that “a lot of people are going to be under financial stress.” Yet he has been unwilling to use his power to lift growth and reduce joblessness.... How can this be? How can Mr. Bernanke simultaneously think that growth is too slow and that it shouldn’t be sped up? There is an answer — whether or not you find it persuasive. Above all, top Fed officials are worried that financial markets are fragile. They are not so much worried about inflation, the traditional source of Fed angst, as they are about upsetting the markets’ confidence in Washington. Yes, investors remain happy to lend the United States money at rock-bottom interest rates, despite our budget deficit and all of the emergency Fed programs that will eventually need to be unwound. But no one knows how long that confidence will last

What Does the Federal Reserve Think that It Is Doing Right Now? -The Treasury real yield curve is at 1.2% for ten years. The Treasury nominal yield curve is at 3.2% for ten years. If anybody out there in the private market thought that such a panic was possible, or even likely, its possibility would be priced into the Treasury yield curve right now.At the start of December 2008 credit default swaps on Greece were at 250 basis points, on Ireland 220, on Portugal 170, on Spain 130, on Italy 100--the marginal investor in the market was betting that there was one chance in 100 that Italy would experience a credit default event, and 2.5 chances in 100 that Greece would experience such an event.Now the United States is at 40: way down from the 100 it was at at the start of March 2009:When CDS prices in the U.S. rise to indicate that there are some investors in the U.S. who think it is worthy buying insurance by betting that there might be a panic, then I can undersand Bernanke's caution.But that's not where we are, is it?

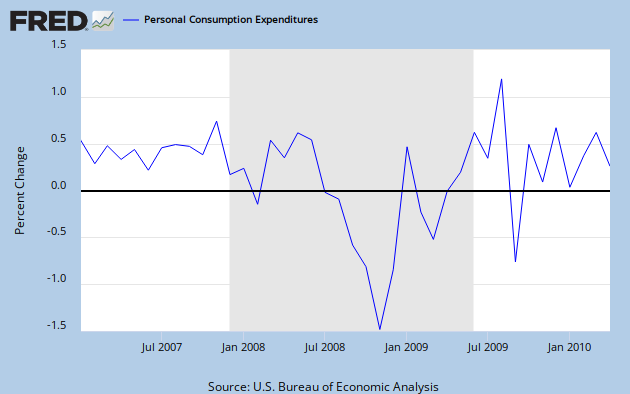

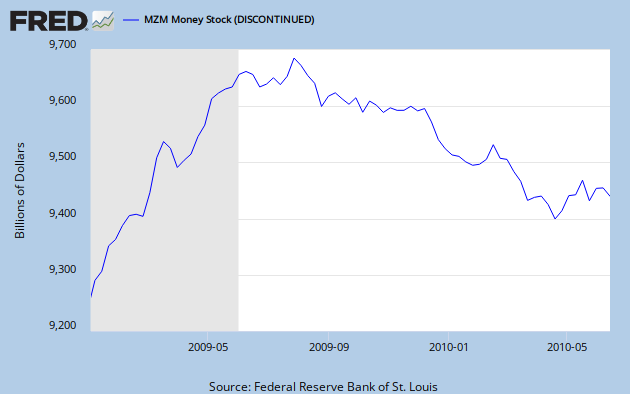

Why Isn't the Fed Doing More? - It appears that that total spending in the U.S. economy is slowing, if not outright contracting. Retail sales fell in May while in April personal consumption expenditures stalled. In addition, housing starts and homes sales plummeted in May. Meanwhile, the MZM measure of the money supply has been declining since late 2009. Since these developments indicate that both money (M) and velocity (V) are declining, it is safe to conclude that aggregate demand (PY) is falling too (i.e. MV = PY). Given these developments why isn't the Fed doing more to help the U.S. economy? Surely, it can stabilize MV. Here is what three observers had to say in response to this question: 1. David Leonhardt. Financial markets are fragile and the Fed does not want to upset the market's confidence in the U.S. government by further easing of monetary policy....2. Daniel Gross: The Fed is exhausted from its grand experiments in central banking.... 3. Ryan Avent: There is division within the Fed on whether further monetary stimulus is really necessary... There may be some truth in these responses, but let me add two more potential reasons for the Fed's inaction.

What the Fed Did and Why - NY Fed - In my remarks this morning, I would like to look back over the events of the past several years and offer my perspective on what were the essential drivers of the financial crisis and the Federal Reserve’s interventions.1 I will review the changes that have been taking place in the U.S. financial system and how these changes created the conditions conducive to the crisis. I will then discuss the developments in residential real estate financing that provided the catalyst for the crisis. With this background, I will outline the interventions that were carried out to mitigate the crisis, focusing on those conducted by the Federal Reserve. I will direct my remarks to the facilities that were created rather than to the actions taken for individual institutions since these have been discussed extensively elsewhere. The lessons learned from the crisis are important for the design of the policy response aimed at reducing the likelihood that the U.S. economy ever again experiences this degree of trauma.

Why Is It Unsustainable for the Fed to Continue to Hold Financial Assets? -David Leonhardt had a thoughtful piece about the Fed's decision to accept higher rates of unemployment rather than engage in more aggressive quantitative easing to boost the economy. At one point he asserts that: "There is a direct analogy between the budget deficit and the Fed’s asset holdings. Neither is sustainable. The Fed has to show it has a strategy for selling the trillions of dollars of assets it bought during the crisis — without damaging the value of private investors’ holdings and without, at some point, igniting inflation." It is not clear that why continued holding of assets is unsustainable. Japan's central banking has been holding vast amounts of the government's debt for more than a decade and yet it is still in the situation of fighting inflation. In the context of sustained economic weakness there is no obvious way that holding government assets will lead to inflation. Furthermore, even if the economy was to rebound, the Fed has other mechanisms for preventing inflation, such as raising reserve requirements, which can allow it to continue to hold assets without causing inflation.

Bruce Krasting: What’s Ben Gonna Do? - Every day the deflation story gets stronger. Almost all of the numbers in the US are pointing in that direction. A slowdown in the EU is a sure thing. Japan is going nowhere. China is a question mark, but even if they do continue growing it will not result in enough Eco. Juice to offset the global deflationary forces. I was anticipating a slowdown in the 4th Q. It is now looking more likely that we will fall of a cliff starting July 1st. Extended benefits will be ending. Most states start a new fiscal year and they are all dead dead dead on revenue. Any benefit we got from the census will be in reverse gear. By August 1st approximately 1mm temporary workers will again be out of a job. Housing is falling off a cliff. The market sees this. The ten-year is at an incredible 3.1%. The last few days of trading in gold has a smell of deflation as well. Bernanke must be beside himself. He bet the farm to save the economy in 2009. He has done things that no other Fed head as ever contemplated. As betting goes, he is “all in” on this one. He bet the economy, our future solvency and his reputation. In my opinion there is no way he is going to throw in the towel and accept that deflation is inevitable.

Ben Bernanke needs fresh monetary blitz as US recovery falters - Federal Reserve chairman Ben Bernanke is waging an epochal battle behind the scenes for control of US monetary policy, struggling to overcome resistance from regional Fed hawks for further possible stimulus to prevent a deflationary spiral. Fed watchers say Mr Bernanke and his close allies at the Board in Washington are worried by signs that the US recovery is running out of steam. The ECRI leading indicator published by the Economic Cycle Research Institute has collapsed to a 45-week low of -5.7 in the most precipitous slide for half a century. Such a reading typically portends contraction within three months or so. Key members of the five-man Board are quietly mulling a fresh burst of asset purchases, if necessary by pushing the Fed's balance sheet from $2.4 trillion (£1.6 trillion) to uncharted levels of $5 trillion. But they are certain to face intense scepticism from regional hardliners. The dispute has echoes of the early 1930s when the Chicago Fed stymied rescue efforts.

