Fed's Balance Sheet Contracts In Latest Week (Dow Jones)- The Fed's asset holdings in the week ended Jan 4. stood at $2.920 trillion, down from $2.928 trillion reported a week earlier, the central bank said in a report released Thursday. Holdings of U.S. Treasury securities fell to $1.663 trillion on Wednesday from $1.672 trillion a week before. The central bank's holdings of mortgage-backed securities rose to $837.74 billion from $837.30 billion. Total borrowing from the Fed's discount lending window was $8.98 billion, down from $9.08 billion a week earlier, according to the report. There was no discount window borrowing by commercial banks, down from $42 million a week earlier. The Fed report showed that U.S. marketable securities held in custody on behalf of foreign official accounts was $3.402 trillion this week, down from $ 3.411 trillion the previous week. Meanwhile, U.S. Treasurys held in custody on behalf of foreign official accounts decreased to $2.671 trillion from $2.679 trillion the previous week. Holdings of agency securities fell to $731.31 billion, from the prior week's $ 731.80 billion.

FRB: H.4.1 Release--Factors Affecting Reserve Balances--January 5 2012

FOMC Minutes: Agreement to provide "projections of appropriate monetary policy" in January - From the Fed: Minutes of the Federal Open Market Committee, December 13, 2011 and conference call on November 28th. Excerpts: In their discussion of the economic situation and outlook, meeting participants agreed that the information received since their previous meeting indicated that economic activity was expanding at a moderate rate, notwithstanding some apparent slowing in global economic growth. Regarding the economic outlook, participants continued to anticipate that economic activity would expand at a moderate rate in the coming quarters and that, consequently, the unemployment rate would decline only gradually. The factors that participants cited as likely to restrain the pace of the economic expansion included an expectation that financial markets would remain unsettled until the fiscal and banking issues in the euro area were more fully addressed. Other factors that were expected to weigh on the pace of economic activity were the slowdown of economic activity abroad, fiscal tightening in the United States, high levels of uncertainty among households and businesses, the weak housing market, and household deleveraging. In assessing the economic outlook, participants judged that strains in global financial markets continued to pose significant downside risks.

Fed to Publish a Forecast of Rate Moves, Guiding Investors — The Federal Reserve will begin later this month to publish the predictions of its senior officials about their own decisions, hoping to increase its influence over economic activity by guiding investor expectations. The change was approved at the most recent meeting of the Fed’s policy-making committee, in December, but was kept secret until Tuesday afternoon, when the Fed released an account of the meeting after a standard three-week delay. The inaugural forecast, set for Jan. 25, will show the range of predictions made by Fed officials about the level of short-term interest rates in the fourth quarter of 2012, 2013 and 2014, although it will not list individual predictions. It also will summarize when they expect to start raising short-term rates, which they have held near zero since late 2008. And it will describe their plans for the Fed’s investment portfolio. According to the meeting minutes, “a number of members” of the 10-person committee “indicated that current and prospective economic conditions could well warrant additional policy accommodation, but they believed that any additional actions would be more effective if accompanied by enhanced communication.”

Fed Announcement on Communications Shift -- The minutes from the latest Federal Reserve meeting included an announcement about a shift in the central bank’s communications strategy. This is the relevant section of the release.

FOMC Decides to Focus on the Rudder, Not the Destination - The FOMC minutes from the December meeting reveal that starting this month the Fed will start publishing conditional long-term forecasts for the federal funds rate in its Summary of Economic Projections (SEP): At the conclusion of their discussion, participants decided to incorporate information about their projections of appropriate monetary policy into the SEP beginning in January. Specifically, the SEP will include information about participants' projections of the appropriate level of the target federal funds rate in the fourth quarter of the current year and the next few calendar years, and over the longer run; the SEP also will report participants' current projections of the likely timing of the first increase in the target rate given their projections of future economic conditions. So what to make of this new policy? One view is that it provides more certainty about the future path of the target policy interest rate. Consequently, it would easier to make long-term investment decisions and that added certainty by itself might add some stimulus to the economy. The long-term forecast could also be used as a back-door way to provide more monetary stimulus to the economy. The Fed could do this by lowering its long-term forecast of the target federal funds rate which could be interpreted as indicating greater than expected monetary stimulus in the future. This, in turn, would improve the economic outlook and thereby encourage households and firms to increase their spending today. In short, a lower forecast of the future target federal funds rates could raise current aggregate demand.

Confused about Communication about Improving Communication - Apparently the Fed do a poor job of communicating its new communications policy. David Altig tries to clear things up: In the interest of precision, by David Altig: As you may have heard, the minutes of the December 13 meeting of the Federal Open Market Committee (FOMC) contained the news that, starting with this month's meeting, committee members will be jointly publishing not only their personal projections for gross domestic product growth, unemployment, and inflation, but also the monetary policy assumptions that underlie those forecasts. In an article published earlier this week, the enhancement to these projections, known as the Summary of Economic Projections (SEP), was described in the Wall Street Journal this way (with my emphasis added): "Federal Reserve officials this month will begin detailing their plans for short-term interest rates, a move that could show that the central bank's easy-money policies will remain in place for years and give the economy a boost."I added the emphasis in both of those passages because I think the highlighted language isn't quite right. ... The minutes are pretty clear about what this information is intended to convey… and what it is not intended to convey (here too, emphasis added):...The broader point is that the new information in the SEPs, according to the minutes, is not intended to be a device for signaling the policy path that the FOMC, by official vote, intends to pursue.

Fed Watch: Still Cautious Heading Into 2012 - I have been hesitant to embrace the recent positive data flow - once bitten, twice shy perhaps. Something about the current dynamics that seems a little too familiar. Indeed, I felt something of relief when FT Alphaville came to a similar conclusion in the waning days of 2011. Cardiff Garcia reports on a Nomura research note that details a new bias in the seasonal adjustment process, noting: Up next, writes Nomura, you can expect exaggeratedly strong readings from the Chicago PMI later this month and the next ISM manufacturing survey at the start of January. I imagine it is premature to call the readings "exaggerated," but both did surprise on the upside, as much data has of late. Read the whole piece - it is worth the time. It seems reasonable to expect, at least as a baseline - a slow "recovery" that is really more of an adjustment to what appears to be the economy's new equilibrium path, one that is decisively subpar to the pre-recession trend. I don't believe that such an adjustment is necessary, as in my view it simply reflects a shortfall of aggregate demand. That said, the longer the cyclical downturn grinds on, the more likely it is that we will indeed see a new equilibrium path. A greater percentage of the cyclical unemployment will become structural unemployment or permanent shifts in the labor force participation rate. In addition, investments will go unmade as firms hoard cash. And, increasingly, policymakers will manage policy along the new equilibrium path, forgetting entirely the pre-recession path.

Latest Fed Transparency Move Draws Mixed Response - The Federal Reserve‘s latest move to open up the policy-making process is getting mixed reviews from economists, who are struggling to make sense of what the central bank is in fact planning to do, as well as what it can accomplish. On Tuesday, the minutes from the Fed’s December monetary policy meeting said the institution will now release its projections of its overnight fed-funds target rate, the traditional focal point of policy making. The forecasts will be made available four times a year, beginning with the Federal Open Market Committee meeting scheduled for the end of the month. The interest-rate outlook will join the projections of GDP, inflation and unemployment the Fed already releases.

