Fed Balance Sheet Grows To $2.92 Trillion In Latest Week - The Fed's asset holdings in the week ended Jan. 18 climbed to $2.922 trillion, from $2.902 trillion a week earlier, it said in a weekly report released Thursday. The Fed's holdings of U.S. Treasury securities climbed slightly to $1.652 trillion on Wednesday from $1.651 trillion. The central bank's holdings of mortgage-backed securities increased to $847.43 billion from $840.27 billion. The report Thursday showed holdings of Treasury securities with a remaining maturity exceeding five years rose over the past week, while the amount of shorter-term maturities declined. Meanwhile, Thursday's report showed total borrowing from the Fed's discount lending window was $8.60 billion Wednesday, down from $8.63 billion a week earlier. Commercial banks borrowed $2 million from the discount window, down from $8 million a week earlier. U.S. government securities held in custody on behalf of foreign official accounts (table 1a) was $3.403 trillion, up from $3.390 trillion in the previous week. U.S. Treasurys held in custody on behalf of foreign official accounts climbed to $2.677 trillion from $2.663 trillion in the previous week. Holdings of agency securities fell to $726.56 billion from the prior week's $ 726.83 billion.

FRB: H.4.1 Release--Factors Affecting Reserve Balances--January 19, 2012

Fed to Weigh Further Easing Amid Doubts About Recovery - Federal Reserve officials are seriously considering giving the US economy—and especially the housing market—an added jolt with more quantitative easing. Fed officials are likely to discuss such a move at their Jan. 24-25 meeting, when the central bank will issue its first quarterly forecast on interest rates under the new communication policy. Two of the new voting members this year on the Federal Open Market Committee , which sets interest-rate policy, have recently suggested they would support more assets purchases. San Francisco Fed President John Williams said that sustained high levels of unemployment, as forecast by many Fed members, "does make an argument that we should have more stimulus." Another new voter, Cleveland Fed President Sandra Pianalto, said in a recent speech that economic models indicate the Fed "should be even more accommodative than it is today." They join other members, including New York Fed President Bill Dudley and several Fed governors, who have openly suggested they would support more QE . As part of an normal rotation of presidents, the makeup of the FOMC will become more dovish this year. Three hawkish members are losing their FOMC vote—Richard Fisher of Dallas, Narayana Kocherlakota of Minneapolis and Charles Plosser of Philadelphia—along with only one dovish member, Charles Evans of Chicago.

Fed Statements Make More Treasury Purchases Less Likely - St. Louis Federal Reserve Bank President James Bullard and Richmond Fed President Jeffrey Lacker are two Federal Reserve Bank officials that have said the Fed should halt (temporarily at least) purchases of U.S. Treasury securities because of a strengthening economy. This is in contrast to comments last week from other Fed officials, including Chicago Fed President Charles Evans and New York Fed President William Dudley, who called for continued liquidity support of the economy with the bond purchase process commonly referred to as quantitative easing (QE). According to an article by Mark Felsenthal (Reuters) the pronouncements by Bullard, who is considered a policy centrist, and the hawkish Lacker make it more likely that the Fed will put more bond purchases on hold.

Fed's Latest Easing Could Cost $1 Trillion: Economists - The Federal Reserve is likely to step in with $1 trillion worth of easing that could be announced as soon as this month, according to a growing consensus of economists who see the recent uptick in economic growth as unsustainable. With the Fed’s Open Market Committee set to meet next week, expectations are rising that the languishing housing market will drive the central bank to buy up mortgage-backed securities. The goal of the purchases will be to drive down interest rates even further from current record-low levels, and, less obviously, to spur confidence that more monetary tools remain to stimulate the economy. Of course, the announcement also could push stock prices higher, as did the Fed's last balance sheet expansion begun in November 2010. Just a few months ago, market observers speculated that another round of quantitative easing — QE3, in this case — would be politically infeasible and probably unnecessary given hopes for better growth in 2012.

Fed Holds Off for Now on Bond Buys - Federal Reserve officials are waiting to see how the economy performs before deciding whether to launch another bond-buying program. The Fed meets again next Tuesday and Wednesday, and officials are preparing to roll out a new communications strategy that is on track to include two key elements: their interest-rate projections and a statement explaining their objectives for inflation and employment. Clarifying the central bank's objectives could make easier the tasks of deciding whether to buy more bonds and explaining their reasons. Enlarge Image Close.The Fed has purchased more than $2 trillion of securities since the crisis began, part of an effort to spur investment, spending and economic growth to reduce unemployment. Unemployment is high but has fallen during recent months, a sign that the recovery may be gaining traction. Some Fed officials are open to more bond buying if the economy doesn't continue to improve, or if inflation falls much below their objective of about 2%, but they believe the outlook is too murky to move now, and views vary on the costs and benefits. When they have publicly discussed the subject of asset purchases recently, many Fed officials have tended to hedge, suggesting that they aren't ready to make the leap.

Fed releases templates for FOMC Fed Funds rate projections - From the Federal Reserve: Federal Reserve releases templates for reporting FOMC participants' projections of the appropriate target federal funds rate The Federal Reserve on Friday released blank templates showing the format of the two charts it will use on January 25 to report Federal Open Market Committee (FOMC) participants' projections of the appropriate target federal funds rate. It also released a draft of an explanatory note that will accompany the projections. The first chart, which will have shaded bars when released on January 25, will show FOMC participants’ projections for the timing of the initial increase in the target federal funds rate. The second chart, which will have dots representing policymakers’ individual projections when released on January 25, will show participants’ views of the appropriate path of the federal funds rate over the next several years and in the longer run. From Luca Di Leo and Jon Hilsenrath at the WSJ: Fed Details How It Will Release Rate Forecasts One of the new charts is a bar chart showing in which year officials expect to see the first short-term interest rate increase, with options ranging from 2012 all the way out to 2016. ... It was striking that the Fed charts go all the way out to 2016 — suggesting that some officials don’t see rate hikes for many more years.

Number of the Week: When Will Fed Raise Rates? -- 37: The number of months the Federal Reserve has kept rates near zero. The Federal Reserve gives its latest signal next week on when it plans to raise rates from historic lows. The only thing we know for sure is that it won’t be any time soon. The central bank first dropped its key interest rate to a 0-to-0.25 range in December 2008 in response to the financial crisis. Though the recession officially ended six months later, the recovery has been slow and the Fed has maintained low rates in order to spur markets and the economy. Following its meeting on Wednesday, the Fed will for the first time offer its own projections for when it expects the economy will be strong enough for interest rates to begin rising. The rate-setting Federal Open Market Committee already has indicated in its postmeeting statements that officials don’t expect to raise rates at least through mid-2013. Markets and most economists surveyed by the Wall Street Journal expect it will be even later. The following charts are based on templates the Fed plans to use next week. They show when economists expect the central bank to increase rates, and where economists expect interest rates to be at the end of each year. (Read more about the Fed’s plans here.)

Four banks set to bid for mortgage securities - Four Wall Street banks were on Tuesday finalising bids for $7bn of mortgage-related securities that used to belong to AIG and are due to be auctioned later this week by the Federal Reserve Bank of New York. Goldman Sachs, Barclays Capital, Bank of America and Credit Suisse will bid on the debt, which was acquired by the New York Fed as part of the bail-out of AIG in 2008. The auction is scheduled to take place on Thursday, with BlackRock Solutions managing the sale, according to people familiar with the matter. The four banks and the New York Fed declined to comment. The securities, which have a notional value of $7bn, are part of a $20bn portfolio housed in a special purpose vehicle called Maiden Lane II. The Fed last spring began efforts to sell the entire portfolio on the open market, but officials suspended the auction during the summer after drawing lacklustre demand, causing the market for subprime and other risky mortgage debt to fall. This time, the sale will involve just the four banks, who will bid based on the appetite of their investor clients. The banks and investors were required to sign confidentiality agreements so they could scrutinise the portfolio and calculate prices. The Fed is expected to sell the whole $7bn in securities to one of the dealers or not sell it at all, if it finds the bids unattractive.