Why it is right for central banks to keep printing - Confronted with huge fiscal deficits, many have concluded that they should hurry fiscal tightening on as fast as possible, in the hope that it will prove expansionary. What are the chances that they will be right? Small, I believe. Moreover, rather better alternatives are on offer. But their drawback is that they are unorthodox: alas, many “sound” people prefer orthodox recessions to unorthodox recoveries. The first, one I made a week ago, is that the deleveraging cycle is generating huge private sector financial surpluses across the developed world. Unless we expect a shift into aggregate external surpluses (and corresponding deficits in the emerging world), these surpluses must now to be invested in government liabilities. This helps explain why yields on the bonds of safer governments remain so low. The second response is that if governments need to run deficits, to support demand at a time of private sector weakness, they can always borrow from central banks. Yes, this is “printing money”. It is also an insanely radical policy recommended by no less insane a radical than Milton Friedman, back in 1948. His view was that the government could expand the money supply during recessions and contract it in the subsequent booms.

Print away your troubles - REGULAR readers will know that I view a more expansionary monetary policy as a more-or-less can't-lose response to the current economic doldrums. It seems the idea is catching. Here's Martin Wolf, from his column this week: [I]f governments need to run deficits, to support demand at a time of private sector weakness, they can always borrow from central banks. Yes, this is “printing money”. It is also an insanely radical policy recommended by no less insane a radical than Milton Friedman, back in 1948. His view was that the government could expand the money supply during recessions and contract it in the subsequent booms. Money-financed stimulus was part of the prescription discussed by Ben Bernanke in the speech that earned him his "Helicopter Ben" nickname. It was also the subject of this recent post of mine. The same day Mr Wolf's column ran, the New York Times' David Leonhardt puzzled over the Fed's seeming complacence: Slate's Dan Gross, also pondering the Fed's inaction suggests today that the Fed may simply be exhausted, or has run out of imagination.

Martin Wolf Calls for a NGDP Target - Okay, maybe not quite but he comes close in his most recent article where makes the following statement (emphasis added): The argument for aggressive monetary expansion remains strong, though not equally everywhere, since the growth of broad money and nominal GDP is weak (see chart). So Friedman’s policy of “quantitative easing”, as it is called, still makes good sense. Note that Martin Wolf did not say the argument for aggressive monetary expansion is the looming deflationary pressures. Rather he focused on the anemic aggregate demand growth as indicated by his "nominal GDP is weak" statement. He seems to be making the point that monetary authorities should be targeting the cause, not the symptom in their conduct of monetary policy. If so, then Martin Wolf should have a chat with his fellow FT columnist Samuel Brittan who has explicitly called for monetary policy to stabilize total cash spending. He should also take time to read Scott Sumner's article on targeting expected aggregate...

Alarming Charts and Graphs June 2010 - Kalpa - Below, are important charts and graphs sounding alarm bells concerning the strength of our "recovery". First, Deutsch Bank released its June 23 "Global Economic Perspectives" (pdf) report titled "Financial Conditions Weakest since '08". What the WSJ has to say: In the second quarter, the U.S. Monetary Policy Forum's Financial Conditions Index fell to minus-1.82, its lowest since the fourth quarter of 2008, says Deutsche Bank. The index tracks 45 variables, including credit and yield spreads, stock-market data, banks' desire to lend and consumer perceptions. Although it remains above the minus-2.5 to minus-3.5 reached in the depths of the crisis, it has slid from minus-1.29 in the first quarter. The index paints a gloomier picture than narrower indexes like the Federal Reserve Bank of Kansas City's. This is because it gives weight to measures of credit availability, including asset-backed-securities issuance. This is weak, driving much of the deterioration. .The other figures which are alarming everyone, are the ECRI figures addressed by John Mauldin's latest newsletter.

ECRI Leading Economic Index Plunges At -6.9% Rate, Back To December 2007 Levels When Recession Officially Started - It's getting close: the fabled -10% annualized change (see David Rosenberg) which guarantees a recession is now just 3.1% away, which at this rate of collapse will be breached in two weeks. The ECRI is now at December 2007 levels, the time when the last recession officially started. The index dropped from an annualized revised -5.8% (previously -5.7%) to -6.9%. As a reminder, from Rosie, "It is one thing to slip to or fractionally below the zero line, but a -3.5% reading has only sent off two head-fakes in the past, while accurately foreshadowing seven recessions — with a three month lag. Keep your eye on the -10 threshold, for at that level, the economy has gone into recession … only 100% of the time (42 years of data)." We are practically there.

Double-dip fears raise worries the Fed is out of bullets - Economists are more nervous about the chances of another recession. And one of biggest fears is that the Federal Reserve may have run out of bullets to fight another downturn. "They do have some ammunition left, but it's not going to pack a lot of punch," said Mark Zandi, chief economist with Moody's Economy.com. Most economists aren't yet predicting that a double dip recession is imminent. Weaker-than-expected readings on job growth and retail sales have added to concerns that the recovery is stalling out. "Whenever the next recession comes, it is very important that policymakers have had the opportunity to reload their gun to fight the downturn," said Lakshman Achuthan, managing director of Economic Cycle Research Institute. "Today it's not clear that there's a lot more policymakers can do."

Fed Chairman Bernanke doesn't seem to care about high unemployment. Why? - The central bank says it has a trio of missions. The Fed "sets the nation's monetary policy to promote the objectives of maximum employment, stable prices, and moderate long-term interest rates." Long-term interest rates are near record lows, inflation is under control, and prices are stable, but maximum employment remains a far-off dream. In a speech earlier this month, Bernanke noted that "in all likelihood, a significant amount of time will be required to restore the nearly 8-1/2 million jobs that were lost nationwide over 2008 and 2009." In another recent speech in Michigan, he acknowledged that "high unemployment imposes heavy costs on workers and their families, as well as on our society as a whole." But he doesn't seem inclined to do anything about it. The Federal Open Market Committee this week stood pat on monetary policy and announced no additional efforts or initiatives to combat persistent high unemployment.

Natural Jobless Rate Seen Shifting Higher - Somewhere out there lies a trigger point for Federal Reserve rate hikes. While that policy tightening may not come for many months or even years, economists still believe the key variable is the interplay between employment and inflation. That interplay, most economists believe, has changed in the wake of the worst recession in generations. Structural changes in the economy mean higher rates of unemployment will be the new normal. As a result, inflation could start to well up from levels of joblessness that until recently had been benign for price pressures.At the heart of the issue is what economists call NAIRU, or Non-Accelerating Inflation Rate of Unemployment. It’s essentially the lowest level of unemployment that, if breached, will lead to rising inflationary pressure. NAIRU is tough to pin down, but even so, the concept has currency with many economists and Fed policy makers. Central bankers generally deal with the issue in a roundabout way, by talking about how much excess capacity the economy has.