Fed Primary-Dealer Survey Predicts Rate Increase in Second Quarter of 2014 - The Federal Reserve Bank of New York’s survey of primary dealers conducted before policy makers’ Dec. 13 meeting showed the firms expected the Fed to raise its benchmark interest rate during the second quarter of 2014. Respondents saw a 45 percent chance the first rate increase would occur in the second quarter of 2014 or later, according to the results posted today on the New York Fed’s website. The median among the predictions for the timing of the first increase was the second quarter of 2014, the bank said in a statement. The Fed has kept its benchmark interest rate near zero since December 2008. The December survey asked primary dealers the probability that central bankers would make changes to their public communications within the next year. Fed officials decided at the last meeting of the Federal Open Market Committee to start publishing their own forecasts for the central bank’s key interest rate, according to minutes of the gathering released yesterday. “While most dealers did not expect any policy changes at the December meeting, some suggested the FOMC could change its communication strategy, and a few saw a change in the guidance on the future path of the federal funds rate as likely,”

Large Banks Uncertain about Economy, Certain about QE3 - Fed - Some of the nation's most influential financial institutions might not know what U.S. GDP growth, inflation and employment data will look like in 2012, but they do know this: no matter what, the Federal Reserve will be there to keep pumping trillions into the world's financial system. A survey of primary dealers conducted by the Federal Reserve Bank of New York -- and released to the public Wednesday -- showed a great deal of uncertainty among the 21 large banks that act as counterparties to the Fed's open market transactions, with the survey noting the firms largely admitted their predictions for GDP growth, inflation and the unemployment rate in 2012 were slightly on the optimistic side. But by the same token, firms were nearly unanimous in believing the U.S. central bank's accommodative zero-interest rate monetary policy would last for at least 30 more months. Furthermore, the survey showed a strong belief that a new round of quantitative easing - the central bank's practice of flooding the financial system with cash by buying up illiquid securities - would occur within the year: the median view held the possibility of this happening in the next 12 months was 60 percent.

Here Is The Real Biggest News Out Of The FOMC Today - The biggest FOMC news released today was not the December minutes - there was absolutely no surprise there. The biggest news, by far, is that as we wrote a few weeks ago, the composition of the FOMC voting members changes drastically as of January 1, with Hawks Fisher, Kocherlakota and Plosser now out of the voting rotation, and replacing them will be the gaggle of ferocious doves Pianalto, Lockhart and Williams. In fact the only hawk left in the Fed as of today through the end of the year is Richmond Fed's Jeffrey Lacker who has shown substantial dovishness in the past. In other words, from a rotation of 7 and 3, the Fed is now uber-dovish by a 9 to 1 majority. So does this mean that printing is imminent? Stay tuned and find out in 3 short weeks: the January FOMC statement comes out on January 25. The only good news: Charles "the fire hydrant" Evans is finally out.

NY Fed to Release Advisory Panel Agendas, Minutes - Capping a week in which various parts of the central bank either announced or followed through on new efforts to disclose information, the Federal Reserve Bank of New York took another step along that path Thursday. The central bank’s most important regional arm announced it will start releasing agendas and meeting minutes from the host of advisory groups associated with the New York Fed. A number of those panels have little relationship to financial markets. But the ones that do include economic and monetary policy groups, as well as the Foreign Exchange Committee and others related to the plumbing of bond markets and the payment system. There could be a lot for Fed watchers to digest.

The Fed and Forward Guidance - The news from the December 13 FOMC minutes is in the very last part, following the policy decision, and relates to "forward guidance," i.e. information that comes from the FOMC about the future path for policy instruments. Here's the relevant passage in the minutes: After the Committee's vote, participants turned to a further consideration of ways in which the Committee might enhance the clarity and transparency of its public communications. The subcommittee on communications recommended an approach for incorporating information about participants' projections of appropriate future monetary policy into the Summary of Economic Projections (SEP), which the FOMC releases four times each year. In the SEP, participants' projections for economic growth, unemployment, and inflation are conditioned on their individual assessments of the path of monetary policy that is most likely to be consistent with the Federal Reserve's statutory mandate to promote maximum employment and price stability, but information about those assessments has not been included in the SEP....Following up on the Committee's discussion of policy frameworks at its November meeting, the subcommittee on communications presented a draft statement of the Committee's longer-run goals and policy strategy. Participants generally agreed that issuing such a statement could be helpful in enhancing the transparency and accountability of monetary policy and in facilitating well-informed decisionmaking by households and businesses, and thus in enhancing the Committee's ability to promote the goals specified in its statutory mandate in the face of significant economic disturbances.

Small and Large Footprints: Reserves and the Fed - As most economists are well aware, financial institutions in the United States currently hold a very large stock of reserves - deposit accounts with the Fed. The first chart shows the stock of reserves for the last five years. Before the financial crisis, the primary role of reserves was as a means of payment among large financial institutions. Commercial banks of course have to fulfill reserve requirements, but given financial innovation that allows banks to essentially bypass the requirements, it is most useful to think of reserve requirements as irrelevant in the United States. Pre-financial crisis, a stock of $5 billion to $20 billion in reserves was sufficient to support all intraday financial payments and settlement in the United States. It is important to note that this small quantity of reserves was funding a huge quantity of daily payments. Indeed, in 2008, the average daily value of transactions on Fedwire (using reserves) was $2.7 trillion, so the intraday velocity of reserves is immense. Since the financial crisis, as can be seen in the chart, reserves have grown to the neighborhood of $1.6 trillion - more than 100 times the typical stock of reserves in the pre-crisis period. What implications does this have? The typical view was that we were in the middle of unusual circumstances requiring unusual monetary policy interventions, but that these interventions would eventually be unwound.

Central banks: Crazy aunt on the loose - THERE was a time when the Federal Reserve wouldn’t say whether it had changed interest rates. Soon it will say where it thinks rates will be years from now. Beginning with its policy meeting on January 24th-25th, Fed officials will disclose when they expect to start raising their short-term interest-rate target, which is at near-zero now, and what they expect its path to be over the coming years. Behind such radical transparency is a grim fact: at the start of a fourth successive year of extraordinarily low short-term rates and a still-moribund economy, the Fed is desperate for new ways to stimulate demand. It is not alone. Of the rich world’s four major central banks, Britain’s and Japan’s already have their policy rates stuck near zero and the fourth, the European Central Bank (ECB), is likely to get there this year. Meanwhile, the balance-sheets of all four institutions have ballooned as they expand the volume and range of assets and loans they hold (see charts). Central banks have never been comfortable with unconventional monetary policies such as verbal interest-rate commitments and quantitative easing (QE), the purchase of assets by printing money. QE is “best kept in the locker marked ‘For Emergency Use Only’”, is how Charlie Bean, the Bank of England’s deputy governor, put it in 2010.

Question for Market Monetarists and MMTers: What Happens if IOR Goes to Zero? - For the non-cognoscenti: "IOR" is interest on reserves. Banks keep money in their accounts at the Fed. In October, 2008 the Fed started paying .25% interest on those accounts. The Fed's also engaged in "quantitative easing," a.k.a. open-market purchases on steroids, creating new money and using it to buy $1.6 trillion dollars worth of bonds from banks. The money is deposited in banks' reserve accounts. The result: banks have $1.6 trillion dollars in excess reserves (in excess of what they're required to hold) sitting in their accounts at the Fed. This is the heart of the "pushing on a string" argument -- giving the banks more reserves (making their holdings more "liquid") doesn't (necessarily) increase real-economy transaction volumes (on consumption or investment), either directly through spending by the banks or via bank loans to people and businesses who will spend it. This $1.6 trillion in new money issued by the Fed is effectively stuffed in an electronic mattress. So I'm curious what would happen if the Fed no longer paid IOR. I asked Scott Sumner this a while back: He gave a somewhat less than satisfactory answer: The IOR question is a good one, and at the risk of being annoying I’m going to slightly dodge the question. I do think it would be expansionary, but it’s hard to know how much, because it’s almost inconceivable to me that it would be done by itself, without any other policy changes. It could be slightly expansionary, or if accompanied by other moves, wildly expansionary.