Fed Back To Its Secretive Ways, Sells $7 Billion In Maiden Lane Assets Directly To Credit Suisse Without Public Auction -Instead of opting for a publicly transparent BWIC in the disposition of its Maiden Lane II assets, the Fed has once again gone opaque - long a critique of the Fed's practices which have required repeated FOIAs in the past to get some clarity on its secret bailouts and transactions - and proceeded with a private sale, without any clarity on the deal terms, in which it sold $7 billion in face amount of Maiden Lane II assets direct to Credit Suisse. The alternative of course would be the same snarling of the MBS and broadly fixed income market that we saw in June of last year. In other words, the Fed looked at the options: transparency and risk of grinding credit demand to a halt, or doing what it does best, which is to transact in the shadows, and avoid capital markets risk. It opted for the latter. As to why the Fed decided to go ahead with a deal shrouded in secrecy? "The New York Fed decided to move forward with the transaction only after determining that the winning bid represented good value for the public." "I am pleased with the strength of the bids and the level of market interest in these assets," said William C. Dudley, President of the New York Fed.

The influence of MIT on macroeconomic policy - At MIT, King, 63, and then-professor Ben S. Bernanke, 58, had adjoining offices in 1983, spending the early days of their academic careers in an environment where economics was viewed as a tool to set policy. Earlier, Bernanke and European Central Bank President Mario Draghi, 64, earned their doctorates from the university in the late 1970s, Draghi with a thesis entitled “Essays on Economic Theory and Applications.” Fischer, 68, advised Bernanke’s thesis on “Long-Term Commitments, Dynamic Optimization and the Business Cycle,” and taught Draghi. Greek Prime Minister and former ECB vice president Lucas Papademos and Olivier Blanchard, now chief economist for the International Monetary Fund in Washington, earned their doctorates from MIT at about the same time.Other monetary policy makers who have passed through MIT’s doors include Athanasios Orphanides, head of the Central Bank of Cyprus, Duvvuri Subbarao, governor of the Reserve Bank of India and Charles Bean, King’s deputy in the U.K.

Graphical Representations of Bernanke's Effort to Stimulate Bank Lending - Bernanke is trying every way he can to get banks to lend (printing coupled with a multitude of lending facilities and Fed programs). It's easy enough to prove the printing: Base money supply is up about $1.8 trillion since the start of the recession. The Money Multiplier Theory (an incorrect theory) suggests this money would be lent out 10 times over causing rampant price-inflation and GDP growth. Alternate (Correct) Bank Lending Theory:

- Banks do not lend simply because they have the money

- Banks lend as long as they have credit-worthy customers provided the banks are not capital impaired

- Reserves are not an issue. Lending comes first, reserves follow if needed.

James Pethokoukis on NGDP Targeting - James Pethokoukis has a new article in Commentary that examines nominal GDP (NGDP) targeting and its potential to spark a recovery. The piece starts out fine, but then gets gets confused because it fails to distinguish between a NGDP growth rate target and a NGDP level target. A NGDP growth rate target, like an inflation target, let bygones be bygones. A NGDP level target, on the other hand, corrects for past mistakes. Under a NGDP level target a central bank would commit to reigning in aggregate nominal spending if it overshot and vice versa. Such a rule would therefore actually anchor long-run inflation expectations while allowing for aggressive catch-up growth (or contraction) in aggregate nominal spending so that NGDP returned to its trend path. The following figure illustrates these important differences:Note that with a NGDP growth rate target (the blue line) NGDP can be growing on target and yet the big collapse in aggregate demand that precedes it is never corrected. With those points made, let's turn to Pethokoukis' piece:

How Did the Fed Get Things So Wrong? - The public’s faith in the Fed’s ability to protect the economy from economic problems has been shaken by the Fed’s failures before and during the Great Recession. The recent release of the transcripts from 2006 monetary policy meetings where Federal Reserve policymakers discuss and ridicule the suggestion that the economy is threatened by a dangerous housing bubble has undermined its reputation even further. How did the Fed get things so wrong? How can policy be improved? The first step in the policy process is for policymakers to be aware that there’s a problem in the economy, and access to reliable, timely, and informative data is critical. Unfortunately, there are substantial lags in the availability of data that indicate where the economy is headed, and it can be six months or longer before key variables such as GDP are known. The fact that these data are not very timely, and are often revised substantially after they are released is not the Fed’s fault. But that doesn’t mean that the Fed can’t do more on its own. The Fed needs to do a much better job than it did before the crisis of using the data at its disposal to construct stress indices, measures of network reliability, price-rent ratios, credit measures, and so on to figure out what is happening in financial markets.

When Did The Fed Screw Up? - I've pasted above a chart that shows two things. The blue line measures market expectations of inflation over a ten year horizon. The red line shows the change in fixed private residential investment. You can see that the red line enters negative territory in the last quarter of 2005. Then it stays negative all four quarters of 2006, and during all this time the FOMC members are makign statements about how the economy should survive the housing bust. Then it's negative for four more quarters throughout 2007. And then for the first two quarters of 2008. It's only in the second half of 2008 that the monetary situation goes haywire, inflation expectations plunge, and the whole economy goes to crap. It then takes a looooong time for expectations to get back to the usual level and when they do so instead of delivering us a spurt of "catch-up" inflation the Fed lets them drop again. More recently, we've been back to a more-or-less stable level but with no catch-up. In my view, it's all that stuff that constitutes the screw-up that the Fed should be lambasted for. The damning transcripts are the ones from late 2008 and all of 2009. We haven't seen those transcripts yet because the Fed loves its secrecy and lack of accountability and Congress doesn't want to know the truth. But I'm not sure Ben Bernanke, Tim Geithner, and the others were in fact making any major mistakes in 2006 beyond underestimating how inept they would be in the fall of 2008 and the winter of 2008-9.

Did Fed Policy Matter to Housing Prices? - Kenneth Kuttner has a new paper that reexamines the relationship between the Fed's interest rates and house prices during the housing boom. The paper is receiving some attention because it claims that the existing literature on this topic collectively shows only a small role for interest rates on the housing prices. Here is Kuttner: All available evidence — existing studies, plus the new findings presented above — points to a rather small effect of interest rates on housing prices. VAR-based estimates of the effect of a 25 basis point expansionary monetary policy shock range from 0.3% to 0.9%, both in the U.S. and in other industrialized countries....they are too small to explain the previous decade’s tremendous real estate boom in the U.S. and elsewhere. Looking back it is clear that there were other developments that contributed to the housing boom like financial innovation, global demand for safe assets, poor governance, industry structure, housing policy, and misaligned creditor incentives. Contrary to the Kuttner's claim, however, this does not mean that the contribution of the Fed's low interest rates were trivial. Here are the reasons why.

The Federal Reserve Knew About the Housing Bubble in 2004…The data — both anecdotal and otherwise — was out there, and the Fed even discussed it internally. Let’s not let it off the hook. I noticed something odd about the recent release of the 2006 Federal Reserve Open Market Committee transcripts. Binyamin Appelbaum has a characteristically good article about the inept chatter at the FOMC meetings that year, where the various participants missed the housing bubble completely. And there has been suitable mockery of the Fed. What I’m finding, though, is a bit of an apologia for these folks in the form of “no one knew.” This is just not true. I remember in 2002-2003 I heard crazy stories about housing, where people would list their home and get 15 bids in 24 hours. It’s why I didn’t consider buying a home. It wasn’t just anecdotal, but the data was out there. And it’s clear, from going into earlier transcripts of FOMC meetings, that the Fed actually knew there was a housing bubble as early as 2004. Or rather, it had the data, both anecdotal and quantitative, and even discussed the possibility of a bubble internally. Ryan Grim and Calculated Risk picked this up in 2010.

A selection of comments from Federal Open Market Committee meetings which resulted in laughter - IN AN effort to boost transparency, the Federal Reserve now releases full transcripts of its Federal Open Market Committee meetings. In an effort to limit transparency, however, it does so on a lag. As of today, therefore, we are able to look back and see what was said in Fed meetings in 2006. In commemoration of this moment, Free exchange now presents: A selection of comments from Federal Open Market Committee meetings which resulted in laughter.

Chart of the day, FOMC laughter edition - I was hoping someone would do this — and now The Daily Stag Hunt has come to the rescue. All I can say is, thank you. It turns out that if you’re on the FOMC, then being in a credit bubble is really funny!