Fed's Next Move Is to Ease, Not Tighten, Says Michael Pento - Michael Pento, chief market strategist at Delta Global Advisors, is confident the Fed’s next move will be to ease rates. “Ben Bernanke is a student of the Great Depression and he doesn’t want his tenure to be marked by the second Greater Depression,” he says. “So he will do whatever he can to boost money supply and fight deflation.” How will he do that with rates already at 0-0.25%?Obviously, they can’t lower rates. The Fed is also reluctant to start buying more mortgage-backed securities so soon after ending that program. The alternative, Pento says, is for the Fed to stop paying interest on excess reserves, a move that will drive banks to lend instead of sit on their cash.

Bursting bubbles - READING policy speeches by central bankers isn't as much fun as you'd imagine. Nonetheless, the past week had some interesting statements that offered a glimpse into the role of central banks post-crisis. A common thread that stands out is the talk of expanding the role of authorities to focus on macro-prudential policy in addition to plain old monetary policy. As Jaime Caruana points out, macro-prudential policy has become a buzzword of late. The BIS definition of the term as... ...the use and calibration of prudential tools with the explicit objective of promoting the stability of the financial system as a whole, not just the individual institutions within it...is sufficiently vague and broad to include a wide variety of instruments and institutions. But the key idea is that central banks should use regulatory policies to moderate asset and credit booms.

Inflation or deflation? - For the last year and a half my assessment has been that the near-term pressures on the U.S. economy were deflationary, while long-term fundamentals involve significant inflation risks. It's time for a look at the data that have come in over the last 6 months, and time to say that I still see things exactly the same way. The short-run deflationary forces come from the substantial underemployment of potentially productive labor and capital. I noted in January that, given the high unemployment rate at the time, a traditional Phillips Curve would predict deflation in the CPI over 2010-2011. Six months into the year, that's about how things have unfolded so far. The Bureau of Labor Statistics reported on Thursday that the seasonally adjusted consumer price index for May was at exactly the same value it had been in December.

Notes from the deflationary quicksand - Deflationary quicksand… We will all end up Japanese… Collapsing houses of cards… Yes, it’s another missive from SocGen’s perma-bear Albert Edwards, who on Thursday developed some recent riffs on deflation a tad further:…although our deflationary arguments are gaining some traction in the bond market, investors have yet to fully acknowledge we are now walking on the deflationary quicksand that will inevitably suck us towards total fiscal and financial ruin – you ain’t seen nothing yet. With core inflation rates now sub-1% in the eurozone and the US, we are only one recession away from Japanese-style deflation. Albert thinks recession will return by the end of the year, but that’s not the main issue. The real problem is that private-sector de-leveraging has barely begun, Edwards says, especially if you strip out the efforts made by financials — see chart (click to enlarge):

John Cochrane: How we get from here to inflation - University of Chicago’s John Cochrane has a new NBER paper out that is sure to generate some debate. He outlines the following scenario of how the U.S. could conceivably go from the current state of affairs to a situation of high inflation: Will we get inflation? The . Lower growth is the single most important negative influence on the Federal budget. Then, the government may have to make good on its many credit guarantees. A wave of sovereign (Greece), semi-sovreign (California) and private (pension funds, mortgages) bailouts may pave the way. A failure to resolve entitlement programs that everyone sees lead to unsustainable deficits will not help. When investors see that path coming, they will quite suddenly try to sell government debt and dollar-denominated debt. We will see a rise in interest rates, reflecting expected inflation and a higher risk premium for U.S. government debt. The higher risk premium will exacerbate the inflationary decline in demand for U.S. debt. A substantial inflation will follow — and likely a “stagflation” not inflation associated with a boom.

The solution to all problems -ADAM OZIMEK sends us to a new paper by John Cochrane, which aims to describe how events could conspire to produce a damaging inflation in America. In his focus on arriving at his inflation destination, I think he ends up burying the lede:Will we get inflation? The scenario leading to inflation starts with poor growth, possibly reinforced by to larger government distortions, higher tax rates, and policy uncertainty. Ok, stop right there. The scenario leading to inflation starts with poor growth. Forget about everything that comes next and focus on that most important factor. Because it happens that the scenario leading to a budget crisis also starts with poor growth, and the scenario leading to a long-term unemployment crisis starts with poor growth, and a scenario leading to a begger-thy-neighbour trade crisis starts with poor growth, and so on. So a very important question is: what can be done to improve the prospects for economic growth? In particular, what is the right countercyclical approach to take to best situate the economy for future growth?

Touch of Deflation Is Way to Price Stability: What’s so bad about a little deflation? As Federal Reserve policy makers gather today and tomorrow in Washington to take the economy’s pulse and assess their policy course, prices will be on their mind. Specifically falling prices. Not that deflation is a reality right now. The core consumer price index, which excludes food and energy, rose 0.9 percent year over year in both April and May, the smallest increase in 44 years. The Fed’s preferred inflation measure, the core personal consumption expenditures price index, rose 1.2 percent in the 12 months ended in April. What the U.S. economy is experiencing is disinflation, a slower rate of price appreciation, not deflation, or falling prices. A little bit of the latter wouldn’t be the worst thing. For starters, if the Fed wants to make good on its pledge of price stability, one of its dual mandates, it will have to do better than its 1.5 percent to 2 percent unofficial target.

Don't Fear Inflation, If It Comes - Economists agree that the deflation of 2008-9 – when prices fell in the economy – resulted from a “flight to quality,” a rather sudden reduction in demand for goods and increase in demand for dollars. They agree that, in principle, inflation will occur in the future if demand suddenly shifts in the opposite direction.Some economists say investors over the next several years will continue to demand dollars, so future deflation is the more likely danger. Other economists, including John Cochrane of the University of Chicago in this recent paper, say our government budget is on an unsustainable path, with lots of public spending promised and elected officials who lack the political will to raise taxes. So the real question is whether the economic damage from inflation is more or less than the economic damage of raising payroll taxes, implementing a national sales tax or paring some of the government’s spending promises. The answer is that inflation is less costly now than it usually is. Inflation would alleviate some damage done by the housing market to the wider economy.

New Treasury Bond Contract Bets on Deflation, Not Inflation - For the average investor, the Ultra US Treasury Bond futures contract is a relatively new way to get protection against deflation. But for at least one trader, it's another sign that a significant price drop is looming for the bond market. The Ultra contract gets futures traders true exposure to the 30-year Treasury bond. The original T-Bond contract included bonds with terms of 15 years or more.While volume remains comparatively low, investors have been turning to the Ultra increasingly as deflation, not inflation, has become a bigger worry for the economy. Inflation erodes the value of fixed-income instruments over time as interest rates rise and outpace the gain of appreciation in bonds and similar securities. Conversely, deflation rewards investors with the rates of return on fixed income that outpace interest rates.

FT Alphaville » Renminbi ruminations - As the FT reports, the Chinese central bank said in a statement on Saturday night that it would increase the flexibility of the exchange rate, effectively abandoning its currency peg with the US dollar via a policy of gradual appreciation of the renminbi against the greenback after nearly two years when the rate has remained unchanged.Lex notes that “a teenager ordered to tidy its room will often do the minimum necessary to get the oppressor off its back.” So it is with China’s announcement that its currency will trade more flexibly against the US dollar, “three days after the US president told it to”. The move, a week before the G20 convenes in Toronto, allows five days of modest gains for Beijing to demonstrate it is a “responsible, if reluctant, world citizen”.