Fed Secretly Bailing Out Europe - Former Vice President of the Federal Reserve bank of Dallas, Gerald ODriscoll, says that the Fed is secretly bailing out Europe: O’Driscoll wrote in a Wall Street Journal editorial: America’s central bank, the Federal Reserve, is engaged in a bailout of European banks. Surprisingly, its operation is largely unnoticed here. The Fed is using what is termed a “temporary U.S. dollar liquidity swap arrangement” with the European Central Bank (ECB). There are similar arrangements with the central banks of Canada, England, Switzerland and Japan. Simply put, the Fed trades or “swaps” dollars for euros. The Fed is compensated by payment of an interest rate (currently 50 basis points, or one-half of 1%) above the overnight index swap rate. The ECB, which guarantees to return the dollars at an exchange rate fixed at the time the original swap is made, then lends the dollars to European banks of its choosing.The two central banks are engaging in this roundabout procedure because each needs a fig leaf. The Fed was embarrassed by the revelations of its prior largess with foreign banks. It does not want the debt of foreign banks on its books. A currency swap with the ECB is not technically a loan.

ECB/Fed Support for the European Banking System – 750 billion USD, and counting - One point that I have been shouting from the proverbial roof tops in my research, to partners and colleagues is that 2012 may well be the year when all major central banks will be conducting both conventional and unconventional monetary easing at the same time. I think this is a very strong testament not only to the severity of the ongoing debt crisis in the developed world, but also to the propensity of central banks to choose inflation as the desired route to recovery. We need not initially discuss whether they are deploying the proper set of policies or even whether such policies represent moral hazard or a Ponzi scheme on government debt. The main thing is to realise that this is an unprecedented global monetary experiment. My message to investors in 2012 would then be not to underestimate this inflation bias by part of global central banks. Inflating your way out of too much debt won’t work in the long run without considerable defaults and/or economic stress (hyper inflation). Events since 2008 are ample evidence of this, but the simultaneous inclination to create inflation and debase your currency (to generate more inflation and exports) by all major central banks will continue to exert a profound effect on asset prices and the global economy.

Presenting The Exchange Stabilization Fund In 5 Parts: Is This The Real "Plunge Protection Team"? - When it comes to the fabled President's Working Group on Capital Markets, also known as the Plunge Protection Team, the myths about the subject are certainly far greater than any underlying reality. To be sure, vast amounts of popular folkflore has been expounded into the public arena, with most of it being shot down simply due to it assuming conspiracy theories of such vast scale that the human mind is unable to grasp the complexity, and ultimately the inverse Gordian Knot makes an appearance with the claim that vast conspiracies are largely untenable simply because it is impossible to keep a secret from so many people for so long. Yet what if the secret is not a secret at all but is fully out in the open, and is only a matter of interpretation, and contextualizing? Why just 3 years ago it would appear preposterous to allege the capital markets are a ponzi and that the Fed does everything in its power to keep stocks higher. Well, what a difference three years make: now the Chairman himself in a Washington Post OpEd has admitted that the sole gauge of Fed success is the loftiness of the Russell 2000, neither unemployment nor inflation really matter now that the Fed's third mandate has been fully whipped out. Furthermore, Keynesian economics, and the entire top echelon of the educational system have also been accurately represented as a paradigm which merely perpetuates the status quo as the alternative is the realization that the whole system is a house of cards. As for the global capital markets being nothing short of a ponzi, we merely point you to the general direction of Europe, the ECB and the continent's banks, where the monetary interplay is nothing short of the world's biggest pyramid scheme.

Bernanke Tells Lawmakers More Action Needed to Fix Housing - The U.S. Federal Reserve on Wednesday called for more action to stabilize the nation’s ailing housing market, warning that failure to do so could harm the broader economy. In a 26-page white paper sent to Congress, the Fed outlined several potential ways to stabilize the housing market, many of which are already under discussion or being implemented by the Obama administration and housing regulators. “Restoring the health of the housing market is a necessary part of a broader strategy for economic recovery,” Bernanke said in a letter to the top lawmakers on the Senate Banking and House Financial Services committees. The paper noted “there is unfortunately no single solution for the problems the housing market faces,” as tight standards for mortgage lending, a 33% decline in home prices since 2007 and a huge number of vacant foreclosed homes on the market make it hard for the housing market to recover. “Continued weakness in the housing market poses a significant barrier to a more vigorous economic recovery,” the paper said. Without action, the paper warned, “the adjustment process will take longer and incur more deadweight losses, pushing house prices lower and thereby prolonging the downward pressure on the wealth of current homeowners and the resultant drag on the economy at large.”

Fed’s Dudley: Housing and Monetary Policy Are Complements - In a speech calling for a host of policy actions to aid the housing market, a top Federal Reserve official also said Friday the central bank may have to provide more stimulus to help the economy. “Because the outlook for unemployment is unacceptably high relative to our dual mandate and the outlook for inflation is moderate, I believe it is also appropriate to continue to evaluate whether we could provide additional accommodation in a manner that produces more benefits than costs, regardless of whether action in housing is undertaken or not,” Federal Reserve Bank of New York President William Dudley said. He noted that as the Fed tries to aid the economy, and address the central role the weak housing market plays in impeding the recovery, the institution cannot go it alone. He said, “monetary policy and housing policy are much more complements than substitutes.”

Fed’s Bullard: Central Bank ‘Very Close’ to Adopting Inflation Target - The U.S. central bank may well get an inflation target this year, a top Federal Reserve official said Thursday. “We are very close” to tying monetary policy explicitly to some measure of overall inflation, Federal Reserve Bank of St. Louis president James Bullard said. He said the Fed may also be near making a collective statement about what level of unemployment is the natural rate, below which inflation pressures tend to rise. Bullard was interviewed Thursday on Bloomberg radio. The official isn’t currently a voting member of the monetary policy setting Federal Open Market Committee. Bullard has been skeptical of the need for additional stimulus for the economy, even as many in the markets believe the odds remain high the Fed will provide more stimulus at some point over the next year. He spoke in the wake of the release this week of the meeting minutes from the Fed’s December meeting. That document said that starting at the end of the month, the Fed will begin making public its forecasts of future Fed interest rate policy, joining the projections it already makes available on growth, employment and inflation.

Is Joblessness a Skills Problem or an FOMC Problem? - Among Lacker’s duties as President of Richmond Federal Reserve Bank is writing a message in the bank’s quarterly publication Region Focus, the third quarter edition of which I found in my mailbox yesterday. Knowing that Lacker has just become one of the most important people on the planet, I was curious to find out his thoughts at the start of his year on the FOMC. My reading of Lacker’s message in the second quarter Region Focus was not exactly an uplifting experience (see this post from October), but I try to look for glimmers of hope wherever I can find them. Sadly, Dr. Lacker’s message, entitled “Is Joblessness Now a Skills Problem?” offers nothing hopeful. Lacker begins by painting a bleak picture of the plight of the long-term unemployed. Today long-term unemployment – that is, unemployment lasting six months or longer – is at a record high. The share of unemployed Americans whose job searches have lasted this agonizingly long is 43.1 percent, a figure that is unprecedented since the Bureau of Labor Statistics began keeping records in 1948. His explanation? A growing number of observers have argued that this state of affairs is caused in significant part by a mismatch between available jobs and available workers, especially a mismatch in skills.

Senate Republicans Could Delay Fed Confirmations Over Recess Appointment Fight - President Barack Obama‘s contentious decision to use a recess appointment to install the first director of a new consumer financial agency could result in delays to Senate confirmations of two recently announced appointees to the Federal Reserve Board, two Senate Republican leadership aides said. A top GOP member of the Senate Banking Committee stopped short of saying he would personally block the confirmations of the two Fed nominees, but predicted there would be a Republican reaction to the move by Obama that could affect outstanding nominees. “Clearly, this is a very bold and extraordinary, unconstitutional move, and it’s going to provoke a reaction from Republican senators,” Sen. David Vitter (R., La.), who sits on the banking panel, said in an interview. “It brings up all sorts of possible reactions, including [delaying confirmation of] the nominations that may have otherwise have happened.”