Laughter: The New Financial Instability Index - Phil Izzo of the Wall Street Journal points us to the invaluable work of the people at The Daily Stag Hunt, who tallied the number of times that laughter appears in the transcripts of the Fed’s FOMC meetings. Peak laughter, as The Daily Stag points out, corresponds nicely with the height of the housing bubble: If there weren’t a six-year delay on the release of these transcripts, this could be a useful tool for measuring systemic risk.

The Fed needs better data - Mark Thoma in The Fiscal Times wrote an interesting post on how the Fed can prevent the next financial crisis. What caught my attention was not his conclusion that the Fed could prevent the next financial crisis, but rather what he considered the critical first step. The first step in the policy process is for policymakers to be aware that there’s a problem in the economy, and access to reliable, timely, and informative data is critical. Unfortunately, there are substantial lags in the availability of data that indicate where the economy is headed, and it can be six months or longer before key variables such as GDP are known. This is a problem that doesn’t get enough attention, and in the information age we ought to be able to do better. His point about the critical need to have access to reliable, timely, and informative data and that in the information age we ought to be able to provide this data is one your humble blogger has been making since before the beginning of the credit crisis.

The Role of Safe Assets in a Financial System - "The Safe-Asset Share," is one of those rare academic papers with a basic empirical finding that shakes up your mental landscape, at the annual meetings of the Allied Social Science Associations a couple of weeks ago in Chicago. Here is their opening: "Over the past sixty years, the total amount of assets in the United States economy has exploded, growing from approximately four times GDP in 1952 to more than ten times GDP at the end of 2010. Yet within this rapid increase in total assets lies a remarkable fact: the percentage of all assets that can be considered “safe” has remained very stable over time. Specifically, the percentage of all assets represented by the sum of U.S. government debt and by the safe component of private financial debt, which we call the “safe-asset share”, has remained close to 33 percent in every year since 1952." The dynamics of the safe-asset share are important for economists, policymakers, and regulators to understand because “safe” debt plays a major role in facilitating trade. ... To the extent that debt is information-insensitive, it can be used efficiently as collateral in financial transactions, a role in finance that is analogous to the role of money in commerce. Thus, information-insensitive or “safe” debt is socially valuable.

Cleveland Federal Reserve: Ten-Year Expected Inflation is Only 1.39%, the Lowest in 30 Years - "The Federal Reserve Bank of Cleveland reports that its latest estimate of 10-year expected inflation is 1.39 percent. In other words, the public currently expects the inflation rate to be less than 2 percent on average over the next decade (see chart above). The Cleveland Fed’s estimate of inflation expectations is based on a model that combines information from a number of sources to address the shortcomings of other, commonly used measures, such as the "break-even" rate derived from Treasury inflation protected securities (TIPS) or survey-based estimates. The Cleveland Fed model can produce estimates for many time horizons, and it isolates not only inflation expectations, but several other interesting variables, such as the real interest rate and the inflation risk premium." Inflation expectations are currently close to the lowest level in at least 30 years (see chart above).

Key Measures of Inflation moderate in December - Earlier today the BLS reported: The Consumer Price Index for All Urban Consumers (CPI-U) was unchanged in December on a seasonally adjusted basis ... The index for all items less food and energy increased 0.1 percent in December after rising 0.2 percent in November. The Cleveland Fed released the median CPI and the trimmed-mean CPI this morning:the median Consumer Price Index rose 0.2% (2.9% annualized rate) in December. The 16% trimmed-mean Consumer Price Index increased 0.1% (1.5% annualized rate) during the month....The CPI less food and energy increased 0.1% (1.8% annualized rate) on a seasonally adjusted basis. Over the last 12 months, the median CPI rose 2.3%, the trimmed-mean CPI rose 2.5%, the CPI rose 3.0%, and the CPI less food and energy rose 2.2%. This graph shows the year-over-year change for these four key measures of inflation . On a year-over-year basis, the median CPI rose 2.3%, the trimmed-mean CPI rose 2.5%, and core CPI rose 2.2%. Core PCE is for November and increased 1.7% year-over-year. On a monthly basis, the median Consumer Price Index increased 2.9% at an annualized rate, the 16% trimmed-mean Consumer Price Index increased 1.5% annualized, and core CPI increased 1.8% annualized.

. On a year-over-year basis, the median CPI rose 2.3%, the trimmed-mean CPI rose 2.5%, and core CPI rose 2.2%. Core PCE is for November and increased 1.7% year-over-year. On a monthly basis, the median Consumer Price Index increased 2.9% at an annualized rate, the 16% trimmed-mean Consumer Price Index increased 1.5% annualized, and core CPI increased 1.8% annualized.

Michael Kinsley And The Phantom Menace - Krugman - Kevin Drum sends us to Michael Kinsley, who is still worried about inflation despite its failure to explode the way he thought it would. Kevin points out that Kinsley makes a claim that is just false: that economists have started saying that a little more inflation would be good are making excuses for a loss of control. Heck, I first made that case almost 14 years ago! And this false claim is the heart of Kinsley’s current argument. But let me focus on something else Kinsley doesn’t seem to get: he protests that I offer no criteria for when it’s time to worry about debt again: Another reason I remain worried about inflation is that for two years I have been waiting for Paul Krugman to tell us when we should reverse course. Krugman’s basic analysis of the situation is persuasive. He thinks President Barack Obama’s $800 billion stimulus package in 2009 was much too small to have the desired Keynesian effect of kick-starting the economy. And then somehow we wasted all of last year arguing about how to reduce the budget deficit, instead of realizing that reducing the deficit – - however you do it — amounts to reducing the stimulus, when we ought to be increasing it. When the economy is robust again, it will be time to start paying down the debt. Hello? Right there he concedes that I have given an answer: when the economy is robust again.

Consumer Price Index vs. Personal Consumption Expenditures Index - Consumer Price Index (CPI) from the Bureau of Labor Statistics is the measure of inflation that gets the most attention, both from the media and in most intro econ classrooms. But I'm thinking that the Personal Consumption Expenditures (PCE) index measure of inflation should start to get equal or perhaps even greater attention. For starters, I hadn't known--although I probably should have known--that when the Federal Reserve looks at rates of inflation, it focuses more on PCE than on CPI. The announcement of this policy change was buried in a footnote in the Fed's Monetary Policy Report to the Congress. There's some jargon in the quotation, which I'll unpack in a minute, but here's the comment: The chain-type price index for PCE draws extensively on data from the consumer price index but, while not entirely free of measurement problems, has several advantages relative to the CPI. The PCE chain-type index is constructed from a formula that reflects the changing composition of spending and thereby avoids some of the upward bias associated with the fixed-weight nature of the CPI. In addition, the weights are based on a more comprehensive measure of expenditures. Finally, historical data used in the PCE price index can be revised to account for newly available information and for improvements in measurement techniques

How Stories about Economic Fundamentals Drive Financial Markets - Fund managers cannot possibly know what the future will bring, yet they have to commit today to holding assets that promise a return tomorrow. Such a commitment requires confidence -- confidence that is hard to find in the face of uncertainty. To cope with the uncertainty, fund managers rely on gut feelings and invent stories that justify their decisions. In the end, it is stories and emotions that drive financial markets. That is, in a nutshell, the theory of asset pricing developed by David Tuckett. Some unconventional advice to monetary policy follows. Central banks, Tuckett says in this interview with INET Executive Director Robert Johnson, should create stories themselves. This is not to call for central bankers to tell fairy tales. No, what central banks can do is create their own stories -- stories that are anchored in meticulous observation and forensic analysis of new markets and new business opportunities.

Paul Davidson: What Makes Economists So Sure of Themselves, Anyway? - In a recent interview I asked the US’s leading post-Keynesian economist and founder of the Journal of Post-Keynesian Economics, Paul Davidson to discuss what is known as the ‘ergodic axiom’ in economics. This is a particularly important axiom as it allows mainstream economists (including left-wing Keynesians like Paul Krugman and Joseph Stiglitz) to claim that they can essentially know the future in a very tangible way. It does this by assuming that the future can be known by examining the past. Without this axiom the whole edifice of mainstream theory rests on very shaky grounds. Yet, it should be clear to anyone that given that the theory is supposed to explain human behaviour it is unlikely that the future will correlate with the past because people and institutions tend to change and evolve over a given period of time. Yes, often past behaviour will help us understand future behaviour – apply this in a simple psychological way to anyone you know and you will find it to be true – however, it should be quite clear that all future behaviour cannot be wholly explained by past behaviour. Clearly it should be quite obvious that the same should apply when we consider large aggregates of individuals and yet mainstream economics steadfastly refuses to accept this.