China’s Renminbi Announcement: A Big Headfake - Yves Smith - The Chinese central bank made a vague announcement about its currency policy on its website today, which the officialdom, on cue, treated as a major move (to wit: “China vows increased currency flexibility” at the Financial Times, “Chinese say they intend to free up their currency,” Washington Post).) As we describe below, this “announcement” is basically a non-statement to silence Westerners calling for a revaluation in the runup to the Toronto G-20 meeting later this month. This is the full text of its English version:

China Moves. Or Not., by Tim Duy: Futures markets are abuzz with excitement over the Chinese currency proclamation issued this weekend. The announcement was quickly hailed by observers worldwide as a major policy shift, yet I am inclined to side with the analysis provided by Yves Smith - the statement leaves plenty of wiggle room, and never really promises to do much of anything. At the moment, the Chinese announcement feels like more smoke than fire. The Wall Street Journal's initial reporting was just want the Bejing and Washington wanted you to believe:China's decision to abandon its currency peg is a victory of pragmatism over divisive politics, the result of careful diplomacy by leaders in Beijing and in Washington, each side vulnerable to powerful domestic lobbies.In the end, both sides agreed that a more flexible exchange rate was good for China, good for the U.S. and good for the global economy. Yet timing was everything.The implication is that hard-working policymakers on both sides of the Pacific have risked all to foster the greater good. But what exactly has changed? From the Chinese statement: I see no commitments here, vague or otherwise.

China Turns Tables on AAA Debt Time-Bomb Nations - Your move, folks. That’s the message from China’s surprise move to allow a more flexible yuan. China, in signaling it’s okay with a rising currency, voiced a strong vote of confidence in its economic outlook. It also shifted the onus to the developed world in a crafty and unambiguous way. Timothy Geithner and his team at the U.S. Treasury should keep on ice the champagne they’re tempted to open. Now it’s time to start getting their own imbalances in order. The debt explosion of the past two years isn’t just unsustainable, it’s a growing threat to global stability. Chess games are won by those who can think and plan the farthest ahead. China, at least at the moment, appears to have a better sense of how the board is laid out. The question now is what Geithner and his partners in history’s greatest debt orgy do.

China to Put Renminbi in a Currency Basket – Things heated up in the currencies this weekend… Yes, while everyone was wiping the milk from their mouths from their cereal they ate for breakfast on Saturday morning, the Chinese made a BIG announcement… Here is the official statement from the People’s Bank of China (PBOC)… “In view of the recent economic situation and financial market developments at home and abroad, and the balance of payments (BOP) situation in China, the People’s Bank of China has decided to proceed further with reform of the RMB exchange rate regime and to enhance the RMB exchange rate flexibility.” (They say RMB for renminbi.)The PBOC also said that the “new currency regime” would be to value the renminbi versus a basket of currencies (that’s how they did it 2005-2008), but this time they mentioned that they would allow the markets some say in the movement of the currency. Now… Please pay attention to what I’m about to say… There are a lot of people that believe that this will mean a HUGE one-way street for renminbi versus the dollar… I’m not one of those! While I think at the moment renminbi should move higher versus the dollar, there’s no “guarantee” that it will always move higher versus the dollar! The renminbi is now “flexible”!

Yuan appreciation not guaranteed – China's announcement that it will allow increased currency flexibility is far from a game-changing move and may actually backfire, some economists said on Monday. While the People's Bank of China's (PBOC) statement over the weekend was labeled "cryptic" by some, a Q&A posted later on the central bank's website showed that it is trying to scale bank expectations of an imminent appreciation in the yuan. Instead, China appeared to suggest that it wants to increase two-way risk given the recent appreciation against the euro. Some analysts say the yuan could actually fall, especially against the euro, which would increase China’s trade advantage on that continent.

Why China's Currency Announcement is Hokum - China isn’t really changing anything. It’s only doing the minimum to prevent Congress from listing China as a currency manipulator, leading to a squeeze on Chinese imports. Over time – and I’m talking about months if not years – China will raise its currency to where it was before the global meltdown in 2008. Big deal. Even then, a stronger yuan won’t generate lots of new jobs in the United States That’s because most of the gains of China’s meteoric growth are still not finding their way into the hands of Chinese consumers, whose spending is growing far more slowly than China’s overall economy. In 2009, total personal consumption in China amounted to only 35 percent of the economy; ten years ago it was almost 50 percent

Two Opposing Opinions On The Yuan Depegging - Yesterday's mega news on the CNY depegging, which went so far as to make headlines out of something as mundane as the PBoC yuan fixing, has now been fully priced in. And before we put the matter to rest, we would like to present two diametrically opposing opinions on this issue: one from Goldman's Sven Jari Stehn, which is full of contained optimism about the future of the world, and one from Gary Shilling, who in a Bberg TV interview, says that the Chinese decision could not have come at a worse time, and that it risks destabilizing the precarious global balance achieved at the cost of so many trillions in stimuli.

More Fire From Washington on China's Economic Policies - Facing continued lackluster economic conditions at home, some American politicians are pointing the finger abroad. Days after China announced that it would allow its currency to float more freely, raising expectations that American-made goods could compete against higher-priced Chinese goods, several House Democrats and a Republican said today that they did not think the measure went far enough. Standing behind a placard emblazoned with the phrase “China Cheats,” Representative Tim Murphy, Republican of Pennsylvania, said that Congress would not tolerate China’s “unfair trade practices, currency manipulation, and deadly products,” and that a bill he introduced last year, the Currency Reform for Fair Trade Act of 2009, would end China’s currency devaluation by requiring penalties on underpriced goods.

The Renminbi Runaround - Krugman - Last weekend China announced a change in its currency policy, a move clearly intended to head off pressure from the United States and other countries at this weekend’s G-20 summit meeting. Unfortunately, the new policy doesn’t address the real issue, which is that China has been promoting its exports at the rest of the world’s expense. n fact, far from representing a step in the right direction, the Chinese announcement was an exercise in bad faith — an attempt to exploit U.S. restraint. To keep the rhetorical temperature down, the Obama administration has used diplomatic language in its efforts to persuade the Chinese government to end its bad behavior. Now the Chinese have responded by seizing on the form of American language to avoid dealing with the substance of American complaints. In short, they’re playing games. To understand what’s going on, we need to get back to the basics of the situation.

More on China’s Renminbi Headfake -Yves Smith - It was hard to miss the Chinese central bank’s announcement last weekend that it was implementing a ore “flexible” policy toward managing its currency. Numerous Western officials and analysts declared the statement to be a major move, signaling China’s willingness to allow the renminbi to appreciate to a meaningful degree. We, by contrast, called it a a non-statement to silence Westerners calling for a revaluation in the runup to the Toronto G-20 meeting later this month: China has committed to do…..absolutely nothing. In fact, this language could just as easily be used to justify shifting its dirty float to be against the dollar to putting greater weight upon the euro in its basket, which would lead to a devaluation against the dollar.China allowed the renminbi to appreciate a grand total of 0.39% against the dollar this week. leading commentators to rethink China’s canny ploy. Today, the Financial Times gives a reassessment. It notes in particular that domestic interests are fiercely opposed to a rise of a mere 2-3% against the dollar, much the less the 20% to 40% that most experts deem necessary to achieve fair value. In addition, it stresses the possibility we mentioned in February: that China could devalue the renminbi.