How to Save the Global Economy: Whip Up Inflation. Now. Recovery from a debt crisis is always painfully slow, for reasons both economic and political. Creditors need to rebuild their balance sheets and are unwilling to make potentially risky loans. Debtors need to boost savings to cover their debts and are unwilling to resume spending. At the same time, debt-ridden countries collapse into political conflict over the question of who will pay to get them out of the red: Should it be taxpayers, bankers, public workers, or investors? A bit of inflation can help on all these fronts. So long as the debts are denominated in national currency and interest rates are kept low by monetary policy, inflation reduces the real debt burden. This is, to be sure, a forced restructuring that puts some of the onus on creditors -- but that is almost always the outcome of more explicit negotiations in any case. When most of the debts are household debts, as they are in the United States and parts of the eurozone, it is not really feasible to renegotiate millions of mortgages and consumer loans; inflation takes care of that for the whole economy. It mitigates some of the political conflict and lessens some of the economic burden.

A Call for Action: Conditional Inflation Targetting - Menzie Chinn - [We need] inflation -- just enough to reduce the debt burden to more manageable levels, which probably means in the 4 to 6 percent range for several years. The Fed could accomplish this by adopting a flexible inflation target, one pegged to the rate of unemployment. Chicago Fed President Charles Evans has proposed something very similar, a policy that would keep the Fed funds rate near zero and supplemented with other quantitative measures as long as unemployment remained above 7 percent or inflation stayed below 3 percent. Making the unemployment target explicit would also serve to constrain inflationary expectations: As the unemployment rate fell, the inflation target would fall with it.Today our highest priority should be to stimulate investment, growth, and employment. Raising the expected inflation rate will lower real interest rates and spur investment and consumption. It will also make it difficult for the de facto dollar peggers, such as China, to sustain their policies. The resulting real depreciation of the dollar would stimulate production of U.S. exports and domestic goods that compete with imports, boosting American production. The United States would get faster growth, an accelerated process of deleveraging, a quicker recovery, and a firmer foundation upon which to address long-term fiscal problems.

Menzie Chinn Explains it All for You: Demand Inflation Now! - Whether it's Market Monetarist NGDP targeting or Menzie's recommendation of Conditional Inflation Targeting with a notably higher target, everything tells us that somewhat higher inflation is the current path to greater and more widespread long-term prosperity. Raising the expected inflation rate will lower real interest rates and spur investment and consumption. It will also make it difficult for the de facto dollar peggers, such as China, to sustain their policies. The resulting real depreciation of the dollar would stimulate production of U.S. exports and domestic goods that compete with imports, boosting American production. The United States would get faster growth, an accelerated process of deleveraging, a quicker recovery, and a firmer foundation upon which to address long-term fiscal problems. Like the market monetarist approach, Chinn's proposal is basically for an automatic stabilizer based on unemployment levels, that anchors expectations:Making the unemployment target explicit would also serve to constrain inflationary expectations: As the unemployment rate fell, the inflation target would fall with it.As I said a while back: Automatic stabilizers are the key to effective 1) policy and 2) expectation-setting. Because 1) They happen, and 2) People know they’re gonna happen. In other words: Demand Inflation Now! Up the Real Economy

Looking Forward in the New Year: Crowding Out and Hyper-Inflation Watch - Menzie Chinn - In my previous post, I cited Jeff Frieden's and my proposal for a conditional inflation target. Yet, according to several observers, we are either on the brink of crowding out due to elevated government deficits [0], or high to hyperinflation, due to monetary base expansion [1]. As has been noted, none of these outcomes have yet materialized, despite months of such warnings. [2] [3] Here, I wanted to evaluate where market expectations stand on these views. As of December 28, constant maturity yields on five and ten year Treasury bills are at an all time (post-War) low. According to the Fisherian relationship, the nominal interest rate is the sum of the ex ante real interest rate and the expected inflation rate. What do real interest rates look like? One can proxy real interest rates by examining yields on Treasury inflation protected securities (TIPS).Well, it is likely that real interest rates would be lower in the presence of smaller deficits. However, with long term real interest rates negative (and persistently so for the bulk of 2011), it’s not clear that would be such a wonderful thing if lower deficits are associated with less economic activity.

Fractional Money Multipliers - Rebecca Wilder - Money multipliers – the stock of money divided by a measure of base money (generally reserves plus currency in circulation) – are dwindling to fractions of what they used to be. FT Alphaville draws our attention to this fact on the Euro area (EA) using SocGen’s analysis. The money multiplier is a representation of how much credit is leaving the banking system via lending and growth (or inflation) enhancing monetary activities. As FT Alphaville points out, the EA M3 multiplier is just over 3/4 its average 2007-2008 level, 7.67 vs 10. But this is global!. The US M2 money multiplier is a little over 2/5 the size of its average 2007-2008 level, 4.1 vs. 9.3. By this simple measure, I’d say that the US is in worse shape than is the EA. Of note, my visual is a bit different from that in FT Alphaville. Specifically, I don’t agree with SocGen’s estimates that the EA money multiplier drops in December to roughly 6. Given that December 2011 EA base money has been published, a 6.2 M3 multiplier implies that M3 dropped by 15% in 1 month. That’s unlikely.

Foreign central banks cut US treasuries - Holdings of US Treasuries by foreign central banks has fallen by a record amount over the past four weeks according to the latest Federal Reserve data. The net $69bn drop in Treasury holdings registered at the Fed by foreign official institutions comes as benchmark yields ended 2011 near record low levels and when the US central bank is conducting Operation Twist, its $400bn programme to sell shorter-lived Treasury bonds and buy those with longer maturities. The decline in foreign holdings of Treasuries in recent weeks has not resulted in higher yields and lower prices because other investors have sought the safety of US debt. “Given where the 10-year Treasury is ending the year, it’s difficult to say the flows are a bearish move,” . The yield on 10-year notes was set to end 2011 below 1.90 per cent on Friday and the Barclays Capital index of long-dated Treasuries has rallied nearly 30 per cent this year, its best annual performance since 1995. “While other buyers have willingly taken up the torch up to this point, it seems clear that this [foreign official flows] source of demand has waned since Operation Twist took yields to these levels and this investor base has little interest in sub-2 per cent 10-year yields,” .

Top 5 Economic Charts of 2011 - As the year draws to a close, Real Time Economics takes a look back at five of our favorite charts from the WallStreetJournal in 2011. These graphics look at the most recent year as well as the past to give us some insight into the future. Click on any image for larger version.

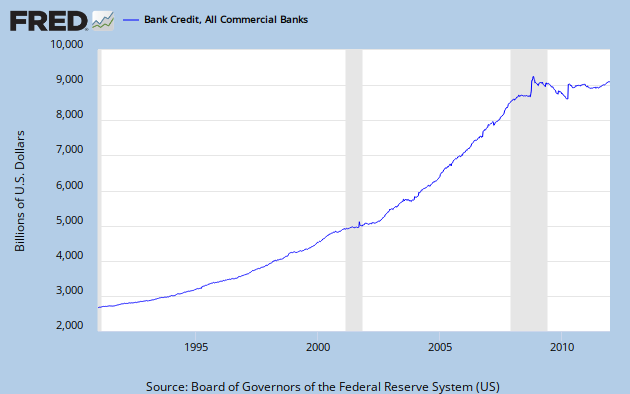

Smithianism and Its Discontents - Matt Yglesias pens an extremely readable version of the Smithian view on the near future of the US economy. What will this recovery look like in concrete terms? Total bank credit, which collapsed during the crisis, is growing again and will keep growing. That will make it easier for Americans to buy new cars and reverse the four years of growth in the average age of America’s passenger vehicles. Families will also invest in other kinds of durable goods—refrigerators, washing machines, etc.—that they’ve been hesitant to upgrade or replace. The housing bust, meanwhile, has been followed by an epic construction slump that’s actually left us with a shortage of homes. But every downward tick in the unemployment rate is another twentysomething moving out of his parents’ basement, stimulating a return to a more normal level of construction. Multifamily housing starts are already up 80 percent over the past year to accommodate the likely coming flood of renters, and there’ll be more to come once people have more cash in their pockets. Not everyone is convinced. Kelly Evans writes Along with nascent signs of recovery in the housing market, it is tempting to forget about 2011′s disappointments and think 2012 will be the year economists aimed not too high, but too low. Trouble is, recent history suggests it usually turns out the other way around.