JOLTS Data and Theories of the Great Recession - The JOLTS data provide three major challenges to any disruptions hypothesis of the Great Recession. That is, any hypothesis that says the United States was engaged in some form of economic production that was disrupted by event X and that led to a huge recession until we could get back on our feet. This includes the vast majority of structural theories. The first problem is that job destruction fell dramatically during the Great Recession. Second, Job Hires are typically very close to separations. However, in late 2008 the two broke apart. Even still the gap, though enormous up to 700K was still small in comparison to the low point in hires 3600K. What’s more is that third, if you look closely at the pattern of separations and hires, it looks like what happened was that separations stalled in late 2008 while hires continued its downward trajectory.

The Fed’s Pyrrhic Victory - Recent data suggest that the mini revival in domestic economic fortunes is largely attributable to an increase in household outlays. This would be good news if the increase was due to household income growth. But, the increase is instead the result of households spending more out of the same income. This questions the durability of the expansion, as declines in savings are hardly a sound foundation on which to build income growth. The economy’s ongoing dependence on consumer outlays also puts a focus on the policy objectives of those on the Federal Open Market Committee, like Federal Reserve Bank of New York President William Dudley, who wish to use the threat of accelerating inflation to increase household spending. The U.S. will never be able to transform itself from a consumption-dependent, net importer as long as the penalization of savings remains the preferred mechanism to generate short-term growth. The economy has received a spate of good news recently, raising hopes that growth will meaningfully dent the chronic unemployment problem. The economy added 200,000 net jobs in December and the narrow and broad unemployment rates fell to 8.5% and 15.2%, respectively. Many economists anticipate that the economy expanded at an annualized rate of more than 3%, due in part to the 1.5% of GDP liquidation of inventories in the third quarter. Even if final demand remains unchanged, the inventory rebuild will likely add more than one point to GDP in the fourth quarter.

GDP Revisions - This is just a short post to illustrate the magnitude of GDP revisions. I downloaded quarterly GDP data from BEA in June 2011. I went back to BEA this morning to update the file. Forgetting about GDP revisions, I thought I'd be adding 2 or three more quarters of data, but discovered that all the numbers since Q2 2003 had been revised. Prior values are unchanged. Plotted below is the difference between the June, 2011 numbers and what I found this morning. The depth of the trough in Q3 2009 was $194 Billion worse than we thought just a few months ago. I was surprised to see the revisions go back a full 9 years. Tyler Cowan got one thing right. We are poorer than we think we are.

Monthly GDP Declined 0.8% in November - Macroadvisers - Monthly GDP declined 0.8% in November, partially reversing a 1.3% increase in October. The November decline was more than accounted for by inventory investment and net exports; domestic final sales posted a decent gain. The level of monthly GDP averaged over October and November was 3.2% above the third-quarter average at an annual rate. Our latest tracking forecast of 3.0% annualized growth of GDP in the fourth quarter assumes a 0.3% increase in monthly GDP in December. This is from a commentary that was published on January 17, 2012.

The Fed, Paul Krugman & The Economic Bullshit Artistry In Election Year 2012 - One of the problems our insolvent industrial economics has, and it’s only one, is quantitatively aggregating value, GDP is the easiest example, then saying this provides a clear picture of what’s happening in the economy. Unfortunately, the fact is all dollars are not equal, for example a dollar spent on potatoes feeding a family of four, has a lot more value than a dollar spent on landscaping a home in Bel-Air, just don’t tell an economist this. It’s why they can interminably bleat American economy is no longer as reliant on oil, and when the price of oil goes up, it’s no harm to the economy, “After all, we now only spend “x”% of GDP on oil.” Nonetheless, the price of oil goes up, the economy slows. Who you going to believe, your lying eyes or a Nobel Laureate? Which gets us to a little report by the Fed, a truly corporate global institution, on how the tit-titting about industry moving to China is much ado about nothing, after all it only adds up to 2.5% of GDP–well, actually the Fed estimates it as “personal consumption data.” Mr. Krugman, who owes his whole career to being a shill for corporate globalization, and in particular selling it to liberals, jumps right in to show how smart the Fed is–and of course, this globalization thing has always been overrated in its impact on the US economy. This by the way is the same guy who has written repeatedly in the august pages of the NYT that the key to revitalizing the American economy is for the Renminbi to appreciate. So, who you gonna believe, a Nobel Lauraete, taking on his election year hack role as a Democrat, or your lying eyes, looking at miles and miles of abandoned manufacturing areas across the midwest and northeast, and shuttered main streets across the country where Wal-Mart, packed with Chinese manufactures, monopolizing a good chunk of “personal consumption” in those communities?

Is The Yield Curve Still A Reliable Signal Of Recession Risk? - In the current debate about recession risk, some commentators have rolled out the yield curve argument or variations thereof. On first glance, this line of analysis looks like a slam-dunk refutation of the forecast by some that another economic contraction is now fate. But such arguments based heavily (or exclusively) on the yield curve risk overplaying their hand. It’s true that the yield curve has been a reliable predictor of recessions for half a century, as many studies assert. But in the dark art of developing macro forecasts, one can never assume that a predictor’s track record—even one as strong as the yield curve’s—seals its fate for repeat performances. It'd be wonderful if we could point to one indicator as a dependable predictor, but macro's just not that simple. But let’s back up for a minute and recognize the yield curve’s allure. It’s well known that when short rates rise above long rates, that’s been a strong signal that the economy was headed for a recession in the near term. This track record is quite clear by reviewing the yield spread for, say, the 10-year Treasury less the 3-month T-bill. For additional clarity, this signal can be transformed with a probit model so that the spread is converted into a probability estimate of future recession risk.

On Predicting the Future - I’ve long admired ECRI for their timely and accurate forecasts, and their willingness to stick by their models when things don’t seem to be immediately going their way. I have also appreciated their lack of willingness to divulge their model elements; my thoughts were, “Hey, it’s probably a simple model that no one has ever thought of. Would I reveal the model if I were in their shoes. No.” But I’m not in their shoes, and I know one of the ECRI pair, so I asked for some insight into the models, which he coldly refused. Okay, fair enough, I’m not a paying subscriber, but we had had good conversations in the past, so I thought I might have some relational capital, but no. Tonight, I bring you my kludge that should be close to the ECRI Weekly leading index. I am not saying that I reverse-engineered it because in econometrics there may be many fits with equal probability that explain the dependent variable well. But here we go.

Industrial Production Confirming Changes To LEI - For the last several months I have been scratching my head about the Leading Economic Indicator Index (LEI), as published by the Conference Board, due to the divergence between it and other leading indicators that we watch. The LEI has risen sharply while real indications of the economy such as changes to employment, industrial production, incomes and personal consumption expenditures have not. Furthermore, the sharp rise in the index from recessionary lows without the confirming rise of economic growth to new highs, as witnessed post every previous recessionary trough, has been a perplexing mystery given the fact ECRI's Weekly Leading Index and others have been showing leading indications of economic weakness. So, what does industrial production have to do with this? The release of industrial production today showed a 0.4% advance over the last month. On the surface this sounds positive, but in reality it goes further to confirm the LEI conundrum. While the LEI has soared off to the moon, industrial production has not only failed to attain a new high in this post-recessionary recovery, but it has peaked and begun to decline.

Insight: Recovery at risk as Americans raid savings (Reuters) - More than four years after the United States fell into recession, many Americans have resorted to raiding their savings to get them through the stop-start economic recovery. In an ominous sign for America's economic growth prospects, workers are paring back contributions to college funds and growing numbers are borrowing from their retirement accounts. Some policymakers worry that a recent spike in credit card usage could mean that people, many of whom are struggling on incomes that have lagged inflation, are taking out new debt just to meet the costs of day-to-day living. American households "have been spending recently in a way that did not seem in line with income growth. So somehow they've been doing that through perhaps additional credit card usage," Chicago Federal Reserve President Charles Evans said on Friday. "If they saw future income and employment increasing strongly then that would be reasonable. But I don't see that. So I've been puzzled by this," he said. After a few years of relative frugality, the amount of money that Americans are saving has fallen back to its lowest level since December 2007 when the recession began. The personal saving rate dipped in November to 3.5 percent, down from 5.1 percent a year earlier, according to the U.S. Commerce Department.