Yuan-way bet - SO, TWO days on, what have we learned about China's new currency strategy? There is a general tendency toward scepticism among the economics commentariat. Take, for instance, this Tim Duy post, in which the author makes much of this story: China’s yuan declined the most since December 2008 on speculation the central bank will encourage more two-way fluctuations in the exchange rate after it pledged to expand flexibility... but of course the currency has been pegged to the dollar over that period. And meanwhile, renminbi were still dearer today than they were on Friday. But it's also important to understand what the Chinese are doing. Here's economist David Li talking to HSBC: The PBoC announcement unpegging the renminbi from the US dollar seems to be a return to an earlier system (July 2005–July 2008). This time round, the renminbi will likely gradually appreciate against major currencies; however, the process may not be as smooth as it was before.

Number of the Week: Yuan Revalue Is No Panacea for U.S - 13%: Growth in the U.S.-China trade deficit* since 2005, the last time China loosened its exchange-rate peg. As leaders of the Group of 20 developed and developing nations meet in Toronto this weekend, one big question on the agenda is how to deal with the global imbalances reflected in the vast U.S. trade deficit — and in China’s similarly vast trade surplus. The concern: If the U.S. keeps borrowing money to buy goods from China and other exporters, it will eventually build up enough debt to undermine confidence in the dollar.

Global Markets Fear U.S. Treasuries Sell-Off As China Ends Currency Freeze - Global markets are braced for a possible sell-off in US Treasury bonds after China said over the weekend that it will allow the yuan exchange rate to adjust against the dollar, ending a two-year currency freeze that has led to trade clashes with Washington and Brussels. China's Central Bank said the economic recovery had opened the way for a return to "flexibility" but ruled out an immediate one-off rise in the yuan. The currency will be allowed to fluctuate within a widened band of 0.5pc each day against a basket of currencies. The yuan is now expected to rise slowly against the dollar, although it may fall if the euro weakens further. "There is at present no basis for major fluctuation or change in the exchange rate," said the bank

How Dangerous Is U.S. Government Debt? - The dollar’s status as the world’s reserve currency has become a facet of U.S. power, allowing the United States to borrow effortlessly and sustain an assertive foreign policy. But the capital inflows associated with the dollar’s reserve-currency status have created a vulnerability, too, opening the door to a foreign sell-off of U.S. securities that could drive up U.S. interest rates. In this Center for Geoeconomic Studies Capital Flows Quarterly, Francis E. Warnock argues that a sell-off came close to happening in 2009. How the United States uses this reprieve will affect the nation’s ability to borrow for years to come, with broad implications for the sustainability of an active U.S. foreign policy. DOWNLOAD THE FULL TEXT OF THE QUARTERLY REPORT HERE (636K PDF)

Yuan can become alternative reserve currency to US dollar-ADB (Reuters) - China's yuan could rapidly become an internationally used currency and serve as an alternative to the U.S. dollar in central bank reserves, the Asian Development Bank said in a report on Thursday. "The renminbi has yet to become an international currency. It could become one much more quickly than many anticipate," the ADB said in a joint study with Columbia University's the Earth Institute. "The internationalization of the renminbi has the potential to become an alternative to the U.S. dollar -- as did the euro -- and help nudge the global reserve system toward a multi-currency reserve structure," it said. The study, undertaken by 11 economists from around the world, including academics Joseph Stiglitz and Barry Eichengren, did not provide a timeline for when the yuan could become a reserve currency. Most analysts expect it to be fully convertible by 2020, the target date set by Beijing to make Shanghai an international financial centre.

Suiting Up for a Post-Dollar World - The global financial crisis is playing out like a slow-moving, highly predicable stage play. In the current scene, Western governments are caught between the demands of entitled welfare beneficiaries and the anxiety of bondholders who fear they will be stuck with the bill. As the crisis reaches an apex, prime ministers and presidents are forced into a Sophie's choice between social unrest and bankruptcy. But with the "Club Med" economies set to fall like dominoes, the US Treasury market is not yet acting the role we would have anticipated. Our argument has always been that the US benefits from its reserve-currency status, allowing it to accumulate unsustainable debts for an unusually long period without the immediate repercussions of inflation or higher borrowing costs. But this false sense of security may be setting us up for a truly monumental crash.

China Backs Obama With Debt Holdings to $900 Billion (Bloomberg) -- A year after criticizing U.S. fiscal policy as “irresponsible,” China’s leaders are showing increasing confidence in President Barack Obama’s leadership of the American economy. China boosted holdings of Treasury notes and bonds by 2.6 percent to $900.2 billion in March and April, after reducing its stake by 6.5 percent from November through February, the longest consecutive monthly declines in a decade, U.S. data released June 15 showed. The People’s Bank of China said June 19 that it will relax its 23-month lock on the yuan. Congressional leaders say the new foreign-exchange policy doesn’t go far enough to keep them from seeking laws to punish China for what they say are unfair trade practices. Regardless of the currency rate, China will continue to be a net buyer of U.S. debt, “It’s just bad economics to pretend we can fix the lives of middle class American workers by getting the Chinese to revalue its currency vis-a-vis the dollar -- it’s a horrible misconception,” Stephen Roach, chairman of Morgan Stanley Asia Ltd. said

Understanding The Global Risk Carry Trade - Given that the worlds central banks answer to global speculators and their money center bank/investment bank sponsors, the people of each country must stand up for a public policy that benefits them. Central bankers have many complex tools in which to exercise their “stability” agenda. While things like currency swap facilities sound harmless when explained as short term in nature, the ability of a central bank to reinstate them at will is a perpetual back stop to global risk asset speculators. When we are asked to fund the IMF in the name of global economic stability, we are really just allowing the sovereign risk hot potato to be passed up the credit ladder in a hidden backstop of foreign folly. The unwinding of the global risk asset carry trade is the ultimate end game for decades of Keynesian lunacy. A credit bubble cannot be cured by more credit. We must recognize the widely accepted fallacies we have lived by, and devise an exit strategy that is fair to all.

America's Ticking Debt Bomb: Like Greece, "Only Worse," Pento Says - America's debt bomb is ticking and is likely to detonate in five years or less, says Michael Pento, senior market strategist at Delta Global Advisors. "It could be much sooner when we hit the debt wall," Pento says. "My opinion doesn't matter: Math tells me we're in a serious problem." The math Pento refers to is the Treasury Department's recent estimate that total U.S. debt will top $13.6 trillion this year and rise to 102% of GDP by 2015. Moreover, the publicly traded debt (debt excluding intra-governmental obligations) will rise to $14 trillion by 2015, up from "just" $7.5 trillion in 2009. At $14 trillion, the interest payments on the public debt will total about $1 trillion in 2015, he continues; even assuming solid growth and low inflation, that would equal about 30% of total government revenue. "What do you think that does to our bond market?," Pento wonders. "It leads to a dollar crisis and a bond market crisis. That's why gold refuses to go down. "

Alan Greenspan v. Paul Krugman - Paul Krugman and Alan Greenspan came out with dueling op-eds Friday about budget deficits gone wild. Krugman: we're slitting our wrists by trying to slash our deficits now. Greenspan: cut spending now, right now, and don't worry your pretty little head about a double-dip recession. Neither was convincing, and there's a reason: the fiscal debate has become so polarized that combatants on both sides are glossing over what they don't know. I would argue that we ought to be doing the opposite: the unknowables right now are huge, and we ought to talk about them. Put another way: we need insurance. Against our next mistake.