I Just Got Here, but I Know Trouble When I See It — From 6 Economists, 6 Ways to Face 2012 : BELIEVE it or not, times are getting better. At least that’s what the dry statistics keep telling us. Industrial production, G.D.P.1 — the kind of figures that Washington and Wall Street sweat over — suggest that the economy is on the mend. Yet if we go beyond the Beltway and the Battery, to where most of American life is lived, the numbers don’t always add up. Yes, the Great Recession officially ended in 2009. But many millions of Americans are out of work or cannot find full-time jobs. Home prices are wobbly. The foreclosure crisis drags on. And the Occupy movement’s campaign against “the 1 percent” has underscored the ravages of income inequality2. It was, as always, a year of ups and downs in business. Washington said the nation’s AAA rating was safe, but Standard & Poor’s concluded that it wasn’t. Europe insisted that its currency was sound, but investors worry that it isn’t. Wall Street seemed perpetually on edge. After so many wild days, the American stock market ended 2011 about where it began. On this side of the Atlantic, aftershocks of the financial crisis of 2008-9 are still reverberating, though the worst has passed. Now, how Europe’s economic troubles play out may determine whether job growth here finally picks up enough to make up for all the lost ground — and whether that 401(k)3 is richer or poorer next Jan. 1.

In With The New: Part III of As Economic Growth Fails, How Do We Live? -- Part I of this series of three articles addressed the four major challenges we now face, there dubbed "The Four Horsemen of the Economic Apocalypse": 1) Too Much Debt; 2) Resource Limits; 3) Destruction and Decay of Infrastructure; and 4) Greed. Bottom line: this crisis is much deeper and more permanent than we've been led us to believe. "Recovery" to former patterns of growth simply won't happen. We must now adapt to new realities, as individuals and as a society. Part II of this series, "Out With The Old", discussed the end of seven "Dead End" unsustainable practices that will falter and decline. We won't pay our unpayable debts or keep impossible promises. We can't keep importing more than we export and borrowing the difference. Our Empire will shrink back. Our use of fossil fuels will decline as we experience Peak Oil and Peak Coal . We must cure Sick Care. We will repeal laws that mandate opulence and forbid prosperity. Finally, we will "drop the shopping" for worthless junk and refocus on the best of what it means to be human. In this third and final article in this series, we will discuss seven new ways of living which we can adopt as economic growth fails. They are not revolutionary (revolutions never achieve their utopian visions because of something called "human nature"). Rather, they may allow us to "muddle through" the best we can right now with what we already know how to do.

PIMCO Outlook - Towards the Paranormal - Bill Gross - How many ways can you say “it’s different this time?” There’s “abnormal,” “subnormal,” “paranormal” and of course “new normal.” Mohamed El-Erian’s awakening phrase of several years past has virtually been adopted into the lexicon these days, but now it has an almost antiquated vapor to it that reflected calmer seas in 2011 as opposed to the possibility of a perfect storm in 2012. The New Normal as PIMCO and other economists would describe it was a world of muted western growth, high unemployment and relatively orderly delevering. Now we appear to be morphing into a world with much fatter tails, bordering on bimodal. It’s as if the Earth now has two moons instead of one and both are growing in size like a cancerous tumor that may threaten the financial tides, oceans and economic life as we have known it for the past half century. Welcome to 2012.

Welcome to the Paranormal Economy: Why One Investor Says the ‘New Normal’ Is Over - Bill Gross, the prominent bond fund manager who is credited with popularizing the phrase a little more than two years ago, says he may be done using the term. What phrase does Gross prefer to describe the current state of our money affairs? The Paranormal economy. In a letter to investors that came out this week, Gross says we may be leaving The New Normal behind. Gross says he used The New Normal to describe the deleveraging, i.e. getting rid of our debts, that needed to go on in the aftermath of the financial crisis, and everything that went with it. For consumers, money that was going toward buying a new car or second house was now going to be used to pay down debt. So more frugal customers. Banks would make fewer loans, and less profit, because no one was going to trust borrowers again. Houses would lose their value, due to a lack of mortgages and a pile up of foreclosures as borrowers walked away from their home loans. Renting, too, would become part of The New Normal. So what makes Gross believe we are entering The Paranormal economy? Basically the fact that interest rates have remained low for such a long period of time, and it appears may stay that way for some time. And here comes the paranormal: Typically, low-interest rates spur more borrowing. But Gross says not so this time around. That’s because banks won’t want to make loans. Low-interest rates, not just for short-term loans but for ones that don’t have to be paid back for 5 or 10 years, will make lending unprofitable. It might make investing not all that attractive either. Why risk your money in the market when it’s not going to go anywhere.

GEAB N°60 is available! Global systemic crisis – USA 2012/2016: An insolvent and ungovernable country: As announced in previous GEABs, in this issue our team presents its anticipations on the changes in the United States for the period 2012-2016. This country, the epicentre of the global systemic crisis and pillar of the international system since 1945, will go through a particularly tragic in its history during these five years. Already insolvent it will become ungovernable bringing about, for Americans and those who depend on the United States violent and destructive economic, financial, monetary, geopolitical and social shocks. If the United States today is already very different from the "super-power" of 2006, the year the first GEAB was published, announcing the global systemic crisis and the end of the all-powerful US, the changes we anticipate for the 2012-2016 period are even more important, and will radically transform the country's institutional system, its social fabric and its economic and financial weight. In addition we also detail our recommendations on foreign currencies, gold, stock exchanges and the consequences of the United Kingdom’s marginalization within the EU (3) on the Pound, Gilts and UK debt and we set out some advice on developments of the American institutional system (4). In this public communiqué we have chosen to present an excerpt from our anticipation on the changes in the United States for the 2012-2016 period. But before addressing the American case, we wish to review the situation in Europe (5).

2012 Forecast: Bang and Whimper - On close examination, the industrial world underwent complete zombification in 2011. Its member states and their institutions are now lurching across the stage of history like so many walking dead. Whole European nations are dead, their citizens squirming around the ruined bones of failed speculative condo projects, housing estates, and luxury hotels like botfly larvae. The USA lies in complete moral ruin despite the exertions of ten thousand evangelical preachers in dusty back-road tilt-up chapels from Texas to Carolina, several new museums of Creation Science, and the shining example of former Senator Rick Santorum. Just look at how we behave, from the cloakrooms of Congress to the piercing parlors of West Hollywood to the 7-Elevens of suburban Maryland: a nation of thieves, racketeers, reality TV sluts, wannabe road warriors, light-fingered gangsta-boyz, and crybabies living in an anomie-drenched decrepitating demolition derby landscape of failure. When everybody is a zombie, whose brains are left to eat? Echo answers.... On to the predictions for 2012 then.

Goldman's Jim O'Neill: 'What Can Go Wrong, Will Go Wrong' - Jim O'Neill, Chairman of Goldman Sachs Asset Management, is out with his latest Viewpoints From The Office Of The Chairman letter. He published his 11 predictions for 2012 back in mid-December, but he spends nearly a third of his new note dwelling on 2011. To cover his bases, he points out a few things that could potentially go wrong this year. By definition, lots of things could go wrong, possibly including a fresh rise in crude oil prices, especially if Iran plans to cause a lot of fun and games early this year. Against this, and read Roger Altman in today’s London Financial Times for an up- to-date view, the energy supply response in recent months is probably still much stronger than many people realize. I suspect that, short of a major problem in the Gulf, this is an overhyped topic – yet again. As for Europe, I shall leave much of this until coming days and weeks as there is so much out there. Of things that really can go wrong, the Greek debt restructuring strikes me as one of the most likely. As for the coming downgrades, I am not sure they will really matter much, and I would certainly suggest the generosity of the ECB’s pre-holiday 3-year LTRO (Long Term Refinancing Operation) to be much more important in keeping things afloat. Plenty more on this topic to come. His note also discusses the recent positive global economic data and addresses a recent BRIC paper authored by Goldman's Dominic Wilson. You can read his whole letter at GSAM.