How high oil prices could squelch the recovery - As my colleague Steven Mufson reports today, tensions with Iran are putting upward pressure on crude prices — and oil was already at a record high in 2011. Analysts are now fretting that oil could kneecap the fragile recovery. So is there a good way of estimating the effects of pricier oil? According to a U.S. Energy Information Administration analysis, a $20 increase in the cost of a barrel of oil — roughly what we saw last year — is estimated to shave roughly 0.4 points off GDP growth in the first year alone and boost unemployment by 0.1 percentage points. So if Iran threatens to close the Strait of Hormuz (through which about 20 percent of the world’s oil flows) and prices start screaming upward from $107 per barrel to $120 or beyond, that would put a very noticeable dent in growth. What’s more, oil shocks tend to have long-lingering effects. The EIA estimates that a $20 price increase continues biting into the economy for at last another year thereafter. James Hamilton, an economist at the University of California, San Diego, has suggested that the consequences of a price spike can persist for several quarters, as the resulting slowdown in consumer spending takes some time to ripple through the economy. That’s true even if the spike is only temporary and recedes quickly.

Credit Stress Indicators: Little Spillover to US from Europe - As we've discussed, there are several possible channels of contagion from the European financial crisis. The most obvious is the trade channel. The recession in Europe appears to already be negatively impacting U.S. exports. The most recent trade report showed exports to eurozone countries declined 6.9% in November. A more significant channel would be tightening of U.S. credit conditions in response to the European crisis. . Since the most significant channel will probably be credit stress, here are a few indicators of credit stress:

- • The three month LIBOR has decreased: Data from the British Bankers' Association showed the three-month dollar London Interbank Offered Rate, or Libor, was fixed at 0.56230%, down from 0.56490% Monday.

- • The TED spread is at 0.537. The TED spread is the difference between the three month T-bill and the LIBOR interest rate. This peaked in December at 0.581 and has declined slightly since then. Here is a screen shot of the TED spread from Bloomberg.

- • The A2P2 spread as at 0.39. This spread is mostly moving sideways, and is far below the peak of the financial crisis of 5.86. This is the spread between high and low quality 30 day nonfinancial commercial paper.

- • The two year swap spread screen shot from Bloomberg. This spread has declined to 34.3.

Too Many Par Claims versus Sub-Par Assets: The world is a maze of debt. Debts layered on debts. The Earth and its productivity is roughly the same or better than prior years. What is the problem with the economy then? The problem is this: there are entities that made bad loans in the past that expect to be paid back in full. They assumed the future would be far better than it turned out to be. There is no way that the loans will be paid back in full. The solution is paying back at a discount, whether through compromise or insolvency. Wait. Many of the lenders are leveraged as well, and can’t take significant losses. Paying back at a discount will bankrupt a number of banks, which will in turn bollix the economy. So, we have to go slow? Does this bring us back to the problem of how one eats an elephant? “One bite at a time.” That is the method of Japan, leaving an over-indebted government, and reasonably indebted private sector. But it took two decades.

Habituating to Contraction - For the past 67 years, Americans have been conditioned to expect expansion and more of everything: more income, more stuff, more opportunity, more benefits, more medical care, more government entitlements, and so on. As a result, Americans have habituated to permanent expansion. The concept that contraction--less of everything--is the new normal simply doesn't register; it is rejected, denied, or decried as a great tragedy. The notion that it is simply reality does not compute with a populace habituated to permanent "growth" that is at worst interrupted by brief recessions. The voting public's demand for "permanent good news" promising permanent expansion has spawned a feedback loop of officially sanctioned manipulated statistics and media spin (a.k.a. propaganda) that expands with every administration, even as the real economy visibly weakens. Though the Obama Administration has perfected the techniques of presenting "permanent good news," the divergence of the real economy and the official "story" that "we've returned to permanent expansion" is widening. The real story is the "expansion" has cost the taxpayers trillions of dollars in new debt and trillions of dollars of backstops, shadow purchases and money-printing by the Federal Reserve. Roughly speaking, $6 trillion in additional Federal borrowing has been blown to simply keep the Status Quo from imploding, and around $13 trillion in guarantees, backstops, asset purchases, and losses made good have been issued to keep the Status Quo's financial sector afloat and in charge.

Global Deleveraging - You Are (Not) Here - In most countries, deleveraging is only in its early stages. In a report today, McKinsey notes that total debt to GDP has declined in only three countries since the 2008-09 crisis (US, South Korea, and Australia) as total debt has actually grown in the world's ten largest mature economies (due mainly to rising government debt - Keynesian style?). Greatly concerned that the UK and Spain are slow to delever, they do note that the US is more closely following the two phase deleveraging process that 1990s Finland and Sweden followed but point to the household segment as leading the way with 15% reduction in debt to disposable income (driven unsurprisingly in major part by mortgage defaults). The bottom line is US (households) are at best one-third of the way through their deleveraging and the UK (financials) and Spain (non-financials) face much more significant pressures (which will inevitably impact aggregate demand given governmental borrowing pressures) as their deleveraging has only just begun. Historically, deleveraging has begun in the private sector and government has stepped up to borrow and fill the aggregate Keynesian hole left behind. McKinsey points out deleveraging normally takes 4-6 years which we suspect will remain an anchor for demand and growth in the mean-time.

Debt And Transfiguration - Krugman - Ryan Avent points out an important fact: if you look at total debt, public and private, the United States is doing better at deleveraging than countries that talk much more about the evils of debt than we do. I thought I would redo the calculation for the US so that I understood it. I focus on nonfinancial debt — that’s because money that banks owe to each other is more a reflection of the structure of the financial system than of the degree of overborrowing more broadly. So here’s nonfinancial debt, public plus private, as a percentage of GDP: What you see here is a gradual decline in overall debt — not at all what you hear in the public debate. Now, the composition of that debt is changing: rising public debt, falling private debt. But that’s exactly what you need to deal with the aftermath of a Minsky moment: you need to reduce the debt of balance-sheet-constrained players, so that the drag on the economy is reduced over time, eventually getting us to the point where deficit spending is no longer needed to sustain the economy. It’s a crime that we aren’t doing more, that unemployment is as high as it is — and sustained high unemployment is itself taking a toll on our future as well as our present. But as far as debt is concerned, America’s situation is getting better, not worse.

U.S. Takes Steps to Avoid Debt Ceiling The U.S. government curtailed its investment in a federal retirement fund Tuesday as it looks to stay under the legal debt limit while awaiting a congressional vote on raising the federal spending ceiling. Even if the Republican-controlled House rejects the increase, a measure of disapproval is unlikely to make it through the Senate, where Democrats hold a majority. The White House informed Congress last week that the government was close to its $15.194 trillion borrowing limit, setting in motion procedures that would likely raise the cap by $1.2 trillion later this month. The White House notification gives Congress 15 days to try to block the increase, though President Barack Obama can veto such a measure. The political theater—the House is expected to vote Wednesday—is a result of last summer's compromise to raise the debt ceiling in stages.

Treasury dips into pension funds to avoid debt - The Treasury on Tuesday started dipping into federal pension funds in order to give the Obama administration more credit to pay government bills. "I will be unable to invest fully" the federal employees retirement system fund beginning Tuesday, Treasury Secretary Timothy Geithner said in a letter to Democratic and Republican leaders in Congress. The House of Representatives is expected to vote on Wednesday on the Obama administration's request to raise the country's legal debt limit to $16.394 trillion.However, unless the lower chamber and the Senate are able to shore up enough votes to block the White House request, the debt limit will be increased by $1.2 trillion next Friday and a repeat of last year's debt ceiling debacle will be averted.