In the hot tub time machine with Alan Greenspan: The "Maestro" tells Americans we can't afford our future. Ten years ago, he sang a different tune - The federal government of the United States better get its finances in order, warns Alan Greenspan in the Wall Street Journal today, or we're going to be in big, big trouble!If I were seeing a therapist, I'm sure she would warn me that my recent habit of reading opinion pieces in the Journal and then collapsing into a fit of apoplectic befuddlement is not good for either my long-term health or sanity. Calmer minds might wonder why we should bother paying any attention to the "Maestro" -- a man whose deepest convictions about the infallibility of self-correcting markets have been proven so profoundly wrong. But after Calculated Risk reminded me of a speech Greenspan gave to Congress in 2001, a speech that just gets better and better with each rereading in the years since, I simply could not resist. Please bear with me.

My Father and Alan Greenspan - Robert Reich -When I was a small boy my father gave me my first economics lesson. “Bobby,” he said with obvious concern, “you and your children and your children’s children will be repaying the national debt created by Franklin D. Roosevelt.” I didn’t know what a national debt was, but I remember being scared out of my wits. Dad, now 96 and still in good health, recognizes how wrong he was then. He admits FDR’s deficit spending not only won World War II but it also got America out of the Great Depression. But now another gaggle of deficit hawks is warning us against more federal spending. “The current federal debt explosion is being driven by an inability to stem new spending initiatives,” warns Alan Greenspan in Friday’s Wall Street Journal, calling for budget cuts and saying “the fears of budget contraction inducing a renewed decline of economic activity are misplaced.” My dad learned from his mistakes. Alan Greenspan obviously didn’t.

The facts have a well-known Keynesian bias (Paul Krugman) There are many things to say about Alan Greenspan’s op-ed yesterday, none of them complimentary. But what struck me is the passage highlighted by Tim Fernholz: Despite the surge in federal debt to the public during the past 18 months—to $8.6 trillion from $5.5 trillion—inflation and long-term interest rates, the typical symptoms of fiscal excess, have remained remarkably subdued. This is regrettable, because it is fostering a sense of complacency that can have dire consequences. You know, some people might take the fact that what’s actually happening is exactly what people like me were saying would happen — namely, that deficits in the face of a liquidity trap don’t drive up interest rates and don’t cause inflation — lends credence to the Keynesian view. But no: Greenspan KNOWS that deficits do these terrible things, and finds it “regrettable” that they aren’t actually happening.

Contemptible Advocates of Debt Default - Historian Jeffrey Rogers Hummel accuses me of being “awfully contemptuous of those opposed to increasing the federal debt limit.” He is right. I am contemptuous of those who know so little about the federal budget that they actually believe the debt limit is an effective tool for controlling growth of the federal debt. I went into detail on this subject some years ago in testimony before the Senate Finance Committee, where I explained the history of the debt limit and why it is totally ineffective at controlling growth of the debt. The curious can find it among the committee’s printed hearings. The date was February 14, 2002. On that occasion I proposed abolition of the debt limit to deafening silence from the committee, but nodding agreement from the Treasury secretary. One doesn’t really need to read my testimony, however, because it is perfectly obvious from the most casual examination of the record that the debt limit has never exercised any constraint on spending or borrowing.

Response from Brad DeLong on fiscal policy -Read the whole thing; my original post was here. On my point 1, that the central bank moves last, Brad writes: Yes, the central bank can neutralize any additional fiscal stimulus by raising interest rates. (It is not clear that it can undo any fiscal contraction by some combination of lowering interest rates and quantitative easing: it may be able to.) What is clear is that the U.S. Federal Reserve and the Bank of England are right now definitely not in a place where they would neutralize any additional fiscal stimulus by raising interest rates. And my bet is that the ECB is also not in such a place--although it is much harder to figure out what they think and what they will do.. Maybe the central bank cannot undo a fiscal tightening, but surely it can undo a fiscal expansion, by making money tighter, limiting QE, and/or changing the pace at which it undoes previous QE. My assumption is that the central bank has a preferred inflation vs. unemployment position for the economy, so why be so sure they won't undo the expansion of the fiscal authority, if only probabilistically?

Why and when to spend - TYLER COWEN has been challenging those looking for bigger short-term deficit spending to defend their arguments, and this has led to an interesting debate between him and Brad DeLong. The back-and-forth has actually come around to re-arguing the value of countercyclical fiscal policy. A couple of specific points of quasi-disagreement appear to emerge from this exchange.First, does the zero bound mean anything? (Mr Cowen calls the zero bound problem "the single largest 'red herring' in the economics profession today".) In fact, the zero bound does not bind, in most cases anyway. Fiscal stimulus supporters might respond that while the zero bound does not bind, the Fed might nonetheless be reluctant to engage in the appropriate amount of monetary expansion, and that a fiscal boost is therefore required. A potential response to this is that if the Fed has chosen the unemployment rate with which it is satisfied, it will simply offset any fiscal measures to push unemployment below that level. And that is a sticky problem. On the other hand, the classic helicopter drop of money approach involves a money-financed tax cut. That's monetary policy as fiscal policy, so in a way, Mr Cowen is accepting that fiscal boosts may be necessary at some point. Is that point the zero bound?

Super-Asinine Propensities - - As Economix notes, Mark Thoma has coined the term "austerians" for those who are calling for budget cutting in the face of continued high unemployment. That's pretty good, but I think Keynes said it even better, as his biographer Robert Skidelsky writes in the FT: He explained to an American correspondent that “every person in this country of super-asinine propensities, everyone who hates social progress and loves deflation, feels that his hour has come and triumphantly announces how, by refraining from every form of economic activity, we can all become prosperous again.” Speaking of Alan Greenspan... Paul Krugman, Andrew Leonard and Calculated Risk respond to his super-asinine WSJ op-ed. See also Andrew Leonard on Skidelsky's piece.

The Unavoidability of Long-Term Austerity - Edmund Andrews surveys the fiscal policy debate and says “If I were king, the plan would allow for another round of stimulus spending but call for real belt-tightening around 2015.” Sure, me too. But one thing that I really think needs to be emphasizes is that the need for medium-term belt-tightening has nothing to do with the argument over short-term stimulus.By which I mean, whether we make the short-term deficit smaller or larger we still need to tackle a serious longer term problem. And we would still need to tackle that problem even if the recession hadn’t happened. It’s a real problem. And a big one. But the shape of the problem is very simple and it looks like this:

- The public sector has assumed responsibility for financing the health care of old people.

- The cost of health care relative to the rest of the economy is rising.

- The proportion of old people relative to the rest of the population is rising

Now and Later, by Paul Krugman - Spend now, while the economy remains depressed; save later, once it has recovered. How hard is that to understand? Very hard, if the current state of political debate is any indication. All around the world, politicians seem determined to do the reverse. They’re eager to shortchange the economy when it needs help, even as they balk at dealing with long-run budget problems. But maybe a clear explanation of the issues can change some minds. So let’s talk about the long and the short of budget deficits. ... America has a long-run budget problem. Dealing with this problem will require, first and foremost, a real effort to bring health costs under control — without that, nothing will work. It will also require finding additional revenues and/or spending cuts. As an economic matter, this shouldn’t be hard..., a modest value-added tax, say at a 5 percent rate, would go a long way toward closing the gap, while leaving overall U.S. taxes among the lowest in the advanced world. But if we need to raise taxes and cut spending eventually, shouldn’t we start now? No, we shouldn’t.