Euro Zone Isn’t Only Potential 2012 Boogey Man - For those obsessed with the euro-zone debt crisis and its impact on 2012, keep this in mind: so much else could go wrong. Here are three more to add to the list. First, U.S. consumers pull back again. U.S. households have been resilient which has lifted global producers. But future spending will depend on better job growth and incomes growing ahead of prices. If payroll gains disappoint, or energy or food costs spike again, then consumers will have to pull back on other spending. Slower demand will not only hurt U.S. companies, but also fall back on foreign producers who count America as their biggest market. Second, a U.S.-China trade war breaks out. China has slowed down. If growth drops more than expected and social unrest increases, Beijing might react by blaming U.S. regulations for the loss of work. Trade skirmishes are bad anytime, but they will be more dangerous in a year when Washington politicians will want to look tough on China. A full-blown trade war also risks higher U.S. interest rates if China slows its purchases of Treasury debt. Last but not least, fiscal policy blunders big-time. Never underestimate the ability of Washington to screw up the economy if political points can be scored.

2012 As 1937 Redux? - Why, with all the talk of America's need to get its spending under control, would radical austerity be a problem? The answer can be structured in many ways, but today we'll go with a historical lesson, circa 1937. Back in 1937, the deleveraging process was even longer and harder in every measure than it is today. By 1937, modest growth had returned, and while unemployment remained stubbornly high at just under 10 percent, that was down from a peak in 1932-33 of 25 percent. At this point, both the Fed and the Roosevelt administration—giving in to orthodoxies that still haunt US economic thought—made terrible, independent errors. FDR acceded to Treasury advisors who declared the recovery self-sustaining and pushed for spending cuts. FDR, by now in complete control of the congressional agenda after a landslide reelection in 1936, duly cut government spending by 10 percent in an effort to balance the federal budget. The Federal Reserve, meanwhile, had been rattled by recent gyrations in commodity prices, particularly in corn and wheat—crops devastated by the Midwestern Dust Bowl. Acting to tame what it saw as the threat of hyperinflation, the Fed raised interest rates sharply. Various economic schools assign different weight to these two decisions, but the overall math is devastatingly clear. By 1938, joblessness had shot back toward 15 percent, industrial production fell by 37 percent, and the worst double dip in US history had begun.

The Peltzman Effect: Why Economic Growth Has Slowed in the US Over Time - In recent years, there have been a number of studies showing that generational income mobility is particularly low in the US. To quote this 2006 study by Tom Hertz: By international standards, the United States has an unusually low level of intergenerational mobility: our parents’ income is highly predictive of our incomes as adults. Intergenerational mobility in the United States is lower than in France, Germany, Sweden, Canada, Finland, Norway and Denmark. Among high-income countries for which comparable estimates are available, only the United Kingdom had a lower rate of mobility than the United States. Hertz provides this handy chart: Most of the "big government" countries that compare favorably with the US on intergenerational mobility also do pretty well on measures of entrepreneurship. The following snapshot comes from this paper by Acs and Szerb: While studies are, no doubt, imperfect, I've seen similar results before and they seem credible to me. The studies note, essentially, that the US is not, for many, the land of opportunity it is touted to be, and is now being beaten out by countries like Denmark and Canada. Big government countries, countries where Americans seem to believe people aren't motivated to get off their duff, are actually quite entrepreneurial and offer offer their citizens a lot of opportunity.

First Core Dump of 2012 - Auto Sales Seem to have ended the year strong but not quite as strong as I might have thought. I was looking for continued gain, up to 13.8M SAAR or so and it doesn’t look like we will see that. Construction ended the year completely as expected, up slightly mainly on residential multifamily. Public construction seems to have stopped falling and this is consistent with my view going forward. We should see sales tax receipts improve for state and local governments and with that a willingness to fund more projects. Non-residential construction will probably continue to be driven by oil exploration well into 2012. The office market just doesn’t feel ready to come back. Though we might see increased hospital construction. I would have to look more into that. Oil: Kevin Drum makes the point that the global economy is energy constrained. I think that is correct and it underlies some of views about US energy policy. I don’t think we are likely to see “many" wild swings in oil prices, though. Such swings generate a huge arbitrage opportunity. To take advantage of it what you need is a place to store excess capacity. Oil – being the accommodating resource that it is – provides that naturally. We call it the ground.

US economic data sees ‘reversion to mean’ - From a Europe mired in an unresolved sovereign debt crisis and in the midst of trying to recapitalise its banking sector, all this positive US economic data is frankly just irritating. In fact it’s been so good in terms of positive employment and manufacturing metrics that the Rates & Currencies team at BofAML published a piece entitled “The USA a safe haven again” with this line in it: In the US, the correlation between strong data and the USD has flipped, where now positive US data surprises are good for the USD given European concerns. Flipping the correlation around?! All sorts of strategies break when people make ridiculous assumptions and bake them into models that happens. But anyway, the Economics team at BofAML have a few reasons why you should think twice before boarding the optimism train. First, from a note published on Thursday: With economic shocks from Japan’s tsunami and the Arab spring fading alongside a modest abatement of the uncertainty from Europe and the US, businesses have increased hiring to meet the underlying pick-up in final demand. The confluence of the employment data released for December – better ISM, stronger confidence, lower jobless claims, and better than expected ADP – is consistent with a steady improvement in the labor market… In other words, think more “recovery from shocks”, and add to that the easing off from the higher commodity prices seen at the beginning of 2011.

As Good as It Gets for the Economy? - The economy was weak in 2011, but it ended better than it started, with growth up from its lows and unemployment down from its highs. The question now is whether that progress will continue into 2012. We wish we could say yes, but unless policy makers are incredibly lucky or remarkably adept — certainly not the description that comes to mind when thinking of, say, Congress — the answer is no. When data is released later this month, economists expect growth of around 3 percent for the last quarter of 2011, compared with 1.2 percent on average in the first three quarters. But there is little in the latest growth spurt to signal a self-reinforcing recovery going forward. Holiday shoppers had more cash to spend because of the decline in oil prices, not a rise in wages. A drop in the jobless rate was driven by a mix of new hiring and a large number of potential workers who gave up futile job searches. Signs of life in the housing market, including more sales, were dampened by falling prices as foreclosures continued. The way to revive sustainable growth is with more government aid to help create jobs, support demand and prevent foreclosures. As things stand now, however, Washington will provide less help, not more, in 2012.

The decline of the American empire - The US has the world's biggest economy, the most influential culture, and the most potent military machine, with a budget that equals that of all other nations combined. It is the only power with a global project defended and supported by more aircraft carriers, Fortune 500 companies, and more successful media-tainment conglomerates than any other. But the last decade has been problematic for the world's only superpower. America's post-Cold War optimism has given way to pessimism, forecasting a declining power and more crucially, the end of "the American era". The rise of new regional and global powers, coupled with Washington's recent war fiascos and financial crisis have worsened the outlook for the future of the US.

Leading Indicators Index Gets Overhaul - Private research group the Conference Board said Thursday that it’s putting in place some major changes in how it compiles a closely watched report that seeks to provide clues to the economy’s future direction. The release in question is the long-running monthly index of Leading Economic Indicators, which is getting its first big overhaul since 1996. The index is made up of a mix of already-announced statistics, and in a bid to make the report more reliable, the Conference Board is swapping out some of the old components and replacing them with new data points. The changes take effect in the report scheduled for release Jan. 26. “These adjustments have been designed to make the U.S. Leading Economic Index an even stronger predictor of peaks and troughs in the business cycle, while recognizing changes in the functioning and drivers of the economy in the short and medium term,” Conference Board chief economist Bart van Ark said in a press release. The firm said it will remove the M2 money supply measure and replace it with something entirely new, which it dubbed the “Leading Credit Index.” The Conference Board said the Leading Credit Index is made up financial market indicators including bond market yield curve data, interest rate swaps and data extracted from a periodic Federal Reserve survey of bank lending.