U.S. could hit debt ceiling again around election (Reuters) - The latest $1.2 trillion increase in the U.S. debt limit may not last through November's election and could provide fresh ammunition for Republicans to attack President Barack Obama on what they see as a particularly vulnerable point - spending. Based on current deficit rates and borrowing estimates, some analysts say the United States could reach the debt ceiling again before the November 6 vote. This would force the U.S. Treasury to turn once more to accounting maneuvers to avoid the unthinkable: asking Congress for another increase as the presidential election campaign reaches its crescendo. But any moves by the Treasury would likely not stop the issue from becoming fodder for Republican attack ads. Estimates on when the United States will reach its debt limit vary, but they leave little room for the Treasury to cope with an economic shock, such as a global slowdown triggered by a worsening of Europe's debt crisis, which could shrink U.S. revenues and boost spending on unemployment aid. "If the debt ceiling were to breached before the election, it would be possibly nuclear," said Ethan Siegal, who advises institutional investors on Washington politics. A full replay of last summer's debt limit battle, which brought the United States to the brink of default and prompted a U.S. credit rating downgrade from Standard & Poor's, would rattle markets and put Obama at the mercy of Republicans in the House of Representatives bent on slashing spending.

US inflation bond sale fetches negative yield (Reuters) - Investors scooped up a record offering of U.S. government debt that promises inflation protection on Thursday, even though there are no signs that food and energy prices are running out of control. They bought $15 billion worth of 10-year Treasury Inflation-Protected Securities at a negative yield at an auction for the first time in the 15 years since TIPS were introduced. These latest 10-year TIPS cleared at a yield of minus 0.046 percent, lower than what traders had expected. This meant investors essentially paid the U.S. government to own 10-year TIPS at a time when some of them have been hoarding Treasuries including TIPS due to fears about Europe's debt crisis spiraling out of control. "It's a safe-haven play. It's all about the return of capital rather than the return on capital," said Richard Schlanger, a portfolio manager at Pioneer Investments USA in Boston. The yield on U.S. 10-year Treasury Inflation-Protected Securities has set a series of record lows in negative territory in recent days on this intense safe-haven demand. Even tame December readings on the government's Consumer Price Index, which TIPS principal and interest payments adjust against, did not cool the bidding for these pricey securities. The total accepted bids for the 10-year TIPS issue to the amount offered came in a ratio of nearly 3-1, which is the strongest since an auction last March.

2012 Budget Debate: Like "The Hangover, Part II" - The 2012 budget debate in Washington is going to be vastly different from the one that took place in 2011. This doesn’t mean the long-term deficit is no longer an issue. It also doesn’t mean there won’t be the usual noise when it comes to spending and revenues. Multiple rounds of finger pointing, recriminations and constantly repeated nonsensical statements should be expected. There also will be the standard complaints that no one outside the Beltway will really care about regarding missed deadlines and the need to use some vote to send a message to (choose all that apply) the American people, Wall Street, the House, the Senate, the Democratic Party, the Republican Party, the leadership, etc. And the phrase “dead on arrival” will be used so often this year that those involved in the budget debate will seem more like medical examiners than legislators with fiscal policy responsibilities.

New Year, New Government Showdown Brewing - With Congress set to return to town this week, staff-level bipartisan discussions are underway over how to pay for extensions of the payroll tax cut, unemployment insurance and the so-called Medicare “doc fix” beyond the end of February, when they’re set to expire. The private meetings are a continuation of the December showdown, which ended with two-month extensions of the three provisions and a guarantee that the House and Senate would negotiate a year-long measure.But many of the factors that made the two month bill so contentious remain in place, and threaten a new brinkmanship at the very beginning of this session of Congress. The political chemistry will be familiar to those who closely followed the highly reactive dynamics on Capitol Hill in 2011. Both parties agree that all three items need to be extended, and Democrats have accepted that they ought to be paid for. The question is how to fund them. And for some Republicans, it’s whether to extend them at all without demanding unrelated, partisan policy concessions from Democrats in return.

Congress Is Back, and So Are Its Battles Over Tax and Budget Policy - The least popular Congress in memory is back. Tax policy will be at the center of much of the partisan squabbling, but it is hard to imagine Congress achieving more than a temporary truce in its ongoing battle over last year’s unfinished business. That skirmishing starts with the 2011 payroll tax cut which, after a bruising battle last December, Congress extended only to the end of February. It also includes about four dozen other temporary tax cuts that expired last December 31. On the spending side, lawmakers must resolve controversies over extended unemployment benefits and Medicare physician payments—the so-called “doc fix”– that also must be addressed by March. But all that will just be a warm up for what promises to be an awful year-end when lame-duck lawmakers will face their own version of an ugly triple witching hour. They’ll have to decide what to do about the expiring Bush-era tax cuts that were extended at the end of 2010 by President Obama and a Democratic Congress, as well as several of Obama’s own temporary tax cuts. And they need to extend the “patch” that protects 25 million households from the Alternative Minimum Tax. There’s more: They’ll also have to figure out what to do about the automatic across-the-board spending cuts that are supposed to be the price of Congress’ failure last year to cut the deficit by $1.2 trillion. And Congress will have to vote yet again on a debt limit extension. All of this will likely happen in a lame-duck Congress that must negotiate with Obama, who either will have been reelected or will himself be on the way out the door.

St. Louis Fed Says CBO Doesn’t Forecast Deficits Well - Congress’s long history of underestimating future budget deficits suggests the current outlook for the nation’s finances may be even grimmer than many now expect. A new paper by the Federal Reserve Bank of St. Louis argues the Congressional Budget Office has for some time consistently underestimated how much the government would need to borrow. According to bank researchers Kevin Kliesen and Daniel Thornton, “if past behavior is a guide to the future, our analysis suggests that projected future deficits will likely be larger than those currently projected.” If they’re right, the already difficult politics surrounding the future of the nation’s finances could become even more fraught. The CBO projected late last summer the deficit would represent 6.2% of the gross domestic product this year, falling to 3.2% in 2013, and then averaging 1.2% between 2014 to 2021. The baseline forecast projects $3.5 trillion in borrowing between 2012 and 2021. Those aren’t great numbers — if they’re worse, the choices before Congress and the administration become even starker than they are now.

Washington is Spending Too Much - In the Wall Street Journal, former Chairman of the Council of Economic Advisers, argues that the real budgetary problems are (much further) down the road: The deficit shot up in basically equal measure from taxes falling and spending rising. Spending rose to 25% of GDP from 20.5% in the recession and soon it will fall back down. Taxes fell to 14.5% of GDP from 18.5% and will also return to more normal levels. The true fiscal challenge is 10, 20 and 30 years down the road. An aging population and rising health-care costs mean that spending will rise again and imply a larger size of government than we have ever had but with all the growth coming from entitlements—while projected federal revenues as a percentage of GDP after the rate cuts of the 2000s will likely remain below even historic levels of 18%… Iowa showed us a series of candidates trying to outdo one another with condemnation for the short-term rise in spending while simultaneously proposing tax policies that would add trillions to the long-term deficit. Goolsbee argues that the Obama Administration’s record on fiscal policy is sound. According to him, high levels of spending (and low levels of taxation) during the past several years were justified as responses to the recession. The real challenge lies instead in managing fiscal headwinds going forward, and political candidates ought to be judged on that basis.

The Least Refuse Of A Squirrel - Krugman - People have been asking me about Steve Rattner’s op-ed, which does seem to be aimed at me. My initial reaction was sheer bafflement: Rattner first attacks a view that, as far as I know, nobody holds, then makes his case by saying in as many ways as he can think of that the debt is huge, huge I tell you. What’s going on here? Luckily, Dean Baker seems to have figured it out. As Dean says, the key piece is here: Here’s the theory, in its most extreme configuration: To the extent that the government sells its debt to Americans (as opposed to foreigners), those obligations will disappear as aging folks who buy those Treasuries die off. Maybe there’s someone in America who believes this; it’s a big country. But what makes Rattner think that anyone with influence on the policy debate believes this? Here’s what I think happened. Rattner read my article, saw that I was denying that debt imposes the kind of burden on the next generation that people say, and immediately threw down the paper and began composing an indignant reply to what he assumed I must have been saying.