Deficits are our saving - Even the most simple understandings are lost in the public debate about budget deficits and public debt. The Flat Earth Theorists who whip up deficit hysteria each day like to stun people with large numbers. They produce debt clocks that relentlessly tick over and try to get us to believe that impending doom is upon us. But if we just take a deep breath and think the situation through we would see that the ticking debt clock is really just a measure of the portion of non-government wealth embodied in public debt. We would then learn that budget deficits are just the mirror image of non-government savings. Saving is usually considered to be something we should aim for. Increased wealth is also something we usually aspire to. So the increasing deficits and increased debt outstanding is, in fact, beneficial to the private sector (overall). Once we understand that then the deficit hysteria becomes transparently ideological. These characters just hate government and want to get their greedy hands on more of the real pie.

Steny Hoyer and the Deficit: “We’re Lying to Ourselves and Our Children” - Speaking to The Third Way, a middle-of-the-road Democratic think-tank, Hoyer called for a bipartisan effort to balance the need for short-run economic recovery with long-term deficit reduction. Not much new there. Lots of pols have delivered a similar message in recent months. But what made Hoyer’s talk matter is that he named names. It is easy to say, “everything is on the table.’ It is not so easy for an elected official to explicitly describe what that means. Hoyer did. And his remarks won’t make him any friends within the Democratic base. Among his proposals: Trim future Medicare costs. Raise the Social Security retirement age. Adjust both programs to focus benefits on those who need them most, even if it means reducing benefits for wealthy retirees. Cut defense spending. Have a “serious discussion” about whether to permanently extend the Bush tax cuts for those making less than $250,000 as President Obama wants. Enforce budget rules that require Congress to pay for new spending and tax cuts.

The Deficit and the Damage to Come - "Our nation's fiscal position has deteriorated appreciably since the onset of the financial crisis and the recession," Bernanke said in his comments on fiscal sustainability. "Unless we as a nation make a strong commitment to fiscal responsibility, in the longer run, we will have neither financial stability nor healthy economic growth."In contrast with Mr. Bernanke's admonishing of the federal government, signs of easing in the purse strings of private market participants are generally well received in policy circles. When businesses and consumers curtail investment and spending in the early stages of a recovery, it may reflect a decline in confidence that augurs poorly for the economic outlook. More restrained spending by consumers, as conveyed in last week's retail spending report, has been interpreted through this particular lens, casting a further pall over already-shaky markets

Do Deficit and Inflation Hawks Know Best? - This is a good example of what's going on with economic policy right now. Marty Feldstein thinks that people ought to be worried about inflation and budget deficits, and the fact that he can't find evidence of this worry puzzles him: while inflation is very likely to remain low for the next few years, I am puzzled that bond prices show that investors apparently expect inflation to remain low for ten years and beyond, and that they also do not require higher interest rates as compensation for the risk that the fiscal deficit will cause real interest rates to rise in the future. Instead of questioning his own assumptions in light of evidence that they are incorrect, he suggests implicitly that investors collectively -- i.e. the vaunted market with its ability to incorporate all relevant information into prices -- is wrong. When do we abandon what markets are actually telling us and instead react to what we -- the less capable humans -- think markets ought to be telling us?

FT Reveals Orszag Resigns Over Inability To Persuade Summers And Obama Keynesianism Leads To Suffering - As we speculated previously, the sudden and unprecedented departure of Peter Orszag, the day prior to the US Budget's formalization (which incidentally never happened as now the US will likely not have a 2010 budget at all, for fear of disclosing to most Americans just how broke the country is ahead of mid-terms) was due to Orszag's disagreement with the administration's, and particularly Larry Summer's, inability to fathom that reckless spending is a recipe for bankruptcy. As the FT reports: "Peter Orszag, Barack Obama’s budget director, resigned this week partly in frustration over his lack of success in persuading the Obama administration to tackle the fiscal deficit more aggressively, according to sources inside and outside the White House." And so, as any remaining voices of reason realize they are dealing with a group of deranged Keynesians, soon there will be nobody left in the administration who dares to oppose the destructive course upon which this country has so resolutely embarked, which ends in one of two ways: debt repudiation, or war. .

Against The Super-Asinine, The Gods Themselves Contend in Vain - Brad DeLong wonders how the proponents of tight budgets and tight money are prevailing in the midst of mass unemployment, low interest rates, and incipient deflation. The natural instinct of almost everyone is to think that tough times require tough measures, and that if the economy is suffering, the government should tighten its own belt. It would take a clear consensus from economists to overcome that natural bias. And that consensus has, of course, been lacking — largely because a significant proportion of the economics profession has spent the last three decades systematically destroying the hard-won knowledge of macroeconomics. It’s truly a new Dark Age, in which famous professors are reinventing errors refuted 70 years ago, and calling them insights. On top of that, anti-stimulus appeals to a fundamental meanness of spirit that is always present in the political world. The super-asinine we shall always have with us.

The Case Against Stimulus - Steve Randy Waldmann has a very good post up noting some problems with discretionary fiscal stimulus. I recommend it to one and all because I think that reading the detailed case for skepticism about stimulus as a general matter only drives home how strong the case for stimulus in the current actual situation is. This all actually reminds me of a story from my youth in the distant land of the USA. Once upon a time an asset bubble burst, but there was little leverage involved and the ensuing downturn was relatively mild. The federal reserve had room to run in terms of cutting interest rates, and the previous ten years’ worth of fiscal policy had seen a series of measures, some bipartisan (1990 & 1997) and some partisan (1993) to improve the country’s budget situation. But the newly inaugurated young president argued that the country needed to enact a large discretionary fiscal stimulus program to combat the downturn, even thought his would shatter the fragile consensus that had guided improvements in the fiscal posture. Oddly, this stimulus program would be phased in and out over a ten-year time horizon. Even odder, the nominally temporary nature of the stimulus was clearly a fraud—everybody understood that the key authors of the stimulus in fact intended the policy change to be permanent in nature. I refer, of course, to the Economic Growth Tax Relief Reconciliation Act of 2001, a.k.a. “the Bush tax cuts,” which IIRC were roundly applauded by most of the right-of-center economists who can today be found assuming a debt-averse and stimulus-skeptical posture.

Has stimulus become a dirty word? – Disastrous home-sale figures and persistently high unemployment make it clear the U.S. economy is still struggling. What’s not so apparent is what new efforts Barack Obama, the U.S. President, might seek to tackle the problem. While he urges America’s allies not to sacrifice economic growth to pay down ballooning deficits at this weekend’s Group of 20 industrial and developing nations summit in Toronto, Mr. Obama is coming under stiff resistance back home against turning any sort of stimulus taps back on.“He’s very skilled and articulate, but he really lost control of the debate on stimulus,” “Polls show most Americans think the stimulus package didn’t create jobs, [although] most economists think it did. The word stimulus has become a dirty word.”

The Instinct for Austerity is Working Against Us – Thoma - A couple of days ago, Room for Debate at the NY Times asked about the need for further stimulus, and part of my response said the following (It hasn't run yet since they decided to cover McChrystal first):But the most important change that is needed is in the attitude of the public and politicians toward using deficit spending to stabilize the economy. Even though it’s the correct response, deficit spending goes against our instincts. When times are tough, our natural response is to cut back on consumption. We may dip into savings or borrow money to prevent too large a fall in consumption, but our overall consumption falls. To see government not only failing to reduce its spending as its income (tax revenue) falls, but actually increasing spending by a large magnitude, cutting taxes, and financing it by taking on debt, and then saying even more is needed runs counter to those instincts. And starting with a budget that is already in the red doesn't help at all.