Tim Duy on the Output Gap - He writes The trend of nondruable goods spending is tracking the pre-recession trend. So, at this point, we are seeing overall consumption supported by a rebound in durable goods spending that offsets a deterioration in the path of spending on services. The bounce in durable goods spending will come to an end at some point, as 16 million units is likely an upper bound for auto sales. Will service spending accelerate to compensate? Or will we see a new normal, with a constrained consumer spending at a path and rate below those prior to the recession? But that still is not a story that rapidly returns the economy to potential output. These are the trends but I don’t know exactly what to make of them. For one, looking at PCE services is a nightmare because so much is housing, finance and medical care. Most of which consumers do not pay for directly and none of which is chosen on a month-by-month basis. The larger issue though has to do with why we think the economy is depressed. If you think that practically speaking the nominal interest rate is too high then is hard to see a world where autos come back to 16 million units, construction comes back to 1 million units and the economy, the Fed is accommodative and the economy is not booming.

Let's Build a Second Measure of Economic Strength - Here's a tale of two equations that represent human exchange. The first is the standard macroeconomist's recipe for an economy: Y = C+G+I+NX. It says: output equals consumption, plus government expenditure, plus investment, plus net exports. Now here's a crude approximation of what eudaimonia might look like: W = N+F+I+H+S+E+O. It says: real human welfare equals natural capital, plus financial capital, plus intellectual capital, plus human capital, plus social, emotional, and organizational capital. Not all these kinds of wealth are created equal; I'd suggest that higher-order wealth, to the right, is scarcer, stickier, more enduring, and more productive. The first equation might be said to neatly represent the industrial-age paradigm of business: the implicit question it answers is maximizing the volume of output or "product." But the second answers a very different question. It's our economy's real balance sheet.

Global financial fiasco: End of the age of US economic dominance - In the spring of 2008, the real estate bubble popped in the United States and it triggered a financial tsunami that engulfed the entire globe. This catastrophe provided an opportunity for change, change that was necessary to restructure the economic architecture of the US Despite the hefty promises made by President Obama during his election campaign, upon taking office he did the complete opposite of what was expected, or to be precise, hoped for, and succumbed, as his predecessors did, to the same interests that were responsible for the catastrophe. Instead of seizing the opportunity, all policies implemented after 2008, were geared towards maintaining the status quo. These polices have exacerbated the magnitude of a crisis that will take effect anytime after 2012.After the 1907 panic, influential bankers agreed to establish the Federal Reserve by 1914. The Fed is a “private” central bank that controls U.S monetary policy, acts as the lender of last resort and its shareholders consists of corporate banks. In addition, it is excluded from independent audits and congressional oversight. The monetary policy of the Fed is the core factor why the US economy is currently on an unsustainable path.

New Asian Union Means The Fall Of The Dollar - One of the most frustrating issues to haunt the halls of alternative economic analysis is the threat of misrepresentative terminology. For instance, when the U.S. government decided to back the private Federal Reserve in lowering the interest rates on lending windows to European banks last month, they did not call this a bailout, even though that’s exactly what it was. The chain of financial events taking place over the past decade in Asia have been correspondingly mislabeled and misunderstood. What some economists see as total collapse is actually a new and decidedly prophetic (or engineered) transition. What some naively see as the “natural” progression of globalism, is actually a distinctly deliberate program of centralization meant to further the goals of world economic and political totalitarianism. Asia, and most especially China, is a Petri dish for elitist psychopaths. What we see as suffocating collectivism in this region of the world today is the exact social schematic intended for the West tomorrow. Call it whatever you will, but on the other side of the Pacific, like the eerie smile of a sinister clown, sits fabricated fate.

Euro could become world's leading currency: Noyer (Reuters) - The euro could become the world's leading currency in the next decade if leaders of the single-currency bloc succeed in tightening fiscal integration, European Central Bank policymaker Christian Noyer said in an article to be published in the Journal du Dimanche. European leaders struck a historic deal at an emergency summit in Brussels on December 9 to draft a new treaty for deeper economic union, in an attempt to stem the debt crisis that is threatening to cause the collapse of the single currency. The news temporarily calmed markets. But concerns quickly resurfaced as the final details of the agreement have yet to be determined and a new treaty could take up to three months to negotiate. Ratings agency Fitch has said it doubts a comprehensive solution to the crisis can be found and urged more decisive action from the ECB. "If we implement all the decisions taken at the Brussels summit we will emerge stronger," Noyer said in the article, due to be published to coincide with the 10-year anniversary of the euro on January 1.

Dream of Universal Currency Just Won't Die - The euro zone maelstrom refuses to end. Thanks to the debt crisis, some Greek officials are contemplating dumping the common currency for the drachma. Meanwhile, Italy and Spain teeter. A decade after the shared currency was heralded as a 21st-century tool for peace and prosperity, it turns out that currency unions aren’t such a hot idea. Not so fast, though. This is undeniably a period of epic turmoil, and many economists will tell you that sovereign states need sovereign currencies—full stop. But this notion ignores a fundamental truth: Countries with their own currency may have monetary independence, but in reality—as gun battles in Libya, CDOs in the US, and tsunamis in Japan have taught us—we are only becoming more economically intertwined, regardless of what our coins look like. Step back from the current crisis to consider the long view, and currency unions—or even a single global currency—have a fair share of appeal. A universal medium of exchange could eliminate currency risk and jack up trade. It would mean speculators couldn’t short an individual country’s currency. Exporters wouldn’t have to fret over the gap between a price on a contract and the value of the payment. A single currency could halt spastic swings in prices and end conversion fees, leaving more of the pie for little stuff like R&D and employee health insurance. Oh—and it could put an end to international disputes over currency manipulation. Hello? China?

Dollar’s Demise Exaggerated as 13% Gain Since 2008 Proves Currency’s Value - Moves by the Federal Reserve to flood the world with dollars are doing little to dent the currency’s value, bolstering the appeal of U.S. assets at a time when the government needs the support of foreign investors the most. The U.S. Dollar Index (DXY) has appreciated 13 percent from a record low in March 2008 even as the Fed kept interest rates at about zero and printed cash to buy $2.3 trillion of Treasury and mortgage-related bonds, and is little changed since 1991. The International Monetary Fund said Dec. 30 that the greenback’s share of global foreign-exchange reserves rose in the third quarter by the most since 2008. That long-term stability shows America’s currency is a store of value and may help explain why the U.S. is attracting record demand for the unprecedented amount of bonds the Treasury Department is selling to finance a budget deficit exceeding $1 trillion. Even though Standard & Poor’s stripped the U.S. of its AAA rating in August, investors see the nation as a refuge from slower global economic growth and Europe’s sovereign-debt crisis. “The safe-haven function of the dollar is still alive,” “The dollar will be strong in 2012,”

U.S. Dollar & Currencies: Review and Outlook - In 2012, policy makers around the world may be driven by the realization that the theme of 2011 was not a Euro-specific crisis, but simply another stage in a global financial crisis. Central bankers may ramp up their printing presses in an effort to limit “contagion” concerns. As such, the currency markets may be the purest way to take a view on the “mania” of policy makers. Market movements may continue to be largely driven by political rhetoric, rather than company earnings announcements or economic data. We don’t believe this trend will abate over the foreseeable future, especially given the likely leadership changes throughout several G-7 nations. The primary motivating force behind politicians’ decision-making may be quite different, and more often than not, at odds with those of the broader market or sound economic fundamentals. Moreover, we have witnessed an unprecedented period of political posturing and increased polarization of views. This has only served to underpin the increased levels of market volatility experienced in 2011. Central banks of the U.S., Japan and the U.K. have shown they are most willing to put in place expansionary policies. For one, there will be a more dovish composition of Federal Open Market Committee (FOMC) voting members in 2012. Many Western and Asian policy makers have already begun to ease. From a currency perspective, we believe these dynamics will serve to benefit the currencies of commodity producing nations, while underpinning Asian economic growth.