Deficit Doves and Owls: How to Worry About Healthcare Costs - You may not agree with Alan Blinder when he writes in the Wall Street Journal that the budget deficit should be an issue in the 2012 campaign. But it certainly will be. And Blinder deserves kudos for pointing out that there are no immediate or near-term economic problems stemming from US deficit and debt levels: “Myth No. 2 is that America’s deficit problem is so acute that government spending must be cut right now, despite the struggling economy. And any fiscal stimulus, even the payroll-tax extension, must be “paid for” immediately. Wrong. Strange as it may seem with trillion-dollar-plus deficits, the U.S. government doesn’t have a short-run borrowing problem at all. On the contrary, investors all over the world are clamoring to lend us money at negative real interest rates. In purchasing-power terms, they are paying the U.S. government to borrow their money!” Blinder also points out that if you accept the CBO’s long-term budget forecasts (James Galbraith notes some problems with the projections here), then the issue is entirely one of healthcare costs. Deficit doves and deficit owls (proponents of “functional finance”) will dispute the optimal or sustainable level of long-term deficits, but if you care about the long-term deficit, then you care about government healthcare costs. And growth of government healthcare costs is largely a function of cost inflation in the private market. So if you have any interest in the long-term deficit, then you have to have a plan for controlling long-term healthcare costs system-wide. If you don’t have such a plan, you’re engaged in some other type of project.

Four Deficit Myths and a Frightening Fact - Try to ignore the current shallowness in American politics, if you can, and assume that the federal budget deficit will be among the major issues of the 2012 campaign. I'd like to explode four myths now masquerading as facts.

- • Myth No. 1 is that the American people now demand deficit reduction as never before. Don't believe it. Yes, if you ask Americans about the deficit, they'll tell you they hate it—as they always have. But opinion polls show that the budget deficit is nowhere close to being Economic Public Enemy No 1. People care far more about high unemployment, the weak economy and the like.

- • Myth No. 2 is that America's deficit problem is so acute that government spending must be cut right now, despite the struggling economy. And any fiscal stimulus, even the payroll-tax extension, must be "paid for" immediately.

- • Myth No. 3: For several years now, our political system has focused exclusively on the 10-year cumulative budget deficit. In truth, however, what happens over the next decade barely matters. Our deficit problem—and it is a whopper—is much longer-term than that.

- • Myth No. 4 is that America has a generalized problem of runaway spending, one that requires cuts across the board. No. The truth is that we have a huge problem of exploding health-care costs, part of which shows up in Medicare and Medicaid spending.

Filling a hole or priming the pump? - Who knew that neoclassical economists had something perspicacious to add to the stimulus debate? Steve Williamson sends me to this AEA talk by Jim Bullard of the St. Louis Fed. The presentation is mostly a rebuttal of the common liquidity-trap arguments for stimulus, but at the end, there was this one really interesting slide: An alternative theory

- An alternative theory is much less studied but closer to the rhetoric on fiscal policy effectiveness.

- Suppose two regimes exist, one involving high growth and the other involving low growth.

- Heavy government borrowing might signal that the high growth regime is likely; this might then influence private sector expectations and private sector decisions.

- The high growth equilibrium could be encouraged as a self-fulfilling prophecy.

- However, if government spending is viewed as wasteful, the private sector could coordinate on low growth.

Williamson adds: As Bullard states, the type of coordination failure that some Keynesians appear to have in mind - self-fulfilling beliefs about the future driven by fiscal policy - has not really been formally studied.

The Pros and Cons of Obama's Reorganization Plan - On Friday, President Obama announced plans to consolidate a number of federal agencies related to business and trade into a single agency in order to improve efficiency and the international competitiveness of American companies. The agencies to be combined are the Department of Commerce, the Small Business Administration, the Export-Import Bank, the Overseas Private Investment Corporation, the Trade and Development Agency, and the Office of the Trade Representative. A 2010 report from the Congressional Research Service provides a good overview of the functions of these organizations.This is not a new idea. In 1983, President Reagan asked Congress for a similar reorganization. According to a New York Times article, the purpose of the new agency was to create an American version of Japan’s powerful Ministry of International Trade and Industry. At the time, Japan was widely viewed the same way China is today: as our greatest economic competitor and potentially a national security threat as well. Economists now discourage developing nations from adopting Japanese-style industrial policies. Nevertheless, the Obama administration appears enamored with exactly the sort of industrial policy that Japan rejected.

Say's Law For Thee But Not For Me - Krugman - In correspondence, Mark Thoma notes a double standard in the conservative outcry over the Keystone XL decision. As he notes, when it comes to the question of whether government spending can create jobs, the usual suspects claim that it’s logically impossible: income has to be spent somewhere, so all the government can do is divert funds from other uses. But when it’s a private investment, somehow that logic no longer applies. The truth is that the logic is wrong in all cases — spending isn’t fixed. But it’s still interesting to note this double standard; it’s more evidence of lack of good faith.

How Austerity Could Fail Its Way Into US Hearts and Minds - Marshall Auerback compares the job numbers in the US to those in Europe and asks why the US is doing so much better (or failing less miserably). One of the differences he highlights is the zealous dedication to fiscal austerity in Europe, compared to the relatively half-hearted, passive observance of doctrine in the US. For people operating on the basis of loose stereotypes about the differences between the US and Europe, this has perhaps turned out to be surprising. You might have assumed that Europe’s more expansive social welfare systems would be accompanied by more progressive approaches to fiscal or monetary policy. But as Matt Yglesias observes, Europe is awash in some pretty conservative ideas about macroeconomic policy:… the American right has lately fallen out of love with both J.M. Keynes’ fiscal stimulus ideas and Milton Friedman’s monetary stimulus ideas. Tussle between these two has dominated practical policymaking for decades in the United States, but if conservatives were to cast their eyes toward Europe they’ll find a continent where these ideas about demand-side management get short shrift.