A Moment of Truth - For lower-income people, unemployment numbers rival those of the Great Depression. And the average unemployed person has now been searching for work for over eight months—the highest average on record. Despite such widespread hardship, the Senate has failed to extend unemployment benefits. As a result, as many as 1.2 million workers will be cut off of unemployment benefits by the end of this week, and at least 140,000 workers will lose healthcare benefits. The Senate and House also failed to approve $24 billion in promised federal assistance to state Medicaid programs—even as states face $260 billion in budget shortfalls over the next two years. The Center on Budget and Policy Priorities estimates that without federal help state cuts could result in the loss of 900,000 jobs. If we fail to understand the need to invest in people and our future—now and in the months, perhaps years, ahead—the already weak recovery will unravel. But with deficit hawks in both parties dominating the debate in Congress, abetted by a lazy media drumbeat, the chances that this country will become a stronger and healthier one don’t look very good.

Is Paul Krugman depressed? - I get the feeling that Paul Krugman is getting gloomier and gloomier. Professor Krugman is a Nobel Prize-winning economist, columnist and blogger. Since December he has been warning about the possibility of a double-dip recession. Now, his latest column suggests that he is looking at something worse. In fact, he used the ‘D’ word–depressed that is–four times: Spend now, while the economy remains depressed; save later, once it has recovered. How hard is that to understand? …Even if the government’s annual borrowing were to stabilize at 4 percent of G.D.P., its total debt would continue to grow faster than its revenues. Furthermore, the budget office predicts that after bottoming out in 2014, the deficit will start rising again, largely because of rising health care costs.Professor Krugman is acknowledging that we will have trillion dollar budget deficits as far as the eye can see. He can see that the day of reckoning is coming, but he is hoping that it will not come soon.

In The Long Run, We Are Still All Dead - Krugman - So, reading Mohamed El-Erian, I’m somewhat at a loss about what he’s actually saying; what, exactly, is the policy recommendation? But in any case, here’s what struck me: he writes, The world is facing deep structural challenges yet its leaders are stuck in a short-term, cyclical mindset. I disagree. If anything, we’re suffering from the opposite problem. Talk to German officials about high unemployment and the looming threat of deflation, and they ramble on about the demographic challenge and the cost of pensions. I mean, why shouldn’t we be focused on the business cycle? We’ve suffered the worst cyclical downturn since the Great Depression; in terms of unemployment and output gaps, we have recovered almost none of the lost ground. Millions of willing workers are idle because of lack of demand; let them stay idle, and we can turn this into a long-term structural problem, but right now it is precisely a short-term, cyclical problem. So saying that we need to focus on the long term, and not worry our little heads about trivial short-term issues like the highest long-term unemployment rate since the Great Depression, may sound like wisdom — but it’s actually folly.

Budget Hawk, Stimulus Dove - It's not my position. But I would think someone would articulate it. It sounds like what Mark Thoma would advocate, for example. That is, someone could advocate: 1 A larger deficit in the short term. 2. Specific, clear measures to reduce deficits over the next ten years, by trimming entitlements and raising taxes. 3. Linking (1) and (2) in a single piece of legislation.This sort of approach might satisfy doves who complain about austerity as well as Europeans and domestic hawks who worry about the U.S. fiscal outlook, . If (2) included some serious structural changes in entitlements I might endorse it.But my point is not whether this compromise is something I could get excited about. My point is that it represents a missing position in the media. Why are the hawks and doves more interested in trying to score debating points against one another than in achieving their objectives?

Resource Hawk, Stimulus Dove -I suggested as much via last summer’s post Means of deficit reduction: Medicare and Social Security. I am a lot more interested in reducing Medicare costs than in cutting Social Security – and this could be done by reducing health care costs overall rather than on Medicare alone. Clearly, if we could get cost growth in healthcare paid by private insurance, it would impact Medicare costs down. Of course, I prefer lower spending and lower taxes to lower spending and higher taxes. And I don’t have a lot of faith in stimulus these days unless it is related to jobs because special interests have a way of getting their hands into the pot and perpetuating malinvestment. But, remember deficits are an ex-post accounting identity. If you think of economic policy as a largely exogenous short-term variable, but perhaps a more endogenous variable in the long-term, then it makes sense to move away from the deficit talk (see my post Out of control US deficit spending for more detail). The real driver of policy has to be a conversation about the allocation of society’s scarce resources.

What caused the Budget Deficit (Before the Financial Crisis)? - Kash on Angry Bear put together a really good graph in 2006 comparing where we might have been if Clinton policies (bad as they were in many cases) had stayed in place compared to where we were and expected to be with the Bush tax cut and spend policies. Responsibility for the Federal Budget Deficit, Angry Bear 2006. Deficits under Bush were projected for more than $500 billion annually. Of course, that was before the greedy, reckless banks threw the financial system into a tizzy with too much credit invested in too many houses by people with too little income to pay for them. Add the costs of backstopping the Big Banks, and we end up with the trillion dollar hole we are currently in. Answer would seem to be--1) make the banks pay with a tax based on leverage and 2) end the tax cuts or at least a goodly share of them and 3) reinstate an estate tax that has some bite, so that those at the top who can afford to pay do pay.

You've seen the stimulus. Now meet the anti-stimulus - A multiple choice question for you: Did the stimulus a) work; b) fail; c) end up locked in an unexpected battle with the massive anti-stimulus that's ripped through the states? Most people haven't heard of "c." But ask Bruce Bartlett, a conservative economist who worked for Ronald Reagan, George H.W. Bush and Jack Kemp, and you'll hear all about it. "When the history of the current crisis is written, much of the blame will be placed on the sharp fiscal contraction of state and local governments," he says. "I think economists will view this as a preventable error equivalent to the Fed's passive shrinkage of the money supply in the early 1930s." Take my home state of California, with an unemployment rate of more than 12 percent. We need the government to help create jobs, and quick. But instead, Sacramento is raising taxes and cutting services. That's like bailing water into the boat rather than out.

“Emergency” does not mean “important” - Emergency spending is advantaged in the Congressional budget process: The total amount of discretionary spending, implemented through annual appropriations bills, is capped by the annual budget resolution. Discretionary spending designated as emergency spending does not count toward these caps. Mandatory spending, most of which is for entitlement programs, is on autopilot. Congressional budget rules require you to offset any legislative increase you propose in mandatory spending. An emergency designation waives this requirement. The same is true for tax cuts designated as emergencies. OK, now that we know how emergency spending is advantaged, what is it? It turns out there is no formally binding definition in the legislative process, so as a formal matter, it’s whatever you can get away with labeling as an emergency. A Member of Congress can argue that X is not an “emergency,” and if he or she can get the votes to strike that emergency designation from the bill, then that spending will count toward the caps (discretionary) or its deficit effect must be offset (mandatory). If, however, a majority of Members (separately in the House and Senate) agree that they’ll label X as an emergency, then there is no procedural challenge available.

House Democrats Announce No Budget Will Be Passed In 2010 -House Democrats will not pass a budget blueprint in 2010, Majority Leader Steny Hoyer (D-Md.) will confirm in a speech on Tuesday. But Hoyer will vow to crack down on government spending, saying Democrats will enforce spending limits that are lower than what President Barack Obama has called for. In the scheduled address to the progressive think tank The Third Way, Hoyer will acknowledge that the lower chamber will do things differently this election year. “It isn’t possible to debate and pass a realistic, long-term budget until we’ve considered the bipartisan commission’s deficit-reduction plan, which is expected in December,” according to Hoyer’s prepared remarks that were provided to The Hill.