What Is a Safe Asset? - Rebecca Wilder - Last month, David Beckworth at Macro and Other Market Musings had some interesting thoughts on the global shortage of safe assets. His essay got me thinking about what is a safe asset? Beckworth alludes to three definitions of ‘safe’: (1) a credit being AAA-rated, (2) satisfying a certain level of liquidity to be used in repo markets (an important aspect of US credit transactions), and (3) backed by a sovereign with sufficient (and targeted) aggregate nominal income. I would agree with (2) and (3) in a broader context, but not necessarily (1). Why does a ‘safe’ asset need to be AAA? To be sure, the share of AAA sovereigns of 76 developed and developing/emerging sovereigns fell by 3% in 2011 compared to 2007. This should hardly be surprising, given the weak recoveries and leverage that exists in the developed markets. But it’s liquidity, and to a lesser extent, sovereign risk that matters, not the rating, per se. Furthermore, ‘safe’ is a matter of perspective. Liquidity is a pre-requisite for a ‘safe asset’ so that investors can purchase this asset in even the harshest of times. The United States runs the most liquid bond and currency market in the world; it can satisfy demand from flight-to-safety in times of stress. But one can think of liquidity in another manner: the ability to print fiat currency that is used to honor the debt instrument (asset). The US government issued just 8% of its external government debt position in non-dollar form. Better put: the US is a ‘safe’ assets because it’s a market large enough to satisfy broad demand and the US government is always going to be able to honor its debts. Liquidity is the most important definition of a safe asset, rather than the rating.

Peak Money Arrives - The world is running out of money. If money is credit, and credit relies on confidence, there is not enough confidence in the financial system to supply the world with the money it needs. Since the initial credit crisis struck in 2008, credit and money have been withdrawn from the system in such staggering amounts that international trade can no longer grow. The world’s central banks are playing a rear guard action by acting as lender of last resort to banks that no longer trust each other and have stopped lending in the interbank market. As liquidity flows out from the system, the rottenness that has corrupted the foundations of global finance is now exposed for all to see. This was especially evident in the bankruptcy of MF Global. For over 100 years the futures exchanges have bragged that no customer on an exchange has lost money due to a broker-dealer’s default. No longer. This is how confidence is lost in the financial system – investors are surprised by large losses from institutions or products thought to be impregnable. When confidence in the financial system is lost, people don’t trust their money to banks nor to the financial markets. Banks in turn don’t trust their money to anybody but the safest of risks. You then have the making of a large-scale financial collapse, particularly at a time like this, when the world’s economy is heavily dependent on ever-increasing amounts of debt. Since the new debt is essential to repaying the old debt, old debts turn into a default, and as one default leads to another, an economic depression ensues. Credit becomes scarce, and so money disappears. The question is: How will this play out?

The Great Ricardian Equivalence Debate of 2011: Do Mainstream Economists Agree on Anything? - Krugman started it, in response to Lucas. Everyone piles on. Plutocracy Files has the list of links. (Plus don't miss Nick Rowe's, which includes a long comment thread.) Here's what wows me: all these world-classical economists are accusing each other of contradicting "textbook economics," and circling through extraordinary contortions in their efforts to reconcile that school of economics with some version of reality. There is no consensus. None. Every one of these folks is bought into classical assumptions, or at least into the Keynesian/classical "synthesis" that's embodied in the IS-LM model (a model that was created explicitly to render Keynes classical, i.e. without the the Keynes, and was later disavowed by its own creator, John Hicks, as nothing more than a "classroom gadget"). And they're all trying to do intergenerational macro in their heads, as a bunch of stylized and simplified thought experiments. Given that several of the world's most notable "textbook" economists can't agree on how to define what in physics would be the equivalent of angular momentum, some of us have to wonder if the whole discipline as taught today offers any useful macro-level insight or modeling utility at all.

US Closes 2011 With Record $15.22 Trillion In Debt, Officially At 100.3% Debt/GDP, $14 Billion From Breaching Debt Ceiling - While not news to Zero Hedge readers who knew about the final debt settlement of US debt about 10 days ahead of schedule, it is now official: according to the US Treasury, America has closed the books on 2011 with debt at an all time record $15,222,940,045,451.09. And, as was observed here first in all of the press, US debt to GDP is now officially over 100%, or 100.3% to be specific, a fact which the US government decided to delay exposing until the very end of the calendar year. We wonder, rhetorically, just how prominent of a talking point this historic event will be in any upcoming GOP primary debates. And yes, technically this number is greater than the debt ceiling but it excludes various accounting gimmicks. When accounting for those, the US has a debt ceiling buffer of... $14 billion, or one third the size of a typical bond auction.

The True Federal Debt - In our personal lives, we all understand that debts may take different forms. They aren’t limited only to credit cards or loans taken out from banks; they consist of various promises and financial obligations as well. These might include commitments to pay for a daughter’s wedding or a child’s graduate school education, to provide the down payment on a sibling’s house or to care for aged parents. While these debts may not show up on anyone’s formal balance sheet, families are well aware of them, and failure to live up to them can be very costly indeed. So, too, with the federal government. The national debt, which is the object of almost obsessive attention these days, is like a bank loan. It is an important part of national indebtedness, but only a small part. The vast bulk of the true debt is in the form of commitments to pay future benefits to retired federal employees, veterans, and Social Security and Medicare beneficiaries. These commitments are generally invisible because the federal government operates on a cash basis. The federal budget is concerned only with income and outgo between two points in time — from Oct. 1 to Sept. 30, the fiscal year. Promises to pay benefits in the future generally show up in the budget only when those benefits are actually paid.

Nobody Understands Debt, by Paul Krugman - In 2011, as in 2010, America was in a technical recovery but continued to suffer from disastrously high unemployment. And through most of 2011, as in 2010, almost all the conversation in Washington was about something else: the allegedly urgent issue of reducing the budget deficit. This misplaced focus said a lot about our political culture, in particular about how disconnected Congress is from the suffering of ordinary Americans. But it also revealed something else: when people in D.C. talk about deficits and debt, by and large they have no idea what they’re talking about — and the people who talk the most understand the least. Deficit-worriers portray a future in which we’re impoverished by the need to pay back money we’ve been borrowing. They see America as being like a family that took out too large a mortgage, and will have a hard time making the monthly payments. This is, however, a really bad analogy in at least two ways. First, families have to pay back their debt. Governments don’t — all they need to do is ensure that debt grows more slowly than their tax base. The debt from World War II was never repaid; it just became increasingly irrelevant as the U.S. economy grew, and with it the income subject to taxation. Second — and this is the point almost nobody seems to get — an over-borrowed family owes money to someone else; U.S. debt is, to a large extent, money we owe to ourselves.

US Net Investment Income - Krugman - I’ve been arguing that the nature of US debt now is not, despite appearances, all that different from debt post-World War 2, when we pretty much entirely owed the money to ourselves. Now, of course, some of the money is owed to foreigners; but as I pointed out, America has large assets abroad, not too much less than its liabilities. But wait, there’s more. American assets. often taking the form of foreign subsidiaries of US corporations, earn a higher rate of return than US liabilities — especially now, when there’s a lot of foreign money parked in Treasuries, but this was true even before the crisis. As a result, income from US-owned assets abroad — the blue line below — consistently exceeds payments on foreign-owned assets in the United States, the red line: Again, if your image is that we’re deeply in hock to foreigners, that our extravagance has condemned us to a future of debt peonage, you’re wrong.