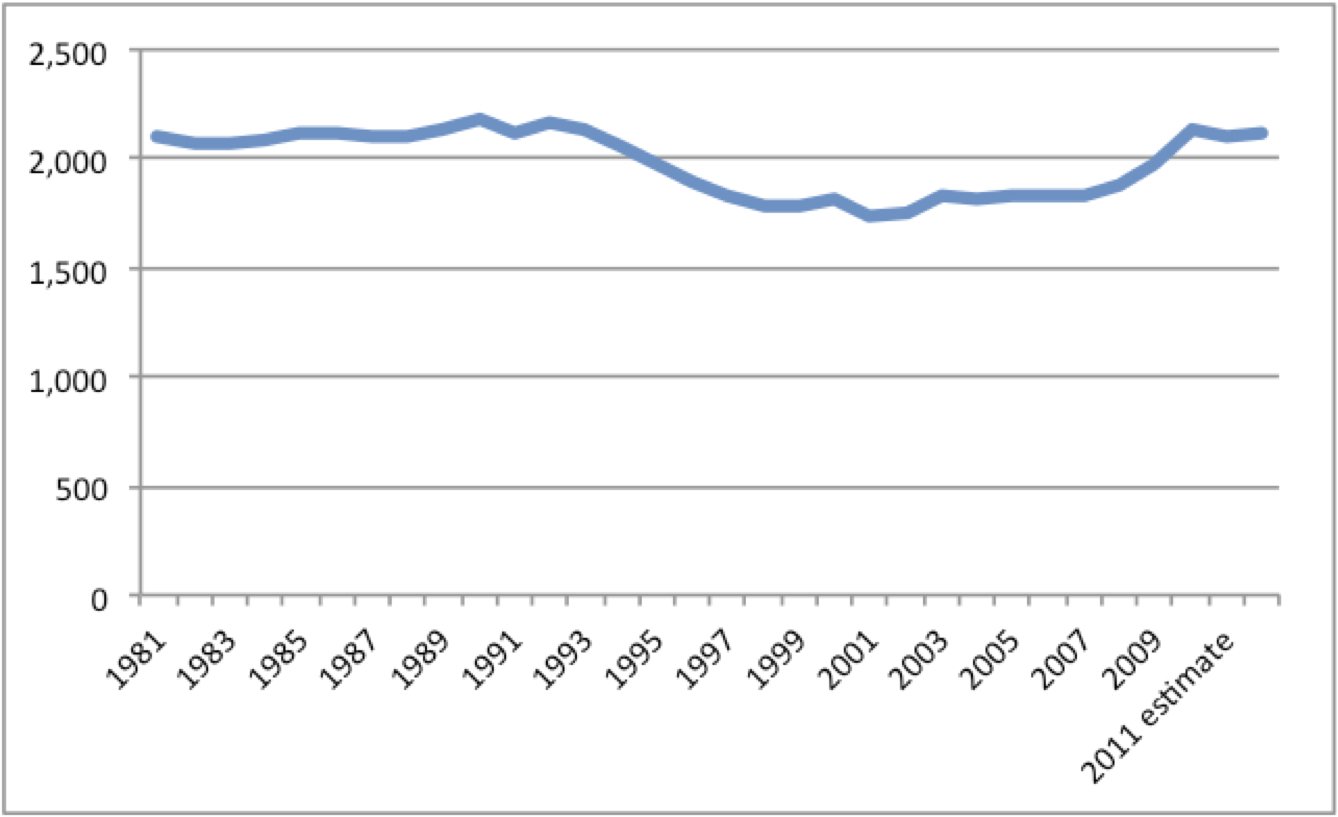

How the Wall Street Journal Misleads About Federal Jobs, by Jeff Sachs: The editorial board of Rupert Murdoch's Wall Street Journal has a simple game. They want to cut taxes for the rich and government services for the rest, and end regulations of banks and the environment. They support taxpayer-financed bailouts of Wall Street when needed. They will twist any facts in the service of these goals. Today's lead editorial, with its graph of "Obama's Growing Payroll," is a perfect example... The gist of the editorial is that Obama is presiding over a massive increase of government, exemplified by the surge of civilian employees. The graph shows a striking rise of federal employment from around 1.875 million in 2008 to 2.1 million in 2011. (I reproduce this as Figure 1 below). The Journal neglects the fact that today's 2.1 million workers is actually identical to the number of Federal employees in 1981 at the start of the Reagan Administration, 1989 at the end of the Reagan Administration, and 1993 at the end of the Bush Sr. Administration. The numbers went down slightly after that ... with a decline in Defense Department civilian employees, a decline that was probably offset by the rise of private defense contractors (not included in the OMB tables). There is no long-term trend at all. (I show this as Figure 2 below).

Would A President Romney Increase The U.S. Deficit And Debt? - Interesting column in yesterday's The New York Times by Jesse Eisinger of ProPublica about the budget strategy the U.S. might be following if it were a private equity firm, that is, if it were run as if it were Bain Capital, Mitt Romney's former employer.Eisinger's conclusion: Given the current incredibly low interest rates, the management of a private equity firm would be rushing to borrow more to finance its activities rather than to be repeatedly demanding that it deleverage and do less. In other words, running the U.S. as a business as Romney says if elected he could/would/will do, would actually get him to do the opposite of what he and others running for president and Congress are insisting needs to be done: They would be increasing the deficit and borrowing more rather than reducing it and shrinking federal activities. This is hardly the first time someone has suggested that a very low interest rate environment means that the federal government should be borrowing more rather than less. But given the hyper rhetorical Dark Ages state of the current budget debate in Washington when facts and substance take a back seat to pseudo religious economic and finance beliefs, it's the first time in a while that it's been talked about prominently in a mainstream publication.

Department of “Duh” - The Times has a story out today: Surprise, all the Republican candidates’ tax plans increase the national deficit! The numbers (reduction in 2015 tax revenues, from the Tax Policy Center):

- Romney: $600 billion

- Gingrich: $1.3 trillion

- (Late lamented) Perry: $1.0 trillion

- Santorum: $1.3 trillion

I guess that makes Romney the “fiscally responsible” choice, at least among the Republicans. But President Obama’s tax proposals would only reduce 2015 tax revenues by $222 billion. (That’s $385 billion in Table S-4 less $163 billion in Table S-3.) Second surprise: The big winners in all of these tax plans are the rich! (That’s not just in dollars, but in percentage increase in after-tax income.)

Ruth (Marcus): Romney Reforms More Ruthless Than (Even) Ryan’s - The Washington Post’s Ruth Marcus points out that if Mitt Romney really cares about the poor, he has a funny way of showing it–in this case, regarding his ideas for fiscal policy reforms: “I’m concerned about the poor in this country,” Mitt Romney said the other day. “We have to make sure the safety net is strong and able to help those who can’t help themselves.” I perked up at those words, because they were something of a departure from his usual stump speech and because they happened to come on a day when I had written about the dire implications of Romney’s proposals for the social safety net. I don’t question his sincerity. The problem: This fine sentiment doesn’t square with his actual policies… The impact of Romney’s approach on the safety net would go far beyond Medicaid. The brutal arithmetic of his stated plan to cap spending at 20 percent of gross domestic product — while, unlike Ryan, increasing defense funding — is that safety-net programs would have to be chopped significantly beyond where even Ryan would take them. Romney’s tax plan would exacerbate the unfairness. He would continue the Bush tax cuts for the wealthiest Americans and provide extra breaks that would primarily help the rich… At the same time, Romney would do away with recent increases in the child tax credit and the earned-income tax credit — provisions that help low-income families…

What difference will it make if Obama or Romney wins? - Karl has requested that, along with a few other people, I answer this question: What are the significant differences that you think we could actually see come to pass from a Romney Presidency versus an Obama Presidency? Here are Tyler Cowen, Kevin Drum, and Matt Yglesias. They all say a lot of believable things. I’m probably my least useful in this type of speculation, but here goes anyway. One thing I’m pretty confident in is that if we’ve arrived at Obama vs Romney, and I think we have, then we’ve already dodged the biggest bullets (you know who I mean). If we’ve passed through the better part of the recession by the time the election is over, one could imagine attention will turn to tax reform. I can see either supporting something like Simpson Bowles, but Romney relying somewhat more on changes in the social security formula and removing exemptions, where Obama would lean somewhat more on increases in top marginal tax rates and some new taxes. I don’t think that the differences here would be huge overall, especially given the range of what could be done, but small differences can be pretty consequential in terms of welfare when you are talking about a multi-trillion dollar economy, so I don’t want to overly minimize these differences.

Obama's tax dilemma: $1M or $250k? -President Obama faces a difficult choice in his upcoming budget: Stick with his policy of raising taxes on families making more than $250,000 annually or boost that threshold to $1 million. The president’s decision has major political ramifications, as Democrats and Republicans are expected to clash repeatedly this election year over taxes. Following historic Republican gains in the 2010 election, many congressional Democrats embraced the $1 million figure over fears that the GOP had gained the upper hand by criticizing the $250,000 mark. Democrats like Sen. Charles Schumer of New York have suggested that many families making $250,000 are not rich. He has acknowledged that Republicans scored political points by arguing that raising taxes on individual income above $200,000 and couples making more than $250,000 would hit a fair amount of small businesses.

Santorum’s Tax Plan Doesn’t Add Up -The good news is that much of Santorum’s plan is centered on lowering taxes. The bad news is that much of his tax relief is either welfare in disguise or social engineering. After weighing the plusses and minuses, the conservative Tax Foundation gave his plan a D+. That score might be generous.His individual income-tax plan has just two rates — 10 and 28 percent. He does not specify at what point those rates begin, but it is safe to assume that no one will experience a tax increase. His plan calls for the elimination of the alternative minimum tax and the estate tax. All that has much to recommend it, but Santorum would also triple the personal exemption for dependent children while maintaining the earned-income tax credit and the child tax credit. This move would radically reduce the percentage of taxpayers paying any federal income tax whatsoever. Since he would retain most of the other major individual tax deductions, complexity would not be reduced, but revenue would be radically lower. I will return to this in a moment.

GOP Candidates' Tax Cuts for the Rich Are Up to 270 Times Larger Than Their Tax Cuts for the Middle Class -The 2012 Republican candidates are largely in lockstep when it comes to economic policy, wanting to give huge tax cuts to the rich and corporations while doing next to nothing to boost consumer demand or help the middle class and the unemployed who have been battered by the Great Recession. In fact, according to an analysis by Citizens for Tax Justice, the average tax cuts received by the richest 1 percent of Americans under the Republican plans would be 270 times as large as the cut received by the middle class: The share of tax cuts going to the richest one percent of Americans under these plans would range from over a third to almost half. The average tax cuts received by the richest one percent would be up to 270 times as large as the average tax cut received by middle-income Americans. Click here to view larger. Perry wins the award with a tax cut for the richest 1 percent that is 270 times larger than his middle class tax cut, while Gingrich’s is 190 times larger. Santorum and Romney pull up the rear with tax cuts for the rich that are 100 times larger than the cuts for the middle class, while CTJ did not analyze Jon Huntsman or Ron Paul’s plans.